Hydrocarbon Resin Market

Hydrocarbon Resin Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701098 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

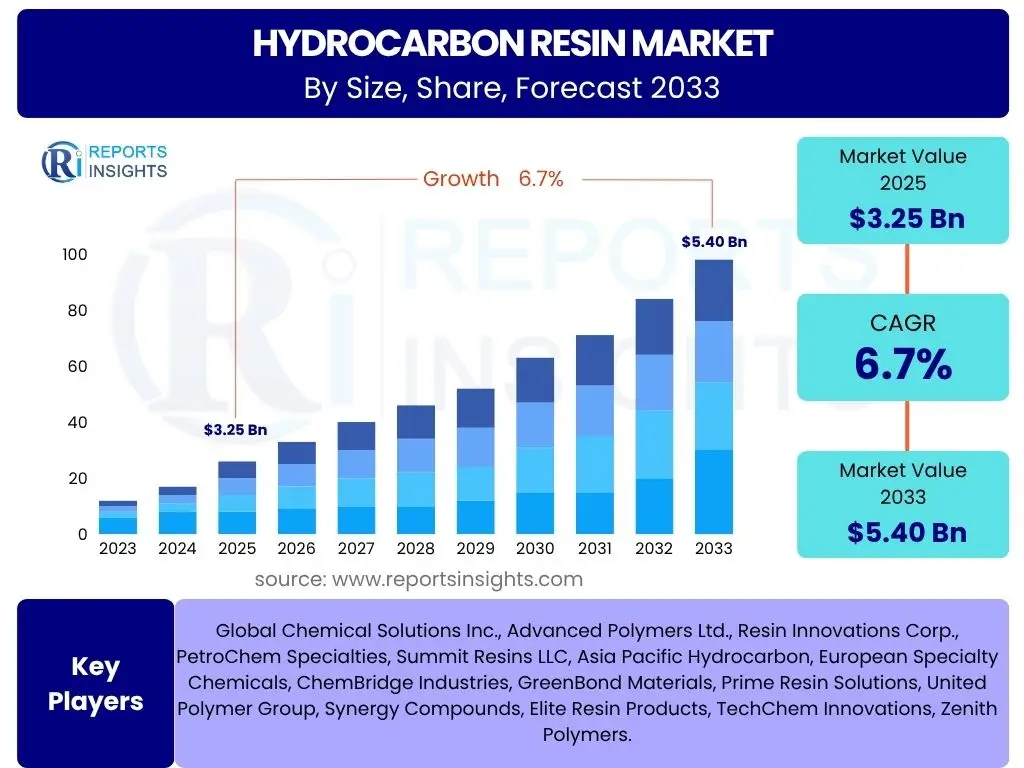

Hydrocarbon Resin Market Size

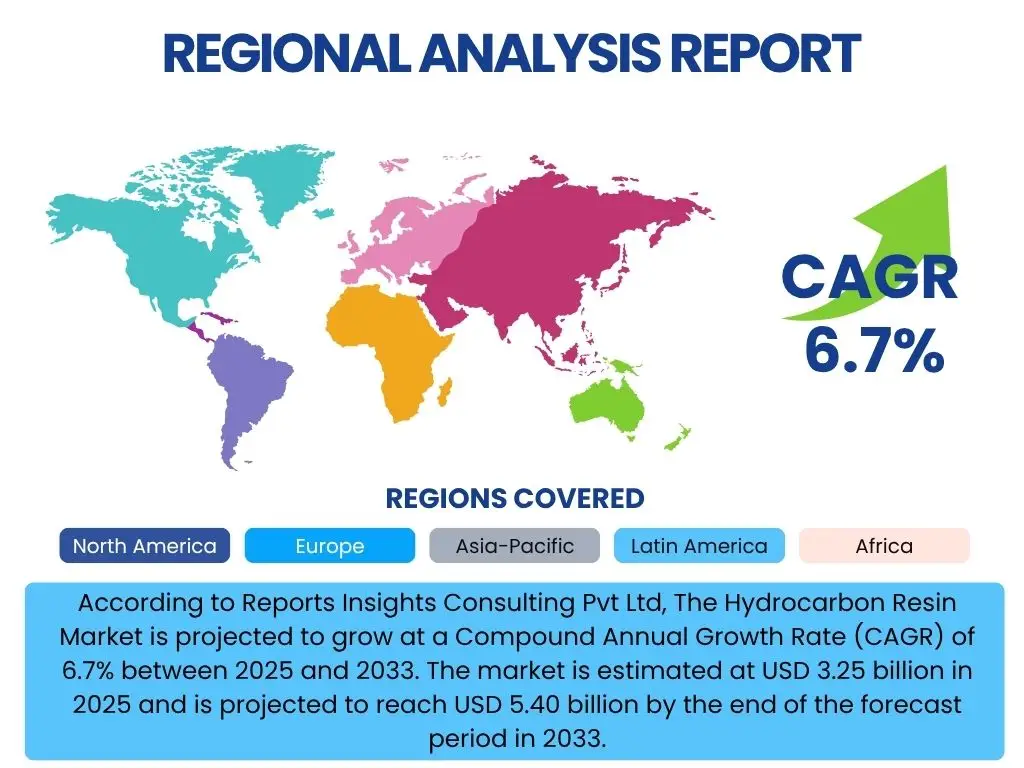

According to Reports Insights Consulting Pvt Ltd, The Hydrocarbon Resin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 3.25 billion in 2025 and is projected to reach USD 5.40 billion by the end of the forecast period in 2033.

Key Hydrocarbon Resin Market Trends & Insights

The hydrocarbon resin market is currently experiencing significant shifts driven by evolving industrial demands and increasing sustainability consciousness. Key trends include the growing adoption of these resins in high-performance adhesive and sealant formulations, spurred by advancements in packaging and construction. There is also a notable emphasis on developing specialized resins for niche applications, enhancing their versatility and market penetration across various sectors.

Furthermore, the market is witnessing a steady inclination towards hydrogenated and bio-based hydrocarbon resins, reflecting a broader industry trend towards environmentally friendlier solutions. Innovations in production processes, aiming for higher efficiency and reduced environmental footprint, are also shaping the market landscape. These trends collectively underscore a dynamic market that is adapting to both technological advancements and global environmental imperatives.

- Increasing demand for hot-melt adhesives and pressure-sensitive adhesives.

- Growing preference for hydrogenated hydrocarbon resins due to their light color, thermal stability, and low odor.

- Expansion of applications in road marking paints, driven by infrastructure development.

- Technological advancements leading to enhanced resin properties like improved tack and adhesion.

- Rising adoption of bio-based and sustainable hydrocarbon resin alternatives.

- Focus on developing customized resins for specific end-use industry requirements.

- Increasing consumption in the tire and rubber industry for improved performance characteristics.

AI Impact Analysis on Hydrocarbon Resin

Artificial intelligence (AI) is poised to significantly transform the hydrocarbon resin industry by optimizing various stages of the value chain, from raw material sourcing to product development and market analysis. Users frequently inquire about AI's potential to enhance production efficiency, improve product quality, and accelerate innovation. AI can enable predictive analytics for raw material price fluctuations, optimize complex manufacturing processes, and facilitate the development of novel resin formulations with desired properties.

The application of AI extends to quality control, where machine learning algorithms can analyze data from production lines to detect anomalies and ensure consistent product specifications, thereby reducing waste and improving yields. Furthermore, AI-driven supply chain management can enhance logistical efficiency, minimizing lead times and optimizing inventory levels. While the adoption is nascent, industry stakeholders anticipate AI will play a crucial role in enhancing competitiveness, fostering sustainable practices, and driving future growth in the hydrocarbon resin market.

- Raw Material Optimization: AI algorithms can predict feedstock price fluctuations and optimize purchasing strategies.

- Process Automation & Efficiency: AI can control and optimize reaction parameters in real-time, improving yield and energy efficiency.

- Quality Control Enhancement: Machine learning for anomaly detection and consistent product specification adherence.

- Predictive Maintenance: AI models can forecast equipment failures, minimizing downtime and maintenance costs.

- Accelerated R&D: AI can screen vast chemical libraries and predict properties of new formulations, speeding up product development.

- Supply Chain Optimization: AI-driven logistics and inventory management for improved efficiency and responsiveness.

Key Takeaways Hydrocarbon Resin Market Size & Forecast

The hydrocarbon resin market is on a trajectory of sustained growth, underscored by robust demand from diverse industrial applications. A primary insight reveals that the market's expansion is intrinsically linked to the performance of the packaging, adhesives, and construction sectors globally. The forecast indicates a notable shift towards specialized and higher-performing resin types, reflecting an industry-wide drive for enhanced product efficacy and longevity.

Furthermore, the increasing awareness and regulatory pressure regarding environmental sustainability are driving innovation towards bio-based and hydrogenated variants, suggesting these segments will contribute significantly to future market value. Geographically, emerging economies are expected to be key growth engines, capitalizing on rapid industrialization and infrastructure development. The competitive landscape is characterized by continuous innovation and strategic collaborations, aiming to capture market share and address evolving consumer preferences.

- The market is projected for steady expansion, fueled by strong demand from key end-use industries.

- Adhesives and sealants remain the dominant application segment, with continued innovation driving growth.

- Asia Pacific is anticipated to maintain its leading position, driven by extensive manufacturing and construction activities.

- Sustainability initiatives are increasingly influencing product development, with a growing focus on bio-based and hydrogenated resins.

- Technological advancements in resin synthesis and application are crucial for enhancing market value.

- Volatile raw material prices and stringent environmental regulations pose ongoing challenges but also foster innovation.

Hydrocarbon Resin Market Drivers Analysis

The hydrocarbon resin market is propelled by a confluence of factors, primarily stemming from the robust growth observed across various end-use industries. Increasing demand for adhesives and sealants, driven by advancements in packaging and construction, forms a significant impetus. Additionally, the automotive sector's continuous evolution, alongside extensive infrastructure development projects globally, further stimulates the consumption of hydrocarbon resins. These resins offer critical properties like tack, adhesion, and compatibility, making them indispensable components in a wide array of applications.

Furthermore, the expanding applications in paints and coatings, especially high-performance variants, contribute substantially to market expansion. The global shift towards urbanization and industrialization, particularly in emerging economies, drives construction activities and manufacturing output, inherently increasing the demand for materials that utilize hydrocarbon resins. Manufacturers are also innovating to produce specialized resins that meet specific performance criteria, thereby opening new avenues for market growth and solidifying the market's trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Adhesives & Sealants Industry | +1.8% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Expansion of the Packaging Sector | +1.5% | Asia Pacific, North America, Europe | Medium to Long-term (2025-2033) |

| Increasing Automotive Production & Aftermarket | +1.2% | Asia Pacific (China, India), Europe, North America | Medium-term (2025-2030) |

| Rising Infrastructure Development & Construction Activities | +1.0% | Asia Pacific, Middle East & Africa, Latin America | Long-term (2025-2033) |

Hydrocarbon Resin Market Restraints Analysis

Despite the positive growth outlook, the hydrocarbon resin market faces several significant restraints that could impede its expansion. One primary concern is the inherent volatility of raw material prices, as these resins are petrochemical derivatives. Fluctuations in crude oil prices directly impact production costs, posing challenges for manufacturers in terms of profitability and consistent pricing strategies. This unpredictability can lead to budget uncertainties and hinder long-term investment planning for market players.

Furthermore, stringent environmental regulations regarding the production and disposal of petrochemical-based products present a formidable hurdle. Concerns over volatile organic compound (VOC) emissions and the non-biodegradable nature of some resins necessitate significant investments in compliance technologies and R&D for more sustainable alternatives. The availability of substitute materials, particularly bio-based polymers, also poses a competitive threat, potentially diverting demand away from traditional hydrocarbon resins. These factors collectively require strategic adaptation from industry participants to navigate market complexities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Naphtha, Aromatics) | -1.5% | Global, especially regions reliant on imports | Short to Medium-term (2025-2028) |

| Stringent Environmental Regulations & Sustainability Concerns | -1.0% | Europe, North America, increasingly Asia Pacific | Long-term (2025-2033) |

| Competition from Alternative Resins & Bio-based Materials | -0.8% | Global, particularly in specialized applications | Medium to Long-term (2025-2033) |

| Health and Safety Concerns Related to Petrochemical Derivatives | -0.5% | Global, particularly in occupational settings | Long-term (2025-2033) |

Hydrocarbon Resin Market Opportunities Analysis

Significant opportunities exist within the hydrocarbon resin market, particularly in the realm of sustainable product development and expansion into high-growth emerging economies. The rising demand for bio-based and environmentally friendly resins presents a lucrative avenue for innovation and market differentiation. Companies investing in research and development of resins derived from renewable resources or those with reduced environmental footprints can capture a growing segment of environmentally conscious consumers and industries.

Furthermore, the rapid industrialization and urbanization in countries across Asia Pacific, Latin America, and the Middle East & Africa offer immense untapped market potential. These regions are experiencing booming construction activities, expanding manufacturing bases, and increasing automotive production, all of which drive the demand for hydrocarbon resins in various applications. Strategic partnerships, capacity expansion, and localized production facilities in these regions can enable market players to capitalize on these growth prospects. Additionally, the continuous pursuit of advanced functionalities and new application areas for hydrocarbon resins, such as in specialized electronics or medical devices, presents further long-term growth opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Commercialization of Bio-based & Sustainable Resins | +2.0% | Global, particularly Europe and North America | Long-term (2026-2033) |

| Growing Demand in Emerging Economies (APAC, Latin America, MEA) | +1.7% | China, India, Brazil, Indonesia, GCC countries | Long-term (2025-2033) |

| R&D for New Applications & Enhanced Performance Resins | +1.3% | Global, especially in niche and high-tech sectors | Medium to Long-term (2025-2033) |

| Technological Advancements in Hydrogenation Processes | +1.0% | Global, focused on improved product quality and efficiency | Medium-term (2025-2030) |

Hydrocarbon Resin Market Challenges Impact Analysis

The hydrocarbon resin market faces several critical challenges that demand strategic foresight and adaptive measures from industry participants. One significant challenge revolves around managing the complex and often unpredictable global supply chain, which can be disrupted by geopolitical tensions, natural disasters, or pandemics. Such disruptions can lead to raw material shortages, production delays, and increased costs, impacting overall market stability and profitability for manufacturers reliant on a consistent flow of inputs.

Another pressing issue is the intense market competition, characterized by numerous domestic and international players. This fierce rivalry often leads to price wars, eroding profit margins and making it difficult for new entrants or smaller players to establish a foothold. Furthermore, the industry faces the continuous challenge of adhering to evolving regulatory landscapes, especially concerning environmental protection and product safety. Ensuring compliance while maintaining cost-effectiveness and innovation remains a balancing act. These challenges necessitate a robust risk management framework, continuous innovation, and efficient operational strategies to sustain growth and maintain a competitive edge in the global hydrocarbon resin market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions & Logistics Issues | -1.2% | Global, particularly affecting import/export heavy regions | Short to Medium-term (2025-2028) |

| Intense Market Competition & Pricing Pressures | -0.9% | Global, prevalent in mature markets | Long-term (2025-2033) |

| Managing Waste & Emissions from Production Processes | -0.7% | Global, especially in regions with strict environmental norms | Long-term (2025-2033) |

| Achieving Cost-Effectiveness for Specialized Applications | -0.6% | Global, especially for niche and high-performance segments | Medium to Long-term (2025-2033) |

Hydrocarbon Resin Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Hydrocarbon Resin Market, offering critical insights into its current dynamics, historical performance, and future growth projections. It covers detailed market sizing, segmentation by type, application, and end-use industry, alongside a thorough regional breakdown. The report also examines key market trends, drivers, restraints, opportunities, and challenges, providing a holistic understanding of the factors influencing market evolution. Special emphasis is placed on the impact of emerging technologies like AI and the growing importance of sustainability within the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.25 Billion |

| Market Forecast in 2033 | USD 5.40 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Chemical Solutions Inc., Advanced Polymers Ltd., Resin Innovations Corp., PetroChem Specialties, Summit Resins LLC, Asia Pacific Hydrocarbon, European Specialty Chemicals, ChemBridge Industries, GreenBond Materials, Prime Resin Solutions, United Polymer Group, Synergy Compounds, Elite Resin Products, TechChem Innovations, Zenith Polymers. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The hydrocarbon resin market is broadly segmented by type, application, and end-use industry, reflecting the diverse characteristics and varied utility of these versatile chemical compounds. This multi-faceted segmentation allows for a granular understanding of market dynamics, pinpointing specific growth drivers and areas of high demand within each category. Understanding these segments is crucial for stakeholders to tailor strategies, develop targeted products, and optimize their market positioning.

The segmentation highlights the dominance of certain resin types, such as C5 and C9, in specific applications, while also showcasing the emerging prominence of hydrogenated and bio-based variants driven by performance and sustainability considerations. Analyzing these segments provides a comprehensive overview of where demand is strongest, where innovation is occurring, and how market participants can best align their offerings with evolving industry needs across different sectors globally.

- By Type: C5 Hydrocarbon Resins, C9 Hydrocarbon Resins, C5/C9 Copolymer Resins, C4 Hydrocarbon Resins, Hydrogenated Hydrocarbon Resins, Others.

- By Application: Adhesives & Sealants (Hot Melt Adhesives, Pressure Sensitive Adhesives), Printing Inks, Rubber Compounding, Coatings, Road Marking, Building & Construction, Others.

- By End-Use Industry: Automotive, Packaging, Building & Construction, Tire & Rubber, Paints & Coatings, Consumer Goods, Others.

Regional Highlights

- Asia Pacific (APAC): Dominates the global hydrocarbon resin market, driven by rapid industrialization, extensive infrastructure development projects, and the thriving automotive and packaging industries, especially in economies like China, India, and Southeast Asian nations. The region benefits from large manufacturing bases and increasing consumption of adhesives, coatings, and rubber products.

- North America: Represents a mature yet steadily growing market, characterized by significant demand from the adhesives and sealants, automotive, and construction sectors. Innovation in sustainable and high-performance resins is a key focus, with stringent environmental regulations pushing for advanced formulations and recycling initiatives.

- Europe: A significant market for hydrocarbon resins, particularly driven by the automotive, packaging, and paints & coatings industries. The region is at the forefront of adopting environmentally friendly and bio-based resins, influenced by strict regulatory frameworks and a strong emphasis on circular economy principles.

- Latin America: Expected to show considerable growth due to increasing industrialization, urbanization, and investments in infrastructure. Brazil and Mexico are key contributors, with rising demand from construction, automotive, and packaging sectors. The market here often seeks cost-effective and versatile resin solutions.

- Middle East & Africa (MEA): Emerging as a high-growth region, propelled by large-scale construction projects, diversification efforts in non-oil sectors, and growing manufacturing capabilities. Countries in the GCC region and South Africa are witnessing increased demand for hydrocarbon resins in road marking, coatings, and adhesives, supporting local development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrocarbon Resin Market.- Global Chemical Solutions Inc.

- Advanced Polymers Ltd.

- Resin Innovations Corp.

- PetroChem Specialties

- Summit Resins LLC

- Asia Pacific Hydrocarbon

- European Specialty Chemicals

- ChemBridge Industries

- GreenBond Materials

- Prime Resin Solutions

- United Polymer Group

- Synergy Compounds

- Elite Resin Products

- TechChem Innovations

- Zenith Polymers

- Dyno Resin Solutions

- MasterBond Adhesives

- Polymeric Solutions Group

- Continental Resins Inc.

- InnovateChem Corp.

Frequently Asked Questions

What is hydrocarbon resin and its primary uses?

Hydrocarbon resin is a low molecular weight thermoplastic polymer derived from petroleum fractions, primarily C5, C9, and DCPD. Its primary uses are as a tackifier in adhesives and sealants, a binder in printing inks and coatings, and a modifier in rubber compounding, enhancing properties like adhesion, tack, and heat resistance across various industrial applications.

Which factors are driving the growth of the hydrocarbon resin market?

The market's growth is primarily driven by the escalating demand from the adhesives and sealants industry, the expanding packaging sector, increased automotive production, and significant infrastructure development projects worldwide. These industries rely heavily on hydrocarbon resins for their performance-enhancing properties.

What are the main challenges facing the hydrocarbon resin industry?

Key challenges include the volatility of raw material prices, which can impact production costs and profitability. Additionally, stringent environmental regulations regarding VOC emissions and sustainability concerns pose hurdles, alongside intense market competition and potential supply chain disruptions.

How is Asia Pacific positioned in the global hydrocarbon resin market?

Asia Pacific is the leading region in the global hydrocarbon resin market, characterized by its substantial share and high growth rate. This dominance is attributed to rapid industrialization, booming construction and packaging industries, and a large manufacturing base in countries like China and India, driving robust demand for resins.

What are the emerging opportunities in the hydrocarbon resin market?

Emerging opportunities include the growing focus on developing and adopting bio-based and sustainable hydrocarbon resins, driven by environmental consciousness and regulatory pressures. Furthermore, significant growth potential lies in expanding applications within fast-developing emerging economies and through continuous R&D for new, high-performance formulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted