Hydrogen Fuel Cell Stack Market

Hydrogen Fuel Cell Stack Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708612 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

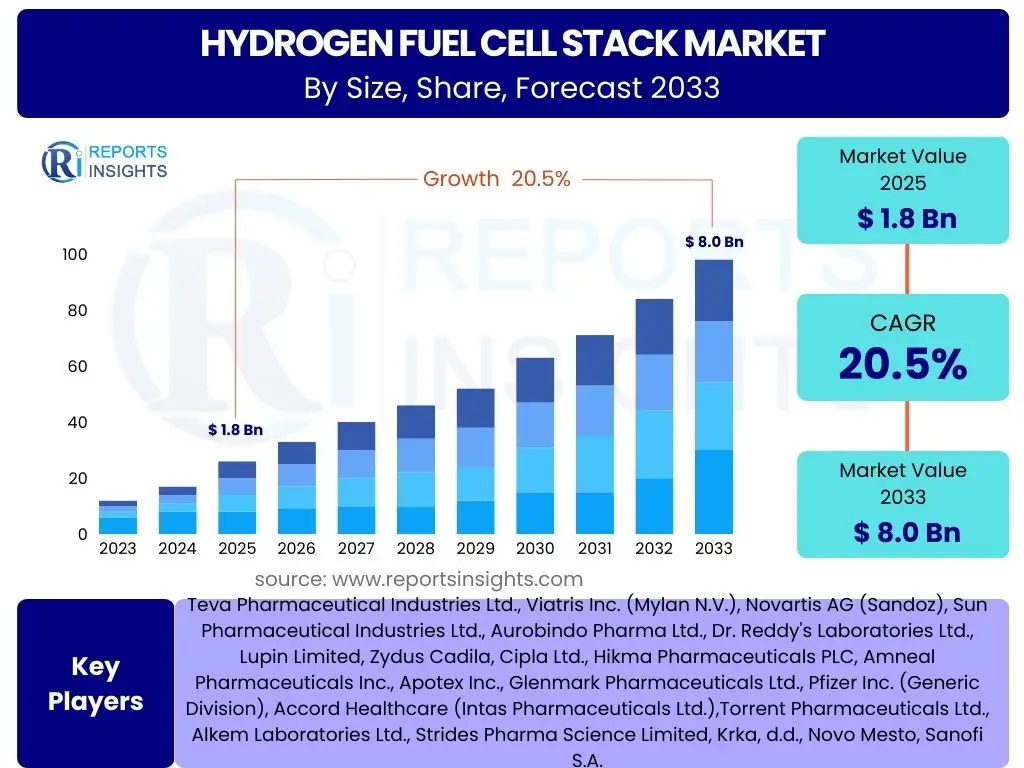

Hydrogen Fuel Cell Stack Market Size

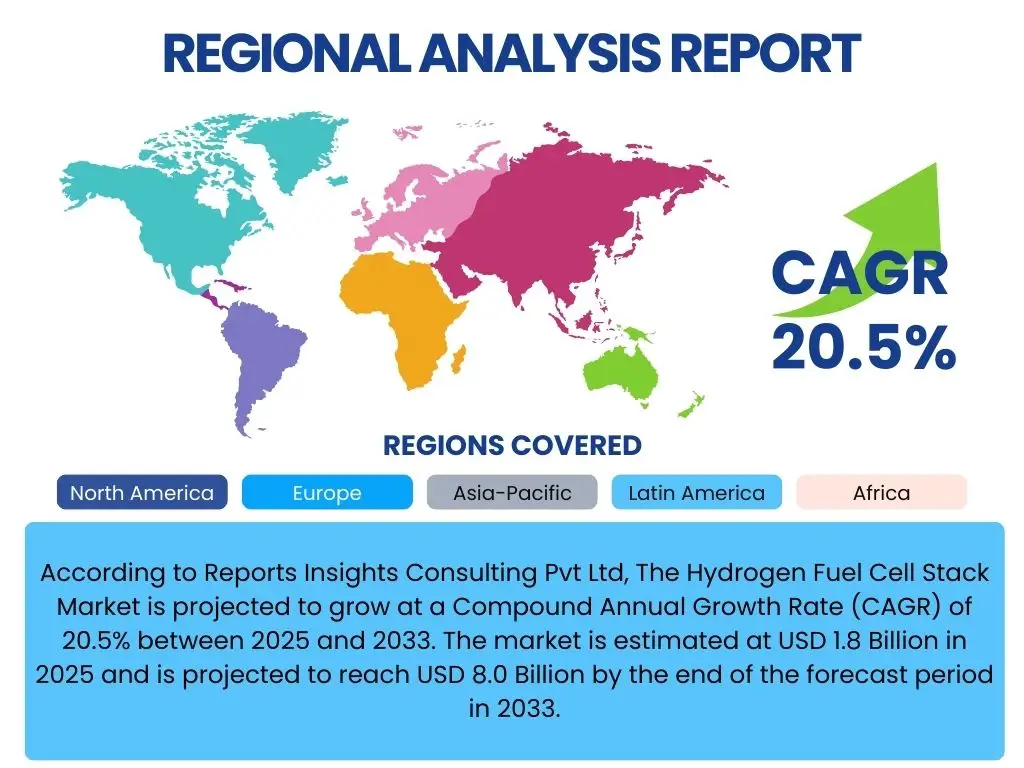

According to Reports Insights Consulting Pvt Ltd, The Hydrogen Fuel Cell Stack Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.5% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 8.0 Billion by the end of the forecast period in 2033.

Key Hydrogen Fuel Cell Stack Market Trends & Insights

The Hydrogen Fuel Cell Stack Market is undergoing a transformative period, driven by an escalating global emphasis on decarbonization and sustainable energy solutions. Common inquiries reveal significant interest in the long-term viability and practical applications of hydrogen technology. Stakeholders are particularly keen on understanding how policy frameworks, technological advancements, and economic factors converge to shape market dynamics. There is a strong focus on the evolution of fuel cell stack efficiency, durability, and manufacturing scalability, as these are critical for broader commercial adoption across various industries.

User questions frequently highlight the market's trajectory towards increased integration within heavy-duty transportation, such as trucks, buses, and maritime vessels, alongside its growing presence in stationary power generation for industrial facilities and critical infrastructure. The trend of linking hydrogen production to renewable energy sources, often termed green hydrogen, is a pivotal insight, indicating a future where the entire hydrogen value chain is environmentally sustainable. This integration is crucial for addressing climate change objectives and enhancing energy security, drawing considerable attention from both public and private sectors invested in the energy transition.

Another prominent area of interest concerns the continuous decline in manufacturing costs and the improvements in power density and operational lifespan of fuel cell stacks. These advancements are instrumental in making hydrogen fuel cell technology more competitive with traditional power sources and other alternative energy solutions. The market is also seeing a trend of increased standardization and modularization of fuel cell components, which simplifies design, manufacturing, and maintenance, thereby accelerating market penetration and reducing overall system costs. This focus on practical, scalable solutions is a recurring theme in market discourse.

- Accelerated decarbonization initiatives and government support for hydrogen economy development.

- Significant cost reduction in fuel cell stack manufacturing through economies of scale and advanced materials.

- Expanding application in heavy-duty transportation (trucks, buses, trains, maritime) and material handling.

- Increasing integration of fuel cell stacks with renewable energy sources for green hydrogen production and storage.

- Advancements in power density, efficiency, and durability leading to enhanced performance and longer operational lifespans.

- Growing demand for stationary power generation in remote areas, critical infrastructure, and data centers.

- Development of standardized and modular fuel cell stack designs simplifying integration and maintenance.

AI Impact Analysis on Hydrogen Fuel Cell Stack

The impact of Artificial Intelligence (AI) on the Hydrogen Fuel Cell Stack Market is a topic of increasing importance, frequently addressed in discussions regarding technological advancement and operational optimization. Users are often curious about how AI can accelerate the research and development cycle, improve the performance characteristics of fuel cell materials, and streamline complex manufacturing processes. The consensus suggests that AI's capabilities in data analysis and pattern recognition are pivotal for identifying novel catalyst materials, optimizing stack designs for higher efficiency, and predicting material degradation, thereby extending the lifespan of fuel cell components.

Furthermore, inquiries often delve into AI's role in enhancing the operational efficiency and reliability of existing fuel cell systems. Predictive maintenance, a key application of AI, is expected to revolutionize how fuel cell stacks are monitored and serviced. By analyzing real-time sensor data, AI algorithms can identify potential failures before they occur, scheduling maintenance proactively and significantly reducing downtime and operational costs. This capability is particularly attractive for large-scale deployments in transportation fleets or stationary power plants where continuous operation is critical and any interruption can lead to substantial financial losses.

Beyond design and maintenance, AI is also anticipated to play a crucial role in optimizing the broader hydrogen ecosystem surrounding fuel cell stacks. This includes intelligent energy management systems that balance hydrogen supply and demand, optimize grid integration for stationary applications, and enhance the logistics of hydrogen storage and distribution. The ability of AI to process vast amounts of data from various sources – including weather patterns, energy prices, and operational metrics – allows for more efficient resource allocation and dynamic system adjustments, contributing to a more resilient and cost-effective hydrogen infrastructure. The application of AI spans the entire lifecycle of hydrogen fuel cell stacks, from initial design to end-of-life management.

- Accelerated material discovery and optimization for catalysts and membranes through AI-driven simulations and data analysis.

- Enhanced fuel cell stack design for improved power density, efficiency, and durability using AI for complex simulations and optimization algorithms.

- Predictive maintenance and fault diagnostics through AI analysis of operational data, minimizing downtime and extending service life.

- Optimization of manufacturing processes, quality control, and assembly through AI-powered robotics and vision systems.

- Intelligent energy management systems for fuel cell-powered applications, optimizing hydrogen consumption and power output.

- Improved supply chain logistics and inventory management for hydrogen and fuel cell components using AI-driven forecasting.

Key Takeaways Hydrogen Fuel Cell Stack Market Size & Forecast

The Hydrogen Fuel Cell Stack Market is poised for substantial expansion, with a robust Compound Annual Growth Rate indicating strong industry confidence and investment. A key takeaway for market participants is the fundamental shift towards hydrogen as a versatile energy carrier, driven by an urgent need for sustainable solutions across numerous sectors. The projected increase in market valuation underscores the growing acceptance and implementation of fuel cell technologies, moving beyond niche applications to becoming a mainstream component of global energy strategies. This growth is not merely incremental but represents a significant leap in technological maturity and commercial viability.

Another crucial insight is the multifaceted nature of the market's growth drivers, which include favorable government policies, significant private sector investment in hydrogen infrastructure, and continuous technological advancements. These elements collectively create an environment conducive to rapid development and adoption. The market's resilience and potential are further highlighted by its ability to address diverse energy needs, from powering heavy-duty transportation and providing backup power for critical facilities to enabling energy independence through distributed generation. This broad applicability positions fuel cell stacks as a cornerstone technology for the energy transition.

Ultimately, the market forecast reflects a clear trajectory towards a hydrogen-powered future, necessitating strategic planning and investment from all stakeholders. Businesses involved in manufacturing, research, infrastructure development, and end-use applications should recognize the imperative to innovate and scale operations to capitalize on this burgeoning opportunity. The sustained growth forecast emphasizes that the hydrogen fuel cell stack market is not a fleeting trend but a foundational element of the evolving global energy landscape, promising long-term opportunities for innovation and economic expansion.

- Significant market expansion with a projected CAGR of 20.5% from 2025 to 2033, reaching USD 8.0 Billion.

- Strong government support and private investments are propelling hydrogen as a critical energy vector for decarbonization.

- Technological advancements in efficiency, durability, and cost reduction are enhancing the commercial attractiveness of fuel cell stacks.

- Diverse applications in heavy-duty transport, stationary power, and industrial sectors are primary growth engines.

- The market is transitioning from early adoption to widespread commercial deployment, indicating maturing technology and infrastructure.

- Strategic partnerships and global collaborations are accelerating research, development, and market penetration.

Hydrogen Fuel Cell Stack Market Drivers Analysis

The Hydrogen Fuel Cell Stack Market is experiencing significant impetus from a convergence of global megatrends and strategic initiatives aimed at energy transition. A primary driver is the accelerating push for decarbonization across industries, driven by international climate agreements and national net-zero targets. Hydrogen, especially when produced from renewable sources (green hydrogen), offers a clean energy pathway, and fuel cell stacks are at the heart of converting this clean fuel into electricity without emissions. This environmental imperative is compelling governments and corporations worldwide to invest heavily in hydrogen technologies, thereby stimulating demand for fuel cell stacks.

Another crucial driver is the increasing focus on energy security and independence. Regions heavily reliant on fossil fuel imports are actively seeking diversified energy portfolios, and hydrogen presents a viable option for reducing this dependence. Fuel cell stacks enable the efficient use of domestically produced hydrogen, strengthening national energy grids and reducing vulnerability to geopolitical fluctuations. Furthermore, the decreasing cost of renewable energy, particularly solar and wind, is making green hydrogen production more economically attractive, which in turn reduces the operating cost of fuel cell applications and broadens their appeal across various sectors.

Technological advancements and economies of scale are also playing a pivotal role. Continuous innovation in materials science, manufacturing techniques, and stack design is leading to more efficient, durable, and cost-effective fuel cell stacks. As production volumes increase, manufacturing costs are declining, making hydrogen fuel cell solutions more competitive with conventional power sources and other clean energy alternatives. This economic viability, coupled with robust policy support through incentives, subsidies, and regulatory frameworks, is creating a fertile ground for market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Targets & Policies | +5.5% | Europe, North America, Asia Pacific | 2025-2033 (Long-term) |

| Increasing Investment in Hydrogen Infrastructure | +4.8% | Global, particularly Germany, Japan, US, China | 2025-2030 (Medium-term) |

| Falling Cost of Renewable Energy & Green Hydrogen Production | +4.2% | Global, especially regions with high renewable potential | 2026-2033 (Medium to Long-term) |

| Growing Demand for Zero-Emission Heavy-Duty Transport | +3.5% | Europe, North America, Japan, South Korea | 2025-2033 (Long-term) |

Hydrogen Fuel Cell Stack Market Restraints Analysis

Despite the promising growth trajectory, the Hydrogen Fuel Cell Stack Market faces several significant restraints that could impede its full potential. One of the primary barriers is the high initial capital expenditure associated with fuel cell systems and the broader hydrogen infrastructure. The cost of manufacturing fuel cell stacks, along with the expense of hydrogen production, storage, and distribution, remains higher compared to established fossil fuel technologies or even some battery-electric alternatives. This economic hurdle can deter potential adopters, particularly in industries where cost-efficiency is paramount and where the long-term total cost of ownership is not yet fully realized or universally accepted.

Another substantial restraint is the nascent stage of hydrogen infrastructure development. The lack of a widespread network for hydrogen refueling stations, especially for heavy-duty vehicles, and the limited availability of industrial-scale hydrogen supply chains create a "chicken and egg" problem. Without sufficient infrastructure, the adoption of fuel cell vehicles and stationary power systems is limited, and without significant demand, investment in infrastructure struggles to justify itself. This geographical and logistical constraint significantly impacts market penetration, particularly in regions where support for hydrogen initiatives is less concentrated or coordinated.

Furthermore, technical challenges related to hydrogen storage, safety perceptions, and the durability of fuel cell components continue to pose hurdles. While advancements are being made, issues such as the energy density of hydrogen storage, the perceived risks associated with handling gaseous hydrogen, and the long-term performance degradation of certain fuel cell components require ongoing research and development. Public awareness and acceptance also play a role; a lack of understanding regarding the safety and benefits of hydrogen technology can create apprehension and slow down adoption rates, necessitating comprehensive educational initiatives and robust safety standards.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Costs of Fuel Cell Systems & Infrastructure | -3.0% | Global, particularly developing economies | 2025-2028 (Short to Medium-term) |

| Limited Hydrogen Refueling & Distribution Infrastructure | -2.5% | Global, varying by region (less in Japan/Germany) | 2025-2030 (Medium-term) |

| Technical Challenges in Hydrogen Storage & Safety Perceptions | -1.8% | Global | 2025-2027 (Short-term) |

| Competition from Established Battery Electric Technologies | -1.5% | Automotive sector, especially light-duty vehicles | 2025-2033 (Long-term) |

Hydrogen Fuel Cell Stack Market Opportunities Analysis

The Hydrogen Fuel Cell Stack Market is brimming with opportunities stemming from the global imperative to transition to sustainable energy. One of the most significant opportunities lies in the expansion into new and underserved application areas. While heavy-duty transportation and stationary power are gaining traction, there is immense potential in niche markets such as maritime shipping, aviation, rail transport, and even portable power solutions for specialized equipment or remote locations. These sectors often require high power density, rapid refueling, and zero emissions, characteristics where fuel cell technology holds a distinct advantage over battery-electric alternatives, thus opening up substantial new revenue streams and market segments.

The accelerating development and scaling of green hydrogen production offer another monumental opportunity. As renewable energy costs continue to fall and electrolysis technologies improve, the ability to produce hydrogen with near-zero carbon emissions becomes more economically viable. This ensures a sustainable supply of fuel for fuel cell stacks, enhancing the overall environmental credentials of hydrogen solutions and appealing to an increasingly environmentally conscious consumer base and regulatory environment. Investments in large-scale green hydrogen projects, coupled with improved distribution networks, will significantly boost the demand and feasibility of fuel cell stack deployments.

Furthermore, the opportunity for technological breakthroughs and continuous innovation remains strong. Advancements in material science, catalyst development, and manufacturing processes can lead to even more efficient, durable, and cost-effective fuel cell stacks. Research into alternative fuel cell chemistries and novel stack designs could unlock new performance benchmarks and reduce dependence on critical raw materials. Additionally, the development of integrated energy systems that combine fuel cells with other renewable technologies, such as solar or wind, for grid balancing and resilient power supply, presents a compelling market opportunity for comprehensive energy solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Verticals (Maritime, Aviation, Rail) | +4.0% | Global | 2028-2033 (Long-term) |

| Scaling of Green Hydrogen Production & Supply Chains | +3.7% | Global, particularly Europe, Middle East, Australia | 2026-2033 (Medium to Long-term) |

| Technological Advancements in Stack Materials and Efficiency | +3.2% | Global R&D Hubs (Japan, US, Germany, South Korea) | 2025-2033 (Long-term) |

| Emergence of Developing Markets for Sustainable Energy Solutions | +2.8% | India, Brazil, Southeast Asia, parts of Africa | 2027-2033 (Long-term) |

Hydrogen Fuel Cell Stack Market Challenges Impact Analysis

The Hydrogen Fuel Cell Stack Market, while promising, contends with several notable challenges that require concerted effort from industry, government, and research institutions. One significant challenge is the establishment of a robust and economically viable hydrogen supply chain. This encompasses everything from the efficient and low-cost production of hydrogen to its storage, transportation, and final distribution to end-users. The current infrastructure is fragmented and insufficient for widespread adoption, particularly for green hydrogen, which often requires significant investment in electrolyzers and renewable energy sources. Overcoming these logistical and economic hurdles is critical for sustained market growth.

Another substantial challenge is achieving cost parity with established conventional and alternative energy technologies. While fuel cell stack costs are declining, they still face intense competition from mature internal combustion engine technologies, as well as increasingly competitive battery-electric solutions, especially in lighter-duty applications. Reducing the capital cost of the fuel cell stack itself, along with the balance of plant components, and the operational cost of hydrogen fuel, is paramount. This requires continued innovation in materials science, manufacturing techniques, and scaling up production to achieve economies of scale necessary for broader market acceptance.

Furthermore, regulatory complexities and the need for international standardization present another set of challenges. Developing harmonized safety standards, certification processes, and deployment regulations for hydrogen infrastructure and fuel cell systems across different regions and countries is crucial for facilitating cross-border trade and accelerating global adoption. The lack of consistent regulatory frameworks can create uncertainty for investors and hinder the rapid deployment of new technologies. Addressing these challenges effectively will require collaborative efforts and long-term strategic planning to build a resilient and competitive hydrogen fuel cell ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Developing Economically Viable Green Hydrogen Supply Chains | -2.8% | Global | 2025-2030 (Medium-term) |

| Achieving Cost Parity with Conventional and Battery Technologies | -2.2% | Global | 2025-2029 (Short to Medium-term) |

| Establishing Standardized Safety Regulations & Certifications | -1.9% | Global, varying by region | 2025-2033 (Long-term) |

| Managing Perceived Risks & Public Acceptance of Hydrogen | -1.5% | Global | 2025-2027 (Short-term) |

Hydrogen Fuel Cell Stack Market - Updated Report Scope

This report provides a comprehensive analysis of the Hydrogen Fuel Cell Stack Market, offering in-depth insights into its current state, future growth trajectories, and key influencing factors. It covers market size estimations, forecast projections, and a detailed examination of market trends, drivers, restraints, opportunities, and challenges. The scope includes a thorough segmentation analysis by various parameters, an assessment of regional dynamics, and profiles of leading market participants, ensuring a holistic view of the market landscape and its potential evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 8.0 Billion |

| Growth Rate | 20.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ballard Power Systems, Plug Power Inc., Ceres Power Holdings plc, FuelCell Energy, Inc., Doosan Fuel Cell America, Inc., Symbio (Michelin & Forvia), Hyundai Mobis, Toyota Motor Corporation, Honda Motor Co., Ltd., Nuvera Fuel Cells, Advent Technologies Holdings, Inc., PowerCell Sweden AB, Nedstack Fuel Cell Technology B.V., Horizon Fuel Cell Technologies, SFC Energy AG, Intelligent Energy Limited, Dana Limited, Cummins Inc., Bosch, Siemens Energy AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Hydrogen Fuel Cell Stack Market is segmented to provide a granular understanding of its diverse components and growth avenues. This segmentation allows for targeted analysis of different technologies, applications, and end-use industries, revealing specific market dynamics and investment opportunities within each category. The inherent versatility of fuel cell technology permits its classification across several dimensions, reflecting the varied requirements of different sectors and consumer needs. This structured breakdown is essential for stakeholders to identify high-growth areas and tailor their strategies accordingly.

Key segmentation categories include the type of fuel cell technology, such as Polymer Electrolyte Membrane Fuel Cells (PEMFC) and Solid Oxide Fuel Cells (SOFC), each with distinct operating characteristics and suitability for specific applications. For instance, PEMFCs are favored in transportation due to their quick start-up and high power density, while SOFCs excel in stationary power generation where high efficiency and fuel flexibility are paramount. Analyzing these segments helps in understanding the technological preferences and market adoption rates across various end-uses, highlighting the innovation focus within the industry.

Furthermore, segmentation by application, power output, and end-use industry provides critical insights into market demand and growth drivers. The transportation segment, particularly heavy-duty vehicles, is a significant consumer, but stationary power and portable power applications are also experiencing robust growth. Understanding the power output requirements helps manufacturers design appropriate stack configurations, while end-use industry segmentation identifies the primary sectors driving adoption. This detailed analysis is vital for strategic planning, product development, and market entry strategies, ensuring that products align with specific market needs and opportunities.

- By Type: Polymer Electrolyte Membrane Fuel Cell (PEMFC), Solid Oxide Fuel Cell (SOFC), Alkaline Fuel Cell (AFC), Phosphoric Acid Fuel Cell (PAFC), Molten Carbonate Fuel Cell (MCFC), Direct Methanol Fuel Cell (DMFC), Others

- By Application: Transportation (Passenger Vehicles, Commercial Vehicles (Buses, Trucks, Forklifts), Maritime, Rail, Aerospace), Stationary Power (Backup Power, Combined Heat & Power (CHP), Primary Power), Portable Power (Consumer Electronics, Military & Defense, Remote Monitoring)

- By Power Output: Below 1 kW, 1 kW - 10 kW, 10 kW - 50 kW, Above 50 kW

- By End-Use Industry: Automotive, Logistics & Material Handling, Energy & Utilities, Telecommunications, Industrial, Marine, Aerospace, Others

Regional Highlights

The global Hydrogen Fuel Cell Stack Market exhibits distinct regional dynamics, influenced by varying policy environments, technological capabilities, and investment landscapes. Asia Pacific, particularly countries like Japan, South Korea, and China, stands out as a leading region due to significant government support, substantial R&D investments, and a strong manufacturing base. These nations have proactive national hydrogen strategies aimed at achieving energy security and reducing emissions, leading to early adoption in both transportation and stationary power applications. The robust industrial infrastructure and a large consumer market further solidify the region's prominent position in the fuel cell stack ecosystem.

Europe represents another key growth region, driven by ambitious decarbonization targets and comprehensive green hydrogen strategies laid out by the European Union and individual member states. Countries such as Germany, the Netherlands, and the UK are heavilyinvesting in hydrogen production, infrastructure development, and the deployment of fuel cell technologies across various sectors, including heavy-duty transport and industrial applications. The strong regulatory push, coupled with increasing public awareness and private sector commitment to sustainable solutions, positions Europe as a frontrunner in fostering a hydrogen economy, thus creating significant demand for fuel cell stacks.

North America, led by the United States and Canada, is also demonstrating substantial growth, propelled by federal and state-level incentives, a burgeoning private investment landscape, and advancements in renewable energy integration. The region is witnessing increased adoption in material handling (e.g., forklifts), commercial fleets, and stationary backup power. Latin America, the Middle East, and Africa (MEA) are emerging markets with considerable potential, driven by vast renewable energy resources for green hydrogen production and the need for reliable, off-grid power solutions. However, these regions often require further infrastructure development and investment to fully capitalize on their hydrogen fuel cell potential.

- North America: Strong government incentives, private investments, and growing adoption in material handling and heavy-duty vehicles; significant R&D in fuel cell technology.

- Europe: Ambitious decarbonization goals, comprehensive hydrogen strategies (e.g., European Hydrogen Strategy), and increasing deployment in transport, industrial, and stationary power applications.

- Asia Pacific (APAC): Leading market driven by strong government support in Japan, South Korea, and China; extensive manufacturing capabilities; high adoption rates in FCEVs and stationary power.

- Latin America: Emerging market with potential for green hydrogen production due to abundant renewable resources; growing interest in fuel cell applications for energy independence.

- Middle East & Africa (MEA): Significant potential for green hydrogen exports; increasing investment in clean energy projects; growing demand for off-grid and reliable power solutions using fuel cells.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrogen Fuel Cell Stack Market.- Ballard Power Systems

- Plug Power Inc.

- Ceres Power Holdings plc

- FuelCell Energy, Inc.

- Doosan Fuel Cell America, Inc.

- Symbio (Michelin & Forvia)

- Hyundai Mobis

- Toyota Motor Corporation

- Honda Motor Co., Ltd.

- Nuvera Fuel Cells

- Advent Technologies Holdings, Inc.

- PowerCell Sweden AB

- Nedstack Fuel Cell Technology B.V.

- Horizon Fuel Cell Technologies

- SFC Energy AG

- Intelligent Energy Limited

- Dana Limited

- Cummins Inc.

- Bosch

- Siemens Energy AG

Frequently Asked Questions

What is a hydrogen fuel cell stack?

A hydrogen fuel cell stack is the core component of a fuel cell system, consisting of multiple individual fuel cells layered together. Each cell converts chemical energy from hydrogen and oxygen into electrical energy through an electrochemical reaction, producing electricity, water, and heat, with no harmful emissions at the point of use. Stacks are designed to achieve the required voltage and power output for specific applications.

What drives the growth of the Hydrogen Fuel Cell Stack Market?

The market's growth is primarily driven by global decarbonization efforts, increasing government support and funding for hydrogen technologies, declining manufacturing costs through economies of scale, and expanding applications in heavy-duty transportation, stationary power generation, and material handling sectors. The push for energy security and the availability of green hydrogen also contribute significantly.

What are the main applications of hydrogen fuel cell stacks?

Hydrogen fuel cell stacks are predominantly used in transportation, including passenger vehicles, buses, trucks, forklifts, and increasingly in maritime and rail. They are also vital for stationary power generation (backup power, combined heat and power, primary power for remote sites) and portable power solutions for niche electronics and military applications.

What are the biggest challenges facing the market?

Major challenges include the high initial cost of fuel cell systems and associated infrastructure, the underdeveloped hydrogen refueling and distribution networks, technical complexities related to efficient and safe hydrogen storage, and the need for harmonized global safety standards and regulations. Competition from battery-electric technologies in certain segments also presents a challenge.

How does AI impact fuel cell development and deployment?

AI significantly impacts fuel cell development by accelerating material discovery, optimizing stack design for enhanced efficiency and durability, and streamlining manufacturing processes. In deployment, AI enables predictive maintenance, intelligent energy management, and optimized supply chain logistics, leading to more reliable, cost-effective, and efficient fuel cell system operation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted