Hereditary Cancer Testing Market

Hereditary Cancer Testing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708586 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

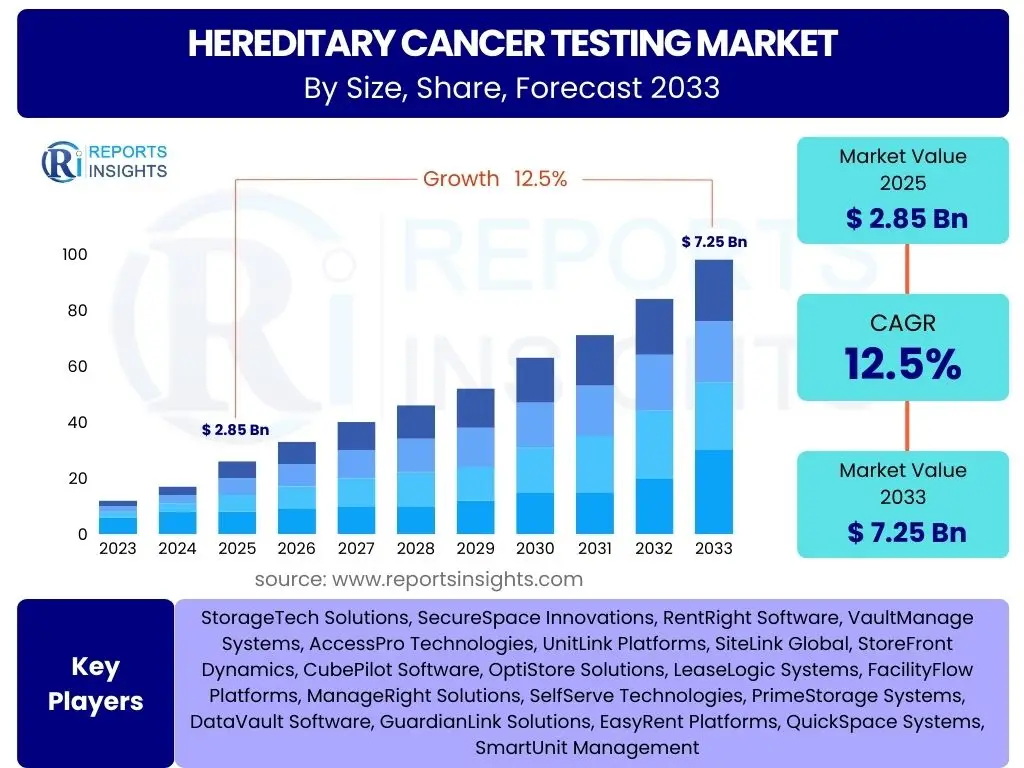

Hereditary Cancer Testing Market Size

According to Reports Insights Consulting Pvt Ltd, The Hereditary Cancer Testing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 7.25 billion by the end of the forecast period in 2033.

Key Hereditary Cancer Testing Market Trends & Insights

The hereditary cancer testing market is undergoing significant transformation driven by advancements in genomic technologies and increasing awareness regarding personalized medicine. A prominent trend involves the shift from single-gene testing to comprehensive multi-gene panel tests, which offer a more holistic risk assessment for various cancer types. This shift is fueled by the falling cost of next-generation sequencing (NGS) and the growing understanding of complex genetic interactions influencing cancer susceptibility.

Furthermore, there is a rising adoption of direct-to-consumer (DTC) genetic testing services, making hereditary cancer testing more accessible to the general population, although regulatory scrutiny and the need for genetic counseling remain crucial aspects. The integration of liquid biopsy for early cancer detection and monitoring, alongside its potential for identifying germline mutations, represents another critical emerging trend. These advancements are collectively enhancing the precision, accessibility, and utility of hereditary cancer diagnostics, paving the way for more targeted prevention and treatment strategies.

- Shift towards comprehensive multi-gene panel testing.

- Increased adoption of Next-Generation Sequencing (NGS) technologies.

- Growing acceptance of direct-to-consumer (DTC) genetic testing.

- Emergence of liquid biopsy applications for germline mutation screening.

- Expansion of hereditary cancer screening guidelines for broader populations.

- Increased focus on preventive medicine and personalized risk assessment.

AI Impact Analysis on Hereditary Cancer Testing

Artificial intelligence (AI) is poised to revolutionize hereditary cancer testing by enhancing various stages of the diagnostic workflow, from data interpretation to patient management. Users are increasingly curious about how AI can improve the accuracy and speed of variant analysis, given the vast amounts of genomic data generated by NGS. AI algorithms are adept at identifying subtle genetic variations, correlating them with disease phenotypes, and predicting pathogenicity, thereby reducing the burden on clinical geneticists and accelerating diagnostic turnaround times.

Moreover, AI tools are expected to play a critical role in personalized risk assessment and treatment planning. By integrating genetic data with clinical histories, lifestyle factors, and epidemiological information, AI can develop more precise predictive models for cancer risk and guide tailored therapeutic interventions. Common concerns, however, revolve around data privacy, the validation of AI models in diverse populations, and ensuring equitable access to these advanced technologies. Despite these challenges, the overarching expectation is that AI will significantly enhance the efficiency, accuracy, and utility of hereditary cancer testing, moving closer to truly personalized healthcare.

- Accelerated and more accurate interpretation of complex genomic data.

- Enhanced identification of pathogenic and likely pathogenic variants.

- Improved personalized cancer risk assessment models.

- Optimized clinical decision support for targeted therapies.

- Streamlined laboratory workflows and reduced manual errors.

- Facilitated integration of multi-omic data for holistic patient profiles.

Key Takeaways Hereditary Cancer Testing Market Size & Forecast

The hereditary cancer testing market demonstrates robust growth, driven by an escalating global cancer burden and the increasing integration of precision medicine into clinical practice. The substantial projected Compound Annual Growth Rate (CAGR) highlights the market's dynamic expansion, reflecting rising awareness among both healthcare providers and patients regarding the benefits of early risk assessment and proactive cancer management. This growth is further propelled by technological advancements, particularly in genomic sequencing, which are making testing more comprehensive and cost-effective.

Key insights indicate a sustained demand for multi-gene panel tests over single-gene assays, reflecting a move towards more thorough genetic profiling. Furthermore, the market's trajectory is strongly influenced by evolving reimbursement policies and expanding clinical guidelines that recommend genetic testing for a broader range of individuals. The shift towards preventative health, coupled with the potential for AI to enhance diagnostic capabilities, positions the hereditary cancer testing sector as a critical component of future oncology strategies, impacting patient outcomes through earlier intervention and highly individualized care.

- Significant market expansion driven by technological advancements and awareness.

- Strong preference for multi-gene panel tests for comprehensive risk assessment.

- Growing importance of genetic counseling to support test interpretation.

- Impact of evolving regulatory frameworks and reimbursement policies on market access.

- Increasing adoption in preventative care and personalized medicine initiatives.

- Emerging markets present substantial opportunities for future growth.

Hereditary Cancer Testing Market Drivers Analysis

The hereditary cancer testing market is significantly propelled by the increasing global incidence of various cancer types, which drives the demand for early detection and risk stratification. As cancer prevalence rises, there is a corresponding surge in the number of individuals seeking to understand their genetic predisposition, leading to greater adoption of genetic screening. This heightened awareness among both medical professionals and the general public about the benefits of identifying hereditary cancer risks early empowers proactive management strategies, including intensified surveillance and prophylactic interventions. Technological advancements, particularly in Next-Generation Sequencing (NGS) and multi-gene panel tests, have made testing more comprehensive, accurate, and cost-effective, further accelerating market growth by expanding the utility and accessibility of these diagnostic tools.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Cancer Incidence and Prevalence | +1.5% | Global | Long-term |

| Advancements in Genomic Technologies (NGS, Multi-gene Panels) | +1.8% | North America, Europe, APAC | Mid to Long-term |

| Growing Awareness and Adoption of Personalized Medicine | +1.2% | Global | Mid-term |

| Expanding Clinical Guidelines for Genetic Testing | +0.9% | North America, Europe | Mid-term |

Hereditary Cancer Testing Market Restraints Analysis

Despite robust growth, the hereditary cancer testing market faces several significant restraints that could impede its full potential. The high cost associated with advanced genetic testing, especially for comprehensive panels or whole-exome sequencing, remains a major barrier for many patients and healthcare systems, particularly in regions with developing economies or limited insurance coverage. Furthermore, the complexities surrounding reimbursement policies, which vary significantly by region and insurer, can create uncertainty and limit patient access to these critical diagnostic services. Ethical considerations, including concerns about genetic discrimination, data privacy, and the psychological impact of receiving a positive test result, also contribute to hesitancy among individuals and healthcare providers. Additionally, a shortage of trained genetic counselors and clinical geneticists poses a challenge to adequately interpret test results and provide appropriate guidance, which is crucial for informed decision-making.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Genetic Testing | -1.0% | Global, particularly emerging markets | Mid-term |

| Varying Reimbursement Policies and Coverage Limitations | -0.8% | Global | Mid-term |

| Ethical Concerns and Data Privacy Issues | -0.5% | Global | Long-term |

| Shortage of Skilled Genetic Counselors and Professionals | -0.7% | Global | Long-term |

Hereditary Cancer Testing Market Opportunities Analysis

The hereditary cancer testing market is rich with opportunities, primarily driven by the expansion into emerging markets where healthcare infrastructure is developing, and awareness is growing. Regions such as Asia Pacific and Latin America present significant untapped potential due to their large populations and rising disposable incomes. The integration of hereditary cancer testing with liquid biopsy technologies represents a substantial opportunity, allowing for less invasive sampling and potentially broader screening applications. Furthermore, the growing trend of direct-to-consumer (DTC) genetic testing, while facing regulatory challenges, opens new avenues for market penetration by increasing public access and engagement with genetic health information. Strategic collaborations between diagnostic companies, pharmaceutical firms, and research institutions also foster innovation and accelerate the development of novel tests and companion diagnostics, unlocking new market segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +1.0% | APAC, LATAM, MEA | Long-term |

| Integration with Liquid Biopsy and Companion Diagnostics | +1.3% | North America, Europe, APAC | Mid to Long-term |

| Growth in Direct-to-Consumer (DTC) Genetic Testing | +0.7% | North America, Europe | Mid-term |

| Strategic Partnerships and Collaborations | +0.6% | Global | Mid-term |

Hereditary Cancer Testing Market Challenges Impact Analysis

The hereditary cancer testing market faces several critical challenges that require strategic navigation to ensure sustainable growth and public trust. A primary challenge involves the accurate and consistent interpretation of genetic variants, especially variants of uncertain significance (VUS), which can lead to patient anxiety and complicate clinical decision-making. The sheer volume of genetic data generated necessitates robust bioinformatics pipelines and expert clinical review, which are often resource-intensive. Ensuring the highest standards of data privacy and security is another paramount concern, given the highly sensitive nature of genetic information, with breaches potentially leading to severe consequences. Furthermore, educating both healthcare providers and the public about the nuances, benefits, and limitations of hereditary cancer testing remains a persistent challenge, crucial for overcoming misinformation and ensuring appropriate test utilization.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexities in Variant Interpretation and Management of VUS | -0.6% | Global | Long-term |

| Data Privacy and Security Concerns | -0.4% | Global | Long-term |

| Lack of Standardized Regulatory Frameworks | -0.5% | Global | Mid-term |

| Need for Public and Professional Education | -0.3% | Global | Long-term |

Hereditary Cancer Testing Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the hereditary cancer testing market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers a forecast period from 2025 to 2033, examining historical data and current market conditions to project future growth trajectories. The scope includes an assessment of key drivers, restraints, opportunities, and challenges influencing market expansion, alongside the impact of emerging technologies like AI and the evolving regulatory environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 7.25 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Agilent Technologies, Thermo Fisher Scientific, Illumina, QIAGEN, Roche Diagnostics, Myriad Genetics, Invitae, Color Health, Exact Sciences, Guardant Health, Natera, NeoGenomics Laboratories, Centogene, Fulgent Genetics, SOPHiA GENETICS, Ambry Genetics, Quest Diagnostics, Eurofins Scientific, F. Hoffmann-La Roche Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The hereditary cancer testing market is extensively segmented to provide a granular view of its diverse components and their respective growth dynamics. This segmentation facilitates a deeper understanding of market trends, consumer preferences, and technological adoption across various dimensions. The market is primarily analyzed by test type, technology employed, specific cancer types targeted, end-user applications, and geographical regions. Each segment represents a unique set of market drivers and competitive landscapes, contributing distinctively to the overall market valuation and future growth potential, reflecting the complex interplay of clinical needs, technological capabilities, and economic factors.

- By Test Type: This segment includes Single Gene Tests, which focus on specific gene mutations known to be associated with cancer, and Multi-Gene Panel Tests, which screen for multiple genes simultaneously, offering a broader risk assessment. More advanced options like Whole Exome Sequencing (WES) and Whole Genome Sequencing (WGS) provide comprehensive genetic information, while Chromosomal Microarray (CMA) detects larger chromosomal abnormalities. The shift towards multi-gene panels and next-generation sequencing is prominent due to their cost-effectiveness and comprehensive nature.

- By Technology: Key technologies driving the market include Next-Generation Sequencing (NGS), which enables high-throughput and cost-efficient genetic analysis, and Polymerase Chain Reaction (PCR), used for targeted amplification. Fluorescence In Situ Hybridization (FISH) is utilized for detecting specific chromosomal rearrangements, while Microarray technology allows for the simultaneous detection of thousands of genetic variations. Other emerging technologies continue to contribute to diagnostic precision and accessibility.

- By Cancer Type: Segmentation by cancer type addresses the specific genetic predispositions for various cancers. Major categories include Breast Cancer, Ovarian Cancer, Colorectal Cancer, Prostate Cancer, Melanoma, and Pancreatic Cancer, each with distinct genetic markers and testing protocols. A broader category of Other Cancer Types encompasses less common hereditary syndromes, highlighting the diverse application of these tests across oncology.

- By End User: The end-user segment outlines where these tests are primarily utilized. Hospitals and Clinics represent the largest user base, integrating tests into patient care pathways. Diagnostic Laboratories perform a significant volume of tests for various clients. Research & Academic Institutions contribute to developing new markers and technologies. Pharmaceutical & Biopharmaceutical Companies use these tests for drug development and companion diagnostics. Direct-to-Consumer (DTC) services are gaining traction, making testing accessible outside traditional clinical settings.

- By Region: Geographical segmentation includes North America, Europe, Asia Pacific (APAC), Latin America, and Middle East & Africa (MEA). Each region exhibits unique market characteristics based on healthcare infrastructure, cancer prevalence, regulatory environment, and economic development, influencing the adoption and growth of hereditary cancer testing.

Regional Highlights

North America currently dominates the hereditary cancer testing market, driven by advanced healthcare infrastructure, high awareness regarding genetic testing, favorable reimbursement policies, and the presence of key market players. The United States, in particular, leads in adopting cutting-edge genomic technologies and personalized medicine approaches. Investment in research and development, coupled with an increasing incidence of cancer and a proactive approach to preventative health, solidifies the region's leading position. Canada also contributes significantly with its robust healthcare system and growing emphasis on early diagnosis and risk assessment.

Europe represents another substantial market, characterized by strong government initiatives for cancer screening and a well-established regulatory framework. Countries like Germany, the U.K., and France are pivotal due to high healthcare expenditure, increasing public awareness, and the adoption of national cancer control programs. The emphasis on data privacy and ethical considerations also shapes market development within the European Union, fostering a balanced approach to innovation and patient protection. Continuous technological advancements and expanding clinical guidelines further support market growth across the region.

The Asia Pacific (APAC) region is projected to experience the fastest growth in the hereditary cancer testing market over the forecast period. This growth is attributable to improving healthcare infrastructure, rising disposable incomes, increasing awareness about cancer prevention, and a vast patient pool. Countries such as China, India, and Japan are investing heavily in genomic research and precision oncology, leading to greater adoption of advanced diagnostic technologies. The increasing prevalence of cancer and the growing demand for personalized treatment options are key factors fueling market expansion in this dynamic region. Latin America and the Middle East & Africa (MEA) regions, while smaller, are emerging markets showing promising growth. Increased healthcare spending, rising cancer burden, and efforts to modernize healthcare systems are contributing to the gradual adoption of hereditary cancer testing in these areas.

- North America: Leading market share due to advanced healthcare, high awareness, and favorable reimbursement. Strong presence of key players and R&D investment.

- Europe: Significant market driven by government initiatives, established regulatory frameworks, and increasing adoption in major economies like Germany and the U.K.

- Asia Pacific (APAC): Fastest-growing market, propelled by improving healthcare infrastructure, rising cancer incidence, and increasing investment in genomic research in countries like China and India.

- Latin America: Emerging market with increasing awareness and healthcare spending, contributing to gradual adoption.

- Middle East & Africa (MEA): Growing market influenced by modernizing healthcare systems and efforts to address the rising cancer burden.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hereditary Cancer Testing Market.- Agilent Technologies

- Thermo Fisher Scientific

- Illumina

- QIAGEN

- Roche Diagnostics

- Myriad Genetics

- Invitae

- Color Health

- Exact Sciences

- Guardant Health

- Natera

- NeoGenomics Laboratories

- Centogene

- Fulgent Genetics

- SOPHiA GENETICS

- Ambry Genetics

- Quest Diagnostics

- Eurofins Scientific

- F. Hoffmann-La Roche Ltd.

Frequently Asked Questions

What is hereditary cancer testing?

Hereditary cancer testing is a type of genetic test that looks for inherited mutations in genes known to increase the risk of developing certain cancers. These tests help identify individuals with a higher genetic predisposition to cancer, enabling proactive screening and risk management strategies.

Who should consider hereditary cancer testing?

Individuals with a personal or family history of early-onset cancer, multiple family members with the same cancer type, rare cancers, or specific patterns of cancer within a family should consider hereditary cancer testing. It is typically recommended after consultation with a genetic counselor or healthcare provider.

What types of genes are commonly analyzed in hereditary cancer testing?

Commonly analyzed genes include BRCA1 and BRCA2 for breast and ovarian cancer, MLH1, MSH2, MSH6, PMS2, and EPCAM for Lynch syndrome (colorectal and other cancers), and TP53 for Li-Fraumeni syndrome. Multi-gene panels can test for mutations in dozens of genes simultaneously.

How accurate are hereditary cancer test results?

Hereditary cancer tests are highly accurate in detecting known genetic mutations. However, a negative result does not completely rule out cancer risk, as not all cancer-predisposing genes are currently known, and some mutations may not be detected. Results require careful interpretation, often with genetic counseling.

Is hereditary cancer testing covered by insurance?

Insurance coverage for hereditary cancer testing varies significantly based on the specific test, medical necessity criteria, and individual insurance plans. Coverage is often available for individuals meeting specific clinical guidelines or with a strong family history, but pre-authorization may be required. Direct-to-consumer tests are typically not covered.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted