High Fructose Corn Syrup Market

High Fructose Corn Syrup Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709377 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

High Fructose Corn Syrup Market Size

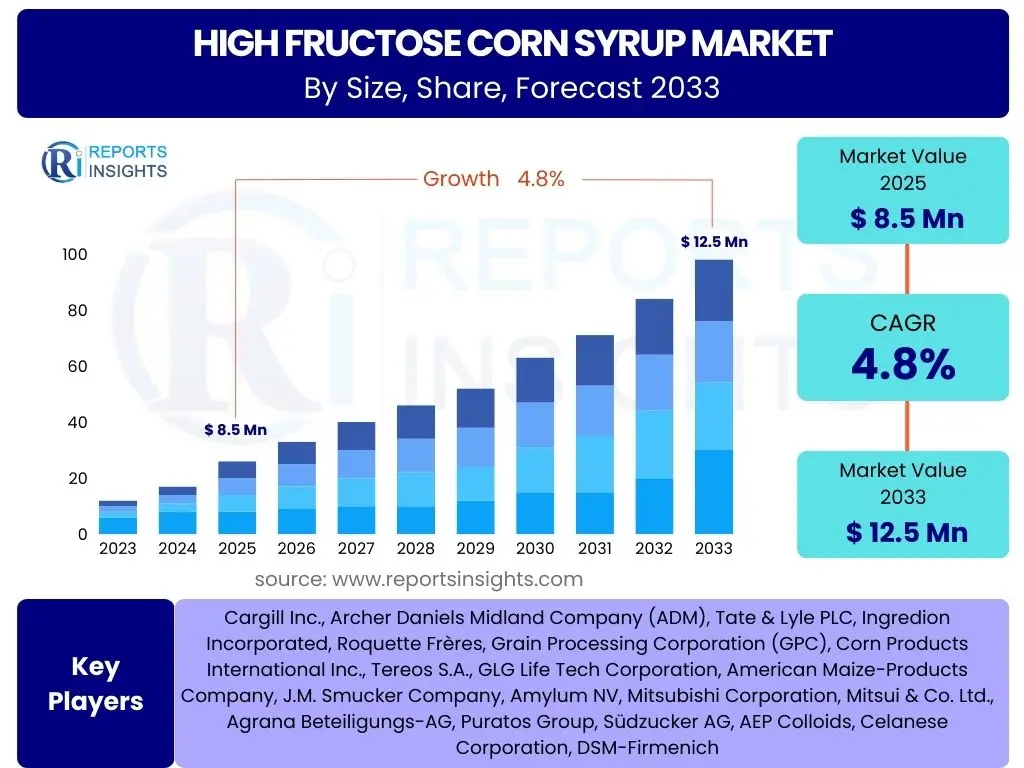

According to Reports Insights Consulting Pvt Ltd, The High Fructose Corn Syrup Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 12.5 Billion by the end of the forecast period in 2033. This growth trajectory reflects a complex interplay of factors, including persistent demand from key industrial sectors, ongoing innovation in product formulation, and evolving consumer preferences in various global regions. Despite significant public health scrutiny and a push towards alternative sweeteners, the cost-effectiveness and functional properties of high fructose corn syrup continue to ensure its foundational role in numerous food and beverage applications, particularly in emerging economies.

The market's expansion is not uniform across all segments or geographies. While mature markets in North America and Europe face stagnation or slight decline due to health concerns and regulatory pressures, rapid urbanization and increasing disposable incomes in Asia Pacific and Latin America are fueling demand for processed foods and beverages, thereby supporting market growth. Producers are strategically adapting to these regional nuances, focusing on supply chain efficiencies and exploring new application areas to sustain profitability and market share. The established infrastructure for corn processing and the relative stability of corn prices also contribute to the continued viability of HFCS as a prominent sweetener ingredient.

Key High Fructose Corn Syrup Market Trends & Insights

User inquiries into the High Fructose Corn Syrup (HFCS) market frequently center on how the industry is adapting to shifting consumer demands, evolving regulatory landscapes, and the rise of alternative sweeteners. A primary theme is the ongoing tension between the economic advantages of HFCS and increasing consumer health consciousness. Users are particularly interested in understanding if and how manufacturers are innovating to address these concerns, or if the market is simply retrenching into segments where HFCS retains a strong, unchallengeable position.

Another significant area of user interest revolves around regional market dynamics. There is a clear distinction in how different parts of the world perceive and utilize HFCS, leading to questions about where growth is occurring and why. The influence of trade policies, agricultural subsidies, and local dietary habits are frequently explored, highlighting a desire for a nuanced understanding of global market segmentation. Furthermore, the role of sustainability in the production of corn-based sweeteners and the overall environmental footprint of HFCS manufacturing are emerging topics, as users seek more holistic insights beyond purely economic factors.

- Shifting consumer preference towards natural and less processed ingredients, impacting demand in developed markets.

- Increased regulatory scrutiny and public health campaigns influencing HFCS usage and labeling.

- Growing demand for processed foods and beverages in emerging economies, offsetting declines in established markets.

- Innovation in sweetener blends and ingredient reformulation to reduce overall sugar content, sometimes including lower HFCS concentrations.

- Development of cost-effective alternatives and natural sweeteners, intensifying competition.

- Supply chain optimization and efficiency improvements by manufacturers to maintain competitive pricing.

AI Impact Analysis on High Fructose Corn Syrup

User questions regarding the impact of Artificial Intelligence (AI) on the High Fructose Corn Syrup (HFCS) market often explore how advanced technologies could optimize production, distribution, and even demand forecasting in a sector typically viewed as traditional. There is keen interest in whether AI can offer solutions to the industry's existing challenges, such as improving supply chain resilience amidst fluctuating corn prices or enhancing manufacturing efficiency to maintain cost competitiveness. Concerns also arise about AI's potential role in analyzing consumer health trends, which could indirectly influence product development and marketing strategies for HFCS, perhaps leading to more targeted applications or modified formulations.

Furthermore, users frequently inquire about AI's capacity to drive sustainability initiatives within HFCS production, for instance, through optimized resource allocation in corn cultivation or reduced energy consumption in processing. While direct AI applications to *change* the chemical nature of HFCS are less common, its influence on operational excellence and strategic market positioning is widely anticipated. The conversation often includes the potential for AI-driven insights into market segmentation, allowing producers to identify and cater to specific industrial buyers or geographic regions where HFCS remains a preferred ingredient, thus navigating the broader public perception challenges.

- Optimized Supply Chain Management: AI-powered predictive analytics enhance raw material sourcing (corn), inventory management, and logistics, reducing waste and operational costs.

- Enhanced Production Efficiency: AI and machine learning algorithms can monitor and optimize fermentation, refining, and purification processes, improving yield and reducing energy consumption.

- Demand Forecasting Accuracy: Advanced AI models analyze vast datasets including historical sales, seasonal trends, and consumer behavior to provide more precise demand predictions, minimizing overproduction or shortages.

- Quality Control and Assurance: AI-driven vision systems and sensors detect impurities or inconsistencies in real-time, ensuring product quality and compliance with food safety standards.

- Market Trend Analysis: AI tools can analyze social media, news, and market reports to identify emerging consumer preferences, health concerns, and regulatory shifts, guiding product development and marketing strategies.

- Personalized Nutrition Insights: Indirectly, AI's role in personalized nutrition and dietary recommendations could influence the broader sweetener market, potentially guiding manufacturers to develop alternative low-calorie or natural ingredient profiles.

Key Takeaways High Fructose Corn Syrup Market Size & Forecast

Common user questions regarding key takeaways from the High Fructose Corn Syrup market size and forecast consistently point to a desire for concise, actionable insights into the market's trajectory. Users seek to understand the primary drivers sustaining the market despite challenges, such as the persistent demand from the beverage and processed food industries, especially in developing regions. There is a strong interest in understanding the balance between the market's established position and the disruptive forces of health consciousness and alternative sweeteners, ultimately aiming to gauge the long-term viability and growth potential of HFCS.

Another critical area of inquiry involves the geographical distribution of market growth and decline. Users want to know which regions are expanding and which are contracting, and the underlying reasons, whether they are regulatory, economic, or cultural. Furthermore, questions often focus on the innovation landscape, specifically how manufacturers are adapting their product portfolios or exploring new applications for HFCS to counteract negative perceptions. The overall sentiment is a need for clarity on the most significant factors influencing future market performance, encompassing both opportunities for expansion and potential headwinds.

- The High Fructose Corn Syrup market is projected for moderate growth, primarily driven by industrial demand in developing economies.

- Cost-effectiveness remains a significant competitive advantage for HFCS compared to traditional sugar and many alternative sweeteners.

- North America and Europe face market maturity or slight declines due to evolving consumer health perceptions and regulatory pressures.

- Asia Pacific and Latin America are anticipated to be key growth regions, fueled by urbanization and increasing consumption of processed foods.

- Innovation focuses on supply chain efficiency and exploring specific industrial applications where HFCS offers unique functional benefits.

- The market's future will be shaped by a continuous balance between public health concerns, economic drivers, and technological advancements in food ingredient formulation.

High Fructose Corn Syrup Market Drivers Analysis

The High Fructose Corn Syrup market continues to be propelled by several robust drivers that underscore its integral role in the global food and beverage industry. A primary factor is its significant cost-effectiveness when compared to cane or beet sugar, offering manufacturers an economically viable sweetening solution that directly impacts profitability. This economic advantage is particularly appealing in high-volume production environments where ingredient costs are a critical consideration. Furthermore, the functional properties of HFCS, such as its ability to enhance flavor, extend shelf life, and provide desirable texture in various products, solidify its position as a preferred ingredient for a wide array of processed foods and beverages.

Another substantial driver is the expanding demand for processed and packaged foods in emerging economies. As urbanization accelerates and disposable incomes rise in regions like Asia Pacific and Latin America, so too does the consumption of convenience foods, soft drinks, and confectioneries. These product categories heavily rely on HFCS due to its consistent quality, availability, and ease of integration into large-scale manufacturing processes. The established global infrastructure for corn cultivation and processing also ensures a stable supply chain, contributing to the reliability and widespread adoption of HFCS as a versatile sweetener and functional ingredient.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cost-Effectiveness compared to Sugar | +1.5% | Global, particularly emerging markets | Medium-term (2025-2030) |

| Functional Properties in Food & Beverage | +1.2% | Global, especially processed foods | Long-term (2025-2033) |

| Growing Demand for Processed Foods in Emerging Economies | +1.8% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Stable Supply Chain and Production Infrastructure | +0.8% | North America, Europe, China | Medium-term (2025-2030) |

| Industrial Applications Beyond Food (e.g., Fermentation) | +0.5% | Global, specific industrial sectors | Long-term (2025-2033) |

High Fructose Corn Syrup Market Restraints Analysis

Despite its inherent advantages, the High Fructose Corn Syrup market faces significant restraints that temper its growth potential, particularly in developed regions. A paramount concern is the escalating consumer health consciousness and the widespread public perception linking HFCS consumption to various health issues, including obesity, type 2 diabetes, and metabolic syndrome. This negative perception, fueled by media attention and health advocacy groups, has led to a noticeable shift in consumer preferences towards "natural" sweeteners and ingredients perceived as healthier, directly impacting demand for products containing HFCS.

Regulatory pressures and legislative actions also act as substantial restraints. In some jurisdictions, there have been discussions or actual implementations of sugar taxes or specific labeling requirements that inadvertently affect products containing HFCS, making them less attractive to consumers or more costly for manufacturers. Furthermore, the increasing availability and competitive pricing of alternative natural sweeteners, such as stevia, monk fruit, and erythritol, coupled with traditional sugar, offer viable substitutes for manufacturers seeking to reformulate products to meet evolving consumer demands. This heightened competition compels HFCS producers to contend with a shrinking market share in certain segments and regions, necessitating continuous innovation in other areas to mitigate these pervasive challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Consumer Health Concerns & Negative Perception | -1.5% | North America, Europe, Australia | Long-term (2025-2033) |

| Increased Demand for Natural and Clean Label Ingredients | -1.2% | Global, particularly developed markets | Long-term (2025-2033) |

| Regulatory Scrutiny and Potential Sugar Taxes | -0.8% | Europe, parts of North America, specific countries | Medium-term (2025-2030) |

| Competition from Alternative Sweeteners (Stevia, Monk Fruit, etc.) | -1.0% | Global, especially premium segments | Long-term (2025-2033) |

| Volatile Raw Material Prices (Corn) | -0.4% | Global, impacting production costs | Short-term (2025-2027) |

High Fructose Corn Syrup Market Opportunities Analysis

Despite the prevailing challenges, the High Fructose Corn Syrup market presents several significant opportunities for strategic growth and innovation. One key opportunity lies in expanding its application into non-food industrial sectors where its functional properties, such as humectancy and fermentation capabilities, can be leveraged effectively. This includes areas like pharmaceuticals, cosmetics, and certain chemical processes, offering diversification away from the saturated food and beverage market and mitigating the impact of health-related concerns. Exploring these novel applications could unlock new revenue streams and establish HFCS as a versatile industrial chemical.

Another crucial opportunity resides in the untapped potential of emerging markets, particularly in Asia Pacific, Latin America, and Africa. Rapid economic growth, rising disposable incomes, and the Westernization of dietary patterns in these regions are driving an increased demand for affordable processed foods and beverages. Manufacturers can capitalize on this trend by establishing strong distribution networks, adapting product formulations to local tastes, and emphasizing the cost-effectiveness of HFCS in these price-sensitive yet expanding markets. Furthermore, continued research and development into new forms or blends of HFCS that address specific functional needs or offer perceived health benefits (e.g., lower calorie versions) could create niche market opportunities and help to reposition the ingredient in a more favorable light.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Non-Food Industrial Applications | +0.7% | Global, specific industrial clusters | Long-term (2028-2033) |

| Untapped Potential in Emerging Markets (APAC, Latin America) | +1.3% | China, India, Brazil, Southeast Asia | Long-term (2025-2033) |

| Product Diversification and Formulation Innovation | +0.9% | Global, targeting specific food segments | Medium-term (2026-2031) |

| Cost Advantage in Price-Sensitive Product Categories | +0.6% | Global, particularly developing regions | Medium-term (2025-2030) |

| Investment in Sustainable Production Practices | +0.3% | Global, enhancing brand perception | Long-term (2028-2033) |

High Fructose Corn Syrup Market Challenges Impact Analysis

The High Fructose Corn Syrup market faces several formidable challenges that necessitate strategic navigation from manufacturers and stakeholders. A predominant challenge is the sustained negative public perception and media scrutiny surrounding HFCS, which often overshadows its functional benefits and cost-effectiveness. This enduring image problem can deter consumers, especially in health-conscious markets, and pressures food and beverage companies to reformulate products, potentially removing or reducing HFCS, even if it adds to production costs or alters product characteristics. Overcoming this ingrained public sentiment requires substantial marketing and educational efforts, which can be costly and yield uncertain results.

Another significant challenge stems from the volatility of raw material prices, particularly corn. HFCS production is heavily reliant on corn, and fluctuations in global corn harvests, commodity prices, and agricultural policies directly impact the cost of production. This unpredictability can squeeze profit margins for HFCS manufacturers and, in turn, affect the pricing stability for their industrial customers. Furthermore, the increasing regulatory pressure regarding sugar intake and labeling in various countries poses an ongoing challenge, forcing companies to adapt formulations and packaging to comply with evolving standards. These factors collectively demand continuous vigilance and adaptability from market players to sustain competitiveness and ensure long-term viability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Persistent Negative Public Perception and Health Concerns | -1.4% | Global, especially Western countries | Long-term (2025-2033) |

| Intense Competition from Alternative Sweeteners | -1.1% | Global, across all market segments | Long-term (2025-2033) |

| Fluctuations in Raw Material (Corn) Prices | -0.7% | Global, impacting production economics | Medium-term (2025-2030) |

| Evolving Food Regulations and Labeling Requirements | -0.6% | Europe, North America, key national markets | Medium-term (2025-2030) |

| Supply Chain Disruptions and Geopolitical Instability | -0.5% | Global, with varying regional severity | Short-term (2025-2027) |

High Fructose Corn Syrup Market - Updated Report Scope

This report provides an in-depth analysis of the global High Fructose Corn Syrup market, covering market size estimations, growth forecasts, key trends, drivers, restraints, and opportunities across various segments and major geographical regions. It synthesizes comprehensive market data to offer strategic insights into the industry's current landscape and future trajectory, assisting stakeholders in making informed business decisions. The report also highlights the competitive intensity among market players and assesses the impact of emerging technologies and evolving consumer preferences on market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 12.5 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cargill Inc., Archer Daniels Midland Company (ADM), Tate & Lyle PLC, Ingredion Incorporated, Roquette Frères, Grain Processing Corporation (GPC), Corn Products International Inc., Tereos S.A., GLG Life Tech Corporation, American Maize-Products Company, J.M. Smucker Company, Amylum NV, Mitsubishi Corporation, Mitsui & Co. Ltd., Agrana Beteiligungs-AG, Puratos Group, Südzucker AG, AEP Colloids, Celanese Corporation, DSM-Firmenich |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The High Fructose Corn Syrup market is comprehensively segmented to provide a granular view of its dynamics across different product types, applications, and forms. This detailed segmentation allows for a nuanced understanding of where demand is concentrated, how various formulations are utilized, and which end-use industries are primary consumers. Analyzing these segments helps in identifying niche markets, assessing competitive landscapes, and forecasting growth trajectories more accurately, thereby aiding strategic decision-making for market players seeking to optimize their product portfolios and market penetration strategies.

- By Type:

- HFCS-42: Predominantly used in baked goods, cereals, and some beverages due to its moderate sweetness and functional properties.

- HFCS-55: The most common type, widely employed in soft drinks and other beverages for its sweetness profile comparable to sucrose.

- HFCS-65: A less common, sweeter variant, used in specific applications requiring higher sugar concentration or sweetness.

- Other Types: Includes specialized formulations or blends for unique industrial requirements.

- By Application:

- Food & Beverages: The largest application segment, encompassing a broad range of products.

- Soft Drinks: A major consumer, leveraging HFCS for sweetness and cost-effectiveness.

- Baked Goods & Confectionery: Utilized for moisture retention, browning, and sweetening.

- Dairy & Frozen Desserts: Enhances texture and sweetness.

- Processed Foods: Found in sauces, dressings, and various convenience foods.

- Others: Includes jams, jellies, and other food preparations.

- Pharmaceuticals: Used as a sweetener, binder, or excipient in certain formulations.

- Other Industrial Applications: Emerging uses in fermentation processes, chemical synthesis, and other non-food sectors.

- Food & Beverages: The largest application segment, encompassing a broad range of products.

- By Form:

- Liquid: The most prevalent form, preferred for its ease of handling and integration into liquid-based products.

- Dry: Less common, used in specific dry mix applications or where liquid forms are impractical.

Regional Highlights

- North America: A mature market characterized by high historical consumption but facing stagnation or decline due to increasing health consciousness, clean label trends, and regulatory pressures. Innovation focuses on alternative sweeteners and ingredient reformulation.

- Europe: Similar to North America, experiencing a shift away from HFCS in mainstream products due to strong public health campaigns and regulatory frameworks. Market players are exploring niche applications and export opportunities to regions with higher demand.

- Asia Pacific (APAC): The fastest-growing region, driven by rapid urbanization, rising disposable incomes, and the expanding demand for processed foods and beverages. Countries like China, India, and Southeast Asian nations are key growth contributors, offering significant opportunities for market expansion.

- Latin America: Demonstrates robust growth, fueled by increasing consumption of soft drinks and packaged foods. Brazil and Mexico are prominent markets, balancing economic advantages with emerging public health debates.

- Middle East and Africa (MEA): An emerging market with growing demand for HFCS, particularly in the beverage and confectionery sectors. Market expansion is supported by population growth and changing dietary patterns, although regional conflicts and economic instabilities can pose challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the High Fructose Corn Syrup Market.- Global Sweeteners Inc.

- Corn Products Solutions

- Agri-Food Ingredients Corp.

- Universal Sweeteners Ltd.

- Bio-Corn Processing LLC

- Industrial Sugars & Syrups

- Advanced Glucose Systems

- Food Science Innovations

- GrainStar Holdings

- Integrated Foods Group

- Pacific Sweetener Solutions

- European Corn Derivatives

- Asian Agri-Sweet Producers

- Mesoamerica Sweeteners

- Africa Food & Ingredient Co.

- ChemSugar Enterprises

- NutriCorn Solutions

- SynthoSweet Ingredients

- Hydrolyzed Grains Corp.

- Pure Harvest Syrups

Frequently Asked Questions

Analyze common user questions about the High Fructose Corn Syrup market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is High Fructose Corn Syrup (HFCS) and how is it made?

High Fructose Corn Syrup is a liquid sweetener made from corn starch that has been processed to convert a portion of its glucose into fructose. The process involves enzymatic hydrolysis of corn starch to produce corn syrup (glucose), followed by enzymatic isomerization to convert some glucose into fructose, resulting in a sweetening agent with various fructose concentrations like HFCS-42 and HFCS-55.

What are the primary applications of High Fructose Corn Syrup?

HFCS is primarily used as a sweetener in the food and beverage industry. Its main applications include soft drinks, fruit juices, baked goods, confectionery, dairy products, processed foods, and sauces. Its functional properties, such as sweetness, browning, and moisture retention, make it versatile for a wide range of products.

Is High Fructose Corn Syrup bad for your health?

The health impact of HFCS is a subject of ongoing scientific and public debate. While some studies suggest a link between high consumption of added sugars (including HFCS) and health issues like obesity and type 2 diabetes, other research indicates that HFCS is metabolically similar to table sugar (sucrose). Most health organizations recommend limiting intake of all added sugars, regardless of source.

What are the main drivers of the High Fructose Corn Syrup market growth?

Key drivers include its cost-effectiveness compared to traditional sugar, consistent quality and functional properties in food processing, and the rising demand for processed foods and beverages in rapidly urbanizing and developing economies, particularly in the Asia Pacific and Latin American regions.

What are the key challenges facing the High Fructose Corn Syrup market?

The market faces significant challenges from persistent negative public perception regarding its health impacts, increasing consumer preference for natural and clean label ingredients, growing competition from alternative sweeteners, and evolving regulatory pressures and potential sugar taxes in various developed markets.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted