Hydrogen Storage Tank Market

Hydrogen Storage Tank Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705426 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

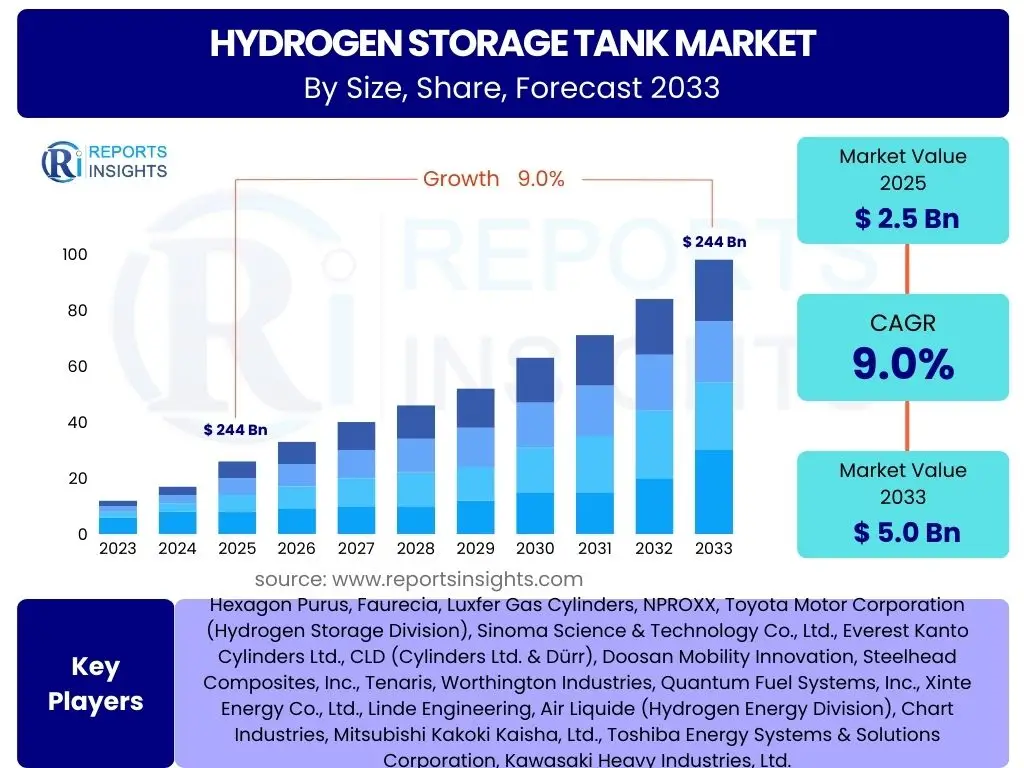

Hydrogen Storage Tank Market Size

According to Reports Insights Consulting Pvt Ltd, The Hydrogen Storage Tank Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.0% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 5.0 Billion by the end of the forecast period in 2033.

Key Hydrogen Storage Tank Market Trends & Insights

The hydrogen storage tank market is undergoing significant transformation, driven by advancements in materials science and increasing global focus on clean energy. Users frequently inquire about the latest technological innovations, the shift towards higher-pressure storage, and the integration of hydrogen across diverse applications. A key trend is the growing prominence of Type IV composite tanks, offering lighter weight and enhanced safety features for automotive and portable applications. This innovation addresses critical concerns regarding efficiency and range, directly influencing market adoption rates.

Another prevalent trend involves the expanding investment in hydrogen infrastructure globally, including the development of large-scale storage solutions for industrial and energy grid applications. This infrastructure build-out is critical for facilitating the broader adoption of hydrogen as an energy carrier. Furthermore, there is a marked increase in research and development efforts focused on solid-state hydrogen storage and liquid organic hydrogen carriers (LOHC), aiming to overcome current limitations related to storage density and cost, thereby unlocking new market opportunities and addressing long-term energy transition goals.

- Advancements in Type IV composite tank technology for lightweight and high-pressure storage.

- Increased investment in global hydrogen production, distribution, and storage infrastructure.

- Growing adoption of hydrogen fuel cell electric vehicles (FCEVs) and industrial applications.

- Development of innovative storage methods like liquid hydrogen and metal hydrides.

- Emphasis on enhanced safety standards and regulatory harmonization across regions.

AI Impact Analysis on Hydrogen Storage Tank

Users are increasingly curious about how artificial intelligence (AI) can revolutionize the hydrogen storage tank sector, specifically questioning its role in optimizing design, ensuring safety, and improving operational efficiency. AI is poised to significantly enhance the design and manufacturing processes of hydrogen storage tanks. Through advanced simulation and predictive modeling, AI algorithms can analyze vast datasets of material properties, structural integrity, and failure modes, enabling engineers to design tanks that are not only lighter and stronger but also safer and more cost-effective. This data-driven approach accelerates the R&D cycle, allowing for rapid iteration and optimization of tank geometries and composite layering.

Beyond design, AI contributes significantly to the operational aspects and safety monitoring of hydrogen storage systems. AI-powered sensors and real-time analytics can continuously monitor tank performance, detect anomalies, and predict potential failures before they occur, thus facilitating proactive maintenance and mitigating risks. Furthermore, AI optimizes filling and dispensing operations by predicting demand patterns and managing pressure levels, leading to increased efficiency and reduced energy consumption. This integration of AI across the lifecycle of hydrogen storage tanks is crucial for building a resilient and safe hydrogen economy, addressing key user concerns about reliability and operational costs.

- AI-driven optimization of tank design for improved material efficiency, strength, and safety.

- Predictive maintenance and real-time monitoring of tank health and performance using AI analytics.

- Enhanced operational efficiency in hydrogen filling and dispensing processes through AI algorithms.

- Accelerated research and development of new storage materials and methods via AI-powered simulations.

- Improved risk assessment and safety protocols using AI to analyze operational data and incident patterns.

Key Takeaways Hydrogen Storage Tank Market Size & Forecast

The hydrogen storage tank market is poised for robust expansion, reflecting global commitments to decarbonization and the increasing viability of hydrogen as a clean energy vector. Users frequently seek concise insights into the market's growth drivers, segment leadership, and the overarching implications of its forecast. A primary takeaway is the market's strong growth trajectory, driven by surging demand from the transportation sector, particularly fuel cell electric vehicles (FCEVs), and growing industrial applications, alongside the nascent but significant role of hydrogen in grid-scale energy storage. This multifaceted demand underpins a positive long-term outlook for the market.

Furthermore, the forecast highlights the critical role of technological innovation, especially in composite materials and advanced manufacturing techniques, which are enabling higher storage densities and improved safety profiles. This innovation is pivotal in overcoming existing cost and performance barriers. Regions with proactive hydrogen strategies and supportive regulatory frameworks, such as parts of Asia Pacific, Europe, and North America, are expected to lead market adoption. The consistent upward trend in investment in hydrogen infrastructure globally further solidifies the market's growth potential and its central role in the broader energy transition.

- The market is experiencing substantial growth, primarily fueled by global decarbonization efforts.

- Automotive and industrial sectors are key drivers of demand for hydrogen storage tanks.

- Technological advancements in composite materials and high-pressure storage are critical enablers.

- Increased governmental support and investment in hydrogen infrastructure are accelerating market expansion.

- The long-term outlook remains highly positive, with significant opportunities in diverse end-use applications.

Hydrogen Storage Tank Market Drivers Analysis

The hydrogen storage tank market is propelled by a confluence of powerful drivers, primarily stemming from the urgent global imperative to transition towards clean energy sources. The escalating focus on reducing carbon emissions and achieving net-zero targets by various nations and industries has positioned hydrogen as a cornerstone of future energy systems. This has led to substantial investments in hydrogen production, transportation, and particularly storage infrastructure, as efficient and safe storage is paramount for hydrogen's widespread adoption across different sectors, from transportation to industrial processes and power generation.

Moreover, the rapid growth in the adoption of fuel cell electric vehicles (FCEVs) across automotive, bus, and heavy-duty transportation segments is significantly boosting the demand for high-pressure, lightweight hydrogen storage tanks. Governments worldwide are implementing supportive policies, offering incentives, and funding research and development initiatives for hydrogen technologies, including storage. This regulatory and financial support fosters an environment conducive to market expansion, enabling technological advancements and cost reductions that further accelerate the integration of hydrogen into the global energy mix, creating a robust demand for advanced storage solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Initiatives | +2.5% | Global, particularly Europe, Asia Pacific, North America | 2025-2033 |

| Growth in Fuel Cell Electric Vehicles (FCEVs) | +2.0% | Japan, South Korea, China, Germany, California (USA) | 2025-2033 |

| Expanding Hydrogen Infrastructure Projects | +1.8% | Europe, North America, Middle East, Australia | 2026-2033 |

| Government Policies and Incentives for Hydrogen | +1.5% | EU, USA, Japan, South Korea, China | 2025-2030 |

Hydrogen Storage Tank Market Restraints Analysis

Despite the optimistic outlook, the hydrogen storage tank market faces several significant restraints that could impede its growth trajectory. One of the primary barriers is the high initial capital expenditure required for setting up hydrogen storage infrastructure, including the cost of advanced tanks, refueling stations, and associated safety systems. This high upfront investment can be prohibitive for smaller players and can delay large-scale deployment, especially in regions with limited financial incentives or nascent hydrogen economies. The complex and specialized manufacturing processes for high-pressure composite tanks also contribute to their elevated production costs, impacting overall market accessibility.

Furthermore, safety concerns and regulatory complexities surrounding hydrogen storage pose considerable challenges. Hydrogen, being highly flammable and explosive, requires stringent safety protocols for its handling, transportation, and storage. The lack of fully harmonized international standards and diverse regional regulations can create compliance hurdles for manufacturers and operators, leading to delays and increased operational costs. Public perception issues, often fueled by historical incidents, can also hinder the widespread acceptance of hydrogen technologies, necessitating extensive public education and robust safety assurances to overcome these perception barriers and encourage broader adoption across various end-use applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Costs of Storage Solutions | -1.5% | Global, especially emerging markets | 2025-2030 |

| Stringent Safety Regulations and Concerns | -1.2% | Global, particularly densely populated areas | 2025-2033 |

| Limited Hydrogen Refueling Infrastructure | -1.0% | Global, especially North America, developing APAC | 2025-2028 |

| Technical Challenges in Achieving High Storage Density | -0.8% | Global R&D focused regions | 2025-2033 |

Hydrogen Storage Tank Market Opportunities Analysis

The hydrogen storage tank market presents numerous compelling opportunities for growth, driven by ongoing technological innovation and the expanding scope of hydrogen applications. Significant advancements in materials science, particularly in the development of lightweight composite materials and new storage methods like metal hydrides and liquid organic hydrogen carriers (LOHCs), promise to enhance storage efficiency, reduce costs, and improve safety. These innovations are critical for addressing the inherent challenges of hydrogen storage, opening avenues for more compact, durable, and cost-effective tanks that can be deployed across a wider array of applications, thereby expanding the overall market reach and commercial viability.

Furthermore, the burgeoning interest in green hydrogen production—hydrogen produced using renewable energy sources—creates a substantial opportunity for large-scale, stationary hydrogen storage. This is particularly relevant for grid-scale energy storage, where hydrogen can serve as a long-duration solution to balance intermittent renewable energy supply. New end-use applications in sectors such as aviation, marine transport, and heavy industry are also emerging, which require specialized and high-capacity storage solutions. These diverse and expanding application areas, coupled with the potential for international collaborations and supportive policy frameworks for renewable hydrogen, represent significant growth prospects for manufacturers and developers in the hydrogen storage tank market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Material Science & Storage Technologies | +2.0% | Global, especially R&D hubs in Europe, North America, Japan | 2026-2033 |

| Growing Investment in Green Hydrogen Production | +1.8% | Europe, Middle East, Australia, North America | 2025-2033 |

| Emergence of New End-Use Applications (e.g., Aviation, Marine) | +1.5% | Global, focused on specialized industrial sectors | 2027-2033 |

| Cross-Sectoral Collaborations and Partnerships | +1.0% | Global | 2025-2030 |

Hydrogen Storage Tank Market Challenges Impact Analysis

The hydrogen storage tank market is confronted by several critical challenges that require innovative solutions and concerted efforts from stakeholders. One significant hurdle is the high production cost of advanced composite tanks, particularly Type IV, which relies on expensive materials like carbon fiber. This cost factor can limit widespread adoption, especially in price-sensitive markets or for applications where hydrogen solutions must compete directly with established fossil fuel alternatives. Scaling up manufacturing processes to meet anticipated demand while simultaneously driving down unit costs remains a complex technical and economic challenge for the industry, necessitating significant capital investment and process optimization.

Furthermore, challenges related to public acceptance and the perception of hydrogen safety persist. Despite advancements in safety protocols and tank design, historical incidents and a general lack of understanding about hydrogen's properties can lead to public apprehension, affecting infrastructure development and the adoption of hydrogen-powered vehicles. Establishing widely accepted and interoperable standards for hydrogen tank design, testing, and refueling infrastructure across different regions also poses a significant challenge. The absence of such harmonization can fragment the market, complicate international trade, and slow down the global deployment of hydrogen technologies, making it harder to achieve economies of scale and integrate hydrogen into diverse energy ecosystems efficiently.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs of Advanced Tanks | -1.5% | Global, particularly manufacturing hubs | 2025-2030 |

| Public Acceptance and Safety Perception | -1.2% | Global, especially urban areas and new markets | 2025-2033 |

| Interoperability and Standardization Issues | -1.0% | Global, affecting trade and infrastructure build-out | 2025-2029 |

| Competition from Alternative Energy Storage Solutions | -0.8% | Global energy sector | 2025-2033 |

Hydrogen Storage Tank Market - Updated Report Scope

This comprehensive market insights report offers an in-depth analysis of the Hydrogen Storage Tank Market, meticulously covering its historical evolution, current landscape, and future projections. The scope encompasses detailed segmentation by tank type, material, pressure, and diverse end-use applications, providing a holistic view of market dynamics. It integrates qualitative assessments of market drivers, restraints, opportunities, and challenges, along with a quantitative forecast of market size and growth trajectories across key regions, offering strategic insights for stakeholders. The report aims to deliver actionable intelligence, enabling businesses to navigate market complexities and capitalize on emerging trends within the global hydrogen economy.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 5.0 Billion |

| Growth Rate | 9.0% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hexagon Purus, Faurecia, Luxfer Gas Cylinders, NPROXX, Toyota Motor Corporation (Hydrogen Storage Division), Sinoma Science & Technology Co., Ltd., Everest Kanto Cylinders Ltd., CLD (Cylinders Ltd. & Dürr), Doosan Mobility Innovation, Steelhead Composites, Inc., Tenaris, Worthington Industries, Quantum Fuel Systems, Inc., Xinte Energy Co., Ltd., Linde Engineering, Air Liquide (Hydrogen Energy Division), Chart Industries, Mitsubishi Kakoki Kaisha, Ltd., Toshiba Energy Systems & Solutions Corporation, Kawasaki Heavy Industries, Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The hydrogen storage tank market is meticulously segmented to provide a granular understanding of its diverse facets, reflecting the varied technological approaches and end-use requirements across the globe. This segmentation is crucial for identifying distinct market niches, understanding specific demand drivers, and assessing the competitive landscape within each sub-category. Segmentation by tank type, such as Type I (all-metal), Type II (hoop-wrapped), Type III (fully wrapped composite with metal liner), and Type IV (fully wrapped composite with plastic liner), highlights the progression in design towards lighter, more efficient, and safer storage solutions, with Type IV tanks emerging as a dominant choice for high-pressure applications in mobility due to their superior gravimetric efficiency.

Further segmentation by material, including steel, aluminum, carbon fiber composites, and hybrid composites, underscores the material science innovations driving the market. Carbon fiber composites, for instance, are critical for high-pressure Type III and Type IV tanks. Pressure-based segmentation (low, medium, high) categorizes tanks based on their operational pressure, catering to different applications, from stationary industrial storage to high-pressure vehicular applications. Application-based segmentation across automotive, industrial, energy storage, aerospace, and marine sectors reveals distinct market demands and regulatory environments, offering insights into where growth opportunities are most pronounced and where specific technological adaptations are required to meet stringent industry standards.

- By Type:

- Type I

- Type II

- Type III

- Type IV

- Liquid Hydrogen Tanks

- Metal Hydride Tanks

- By Material:

- Steel

- Aluminum

- Carbon Fiber Composites

- Glass Fiber Composites

- Hybrid Composites

- By Pressure:

- Low-Pressure Tanks (<200 bar)

- Medium-Pressure Tanks (200-500 bar)

- High-Pressure Tanks (>500 bar)

- By Application:

- Automotive (Passenger Vehicles, Commercial Vehicles)

- Industrial (Chemical, Refining, Metals, Electronics)

- Energy Storage (Grid-Scale, Renewable Integration)

- Aerospace & Defense

- Marine

- Portable & Consumer Electronics

- Others

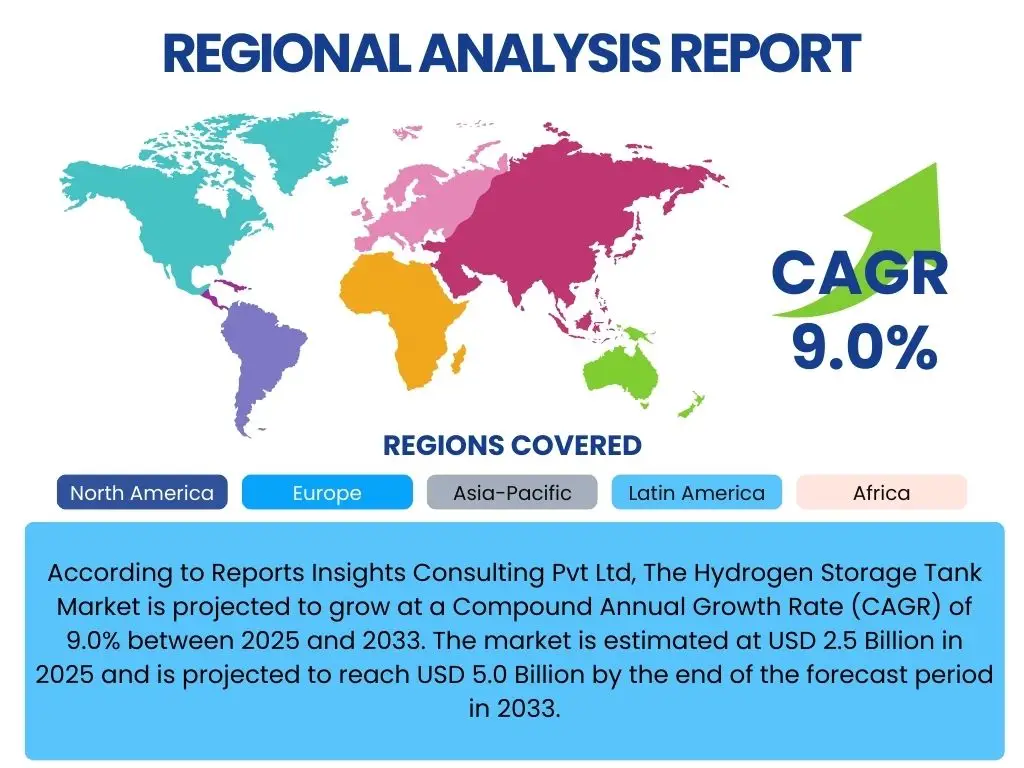

Regional Highlights

The global hydrogen storage tank market exhibits significant regional variations, influenced by differing energy policies, economic development, and hydrogen adoption strategies. Each region presents unique growth drivers, challenges, and opportunities, shaping its contribution to the overall market. Asia Pacific, particularly countries like Japan, South Korea, and China, stands out as a leading region due to aggressive governmental initiatives to establish hydrogen economies, substantial investments in fuel cell technology, and a large manufacturing base. This region is witnessing rapid deployment of FCEVs and the development of extensive hydrogen infrastructure for industrial and transportation applications, driving robust demand for various storage solutions, especially high-pressure composite tanks.

Europe is another pivotal region, driven by ambitious decarbonization targets set by the European Union and its member states, coupled with significant investments in green hydrogen production and related infrastructure under the European Green Deal. Countries like Germany, France, and the Netherlands are at the forefront of developing hydrogen corridors and increasing the adoption of hydrogen in industrial processes and heavy-duty transport, fostering demand for both stationary and mobile storage solutions. North America, propelled by initiatives in the United States and Canada focusing on clean hydrogen hubs and tax incentives, is seeing increasing interest and investment, particularly in California for FCEVs and in industrial applications. The Middle East and Africa, along with Latin America, represent emerging markets with vast potential for green hydrogen production and export, which will necessitate significant investment in large-scale storage technologies in the long term, though their current adoption is comparatively nascent.

- North America: Strong emphasis on R&D, growing FCEV adoption (especially California), and increasing industrial hydrogen demand driven by federal incentives and clean energy goals.

- Europe: Leading global efforts in green hydrogen development, substantial policy support (e.g., European Hydrogen Strategy), and widespread integration of hydrogen in industrial and mobility sectors, fostering demand for advanced storage.

- Asia Pacific (APAC): Dominates in hydrogen technology adoption, particularly in Japan, South Korea, and China, with significant investments in FCEV deployment, industrial hydrogen use, and robust governmental support for building a hydrogen-based society.

- Latin America: Emerging region with vast renewable energy potential, fostering early-stage green hydrogen projects, primarily for export, indicating future demand for large-scale storage solutions.

- Middle East and Africa (MEA): Positioning itself as a future hub for green hydrogen production and export due to abundant solar and wind resources, necessitating development of large-scale, cost-effective hydrogen storage infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrogen Storage Tank Market.- Hexagon Purus

- Faurecia

- Luxfer Gas Cylinders

- NPROXX

- Toyota Motor Corporation

- Sinoma Science & Technology Co., Ltd.

- Everest Kanto Cylinders Ltd.

- CLD (Cylinders Ltd. & Dürr)

- Doosan Mobility Innovation

- Steelhead Composites, Inc.

- Tenaris

- Worthington Industries

- Quantum Fuel Systems, Inc.

- Xinte Energy Co., Ltd.

- Linde Engineering

- Air Liquide

- Chart Industries

- Mitsubishi Kakoki Kaisha, Ltd.

- Toshiba Energy Systems & Solutions Corporation

- Kawasaki Heavy Industries, Ltd.

Frequently Asked Questions

Analyze common user questions about the Hydrogen Storage Tank market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary types of hydrogen storage tanks?

Hydrogen storage tanks are primarily categorized into Type I (all-metal), Type II (hoop-wrapped metal liner), Type III (fully wrapped composite with metal liner), and Type IV (fully wrapped composite with plastic liner). Additionally, liquid hydrogen tanks and metal hydride tanks represent distinct storage technologies.

How does the hydrogen storage tank market contribute to decarbonization goals?

The hydrogen storage tank market is crucial for decarbonization by enabling the safe and efficient storage of hydrogen, which serves as a clean energy carrier. This facilitates the adoption of fuel cell electric vehicles and supports the integration of renewable energy through grid-scale hydrogen storage, significantly reducing reliance on fossil fuels.

What are the main challenges in developing hydrogen storage technologies?

Key challenges include achieving high storage density at ambient conditions, reducing the high manufacturing costs of advanced tanks, ensuring stringent safety standards, establishing a comprehensive refueling infrastructure, and overcoming public perception issues related to hydrogen safety and adoption.

Which industries are the key end-users for hydrogen storage tanks?

The primary end-user industries include automotive (for fuel cell electric vehicles), industrial applications (e.g., chemical, refining, metals), energy storage (for grid balancing and renewable energy integration), aerospace & defense, and increasingly, marine transportation.

How is artificial intelligence impacting hydrogen storage tank design and operations?

Artificial intelligence is impacting hydrogen storage tank design through optimized material selection and structural simulations, leading to lighter and stronger tanks. In operations, AI enhances safety through predictive maintenance, real-time monitoring, and optimizing filling/dispensing processes, improving overall efficiency and reliability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted