Hydraulic Fitting Market

Hydraulic Fitting Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707315 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

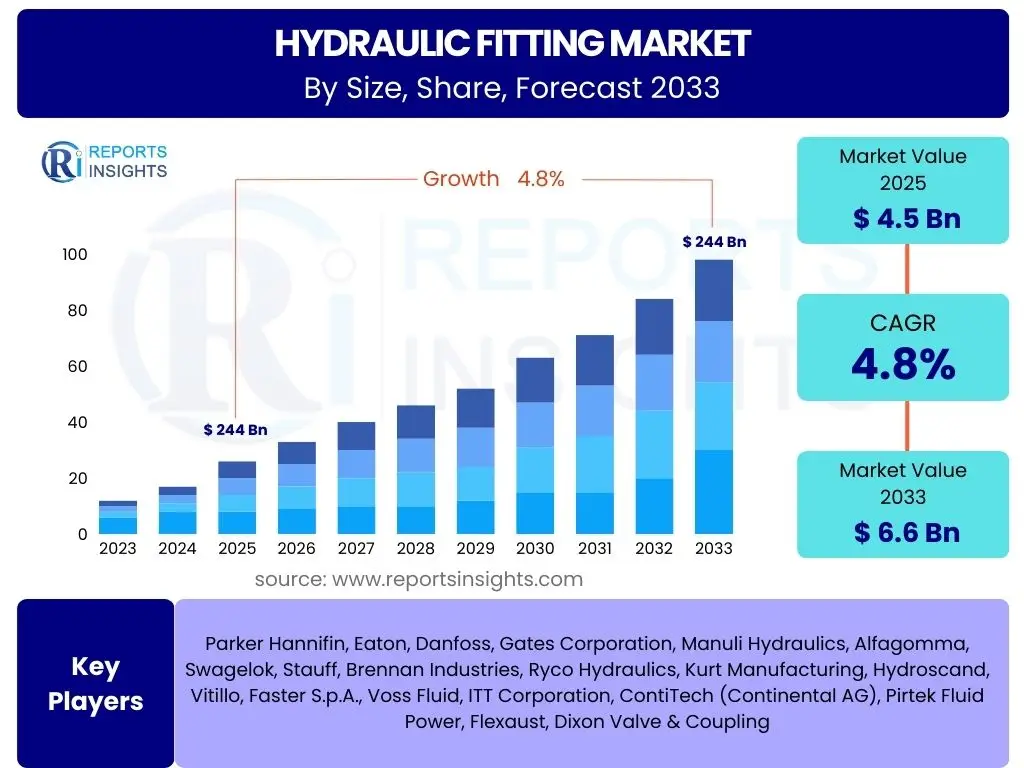

Hydraulic Fitting Market Size

According to Reports Insights Consulting Pvt Ltd, The Hydraulic Fitting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 6.6 Billion by the end of the forecast period in 2033.

Key Hydraulic Fitting Market Trends & Insights

User inquiries frequently revolve around the evolving technological landscape and market dynamics shaping the hydraulic fitting industry. A primary concern is the drive towards enhanced efficiency and durability in fluid power systems, leading to significant interest in advanced material science and design innovations. Additionally, there is a clear demand for understanding how the industry is adapting to stringent environmental regulations and the increasing emphasis on sustainable manufacturing practices.

The market is witnessing a profound shift towards the adoption of lightweight materials, driven by the aerospace and automotive sectors' need for fuel efficiency and reduced operational costs. Concurrently, the integration of smart technologies, such as sensors for predictive maintenance and condition monitoring, is emerging as a critical trend, allowing for greater system uptime and operational reliability. This push for smart solutions extends to optimizing supply chains and improving overall system performance.

Furthermore, the global expansion of infrastructure projects, particularly in emerging economies, is creating sustained demand for robust and reliable hydraulic components. This trend is coupled with the growing mechanization of agriculture and the expansion of the construction industry worldwide, which are key drivers for the hydraulic fitting market. The ongoing modernization of industrial equipment across various sectors also contributes to a continuous need for innovative and high-performance fitting solutions.

- Miniaturization and compact designs for space-constrained applications.

- Integration of smart features for predictive maintenance and diagnostics.

- Adoption of advanced materials, including composites and high-strength alloys.

- Emphasis on eco-friendly manufacturing processes and recyclable materials.

- Increased demand for customized and application-specific fitting solutions.

AI Impact Analysis on Hydraulic Fitting

Discussions among users regarding artificial intelligence's influence on the hydraulic fitting domain frequently highlight its potential to revolutionize operational efficiencies and product lifecycle management. There is considerable interest in how AI can enhance the design and engineering phases, particularly in optimizing fitting geometries for improved flow dynamics and structural integrity. Users are keen to understand the tangible benefits AI offers in reducing development cycles and prototyping costs, leading to more agile product innovation.

Another significant area of user inquiry pertains to AI's role in manufacturing and quality assurance within the hydraulic fitting sector. The ability of AI-powered vision systems to detect minute defects with unparalleled precision, far exceeding human capability, is a key point of focus. Furthermore, the application of machine learning algorithms for predictive maintenance on manufacturing equipment is highly anticipated, promising to minimize downtime and optimize production schedules. This integration is expected to lead to higher quality products and more efficient manufacturing lines.

The broader impact of AI also extends to supply chain management and inventory optimization for hydraulic fittings. Users express interest in how AI can forecast demand with greater accuracy, manage inventory levels more effectively, and optimize logistics, thereby reducing lead times and improving customer satisfaction. The potential for AI to create a more resilient and responsive supply chain, mitigating risks associated with global disruptions, is a recurring theme, underscoring its transformative potential across the entire value chain of hydraulic fittings.

- AI-driven generative design for optimized fitting geometries.

- Predictive maintenance for hydraulic systems and manufacturing equipment.

- Enhanced quality control through AI-powered visual inspection.

- Supply chain optimization and demand forecasting via machine learning.

- Automation of manufacturing processes and robotic assembly.

Key Takeaways Hydraulic Fitting Market Size & Forecast

The core insights from the hydraulic fitting market size and forecast consistently point towards a robust and expanding industry, driven by global industrialization and infrastructure development. Users are primarily seeking clarity on the long-term growth trajectory and the underlying factors contributing to market resilience. The forecast indicates that despite potential economic fluctuations, the fundamental demand for fluid power components remains strong, propelled by ongoing advancements in machinery and equipment across diverse sectors.

A significant takeaway is the strategic importance of technological innovation in sustaining market momentum. The shift towards higher-pressure applications, the need for enhanced corrosion resistance, and the demand for lighter yet more durable materials are key themes. These technological imperatives underscore the industry's commitment to continuous improvement and its ability to adapt to evolving performance requirements from end-use industries, ensuring the market remains dynamic and competitive.

Furthermore, the market's growth is inherently linked to global economic health and investment in key industries such as construction, agriculture, and manufacturing. The projections highlight the critical role of emerging economies as growth engines, with increasing industrial activity and infrastructure spending translating directly into higher demand for hydraulic fittings. Understanding these regional growth patterns is crucial for stakeholders planning market entry or expansion strategies, emphasizing the global nature of this essential component market.

- Steady growth driven by industrial expansion and infrastructure projects.

- Technological advancements in materials and design are crucial for market competitiveness.

- Emerging economies are pivotal growth engines for demand.

- Demand for high-performance and application-specific fittings is increasing.

- The market is resilient to economic shifts due to essential applications.

Hydraulic Fitting Market Drivers Analysis

The expansion of the global hydraulic fitting market is fundamentally propelled by the increasing mechanization across various industrial sectors. Industries such as construction, agriculture, and mining are undergoing significant growth and modernization, leading to a surge in demand for heavy machinery and equipment. Each piece of this machinery relies heavily on complex hydraulic systems, necessitating a vast array of fittings to ensure efficient and reliable operation, thereby directly boosting market expansion.

Moreover, the global push for infrastructure development, including roads, bridges, public utilities, and commercial buildings, significantly contributes to the market's upward trajectory. These large-scale projects require extensive use of hydraulic equipment, from excavators and cranes to bulldozers and concrete pumps. As nations invest in improving and expanding their foundational infrastructure, the inherent demand for robust and durable hydraulic fittings experiences a corresponding rise.

Technological advancements and the growing adoption of automation in manufacturing processes also serve as a strong driver. Modern industrial facilities increasingly incorporate automated systems that utilize hydraulic power for precision and force. This trend, coupled with the ongoing replacement and upgrading of older equipment with more efficient, technologically advanced hydraulic systems, ensures a continuous and evolving demand for high-performance hydraulic fittings across diverse industrial applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Infrastructure Development | +1.2% | Asia Pacific, North America, Europe | Throughout Forecast Period |

| Increasing Mechanization in Agriculture & Construction | +1.0% | Asia Pacific, Latin America, Africa | Mid to Long-term |

| Growth in Industrial Automation & Robotics | +0.8% | North America, Europe, Asia Pacific | Short to Mid-term |

| Rise in Mining and Material Handling Activities | +0.7% | Australia, Canada, South America, Africa | Mid-term |

| Modernization of Aerospace & Defense Equipment | +0.5% | North America, Europe | Long-term |

Hydraulic Fitting Market Restraints Analysis

The hydraulic fitting market faces notable constraints, primarily stemming from the volatility of raw material prices. Critical materials such as steel, brass, and specialized alloys, which are essential for manufacturing durable and high-performance fittings, are subject to significant price fluctuations driven by global supply and demand dynamics, geopolitical events, and trade policies. This unpredictability directly impacts production costs, potentially leading to increased end-product prices and subsequently affecting market demand and profit margins for manufacturers.

Another significant restraint is the increasingly stringent environmental regulations and standards imposed globally. Regulations concerning material sourcing, manufacturing processes, and waste disposal, particularly those related to hazardous substances and emissions, necessitate significant investments in compliance. While crucial for environmental protection, these regulations can increase operational complexities and costs for manufacturers, potentially hindering market growth, especially for smaller enterprises or those unable to adapt quickly to new mandates.

Furthermore, the cyclical nature of end-use industries, such as construction and automotive, presents a inherent restraint on market stability. Economic downturns or slowdowns in these major sectors can lead to reduced investment in new machinery and equipment, directly impacting the demand for hydraulic fittings. This dependency on industrial cycles means the market can experience periods of sluggish growth or contraction, requiring manufacturers to diversify their market reach or adjust production capacities to mitigate these effects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.8% | Global | Throughout Forecast Period |

| Stringent Environmental Regulations | -0.6% | Europe, North America | Mid to Long-term |

| Economic Downturns in Key End-Use Industries | -0.5% | Global, especially developed economies | Short-term to Mid-term |

| Competition from Alternative Technologies (e.g., Electric Actuators) | -0.3% | North America, Europe, Asia Pacific | Long-term |

| Trade Barriers and Tariffs | -0.4% | Specific Trade Blocs/Countries | Short-term |

Hydraulic Fitting Market Opportunities Analysis

Significant opportunities in the hydraulic fitting market emerge from the ongoing technological advancements in fluid power systems, particularly the development of smart hydraulics and connected systems. The integration of sensors, IoT devices, and data analytics within hydraulic components allows for real-time monitoring, predictive maintenance, and optimized system performance. This evolution creates avenues for manufacturers to offer higher-value, intelligent fitting solutions that enhance efficiency and reliability across various applications, moving beyond traditional, passive components.

The increasing global focus on renewable energy sources, such as wind power, solar tracking systems, and hydroelectric power, presents another substantial growth opportunity. These sectors heavily rely on robust and reliable hydraulic systems for critical operations like blade pitch control in wind turbines or tracking mechanisms for solar panels. The long service life and harsh operating conditions in these applications create a specific demand for high-performance, durable, and corrosion-resistant hydraulic fittings, fostering a specialized segment within the market.

Furthermore, the expansion into emerging economies and underdeveloped regions offers considerable untapped potential. As these regions experience rapid industrialization, urbanization, and infrastructure development, the demand for construction equipment, agricultural machinery, and industrial automation grows exponentially. Localizing manufacturing, establishing robust distribution networks, and offering cost-effective yet high-quality solutions tailored to regional needs can unlock significant market share and revenue streams for hydraulic fitting manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Smart Hydraulics and IoT Integration | +1.5% | Global, especially developed markets | Mid to Long-term |

| Expansion in Renewable Energy Sector (Wind, Solar) | +1.3% | Europe, Asia Pacific, North America | Throughout Forecast Period |

| Emerging Market Industrialization & Infrastructure Development | +1.1% | Asia Pacific, Latin America, Africa | Throughout Forecast Period |

| Demand for Lightweight and High-Pressure Fittings | +0.9% | North America, Europe, Asia Pacific | Mid-term |

| Retrofitting and Upgrading Existing Hydraulic Systems | +0.7% | Global | Short to Mid-term |

Hydraulic Fitting Market Challenges Impact Analysis

The hydraulic fitting market faces significant challenges from the pervasive issue of counterfeit products. The proliferation of low-quality, unauthorized reproductions of fittings poses a substantial risk to market integrity and legitimate manufacturers. These counterfeit products, often lacking stringent quality control and material specifications, can lead to premature failure, system damage, and even safety hazards, eroding consumer trust and undermining the reputation of genuine brands. Battling these illicit goods requires continuous vigilance, legal action, and robust intellectual property protection strategies, adding complexity and cost to operations.

Another pressing challenge is the shortage of skilled labor across the value chain, from design and engineering to manufacturing and installation. The specialized nature of hydraulic systems demands a workforce with specific technical expertise in fluid dynamics, material science, and precision manufacturing. A dwindling pool of qualified professionals can hamper innovation, delay production, and compromise the quality of hydraulic fittings. Addressing this requires significant investment in training programs, educational partnerships, and attractive career pathways to draw new talent into the industry.

Furthermore, intense price competition, particularly from manufacturers in regions with lower production costs, presents a significant hurdle. While driving efficiency, this competitive pressure can squeeze profit margins for established players, especially those operating in high-cost regions. Maintaining a competitive edge necessitates a focus on product differentiation through superior quality, innovation, and value-added services, rather than solely competing on price. This environment compels companies to continuously optimize their production processes and supply chain for cost-effectiveness without compromising on product integrity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Presence of Counterfeit Products | -0.7% | Global, especially emerging markets | Throughout Forecast Period |

| Skilled Labor Shortage | -0.6% | North America, Europe | Long-term |

| Intense Price Competition | -0.5% | Global | Throughout Forecast Period |

| Supply Chain Disruptions and Geopolitical Instability | -0.4% | Global | Short-term to Mid-term |

| Rapid Technological Obsolescence | -0.3% | Global, especially developed markets | Mid-term |

Hydraulic Fitting Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global hydraulic fitting market, offering insights into its current status, historical performance, and future growth projections. It covers market size estimations, key trends, drivers, restraints, opportunities, and challenges influencing the industry landscape. The report also includes detailed segmentation analysis, regional insights, and profiles of key market players, aiming to equip stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 6.6 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Parker Hannifin, Eaton, Danfoss, Gates Corporation, Manuli Hydraulics, Alfagomma, Swagelok, Stauff, Brennan Industries, Ryco Hydraulics, Kurt Manufacturing, Hydroscand, Vitillo, Faster S.p.A., Voss Fluid, ITT Corporation, ContiTech (Continental AG), Pirtek Fluid Power, Flexaust, Dixon Valve & Coupling |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The hydraulic fitting market is broadly segmented to provide a granular view of its diverse applications and product specifications. This segmentation enables a clearer understanding of specific market niches, technological preferences, and demand drivers within various industries. The categorization by type differentiates between hose, tube, and pipe fittings, alongside specialized components like adapters and couplings, reflecting the distinct requirements for fluid conveyance in different pressure and application environments.

Further segmentation by material highlights the critical role of material science in determining fitting performance, durability, and suitability for various operating conditions. Stainless steel, carbon steel, and brass are common choices, each offering unique properties regarding corrosion resistance, strength, and cost-effectiveness. The choice of material is often dictated by the fluid being conveyed, the operating temperature, and the environmental factors, directly influencing demand within specific end-use sectors.

The end-use industry segmentation reveals the primary sectors driving market demand, encompassing heavy machinery industries like construction and agriculture, as well as specialized fields such as aerospace and oil & gas. Each industry presents unique challenges and demands for hydraulic fittings, ranging from high-pressure requirements in mining to lightweight designs in aviation. Understanding these industry-specific needs is vital for manufacturers to tailor their product offerings and market strategies effectively.

- By Type: Hose Fittings, Tube Fittings, Pipe Fittings, Connectors, Adapters, Couplings, Valves, Others.

- By Material: Stainless Steel, Carbon Steel, Brass, Aluminum, Plastic, Others.

- By End-Use Industry: Construction, Agriculture, Mining, Oil & Gas, Automotive, Aerospace & Defense, Marine, Material Handling, Industrial Manufacturing, Others.

- By Pressure Range: Low Pressure, Medium Pressure, High Pressure, Ultra-High Pressure.

- By Standard: SAE, DIN, ISO, JIS, BSP, NPT, Others.

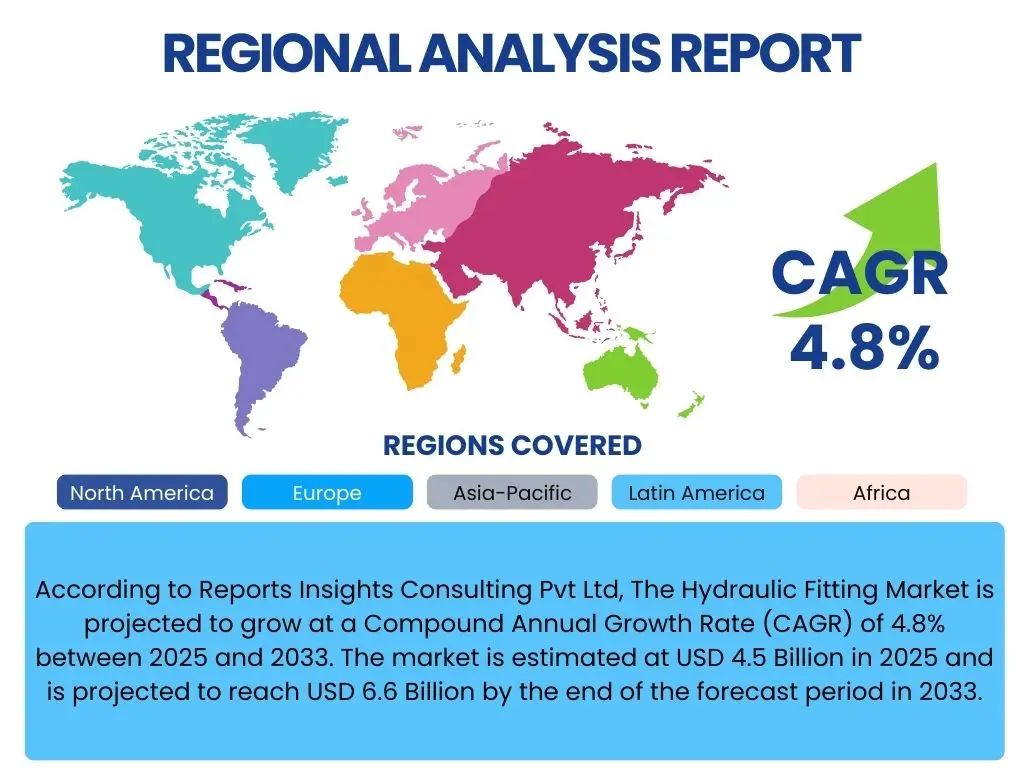

Regional Highlights

The global hydraulic fitting market exhibits distinct regional dynamics driven by varying levels of industrialization, infrastructure development, and technological adoption. North America, characterized by its mature industrial base and significant investments in advanced manufacturing and aerospace, represents a key market. The region's focus on automation and the modernization of existing infrastructure drives consistent demand for high-performance and innovative hydraulic fitting solutions, particularly in high-pressure applications.

Europe stands as another prominent region, influenced by stringent environmental regulations, a strong automotive sector, and substantial investment in renewable energy. The emphasis on efficiency, sustainability, and precision engineering in European industries fosters demand for technically advanced and compliant hydraulic fittings. Furthermore, the region's focus on Industry 4.0 principles encourages the adoption of smart hydraulic components with integrated sensors and connectivity.

Asia Pacific is projected to be the fastest-growing region, fueled by rapid industrialization, massive infrastructure projects, and expanding manufacturing capabilities, especially in China and India. The burgeoning construction and agricultural sectors, coupled with increased foreign direct investment in manufacturing facilities, are accelerating the demand for a wide range of hydraulic fittings. This region also presents significant opportunities for mass production and competitive pricing, making it a critical hub for both consumption and production.

- North America: Dominant market due to strong manufacturing, aerospace, and construction sectors; focus on advanced technology and high-performance applications.

- Europe: Driven by stringent regulations, automotive industry, and renewable energy investments; emphasis on precision and sustainable solutions.

- Asia Pacific (APAC): Fastest-growing market due to rapid industrialization, urbanization, and infrastructure development in China, India, and Southeast Asian countries.

- Latin America: Emerging market with growth potential from increasing agricultural mechanization and mining activities; recovering economic conditions driving investment.

- Middle East & Africa (MEA): Growth attributed to oil & gas exploration, infrastructure development, and increasing demand for heavy equipment in mining and construction.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydraulic Fitting Market.- Parker Hannifin

- Eaton

- Danfoss

- Gates Corporation

- Manuli Hydraulics

- Alfagomma

- Swagelok

- Stauff

- Brennan Industries

- Ryco Hydraulics

- Kurt Manufacturing

- Hydroscand

- Vitillo

- Faster S.p.A.

- Voss Fluid

- ITT Corporation

- ContiTech (Continental AG)

- Pirtek Fluid Power

- Flexaust

- Dixon Valve & Coupling

Frequently Asked Questions

What are the primary drivers for the growth of the hydraulic fitting market?

The hydraulic fitting market's growth is primarily driven by global industrial expansion, significant investments in infrastructure development, and the increasing mechanization of key sectors like construction, agriculture, and mining. Additionally, the growing adoption of automation and robotics in manufacturing processes fuels demand for reliable and high-performance hydraulic components. These factors collectively stimulate the need for a wide array of fittings required for modern machinery and fluid power systems.

Furthermore, the ongoing modernization and upgrade of existing industrial equipment across various industries contribute significantly to market expansion. As older systems are replaced with more efficient and technologically advanced hydraulic solutions, there is a continuous demand for new and compatible hydraulic fittings. This steady replacement cycle ensures sustained market vitality.

How do material advancements influence the hydraulic fitting industry?

Material advancements significantly influence the hydraulic fitting industry by enabling the production of fittings that are more durable, lighter, and resistant to extreme conditions. Innovations in alloys and composites allow manufacturers to create components capable of withstanding higher pressures, extreme temperatures, and corrosive environments, which is crucial for demanding applications in aerospace, marine, and oil & gas sectors.

These material enhancements directly contribute to the longevity and reliability of hydraulic systems, reducing maintenance needs and operational costs. The development of advanced materials also supports miniaturization efforts, allowing for more compact and efficient hydraulic designs. This continuous evolution in material science is vital for meeting the escalating performance requirements and achieving higher operational efficiencies across various end-use industries.

What role does sustainability play in the hydraulic fitting market?

Sustainability is increasingly playing a crucial role in the hydraulic fitting market, driven by stringent environmental regulations and growing corporate responsibility. Manufacturers are focusing on eco-friendly production processes, reducing waste, and minimizing the environmental footprint of their operations. This includes adopting energy-efficient manufacturing techniques and utilizing recyclable materials where feasible.

The demand for hydraulic systems that are more leak-resistant and efficient in fluid usage also contributes to sustainability efforts, as this minimizes fluid loss and potential environmental contamination. Moreover, the long lifespan and reparability of high-quality hydraulic fittings contribute to a circular economy model by extending the product's utility and reducing the need for frequent replacements, aligning with broader sustainability objectives.

Which regions are leading the growth in the hydraulic fitting market?

The Asia Pacific region is currently leading the growth in the hydraulic fitting market, primarily driven by rapid industrialization, extensive infrastructure development projects, and expanding manufacturing sectors in countries like China and India. The substantial investments in construction, agriculture, and automotive industries within this region are generating significant demand for hydraulic components.

Following Asia Pacific, North America and Europe continue to be strong markets, characterized by advanced industrial bases, high adoption rates of automation, and continuous technological innovation. While these regions demonstrate more mature growth, their sustained investment in modernizing existing infrastructure and pioneering new applications ensures their continued prominence in the global hydraulic fitting landscape.

What are the key challenges faced by hydraulic fitting manufacturers?

Hydraulic fitting manufacturers face several key challenges, including the volatility of raw material prices, which can significantly impact production costs and profit margins. The pervasive issue of counterfeit products also poses a considerable threat, undermining product quality, brand reputation, and market integrity, often leading to performance failures and safety concerns.

Additionally, the industry is grappling with a shortage of skilled labor, particularly for specialized roles in design, manufacturing, and maintenance, which can impede innovation and production efficiency. Intense price competition, especially from low-cost manufacturers, further compresses profit margins, necessitating a constant focus on cost optimization and product differentiation to maintain competitiveness in the global market.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted