Hydrogen and Fuel Cell Market

Hydrogen and Fuel Cell Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704514 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Hydrogen and Fuel Cell Market Size

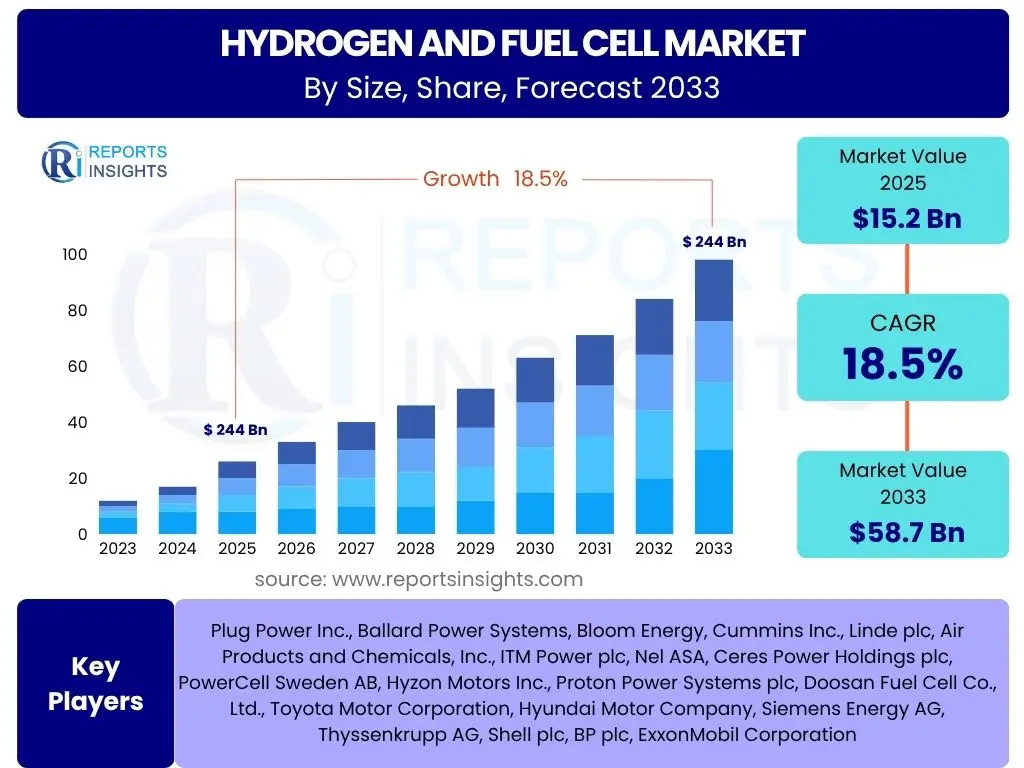

According to Reports Insights Consulting Pvt Ltd, The Hydrogen and Fuel Cell Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 58.7 Billion by the end of the forecast period in 2033.

Key Hydrogen and Fuel Cell Market Trends & Insights

User inquiries frequently focus on understanding the overarching shifts and innovative developments shaping the hydrogen and fuel cell landscape. Common questions revolve around the adoption rates of clean hydrogen, the integration of fuel cell technology in new applications, and the role of policy in accelerating market growth. There is significant interest in how these trends will influence infrastructure development, investment flows, and the overall transition towards a decarbonized energy system. The market is witnessing a rapid evolution driven by technological advancements, increasing environmental imperatives, and strategic collaborations across various industries.

A notable trend is the escalating global focus on green hydrogen production, fueled by declining renewable energy costs and supportive governmental policies aimed at achieving net-zero emissions. This emphasis is shifting investment away from fossil fuel-derived hydrogen towards electrolysis powered by renewable sources. Furthermore, the diversification of fuel cell applications beyond automotive into stationary power, heavy-duty transport, and industrial processes highlights the technology's versatility and growing commercial viability. These trends indicate a maturing market that is increasingly integrated into broader energy transition strategies, moving from niche applications to mainstream energy solutions.

- Accelerated investment in green hydrogen production through electrolysis.

- Expanding applications of fuel cells in heavy-duty transportation (trucks, trains, marine vessels).

- Growing adoption of hydrogen in industrial processes for decarbonization (e.g., steel, ammonia).

- Increasing government incentives and policy support for hydrogen infrastructure development.

- Development of hydrogen hubs and valleys for localized production and distribution.

- Cross-sectoral partnerships between energy companies, industrial players, and technology providers.

- Technological advancements reducing the cost and improving the efficiency of fuel cells and electrolyzers.

AI Impact Analysis on Hydrogen and Fuel Cell

User questions related to the impact of AI on the Hydrogen and Fuel Cell market frequently explore how artificial intelligence can enhance efficiency, optimize production processes, and improve the performance and safety of related technologies. There is keen interest in AI's role in predictive maintenance for fuel cells, optimizing electrolyzer operations, and managing complex hydrogen supply chains. Users also inquire about AI's potential to accelerate research and development, particularly in material science and system design, anticipating that AI could unlock new levels of performance and cost reduction.

The integration of AI is increasingly viewed as a critical enabler for scaling hydrogen and fuel cell technologies. AI algorithms can analyze vast datasets from operational systems, identifying patterns that lead to improved energy efficiency, reduced downtime, and enhanced overall system reliability. For instance, in hydrogen production, AI can optimize renewable energy input to electrolyzers based on real-time grid conditions and hydrogen demand, minimizing operational costs. In fuel cell applications, AI-driven diagnostics can predict component failures, allowing for proactive maintenance and extending the lifespan of critical assets. This pervasive application of AI is expected to significantly contribute to the economic viability and widespread adoption of hydrogen and fuel cell solutions.

- Optimization of hydrogen production processes, particularly electrolysis, through predictive modeling.

- Enhanced efficiency and lifespan of fuel cell stacks via AI-driven predictive maintenance and performance monitoring.

- Intelligent management of hydrogen supply chains, including storage, distribution, and demand forecasting.

- Acceleration of R&D in new materials and catalyst discovery for improved fuel cell and electrolyzer efficiency.

- Real-time anomaly detection and fault diagnosis in hydrogen infrastructure for improved safety.

- Automated control systems for hydrogen energy systems, optimizing energy flow and grid integration.

- Data-driven insights for strategic investment decisions and market trend analysis within the sector.

Key Takeaways Hydrogen and Fuel Cell Market Size & Forecast

User inquiries regarding key takeaways from the Hydrogen and Fuel Cell market size and forecast often center on the market's growth trajectory, the primary drivers of this expansion, and the factors that could potentially impede or accelerate its progress. There is a strong desire to understand the long-term outlook for hydrogen as a clean energy carrier and the commercial viability of fuel cell technologies across various sectors. Users are looking for concise summaries that highlight the most significant opportunities for investment and strategic development, as well as the critical challenges that need to be addressed for sustained growth.

The forecast data unequivocally points to robust growth in the Hydrogen and Fuel Cell market, driven by global decarbonization mandates and significant advancements in production and application technologies. A crucial takeaway is the increasing policy support and financial incentives from governments worldwide, positioning hydrogen as a cornerstone of future energy systems. While substantial investments are required for infrastructure development and cost reduction, the market is poised for transformative expansion. The emphasis on green hydrogen and diversified fuel cell applications signals a strong shift towards sustainable and versatile energy solutions, making this sector a high-potential area for innovation and economic growth.

- The market exhibits a substantial Compound Annual Growth Rate (CAGR), indicating strong investment potential.

- Decarbonization efforts and climate goals are primary catalysts for market expansion.

- Technological advancements in electrolysis and fuel cell efficiency are driving cost reduction and broader adoption.

- Government policies and subsidies play a critical role in fostering market growth and infrastructure development.

- Hydrogen is increasingly recognized as a vital component for hard-to-abate sectors like heavy industry and transportation.

- Infrastructure development, particularly for hydrogen production, storage, and distribution, remains a key focus area.

- The market is characterized by a shift towards sustainable, green hydrogen production methods.

Hydrogen and Fuel Cell Market Drivers Analysis

The hydrogen and fuel cell market is primarily propelled by an accelerating global commitment to decarbonization and the urgent need to address climate change. Governments and corporations worldwide are setting ambitious net-zero emission targets, positioning clean hydrogen as a crucial element in achieving these goals. This strategic emphasis translates into substantial policy support, including subsidies, tax incentives, and regulatory frameworks designed to foster hydrogen production, infrastructure development, and fuel cell adoption across various sectors. The increasing availability and affordability of renewable energy sources, such as solar and wind power, are directly reducing the cost of green hydrogen production, making it a more economically attractive alternative to traditional fossil fuels.

Furthermore, the market benefits significantly from ongoing technological advancements that are improving the efficiency and durability of electrolyzers and fuel cells while simultaneously driving down manufacturing costs. These innovations make hydrogen solutions more competitive and reliable for a wider range of applications, from stationary power generation to heavy-duty transportation and industrial processes. The growing demand for energy security and diversification, coupled with the inherent versatility of hydrogen as an energy carrier and industrial feedstock, further underscores its importance. As countries seek to reduce reliance on volatile fossil fuel markets, hydrogen offers a resilient and sustainable energy pathway, stimulating significant private and public investment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Goals and Net-Zero Targets | +5.0% | Global, particularly EU, North America, Japan, South Korea, China | Short to Long-term (2025-2033) |

| Government Policies, Incentives, and Subsidies | +4.5% | EU (Hydrogen Strategy), USA (IRA, Infrastructure Bill), Japan, Germany, Australia | Short to Mid-term (2025-2030) |

| Declining Cost of Renewable Energy Sources | +3.5% | Global, especially regions with high solar/wind potential (e.g., Middle East, Australia, Chile) | Mid to Long-term (2027-2033) |

| Technological Advancements in Electrolyzers and Fuel Cells | +3.0% | Global, R&D hubs in North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Increasing Demand for Clean Transportation Solutions | +2.5% | North America, Europe, China, Japan, South Korea | Mid to Long-term (2027-2033) |

Hydrogen and Fuel Cell Market Restraints Analysis

Despite its significant growth potential, the hydrogen and fuel cell market faces several substantial restraints that could impede its rapid expansion. A primary challenge is the high upfront capital expenditure required for hydrogen production facilities, particularly for green hydrogen, as well as for the extensive infrastructure needed for storage, transportation, and refueling. These significant initial investments often pose a barrier to entry for new players and can slow down project deployment, making it challenging to achieve economies of scale necessary for widespread adoption. The cost of fuel cell systems themselves, though declining, remains relatively high compared to conventional alternatives in certain applications, impacting commercial viability and consumer acceptance.

Another critical restraint is the nascent and often fragmented nature of hydrogen infrastructure globally. A lack of comprehensive and interconnected networks for hydrogen supply and distribution limits the practical applications of fuel cell technologies, especially in transportation. Furthermore, the efficiency of hydrogen production and conversion processes, while improving, still presents a challenge. Energy losses during electrolysis, compression, and fuel cell operation mean that the overall "well-to-wheel" efficiency can be a concern. Additionally, public perception and safety concerns associated with hydrogen, despite its proven safety record under proper handling, can lead to regulatory hurdles and social resistance, particularly in urban environments, thereby slowing down infrastructure development and market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Costs for Production and Infrastructure | -4.0% | Global, particularly emerging economies | Short to Mid-term (2025-2030) |

| Limited Hydrogen Infrastructure and Refueling Network | -3.5% | Global, especially outside established industrial zones | Short to Mid-term (2025-2030) |

| Cost Competitiveness Against Established Energy Solutions | -3.0% | Global, particularly in sectors with low-cost alternatives | Short to Mid-term (2025-2030) |

| Technical Challenges and Efficiency Losses in Conversion | -2.0% | Global, R&D intensive regions | Short-term (2025-2028) |

| Public Perception and Safety Concerns Around Hydrogen | -1.5% | Urban areas, regions with limited public education | Mid-term (2027-2033) |

Hydrogen and Fuel Cell Market Opportunities Analysis

The hydrogen and fuel cell market is ripe with significant opportunities, primarily driven by the burgeoning potential of green hydrogen as a truly sustainable energy carrier. As renewable energy costs continue to fall and electrolysis technologies mature, the production of hydrogen with near-zero carbon emissions becomes increasingly viable and scalable. This shift unlocks vast opportunities for decarbonizing hard-to-abate sectors such as heavy industry (steel, cement, chemicals) and long-haul transportation (maritime, aviation, heavy-duty trucking), where electrification is challenging. The development of regional hydrogen hubs, where production, storage, and demand centers are co-located, represents a major opportunity to create integrated and efficient hydrogen economies, fostering localized growth and optimizing supply chains.

Furthermore, the expanding range of fuel cell applications beyond traditional automotive uses presents a broad spectrum of market opportunities. Stationary power generation, particularly for backup power, grid stability, and remote installations, is a growing segment. The use of fuel cells in material handling equipment (e.g., forklifts), drones, and even in residential heating offers diversified revenue streams. Cross-sector collaboration among energy companies, industrial giants, technology developers, and financial institutions is creating synergistic partnerships that accelerate innovation and project deployment. These collaborations are crucial for overcoming technical and financial hurdles, leveraging diverse expertise, and scaling up the hydrogen economy. The long-term potential for hydrogen as a storage medium for intermittent renewable energy also positions it as a key enabler of a fully decarbonized and resilient energy grid.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Green Hydrogen Production Capacity | +4.8% | Global, particularly Middle East, Australia, South America, North Africa | Mid to Long-term (2027-2033) |

| Decarbonization of Heavy Industry and Hard-to-Abate Sectors | +4.2% | Europe, North America, Asia Pacific (China, India) | Mid to Long-term (2027-2033) |

| Development of Regional Hydrogen Hubs and Valleys | +3.5% | North America (USA), Europe (Germany, Netherlands), Japan, Australia | Short to Mid-term (2025-2030) |

| Emerging Applications in Power Generation and Energy Storage | +2.8% | Global, particularly grid-constrained regions | Mid-term (2027-2033) |

| Cross-Sectoral Collaboration and Strategic Partnerships | +2.0% | Global, across energy, automotive, industrial, and finance sectors | Short to Long-term (2025-2033) |

Hydrogen and Fuel Cell Market Challenges Impact Analysis

The hydrogen and fuel cell market, despite its promising outlook, is confronted by several significant challenges that require concerted efforts for mitigation. One of the primary hurdles is establishing a robust and scalable hydrogen supply chain. This encompasses everything from efficient production (especially green hydrogen), to safe and cost-effective storage, and finally, reliable distribution and refueling infrastructure. The current fragmented nature of this supply chain, coupled with the capital intensity of building new infrastructure, poses a considerable impediment to widespread adoption and market maturation. Addressing these logistical complexities and ensuring a continuous, accessible supply of hydrogen is critical for unlocking the market's full potential.

Another major challenge lies in the regulatory and policy landscape, which is still evolving in many regions. While there is growing governmental support, inconsistencies in regulations, permitting processes, and safety standards across different jurisdictions can create uncertainty for investors and developers, hindering project deployment. The cost competitiveness of hydrogen and fuel cell solutions relative to established fossil fuel technologies also remains a challenge in many applications without significant policy support or carbon pricing mechanisms. Furthermore, ensuring the long-term reliability and durability of fuel cell systems in diverse operating environments, as well as overcoming public perception issues related to hydrogen safety, are crucial for gaining widespread acceptance and trust. These multifaceted challenges necessitate innovative solutions, collaborative efforts, and a clear, consistent regulatory framework to de-risk investments and accelerate market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Developing Scalable and Cost-Effective Hydrogen Supply Chain | -4.5% | Global, particularly for green hydrogen at scale | Short to Mid-term (2025-2030) |

| Regulatory Uncertainty and Inconsistent Policy Frameworks | -3.8% | Global, especially emerging hydrogen markets | Short to Mid-term (2025-2030) |

| Cost Competitiveness without Subsidies | -3.2% | Global, in competition with traditional energy sources | Mid-term (2027-2033) |

| Durability and Long-term Performance of Fuel Cells | -2.5% | Global, R&D focus areas | Short-term (2025-2028) |

| Overcoming Public Acceptance and Safety Concerns | -1.8% | Global, particularly for infrastructure development in populated areas | Long-term (2030-2033) |

Hydrogen and Fuel Cell Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Hydrogen and Fuel Cell market, providing an in-depth analysis of its current state, historical performance, and future growth trajectory. It offers a detailed examination of market size estimations, growth drivers, key restraints, emerging opportunities, and significant challenges impacting the industry. The report segments the market extensively by type, technology, application, and end-user, providing granular insights into each category's contribution to the overall market landscape. Furthermore, it presents a thorough regional analysis, highlighting key market trends and opportunities across major geographical areas. Strategic profiles of leading market players are included, offering a competitive assessment of their market positioning, product portfolios, and recent developments, providing stakeholders with critical intelligence for informed decision-making and strategic planning within this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 58.7 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Plug Power Inc., Ballard Power Systems, Bloom Energy, Cummins Inc., Linde plc, Air Products and Chemicals, Inc., ITM Power plc, Nel ASA, Ceres Power Holdings plc, PowerCell Sweden AB, Hyzon Motors Inc., Proton Power Systems plc, Doosan Fuel Cell Co., Ltd., Toyota Motor Corporation, Hyundai Motor Company, Siemens Energy AG, Thyssenkrupp AG, Shell plc, BP plc, ExxonMobil Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Hydrogen and Fuel Cell market is extensively segmented to provide granular insights into its diverse components, reflecting the varied methods of hydrogen production, the different types of fuel cell technologies, and their wide array of applications across multiple end-use industries. This detailed segmentation allows for a comprehensive understanding of market dynamics within each specific category, identifying high-growth areas and emerging niches. The classification by hydrogen type differentiates between carbon-intensive methods and those aligned with decarbonization goals, while the technology segmentation highlights the various fuel cell designs suited for different operational requirements and power outputs. These detailed breakdowns enable a nuanced analysis of market trends and competitive landscapes within each segment.

The application and end-user segments further delineate the market by the specific sectors and industries leveraging hydrogen and fuel cell solutions, ranging from heavy-duty transportation and industrial feedstock to stationary power generation and residential heating. This multi-dimensional segmentation is crucial for stakeholders to pinpoint specific market opportunities, allocate resources effectively, and develop targeted strategies. Understanding how each segment contributes to the overall market growth, and identifying the leading technologies and applications, is essential for navigating the complexities of this evolving energy landscape and capitalizing on its inherent potential for sustainable development.

- By Type:

- Green Hydrogen

- Blue Hydrogen

- Grey Hydrogen

- Others

- By Technology (Fuel Cells):

- Proton Exchange Membrane Fuel Cells (PEMFC)

- Solid Oxide Fuel Cells (SOFC)

- Alkaline Fuel Cells (AFC)

- Phosphoric Acid Fuel Cells (PAFC)

- Molten Carbonate Fuel Cells (MCFC)

- Direct Methanol Fuel Cells (DMFC)

- By Application (Hydrogen):

- Power Generation

- Transportation (Fuel Cell Electric Vehicles - FCEVs, Marine, Rail, Aviation)

- Industrial Feedstock (Ammonia, Methanol, Refining)

- Heating & Cooling

- Energy Storage

- By Application (Fuel Cells):

- Stationary Power

- Portable Power

- Transportation (Automotive, Marine, Aerospace, Rail, Material Handling)

- By End-User:

- Automotive

- Power & Utilities

- Oil & Gas

- Chemicals

- Manufacturing

- Logistics

- Building & Construction

Regional Highlights

- North America: Driven by supportive policies like the Inflation Reduction Act (IRA) and Infrastructure Investment and Jobs Act in the United States, alongside increasing investments in hydrogen hubs and fuel cell vehicle deployment. Canada is also actively pursuing green hydrogen production.

- Europe: Leading the charge in hydrogen strategy with ambitious targets for green hydrogen production and consumption, significant funding through initiatives like the European Green Deal, and strong focus on decarbonizing heavy industry and transport, particularly in Germany, Netherlands, and France.

- Asia Pacific (APAC): Emerging as a major growth hub, led by robust initiatives in China, Japan, and South Korea, focusing on fuel cell electric vehicles (FCEVs), large-scale green hydrogen projects, and developing comprehensive hydrogen supply chains to meet industrial and energy demands. Australia and India are also making substantial investments.

- Latin America: Possesses immense potential for green hydrogen production due to abundant renewable energy resources (e.g., wind in Chile, solar in Brazil), attracting international investment for export-oriented projects, with early-stage infrastructure development underway.

- Middle East and Africa (MEA): Positioning itself as a future global leader in green hydrogen exports, leveraging vast solar resources and strategic geographic location. Countries like Saudi Arabia, UAE, and Oman are investing billions in large-scale green hydrogen and ammonia projects, primarily for export to Europe and Asia.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrogen and Fuel Cell Market.- Plug Power Inc.

- Ballard Power Systems

- Bloom Energy

- Cummins Inc.

- Linde plc

- Air Products and Chemicals, Inc.

- ITM Power plc

- Nel ASA

- Ceres Power Holdings plc

- PowerCell Sweden AB

- Hyzon Motors Inc.

- Proton Power Systems plc

- Doosan Fuel Cell Co., Ltd.

- Toyota Motor Corporation

- Hyundai Motor Company

- Siemens Energy AG

- Thyssenkrupp AG

- Shell plc

- BP plc

- ExxonMobil Corporation

Frequently Asked Questions

What is the primary driver for hydrogen and fuel cell market growth?

The primary driver for hydrogen and fuel cell market growth is the global imperative to decarbonize various sectors and achieve net-zero emission targets. This is strongly supported by increasing government incentives, declining renewable energy costs making green hydrogen more viable, and advancements in fuel cell and electrolyzer technologies.

What are the main types of hydrogen in the market?

The main types of hydrogen in the market include Green Hydrogen (produced via electrolysis with renewable energy), Blue Hydrogen (produced from natural gas with carbon capture and storage), and Grey Hydrogen (produced from natural gas without carbon capture, the most common type currently). Other emerging types include Pink (nuclear power), Yellow (solar power), and Turquoise (methane pyrolysis).

How does AI impact the hydrogen and fuel cell sector?

AI significantly impacts the hydrogen and fuel cell sector by optimizing production processes, enhancing the efficiency and lifespan of fuel cells through predictive maintenance, and intelligently managing complex supply chains. AI also accelerates research and development, aiding in new material discovery and system design, ultimately reducing costs and improving reliability.

What are the biggest challenges facing the hydrogen and fuel cell market?

The biggest challenges facing the hydrogen and fuel cell market include high upfront capital costs for production and infrastructure, the limited and fragmented global hydrogen infrastructure, and ensuring long-term cost competitiveness against established energy solutions without subsidies. Regulatory inconsistencies and public perception regarding safety also pose significant hurdles.

Which regions are leading the adoption of hydrogen and fuel cell technologies?

Europe, North America, and Asia Pacific (particularly China, Japan, and South Korea) are currently leading the adoption of hydrogen and fuel cell technologies. These regions are characterized by strong policy support, significant investments in R&D and infrastructure, and ambitious decarbonization goals driving widespread implementation across various applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted