HSS Tool Market

HSS Tool Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706457 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

HSS Tool Market Size

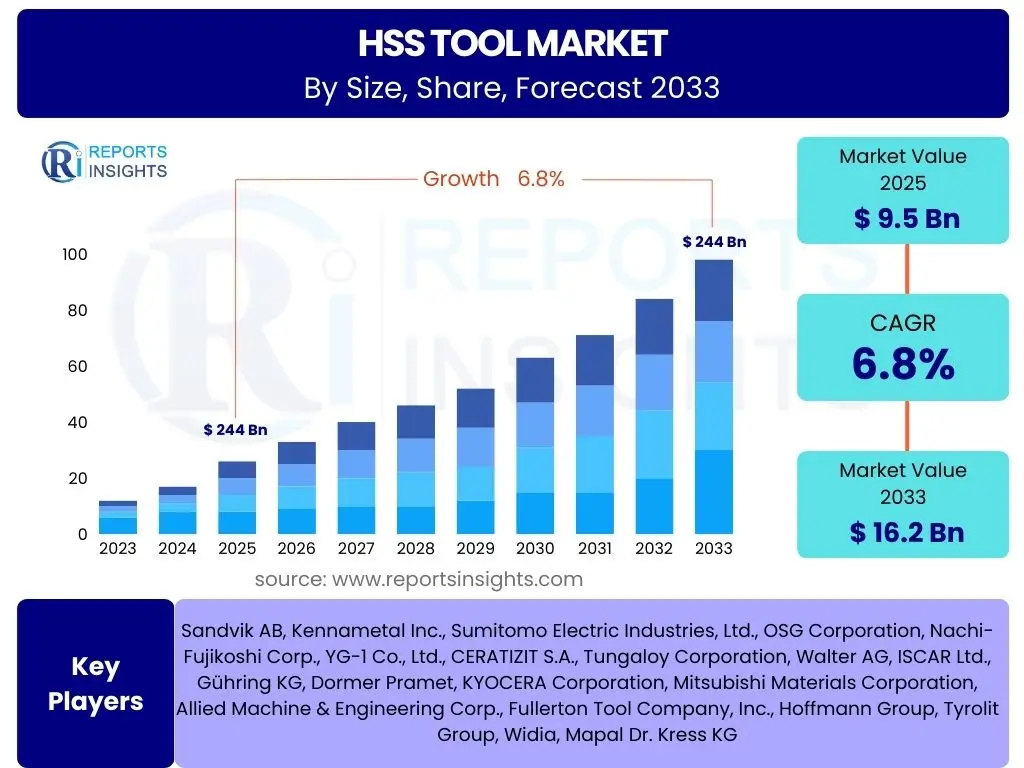

According to Reports Insights Consulting Pvt Ltd, The HSS Tool Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 9.5 Billion in 2025 and is projected to reach USD 16.2 Billion by the end of the forecast period in 2033.

Key HSS Tool Market Trends & Insights

The HSS Tool market is currently undergoing significant transformation, driven by advancements in manufacturing processes and evolving industry demands. A key trend is the increasing adoption of high-performance HSS tools, particularly those with specialized coatings, which enhance tool life and cutting efficiency. This demand is spurred by the need for faster production cycles and improved precision in various end-use industries, including automotive, aerospace, and general manufacturing. Furthermore, the integration of smart manufacturing principles and automation within production environments is fostering the development of HSS tools optimized for automated systems.

Another prominent trend involves the growing emphasis on custom and application-specific HSS tools. Manufacturers are increasingly seeking tailored solutions that can address unique machining challenges, requiring HSS tool producers to offer greater customization capabilities. This trend is complemented by the rising adoption of advanced materials in components, which necessitates more robust and specialized HSS tools capable of machining these difficult-to-cut alloys effectively. The push for sustainability within manufacturing also influences tool design, with a focus on extending tool life to reduce material waste and energy consumption.

Moreover, the digitalization of manufacturing operations, including the use of advanced simulation and design software, is impacting HSS tool development. This allows for more precise tool geometries and optimized performance characteristics before physical prototyping. The global economic landscape and supply chain resilience are also shaping market dynamics, with an increased focus on localized production and diversified sourcing of raw materials to mitigate risks and ensure consistent supply.

- Increased demand for high-performance HSS tools with advanced coatings.

- Growing integration of HSS tools with automation and smart manufacturing systems.

- Rising adoption of custom and application-specific HSS tool solutions.

- Emphasis on sustainability through extended tool life and efficient material usage.

- Digitalization in tool design and manufacturing processes for optimized geometries.

AI Impact Analysis on HSS Tool

The advent of Artificial Intelligence (AI) is poised to significantly impact the HSS Tool market across several dimensions, from design and manufacturing to predictive maintenance and supply chain optimization. AI algorithms can revolutionize the design process by enabling generative design, where optimal tool geometries and material compositions are autonomously identified based on specific performance criteria. This capability shortens development cycles and leads to the creation of HSS tools with superior cutting efficiency, extended tool life, and reduced material consumption, addressing complex machining challenges with unprecedented precision.

In manufacturing, AI-powered systems can enhance production efficiency and quality control. Machine learning models can analyze vast amounts of production data from CNC machines, identifying patterns for process optimization, defect prediction, and real-time adjustments. This leads to higher consistency in HSS tool quality, reduced scrap rates, and improved manufacturing throughput. Furthermore, AI contributes significantly to predictive maintenance of manufacturing equipment, minimizing downtime and extending the lifespan of machinery involved in HSS tool production, thereby reducing operational costs.

Beyond production, AI's influence extends to market forecasting and supply chain management. AI-driven analytics can provide more accurate demand predictions for various HSS tool types, enabling manufacturers to optimize inventory levels and production schedules. This reduces waste and improves responsiveness to market shifts. Additionally, AI can enhance the traceability and efficiency of global supply chains for HSS tool raw materials and finished products, leading to more resilient and cost-effective operations by identifying potential disruptions and optimizing logistics routes.

- AI-driven generative design for optimal HSS tool geometries and material formulations.

- Enhanced manufacturing efficiency and quality control through AI-powered process optimization and defect prediction.

- Improved predictive maintenance for HSS tool production machinery, reducing downtime.

- More accurate market forecasting and optimized inventory management using AI analytics.

- Increased supply chain resilience and efficiency for HSS tool components and finished goods.

Key Takeaways HSS Tool Market Size & Forecast

The HSS Tool market is positioned for steady and robust growth throughout the forecast period, driven by persistent demand from a diverse array of industrial sectors. The projected Compound Annual Growth Rate (CAGR) reflects a healthy expansion trajectory, indicating sustained investment in manufacturing capabilities and the continuous need for high-performance cutting tools. This growth is underpinned by the ongoing industrialization in emerging economies and the modernization of manufacturing infrastructure in developed regions, both of which require reliable and efficient tooling solutions.

A significant takeaway from the market forecast is the increasing value addition within the HSS tool segment. While HSS tools face competition from carbide and ceramic alternatives, their cost-effectiveness, toughness, and versatility ensure their continued relevance, particularly for applications requiring intermittent cutting, high-speed machining of softer materials, or when precise control over chip formation is crucial. The market's expansion is not merely volume-driven but also reflects a shift towards more specialized and coated HSS tools that command higher prices due to their enhanced performance characteristics and longer service life.

Furthermore, the market's trajectory highlights the critical role of innovation in maintaining competitiveness. Manufacturers investing in research and development for new HSS alloys, advanced coatings, and improved tool geometries are likely to capture a larger market share. The forecast suggests that segments driven by precision engineering, such as aerospace and medical device manufacturing, will be key contributors to overall market growth, emphasizing the demand for tools capable of extremely tight tolerances and superior surface finishes. The resilience of the HSS tool market is therefore contingent upon ongoing technological advancements and adaptability to evolving industrial requirements.

- Steady and robust market growth projected with a significant CAGR, indicating sustained demand.

- Increasing value addition within the HSS tool segment due to specialization and advanced coatings.

- Continued relevance of HSS tools due to their cost-effectiveness, toughness, and versatility for specific applications.

- Innovation in HSS alloys, coatings, and geometries is crucial for market competitiveness.

- Precision engineering sectors like aerospace and medical devices will be key growth drivers.

HSS Tool Market Drivers Analysis

The expansion of the HSS Tool market is significantly propelled by the robust growth across various end-use industries, particularly in manufacturing sectors that rely heavily on machining operations. The automotive industry, for instance, continues to be a major consumer of HSS tools for tasks such as drilling, reaming, and milling engine components and chassis parts, driven by increasing vehicle production and the evolution of automotive designs. Similarly, the aerospace and defense sectors demand high-precision HSS tools for machining complex and critical components from various alloys, ensuring the safety and performance of aircraft and defense systems. These industries' consistent demand underpins a foundational growth driver for the HSS tool market.

Another crucial driver is the ongoing global industrialization and infrastructure development, especially in emerging economies. As these regions invest in manufacturing capabilities and construct new facilities, the demand for essential cutting tools like HSS tools naturally escalates. This widespread industrial expansion fuels both the initial outfitting of new production lines and the continuous replacement market for tools. Furthermore, the increasing complexity of manufactured parts and the growing adoption of automated and CNC machining technologies necessitate higher quality and more specialized HSS tools, which contribute to the market's value and volume growth.

Technological advancements in HSS tool manufacturing itself also act as a significant driver. Innovations in HSS material composition, such as the introduction of powder metallurgy HSS (PM HSS), and the development of advanced coatings like TiN, TiCN, and AlTiN, substantially improve tool performance, extend tool life, and enable faster cutting speeds. These enhanced tools lead to greater productivity and cost-efficiency for end-users, thereby increasing their attractiveness and adoption across a wider range of applications. The ongoing research and development into more durable and efficient HSS tool solutions ensure their competitive edge against alternative tool materials for many applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Automotive and Aerospace Industries | +1.5% | Global (USA, Germany, China, India, Japan) | 2025-2033 |

| Increasing Industrialization & Infrastructure Development | +1.2% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Advancements in HSS Tool Materials & Coatings | +1.0% | Global (Developed Economies) | 2025-2033 |

| Rising Adoption of Automated & CNC Machining | +0.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Demand for Cost-Effective and Versatile Cutting Solutions | +0.7% | Global | 2025-2033 |

HSS Tool Market Restraints Analysis

Despite the positive growth trajectory, the HSS Tool market faces several significant restraints that could impede its full potential. A primary challenge is the intense competition from alternative tool materials, particularly carbide tools. Carbide tools offer superior hardness, wear resistance, and the ability to operate at much higher cutting speeds and temperatures, making them preferred for demanding applications involving hard-to-machine materials. While HSS tools remain cost-effective for general-purpose machining, the continuous improvement in carbide manufacturing techniques and cost reduction efforts poses a direct threat to HSS market share in high-performance segments.

Another considerable restraint is the volatility of raw material prices, specifically for high-speed steel alloys which typically contain elements like tungsten, molybdenum, vanadium, and cobalt. Fluctuations in the global prices of these metals, often influenced by geopolitical factors, supply chain disruptions, or speculative trading, directly impact the production costs of HSS tools. This unpredictability makes it challenging for manufacturers to maintain stable pricing, affecting profit margins and potentially leading to price increases that might deter buyers, especially in price-sensitive markets. Supply chain vulnerabilities for these critical raw materials also present a continuous challenge.

Furthermore, the high initial investment required for advanced HSS tool manufacturing technologies and research and development acts as a barrier, particularly for smaller market players. Developing and implementing new HSS alloys, coatings, and precision manufacturing processes requires substantial capital expenditure and a highly skilled workforce. This creates a competitive landscape where larger, more established companies with greater financial resources have an advantage, potentially limiting innovation and market entry for new participants. The environmental regulations concerning the disposal of certain metalworking fluids and tool waste also add to operational complexities and costs for HSS tool manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Carbide and Ceramic Tools | -1.3% | Global (Developed Manufacturing Hubs) | 2025-2033 |

| Volatility of Raw Material Prices | -0.9% | Global | 2025-2030 |

| High Initial Investment in Advanced Manufacturing | -0.6% | Global | 2025-2033 |

| Technological Obsolescence & Innovation Pace | -0.5% | North America, Europe | 2028-2033 |

HSS Tool Market Opportunities Analysis

The HSS Tool market presents compelling opportunities for growth and innovation, particularly through strategic geographical expansion and increased demand for specialized applications. Emerging economies in Asia Pacific, Latin America, and the Middle East & Africa are undergoing rapid industrialization and infrastructure development, creating substantial new markets for HSS tools. As manufacturing bases shift and expand in these regions, there is a growing need for reliable, cost-effective cutting solutions, positioning HSS tools favorably due to their versatility and lower initial cost compared to some alternatives. This demographic and economic shift offers significant potential for market penetration and revenue growth.

Another significant opportunity lies in the development of customized and high-performance HSS tools tailored for specific demanding applications. As industries like aerospace, medical devices, and precision engineering evolve, they require tools capable of machining new, challenging materials with stringent accuracy and surface finish requirements. Investing in R&D to produce HSS tools with novel geometries, advanced coatings (e.g., PVD, CVD, multi-layered), and improved HSS grades (e.g., PM HSS, super HSS) can unlock new market segments and command premium pricing. This focus on niche, high-value applications can differentiate HSS tool manufacturers from competitors and secure long-term contracts.

Furthermore, the growing emphasis on sustainability and circular economy principles provides an opportunity for HSS tool manufacturers. HSS tools are inherently recyclable, and their ability to be resharpened multiple times extends their lifespan, reducing material waste. Promoting these sustainable attributes can appeal to environmentally conscious manufacturers and align with corporate sustainability goals. Additionally, the integration of Industry 4.0 technologies, such as advanced analytics for tool performance monitoring and predictive maintenance, can enhance the value proposition of HSS tools by improving their operational efficiency and optimizing usage in smart manufacturing environments. This digital integration opens avenues for value-added services and stronger customer relationships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Economies (Industrialization) | +1.1% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Development of High-Performance & Customized HSS Tools | +0.9% | Global (Developed Manufacturing Hubs) | 2025-2033 |

| Integration with Industry 4.0 & Smart Manufacturing | +0.7% | North America, Europe, East Asia | 2027-2033 |

| Focus on Sustainable Manufacturing Practices & Recycling | +0.6% | Europe, North America | 2028-2033 |

HSS Tool Market Challenges Impact Analysis

The HSS Tool market confronts several persistent challenges that can hinder its growth and operational efficiency. One significant challenge is the rapid pace of technological advancements in cutting tool materials, particularly the continuous improvements in carbide, ceramic, and super-hard materials. These alternatives often offer superior performance in specific, highly demanding applications, leading to a potential displacement of HSS tools in certain high-value segments. HSS manufacturers must continuously innovate to keep their products competitive in terms of performance characteristics, or risk losing market share to more advanced materials, especially as manufacturing processes become more intricate and require faster, more robust tooling solutions.

Another critical challenge revolves around supply chain complexities and geopolitical instability. The HSS tool industry relies on a global network for sourcing critical raw materials such as tungsten, molybdenum, and cobalt, which are often concentrated in specific geographical regions. Geopolitical tensions, trade disputes, or natural disasters in these regions can lead to severe supply chain disruptions, impacting material availability and increasing costs. Managing these complex global supply chains efficiently and building resilience against unforeseen events is a constant battle for HSS tool manufacturers, directly affecting production schedules and profitability.

Furthermore, the shortage of skilled labor in manufacturing industries globally poses a significant challenge. The effective use and maintenance of HSS tools, especially specialized variants, require a trained workforce proficient in machining operations, tool selection, and process optimization. A lack of skilled machinists and engineers can limit the adoption of advanced HSS tooling, reduce operational efficiency for end-users, and slow down the implementation of new manufacturing technologies. This scarcity impacts not only the demand for HSS tools but also the overall productivity of the industries that rely on them, creating a bottleneck for market expansion.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Advancements of Alternative Tools | -1.0% | Global | 2025-2033 |

| Supply Chain Complexities & Geopolitical Instability | -0.8% | Global | 2025-2030 |

| Shortage of Skilled Labor in Manufacturing Sector | -0.7% | North America, Europe, parts of Asia | 2025-2033 |

| Environmental Regulations & Compliance Costs | -0.4% | Europe, North America | 2026-2033 |

HSS Tool Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global High-Speed Steel (HSS) Tool market, detailing its current size, historical performance, and future growth projections. It offers strategic insights into market dynamics, including key drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. The report segments the market extensively by various parameters, offering granular details on product types, applications, and regional contributions, enabling stakeholders to make informed decisions and identify lucrative growth avenues. It also highlights the competitive landscape by profiling key market players, their strategies, and recent developments.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.5 Billion |

| Market Forecast in 2033 | USD 16.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sandvik AB, Kennametal Inc., Sumitomo Electric Industries, Ltd., OSG Corporation, Nachi-Fujikoshi Corp., YG-1 Co., Ltd., CERATIZIT S.A., Tungaloy Corporation, Walter AG, ISCAR Ltd., Gühring KG, Dormer Pramet, KYOCERA Corporation, Mitsubishi Materials Corporation, Allied Machine & Engineering Corp., Fullerton Tool Company, Inc., Hoffmann Group, Tyrolit Group, Widia, Mapal Dr. Kress KG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The HSS Tool market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for targeted analysis of market performance across different product types, material compositions, and end-use applications, revealing specific growth pockets and demand trends. Understanding these segments is crucial for manufacturers to tailor their product offerings, for suppliers to optimize their distribution channels, and for investors to identify promising areas for strategic investment within the global HSS tool landscape. Each segment responds uniquely to technological advancements and economic shifts, necessitating a detailed breakdown for accurate market assessment.

The market is primarily segmented by product type, encompassing the most commonly used HSS cutting tools, each serving distinct machining purposes. Further division by material type differentiates between conventional HSS grades and advanced powder metallurgy (PM) HSS, reflecting advancements in material science that enhance tool performance. Application-based segmentation highlights the specific machining operations where HSS tools are predominantly utilized, illustrating their versatility across various industrial processes. Finally, end-use industry segmentation provides insight into the primary sectors driving demand, from heavy manufacturing to precision-intensive industries, showcasing the broad applicability of HSS tools.

- By Product Type:

- Drills

- Reamers

- Milling Cutters

- Taps & Dies

- Gear Cutters

- Saw Blades

- Other Cutting Tools

- By Material Type:

- M-Series HSS

- T-Series HSS

- Powder Metallurgy HSS (PM HSS)

- By Application:

- Drilling

- Milling

- Turning

- Threading

- Gear Cutting

- Sawing

- Other Machining Operations

- By End-Use Industry:

- Automotive

- Aerospace & Defense

- General Manufacturing

- Construction

- Medical & Healthcare

- Energy

- Other Industries

- By Sales Channel:

- Direct Sales

- Distributors

- Online Retailers

Regional Highlights

The global HSS Tool market exhibits significant regional disparities, driven by varied levels of industrialization, technological adoption, and economic growth across different geographies. North America and Europe represent mature markets characterized by high demand for precision engineering, aerospace, and automotive components, leading to a strong focus on high-performance and specialized HSS tools. These regions also witness significant adoption of advanced manufacturing techniques and smart factory initiatives, which further influence the demand for advanced HSS tools and their integration into automated systems. Established manufacturing infrastructures and continuous R&D investments define these markets.

Asia Pacific is projected to be the fastest-growing region in the HSS Tool market, primarily due to rapid industrialization, expanding manufacturing bases, and significant foreign direct investments in countries like China, India, Japan, and South Korea. The region's robust automotive, electronics, and general manufacturing sectors are driving substantial demand for HSS tools for mass production and precision applications. Furthermore, the rising labor costs in some APAC countries are accelerating the adoption of automated machining solutions, which, in turn, fuels the demand for high-quality, long-lasting HSS tools. This dynamic economic environment creates numerous opportunities for market expansion and revenue generation.

Latin America and the Middle East & Africa (MEA) are emerging markets for HSS tools, with growth primarily driven by infrastructure development, expanding oil and gas industries, and increasing foreign investment in manufacturing sectors. While currently smaller in market share compared to the developed regions, these areas offer considerable untapped potential as their industrial capabilities continue to evolve. Challenges such as economic volatility and less developed manufacturing ecosystems exist, but the long-term industrialization trends provide a promising outlook for HSS tool market expansion in these regions, particularly for general-purpose and cost-effective tooling solutions.

- North America: Strong demand for precision tools in aerospace and automotive; high adoption of advanced manufacturing.

- Europe: Focus on high-performance and customized HSS tools; robust automotive, machinery, and energy sectors.

- Asia Pacific (APAC): Fastest-growing region due to rapid industrialization, expanding manufacturing base, and automotive sector growth in China, India, Japan, and South Korea.

- Latin America: Growth driven by infrastructure development, automotive manufacturing, and general industrial expansion.

- Middle East and Africa (MEA): Emerging market with potential from oil & gas, construction, and nascent manufacturing industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the HSS Tool Market.- Sandvik AB

- Kennametal Inc.

- Sumitomo Electric Industries, Ltd.

- OSG Corporation

- Nachi-Fujikoshi Corp.

- YG-1 Co., Ltd.

- CERATIZIT S.A.

- Tungaloy Corporation

- Walter AG

- ISCAR Ltd.

- Gühring KG

- Dormer Pramet

- KYOCERA Corporation

- Mitsubishi Materials Corporation

- Allied Machine & Engineering Corp.

- Fullerton Tool Company, Inc.

- Hoffmann Group

- Tyrolit Group

- Widia

- Mapal Dr. Kress KG

Frequently Asked Questions

Analyze common user questions about the HSS Tool market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the HSS Tool Market?

The HSS Tool Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 16.2 Billion by 2033.

Which factors are primarily driving the HSS Tool Market's growth?

Key drivers include the growth of the automotive and aerospace industries, increasing global industrialization and infrastructure development, and continuous advancements in HSS tool materials and coatings.

How do alternative materials like carbide affect the HSS Tool Market?

Competition from carbide and ceramic tools is a significant restraint, as these materials offer superior hardness and wear resistance for demanding applications, potentially impacting HSS tool market share in high-performance segments.

What role does Artificial Intelligence (AI) play in the HSS Tool industry?

AI is influencing HSS tool design through generative approaches, enhancing manufacturing quality control, optimizing production efficiency, enabling predictive maintenance, and improving supply chain management for the industry.

Which geographical regions are key to the HSS Tool Market?

North America and Europe are mature markets for precision tools, while Asia Pacific is the fastest-growing region due to rapid industrialization. Latin America and MEA are emerging markets driven by infrastructure and manufacturing growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted