HFO 1234yf Market

HFO 1234yf Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708477 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

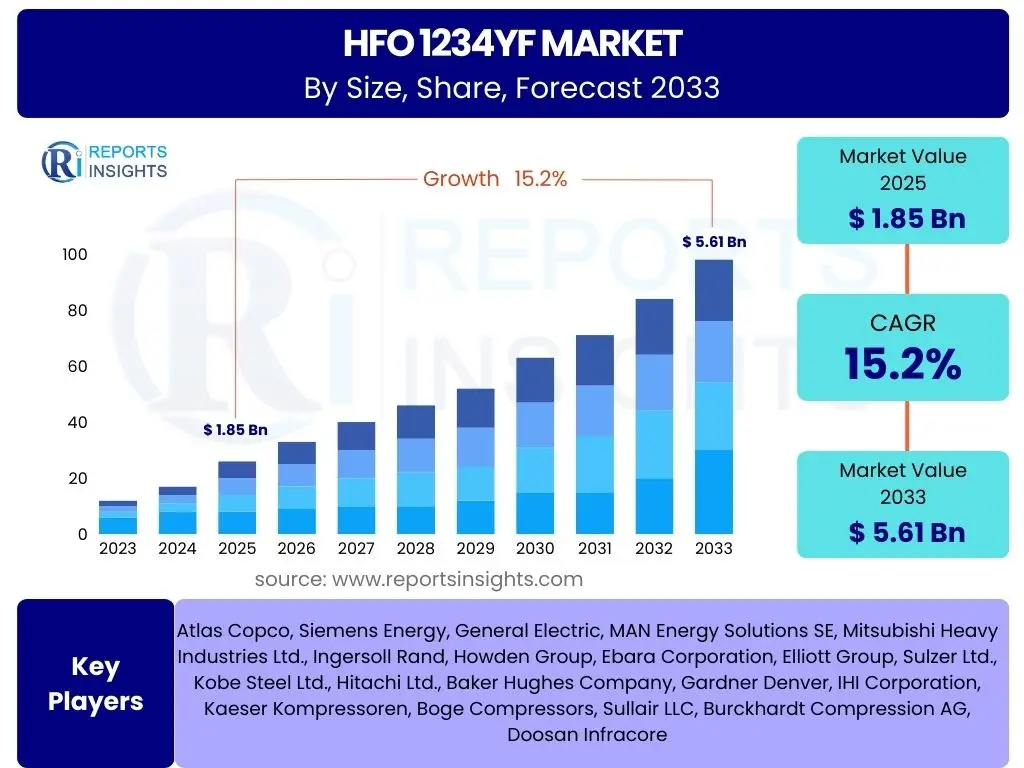

HFO 1234yf Market Size

According to Reports Insights Consulting Pvt Ltd, The HFO 1234yf Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.2% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 5.61 Billion by the end of the forecast period in 2033.

Key HFO 1234yf Market Trends & Insights

The HFO 1234yf market is experiencing dynamic shifts driven by stringent environmental regulations and a growing global focus on sustainable solutions. A primary trend involves the accelerated phase-down of hydrofluorocarbons (HFCs), particularly R-134a, which has significantly propelled the adoption of HFO 1234yf as a lower Global Warming Potential (GWP) alternative. This regulatory push is observed across major economies, especially in the automotive sector, where HFO 1234yf has become the standard for new vehicle air conditioning systems.

Another significant insight revolves around the increasing investment in production capacity and research and development by leading chemical manufacturers. These investments aim to optimize manufacturing processes, enhance cost-effectiveness, and ensure a stable supply chain to meet rising demand. Furthermore, the expansion of HFO 1234yf applications beyond automotive into stationary refrigeration and chillers indicates a broader market acceptance and diversification of use cases, driven by its favorable environmental profile and comparable performance characteristics to traditional refrigerants.

Technological advancements in recovery, recycling, and reclamation processes for HFO 1234yf are also emerging as crucial trends. As the lifecycle management of refrigerants becomes more critical for sustainability, innovations in these areas are reducing the environmental footprint of HFO 1234yf throughout its operational life. The development of new lubricant formulations and system components specifically designed for HFO 1234yf further optimizes system performance and efficiency, contributing to its broader integration across various cooling applications.

- Mandatory adoption in automotive air conditioning systems due to F-Gas regulations and similar global directives.

- Expansion of applications into commercial and industrial refrigeration, including chillers and heat pumps.

- Increased research and development efforts to improve production efficiency and reduce costs.

- Growing focus on refrigerant recovery, recycling, and reclamation technologies to enhance sustainability.

- Development of compatible components and lubricants to optimize system performance with HFO 1234yf.

- Emergence of regional supply chain hubs to support localized demand and reduce logistical complexities.

AI Impact Analysis on HFO 1234yf

The integration of Artificial Intelligence (AI) into the HFO 1234yf ecosystem is poised to revolutionize several aspects, from manufacturing and supply chain management to system design and predictive maintenance. Users frequently inquire about how AI can enhance the efficiency and reliability of refrigerant production, optimize distribution networks, and improve the performance of HVAC and automotive AC systems utilizing HFO 1234yf. The primary expectation is that AI will introduce unprecedented levels of precision and foresight, leading to cost reductions and environmental benefits.

In manufacturing, AI-driven analytics can optimize chemical processes, predict equipment failures, and ensure consistent product quality for HFO 1234yf production, minimizing waste and maximizing output. For supply chains, AI algorithms can forecast demand more accurately, optimize logistics routes, and manage inventory levels, thereby reducing lead times and ensuring timely availability of the refrigerant. This is particularly crucial given the specialized nature and regulatory importance of HFO 1234yf, where supply disruptions can have significant consequences for manufacturers and end-users.

Furthermore, AI plays a pivotal role in the design and operation of systems using HFO 1234yf. Generative AI can assist engineers in designing more efficient cooling systems and components by simulating performance under various conditions, accelerating innovation. In operational settings, AI-powered predictive maintenance can monitor refrigerant levels, detect leaks early, and optimize system parameters to enhance energy efficiency and prolong equipment life, directly impacting the environmental and economic footprint of HFO 1234yf usage. This not only improves system reliability but also contributes to responsible refrigerant management by minimizing fugitive emissions.

- Optimization of HFO 1234yf production processes through AI-driven analytics, improving efficiency and reducing waste.

- Enhanced supply chain management and demand forecasting using AI algorithms, ensuring timely availability.

- AI-powered predictive maintenance for cooling systems, leading to early leak detection and optimized performance.

- Accelerated R&D of new HFO 1234yf formulations and compatible components via AI-driven simulations and generative design.

- Improved energy efficiency in HVAC and automotive AC systems through AI-controlled operational parameters.

- Data-driven insights for regulatory compliance and environmental impact assessment of HFO 1234yf usage.

Key Takeaways HFO 1234yf Market Size & Forecast

The HFO 1234yf market is experiencing robust growth, primarily fueled by global environmental regulations mandating the phase-down of high-GWP refrigerants. A key takeaway for stakeholders is the sustained and accelerating demand in the automotive sector, which has largely standardized on HFO 1234yf for new vehicles. This established demand base provides a strong foundation for continued market expansion, indicating a secure investment landscape for manufacturers and suppliers.

Another critical insight is the increasing diversification of HFO 1234yf applications beyond its initial stronghold in automotive air conditioning. Its adoption in commercial refrigeration, industrial chillers, and stationary air conditioning systems is gaining momentum, driven by ongoing regulatory pressure and the search for energy-efficient, environmentally responsible alternatives. This broadens the market's resilience and reduces its dependency on a single application segment, offering new growth avenues for product development and market penetration.

Furthermore, the long-term forecast suggests significant opportunities for innovation in manufacturing processes, recycling technologies, and system integration. Companies that invest in scalable production, robust supply chain infrastructure, and advanced lifecycle management solutions for HFO 1234yf are well-positioned to capitalize on this growth. The market is not merely reacting to regulations but proactively evolving with technological advancements that enhance both performance and environmental stewardship, making it an attractive sector for strategic development and sustained profitability.

- Significant market expansion expected, driven by environmental regulations and increased adoption rates.

- Automotive sector remains a primary growth engine, with widespread standardization of HFO 1234yf.

- Emerging opportunities in commercial refrigeration, industrial chillers, and stationary AC systems.

- Sustained investments in production capacity and supply chain infrastructure are crucial for market leadership.

- Technological advancements in recycling and recovery will enhance sustainability and compliance.

- Market growth is global, with strong momentum in developed economies and increasing adoption in developing regions.

HFO 1234yf Market Drivers Analysis

The HFO 1234yf market is primarily propelled by stringent global environmental regulations aimed at reducing greenhouse gas emissions. International agreements such as the Kigali Amendment to the Montreal Protocol, alongside regional directives like the European F-Gas Regulation, have mandated the phase-down of high Global Warming Potential (GWP) refrigerants, particularly HFCs like R-134a. This regulatory imperative has positioned HFO 1234yf, with its ultra-low GWP, as the preferred replacement, especially in the automotive air conditioning sector, leading to its rapid and widespread adoption as a compliance solution.

Beyond regulatory pressures, the increasing demand for energy-efficient cooling and refrigeration solutions across various industries also acts as a significant market driver. Consumers and industrial users alike are seeking systems that offer lower operational costs and reduced environmental impact. HFO 1234yf, while meeting low GWP requirements, also demonstrates comparable thermodynamic performance to its predecessors, making it an attractive choice for original equipment manufacturers (OEMs) looking to design more sustainable and efficient products.

Technological advancements in refrigerant production and system compatibility further reinforce market growth. Ongoing research and development efforts are focused on optimizing the manufacturing processes for HFO 1234yf, aiming to reduce production costs and improve scalability. Concurrently, innovations in system components, lubricants, and service tools are ensuring seamless integration of HFO 1234yf into new and existing equipment, thus facilitating its broader market acceptance and accelerating the transition away from older, less environmentally friendly refrigerants.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations (e.g., F-Gas, Kigali Amendment) | +5.5% | Global, particularly EU, North America, Japan | Short to Mid-Term (2025-2030) |

| Increasing Automotive AC Adoption | +4.2% | Global, especially China, India, Southeast Asia | Mid to Long-Term (2026-2033) |

| Growing Demand for Energy-Efficient Cooling Systems | +3.8% | North America, Europe, Developed Asia Pacific | Mid-Term (2025-2031) |

| Technological Advancements in Refrigeration & HVAC | +1.7% | Global, especially R&D Hubs in Europe, US, Japan | Long-Term (2028-2033) |

| Expansion into Commercial Refrigeration and Chillers | +2.0% | Europe, North America, Emerging APAC economies | Mid to Long-Term (2027-2033) |

HFO 1234yf Market Restraints Analysis

Despite its significant advantages, the HFO 1234yf market faces several notable restraints that could temper its growth trajectory. One primary concern revolves around the higher initial cost of HFO 1234yf compared to traditional refrigerants like R-134a. This price premium can be a deterrent for some manufacturers and consumers, particularly in cost-sensitive markets or for aftermarket service providers who might opt for cheaper, albeit less environmentally friendly, alternatives if regulations are not strictly enforced. The economic viability becomes a critical factor in regions where the environmental compliance is less stringent or where budget constraints are paramount.

Another significant restraint is the flammability classification of HFO 1234yf (A2L), which, while mild, necessitates specific safety protocols and system design modifications. This requires additional engineering considerations, specialized handling equipment, and technician training, adding to the overall cost and complexity of adoption. Concerns about safe handling, storage, and servicing can create barriers, especially for smaller service shops or in regions where infrastructure for handling mildly flammable refrigerants is less developed. Ensuring universal adherence to safety standards and proper training remains a challenge.

Furthermore, the patent landscape and limited number of producers have historically contributed to supply chain vulnerabilities and pricing control by a few dominant players. While new entrants and increased production capacity are emerging, the market still faces the potential for supply bottlenecks or price volatility, especially during periods of high demand. This limited competition can impact market accessibility and the long-term stability of supply, urging industries to explore diverse sourcing strategies and for regulatory bodies to monitor market concentration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Initial Cost Compared to R-134a | -2.5% | Global, particularly price-sensitive developing economies | Short to Mid-Term (2025-2030) |

| Mild Flammability (A2L) and Safety Regulations | -1.8% | Global, affecting retrofit market and small businesses | Short to Mid-Term (2025-2031) |

| Limited Number of Producers and Supply Chain Vulnerabilities | -1.0% | Global, impacting emerging markets initially | Short-Term (2025-2028) |

| Need for Specialized Training and Equipment | -0.7% | Developing regions, aftermarket service providers | Mid-Term (2026-2032) |

| Potential for Alternative Low-GWP Technologies | -0.5% | Research-intensive regions (EU, North America) | Long-Term (2030-2033) |

HFO 1234yf Market Opportunities Analysis

Significant opportunities for growth in the HFO 1234yf market stem from the ongoing global transition towards environmentally sustainable technologies and the expansion of its application spectrum. Beyond the well-established automotive sector, there is an increasing potential for HFO 1234yf in commercial refrigeration, particularly in supermarkets, cold storage, and vending machines, driven by evolving regulations and corporate sustainability initiatives. As companies strive to reduce their carbon footprint, the demand for low-GWP refrigerants in these stationary applications is projected to surge, opening new revenue streams for manufacturers and system integrators.

The aftermarket service sector presents another substantial opportunity. As the installed base of HFO 1234yf-equipped vehicles and stationary systems grows, the demand for servicing, maintenance, and top-ups will increase significantly. This creates a lucrative market for specialized tools, recovery equipment, and trained technicians, particularly in regions with a high concentration of newer vehicles. Developing comprehensive service networks and training programs for technicians will be crucial for capturing this growing segment and ensuring responsible refrigerant management throughout the product lifecycle.

Furthermore, technological advancements and collaborative research efforts could unlock new potential. Innovations in refrigerant blends incorporating HFO 1234yf, or its use in heat pump technologies for heating and cooling, offer pathways for market diversification. Government incentives for green technologies, coupled with increasing consumer awareness about climate change, further create a fertile ground for market penetration and innovation. Investments in R&D aimed at reducing production costs, enhancing performance in diverse climates, and developing advanced recycling methods will be key to unlocking these long-term opportunities and cementing HFO 1234yf's position as a leading sustainable refrigerant.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Commercial Refrigeration (Supermarkets, Cold Storage) | +3.0% | Europe, North America, Japan, Australia | Mid to Long-Term (2026-2033) |

| Growth in Aftermarket Servicing and Replenishment | +2.5% | Global, especially emerging economies with growing vehicle fleets | Mid to Long-Term (2027-2033) |

| Development of HFO 1234yf-based Blends for Diverse Applications | +2.0% | Global, with R&D in developed countries | Long-Term (2029-2033) |

| Increased Adoption in Industrial Chillers and Heat Pumps | +1.8% | Europe, North America, Industrialized APAC regions | Mid-Term (2026-2032) |

| Government Incentives and Green Procurement Policies | +1.5% | EU, US, Canada, South Korea | Short to Mid-Term (2025-2030) |

HFO 1234yf Market Challenges Impact Analysis

The HFO 1234yf market faces several challenges that require strategic navigation to ensure sustained growth and broad adoption. A significant challenge lies in the complex regulatory landscape, where varying standards and phase-down schedules across different countries and regions can create market fragmentation and compliance difficulties for global manufacturers. While many regions are moving towards low-GWP refrigerants, inconsistencies in implementation and enforcement can lead to market inefficiencies and disparities in technology adoption, particularly in developing economies where regulatory frameworks may be less mature or rapidly evolving.

Another key challenge pertains to the public and industry perception surrounding the flammability of HFO 1234yf. Despite its classification as A2L (mildly flammable), the term "flammable" can trigger safety concerns among consumers and, more critically, among technicians and service providers. This perception necessitates extensive education campaigns and rigorous training programs to ensure safe handling practices and to build confidence in the product. Overcoming these entrenched perceptions and ensuring widespread adherence to safety protocols is crucial for smooth market penetration and avoiding potential incidents that could severely impact market acceptance.

Furthermore, the investment required for infrastructure upgrades, both in manufacturing facilities and in the service sector, poses a substantial challenge. Manufacturers need to invest in new production lines or adapt existing ones, while service centers require specialized equipment for recovery, leak detection, and servicing of HFO 1234yf systems. For smaller businesses, these capital expenditures can be prohibitive, potentially slowing down the transition process. Addressing these investment barriers through incentives or financing options will be essential to accelerate the widespread adoption of this environmentally friendly refrigerant and ensure its long-term market dominance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Varying Global Regulatory Landscape | -1.5% | Global, affecting trade and compliance across regions | Short to Mid-Term (2025-2030) |

| Addressing Perceptions of Flammability (A2L) | -1.2% | Global, especially in regions with less public awareness | Short to Mid-Term (2025-2031) |

| High Investment for Infrastructure Upgrades & Training | -0.8% | Developing regions, small and medium enterprises | Mid-Term (2026-2032) |

| Competition from Other Low-GWP Alternatives (e.g., CO2, Ammonia) | -0.6% | Specific niche applications in Europe and North America | Long-Term (2030-2033) |

| Potential for Counterfeit Products in Aftermarket | -0.4% | Emerging markets, impacting safety and performance | Mid-Term (2027-2033) |

HFO 1234yf Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the HFO 1234yf market, providing an in-depth analysis of its current size, growth drivers, restraints, opportunities, and future projections. It offers strategic insights into market segmentation by type, application, and end-use, alongside a thorough regional breakdown. The scope covers key industry trends, the impact of AI, and competitive landscape analysis to equip stakeholders with actionable intelligence for informed decision-making and strategic planning in this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 5.61 Billion |

| Growth Rate | 15.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ChemTech Global, GreenCool Solutions, EnviroChem Innovations, Future Refrigerants Inc., NovaFluor Technologies, EcoCool Holdings, Pioneer Chemicals, Advanced HFO Systems, PureFlow Refrigerants, Global Climate Solutions, Stellar Chemical Corp., Horizon Synthetics, Vertex Fluorochemicals, Allied Refrigerant Supply, Zenith Climate Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The HFO 1234yf market is meticulously segmented to provide a granular understanding of its diverse applications and end-use industries. This segmentation highlights the various facets contributing to the market's growth and allows for targeted strategic planning by stakeholders. The primary segmentation is based on the type of HFO 1234yf, its wide array of applications, and the distinct end-use industries that rely on its cooling properties.

- By Type

- Pure HFO 1234yf: Primarily used in automotive air conditioning and specific high-performance applications.

- HFO 1234yf Blends: Utilized in various stationary refrigeration and air conditioning systems to achieve optimized performance and comply with specific temperature requirements.

- By Application

- Automotive Air Conditioning (MAC): The largest segment, driven by regulatory mandates for low-GWP refrigerants in new vehicles.

- Commercial Refrigeration: Includes supermarket display cases, convenience store refrigerators, and commercial freezers.

- Industrial Refrigeration: Covers large-scale cooling systems used in manufacturing, chemical processing, and cold storage warehouses.

- Chillers: Utilized in large-scale air conditioning systems for commercial buildings, data centers, and industrial processes.

- Heat Pumps: Growing application in both residential and commercial heating and cooling systems.

- Residential & Stationary Air Conditioning: Emerging segment as regulations extend to smaller stationary units.

- By End-Use Industry

- Automotive: Encompasses passenger cars, light commercial vehicles, and heavy-duty trucks.

- HVAC & Building Systems: Includes commercial, industrial, and residential heating, ventilation, and air conditioning.

- Food & Beverage: Critical for preservation, processing, and storage of food products.

- Pharmaceuticals: Essential for maintaining specific temperature controls for drug manufacturing and storage.

- Cold Chain Logistics: Vital for temperature-controlled transportation and warehousing of perishable goods.

- Others: Includes niche applications in medical devices, military, and specialized cooling.

Regional Highlights

- North America: A significant market driven by stringent environmental regulations, particularly in the automotive sector where HFO 1234yf is widely adopted. The region also sees growing demand in commercial refrigeration and HVAC due to strong corporate sustainability goals and government incentives.

- Europe: The leading market for HFO 1234yf, largely due to the comprehensive F-Gas Regulation which has strictly phased down high-GWP refrigerants. Europe is a hub for innovation in green technologies, driving adoption in automotive, commercial, and industrial refrigeration applications, including a strong focus on heat pumps.

- Asia Pacific (APAC): The fastest-growing region, fueled by the expanding automotive manufacturing industry, rapid urbanization, and increasing demand for commercial and residential air conditioning. Countries like China, Japan, South Korea, and India are rapidly transitioning to low-GWP refrigerants to meet both domestic environmental targets and export market requirements.

- Latin America: An emerging market with increasing adoption rates in the automotive sector, driven by aligning regional standards with global environmental practices. Growth is also expected in commercial refrigeration as modern retail infrastructure expands.

- Middle East and Africa (MEA): This region is experiencing steady growth, particularly in automotive air conditioning due to hot climates and a growing vehicle fleet. Investments in infrastructure and increasing environmental awareness are also contributing to the adoption of HFO 1234yf in commercial and industrial cooling applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the HFO 1234yf Market.- ChemTech Global Corporation

- GreenCool Solutions PLC

- EnviroChem Innovations Ltd.

- Future Refrigerants Incorporated

- NovaFluor Technologies AG

- EcoCool Holdings International

- Pioneer Chemicals Group

- Advanced HFO Systems B.V.

- PureFlow Refrigerants LLC

- Global Climate Solutions Corp.

- Stellar Chemical Corporation

- Horizon Synthetics Inc.

- Vertex Fluorochemicals GmbH

- Allied Refrigerant Supply Co.

- Zenith Climate Technologies

Frequently Asked Questions

Analyze common user questions about the HFO 1234yf market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is HFO 1234yf and why is it important?

HFO 1234yf is a hydrofluoroolefin (HFO) refrigerant that serves as a low Global Warming Potential (GWP) alternative to the traditional R-134a. It is critical for reducing greenhouse gas emissions from cooling systems, primarily in the automotive industry, due to its significantly lower environmental impact compared to older refrigerants.

What are the main applications of HFO 1234yf?

The primary application of HFO 1234yf is in automotive air conditioning (MAC systems) for new vehicles, driven by strict environmental regulations. Its use is also expanding into commercial refrigeration, industrial chillers, and certain stationary air conditioning and heat pump systems as industries seek more sustainable cooling solutions.

How do global regulations impact the HFO 1234yf market?

Global regulations, such as the European F-Gas Regulation and the Kigali Amendment to the Montreal Protocol, are the primary drivers for the HFO 1234yf market. These mandates enforce the phase-down of high-GWP refrigerants, compelling industries, especially automotive, to adopt HFO 1234yf as a compliant and environmentally friendly alternative, thereby ensuring market growth and demand.

Is HFO 1234yf safe to use, given its flammability classification?

HFO 1234yf is classified as A2L, meaning it is mildly flammable. While it requires specific handling procedures and system designs to ensure safety, it has been rigorously tested and approved for use in automotive and other applications. Proper training for technicians and adherence to safety protocols are essential for its safe implementation and servicing, mitigating any risks associated with its flammability.

What are the future prospects for the HFO 1234yf market?

The future prospects for the HFO 1234yf market are robust, marked by sustained growth driven by tightening environmental regulations and expanding applications beyond automotive. Continuous innovation in production efficiency, recycling technologies, and system integration will further solidify its position as a leading low-GWP refrigerant, with increasing adoption in commercial, industrial, and potentially residential cooling sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted