Hemostat Market

Hemostat Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708756 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Hemostat Market Size

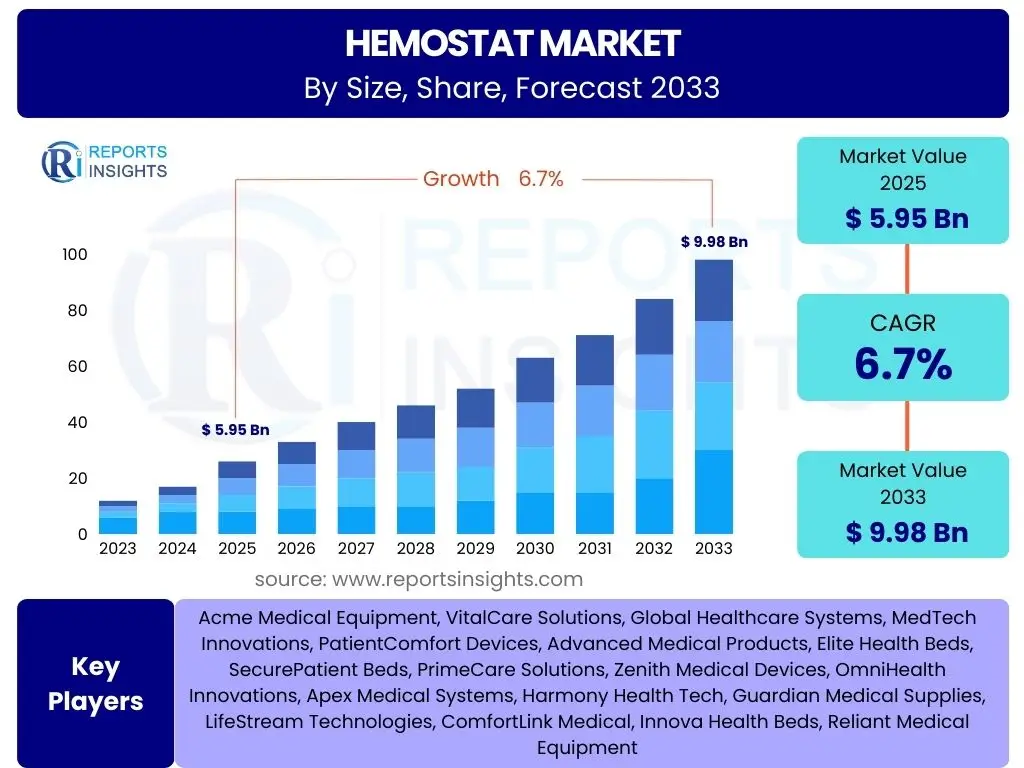

According to Reports Insights Consulting Pvt Ltd, The Hemostat Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 5.95 Billion in 2025 and is projected to reach USD 9.98 Billion by the end of the forecast period in 2033.

Key Hemostat Market Trends & Insights

The Hemostat market is witnessing a significant evolution driven by various factors, prominently including advancements in surgical techniques and an increasing global surgical volume. Users frequently inquire about the latest innovations and how these are shaping the industry. The shift towards minimally invasive procedures has amplified the demand for advanced hemostatic agents that offer rapid and effective blood clotting with minimal tissue disruption. This trend is fostering innovation in product development, focusing on biocompatibility, ease of use, and efficacy in complex surgical environments. Furthermore, the growing elderly population, which often requires various surgical interventions, coupled with the rising prevalence of chronic diseases necessitating surgical management, is substantially contributing to the market's expansion.

Another critical insight centers on the integration of smart technologies and biomaterials within hemostatic solutions. Stakeholders are keen to understand how these innovations are improving patient outcomes and reducing surgical complications. The development of next-generation hemostats incorporates features such as self-assembly, localized drug delivery, and enhanced biodegradability, moving beyond traditional methods. Regulatory pathways and reimbursement policies also play a crucial role in market adoption, with a strong emphasis on evidence-based efficacy and safety profiles. The global competitive landscape is intensifying, pushing manufacturers to differentiate their offerings through superior performance, cost-effectiveness, and broader application suitability across diverse medical specialties, including cardiology, orthopedics, and neurosurgery.

- Growing adoption of minimally invasive surgical procedures.

- Technological advancements in hemostatic agents, including advanced biomaterials and localized delivery systems.

- Increasing prevalence of chronic diseases requiring surgical intervention.

- Rising geriatric population leading to higher surgical volumes.

- Shift towards combination hemostatic products for enhanced efficacy.

AI Impact Analysis on Hemostat

Users frequently express curiosity about the transformative potential of Artificial Intelligence (AI) within the medical device landscape, particularly concerning hemostasis. The primary areas of interest revolve around how AI can enhance surgical precision, improve diagnostic capabilities related to coagulation disorders, and optimize the development and application of hemostatic agents. AI's ability to analyze vast datasets can lead to more accurate real-time predictions of bleeding risk during surgery, allowing for proactive intervention. This predictive analytics capability is crucial for guiding surgeons in selecting the most appropriate hemostatic strategy, thereby potentially reducing blood loss, operative time, and overall patient recovery periods.

Beyond predictive analytics, AI is anticipated to significantly impact the research and development (R&D) of novel hemostatic materials. Machine learning algorithms can accelerate the identification of new biomaterials, optimize their composition for superior clotting efficacy and biocompatibility, and simulate their performance under various physiological conditions, thus shortening the drug and device development cycle. Furthermore, AI-powered imaging systems can offer enhanced visualization of surgical fields, aiding in the precise application of hemostatic agents and ensuring comprehensive bleeding control. Concerns often include data privacy, regulatory challenges for AI-driven medical devices, and the need for robust validation to ensure clinical reliability and safety, underscoring the necessity for careful implementation and ethical considerations.

- Enhanced predictive analytics for real-time bleeding risk assessment during surgery.

- Accelerated research and development of novel hemostatic biomaterials and drug-device combinations.

- AI-guided surgical systems for precise application and optimized hemostatic agent delivery.

- Improved diagnostics for coagulation disorders through advanced data interpretation.

- Personalized hemostatic treatment plans based on patient-specific data and AI algorithms.

Key Takeaways Hemostat Market Size & Forecast

Analysis of common user questions regarding the Hemostat market size and forecast reveals a strong interest in understanding the primary growth drivers, the segments expected to exhibit the most robust expansion, and the overarching factors influencing long-term market sustainability. A significant takeaway is the consistent growth trajectory of the market, primarily fueled by an aging global population and the increasing prevalence of chronic diseases requiring surgical intervention. These demographic and epidemiological trends ensure a steady demand for effective hemostatic solutions across various medical specialties. Furthermore, the continuous innovation in product development, including absorbable and advanced topical hemostats, is a crucial factor in maintaining market momentum, addressing unmet clinical needs, and improving patient outcomes.

Another key insight is the regional disparities in market growth, with emerging economies, particularly in Asia Pacific and Latin America, presenting substantial opportunities due to improving healthcare infrastructure, rising healthcare expenditure, and increasing access to surgical care. While established markets in North America and Europe continue to dominate in terms of market share, these regions are characterized by a strong focus on advanced, high-value hemostatic products and sophisticated surgical techniques. The forecast indicates that while cost-effectiveness will remain a critical consideration, the emphasis on product efficacy, safety, and integration with minimally invasive procedures will increasingly dictate market leadership and adoption rates, driving investment in R&D and strategic collaborations among market players.

- The market is set for sustained growth, driven by demographic shifts and rising surgical volumes.

- Technological advancements in absorbable and combination hemostats are crucial for market expansion.

- Asia Pacific and Latin America represent high-growth potential due to healthcare infrastructure development.

- Efficacy, safety, and cost-effectiveness remain paramount factors for product adoption.

- Minimally invasive surgery trends will significantly influence product innovation and demand.

Hemostat Market Drivers Analysis

The Hemostat market is significantly propelled by several interconnected factors that collectively contribute to its robust growth. A primary driver is the global increase in surgical procedures across various medical disciplines, including general surgery, cardiovascular surgery, orthopedic surgery, and neurosurgery. This rise is attributed to an aging population more prone to chronic diseases requiring surgical intervention, along with advancements in surgical techniques that enable a broader range of treatable conditions. Effective hemostasis is critical in these procedures to manage blood loss, reduce complications, and improve patient recovery outcomes, thereby sustaining demand for a diverse range of hemostatic products.

Technological innovation represents another powerful driver, with continuous advancements in biomaterials, drug delivery systems, and product formulations leading to the development of more effective, safer, and user-friendly hemostatic agents. The emergence of combination hemostats, absorbable products, and specialized sealants addresses specific surgical needs, offering enhanced performance and reduced operative time. Furthermore, the growing awareness among healthcare professionals about the benefits of advanced hemostatic solutions in minimizing surgical risks and improving post-operative care further accelerates their adoption. The market also benefits from increasing healthcare expenditure in developing regions and a heightened focus on patient safety globally, which mandates the use of reliable hemostatic products.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Surgical Procedures Globally | +1.8% | Global (North America, Europe, APAC) | 2025-2033 |

| Technological Advancements in Hemostatic Agents | +1.5% | North America, Europe, Japan | 2025-2033 |

| Rising Geriatric Population & Chronic Diseases | +1.3% | Global | 2025-2033 |

| Growing Adoption of Minimally Invasive Surgeries | +1.1% | North America, Europe, Developed APAC | 2025-2033 |

Hemostat Market Restraints Analysis

Despite robust growth drivers, the Hemostat market faces several significant restraints that could impede its expansion. One prominent challenge is the high cost associated with advanced hemostatic agents, particularly in developing economies where healthcare budgets are constrained. These products often involve complex manufacturing processes and proprietary materials, leading to premium pricing. This cost factor can limit widespread adoption, especially in public healthcare systems or regions with lower purchasing power, forcing a preference for more traditional and less expensive methods, even if less effective.

Another critical restraint involves stringent regulatory approval processes and product recalls. Medical devices, including hemostats, are subject to rigorous testing and approval by regulatory bodies such as the FDA, EMA, and other national agencies. These processes are time-consuming and costly, potentially delaying market entry for innovative products. Furthermore, post-market surveillance can lead to product recalls due to unexpected side effects or efficacy issues, which can severely impact consumer trust, company reputation, and financial performance. Additionally, a lack of awareness or training among healthcare professionals in some regions regarding the proper application and benefits of newer hemostatic agents can also act as a bottleneck for market penetration and optimal utilization.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Hemostatic Agents | -0.9% | Developing Regions (APAC, Latin America, MEA) | 2025-2033 |

| Stringent Regulatory Approval Processes | -0.7% | Global (North America, Europe) | 2025-2033 |

| Product Recalls and Safety Concerns | -0.5% | Global | 2025-2030 |

| Lack of Skilled Professionals in Certain Regions | -0.4% | Emerging Economies | 2025-2033 |

Hemostat Market Opportunities Analysis

The Hemostat market is characterized by several promising opportunities that are poised to drive significant growth and innovation. One major opportunity lies in the burgeoning markets of developing economies, particularly in Asia Pacific, Latin America, and the Middle East & Africa. These regions are experiencing rapid improvements in healthcare infrastructure, increasing disposable incomes, and a rising patient population gaining access to advanced medical treatments. As surgical volumes grow in these areas, the demand for effective and affordable hemostatic solutions will surge, creating a fertile ground for market expansion and the introduction of tailored product offerings.

Another significant opportunity stems from the continuous innovation in product development, particularly the creation of specialized hemostats for niche applications and personalized medicine approaches. This includes the development of products optimized for specific surgical environments, such as cardiovascular, neuro, or orthopedic surgeries, as well as hemostats for patients with complex coagulopathies or those on anticoagulant therapies. Furthermore, strategic collaborations and partnerships between device manufacturers, research institutions, and healthcare providers can accelerate the development and commercialization of next-generation hemostatic technologies. The increasing focus on value-based healthcare also opens doors for products that demonstrate superior clinical outcomes and cost-effectiveness, appealing to healthcare systems looking to optimize patient care while managing expenditures.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Economies | +1.2% | APAC, Latin America, MEA | 2025-2033 |

| Development of Specialized & Advanced Hemostats | +1.0% | Global (North America, Europe) | 2025-2033 |

| Strategic Collaborations & Partnerships | +0.8% | Global | 2025-2030 |

| Integration with Minimally Invasive & Robotic Surgeries | +0.7% | North America, Europe, Developed APAC | 2025-2033 |

Hemostat Market Challenges Impact Analysis

The Hemostat market faces several significant challenges that could impede its growth trajectory and present hurdles for market participants. Intense price competition, particularly among generic and traditional hemostatic products, is a persistent challenge. As more players enter the market and established products become commoditized, manufacturers face pressure to reduce prices, which can impact profit margins and limit investments in research and development for innovative solutions. This competitive landscape demands continuous product differentiation and a strong value proposition to maintain market share.

Another critical challenge is the complexity of managing global supply chains, especially in light of geopolitical instability, trade barriers, and unforeseen events such as pandemics. Disruptions in the supply of raw materials or manufacturing components can lead to production delays, increased costs, and shortages of essential hemostatic products. Furthermore, the variability in product efficacy and the potential for adverse reactions, although rare, necessitate continuous post-market surveillance and can lead to challenges in gaining and maintaining physician trust. Overcoming these hurdles requires robust quality control, efficient logistics, and transparent communication with healthcare providers and regulatory bodies to ensure patient safety and market confidence.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition | -0.8% | Global | 2025-2033 |

| Stringent Regulatory Compliance and Product Development Costs | -0.6% | Global (Developed Markets) | 2025-2033 |

| Supply Chain Disruptions & Raw Material Volatility | -0.5% | Global | 2025-2030 |

| Limited Awareness and Training in Emerging Markets | -0.4% | APAC, Latin America, MEA | 2025-2033 |

Hemostat Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Hemostat market, offering critical insights into its current size, historical performance, and future growth projections from 2025 to 2033. The scope includes a detailed examination of market trends, drivers, restraints, opportunities, and challenges influencing industry dynamics. Key segments and sub-segments are thoroughly analyzed, alongside regional perspectives to provide a holistic view of the market landscape. The report aims to equip stakeholders with actionable intelligence for strategic decision-making in this evolving medical device sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.95 Billion |

| Market Forecast in 2033 | USD 9.98 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ethicon (Johnson & Johnson), Baxter International Inc., C. R. Bard (BD), B. Braun Melsungen AG, Teleflex Incorporated, Coagulation Technologies, Arch Therapeutics Inc., CryoLife Inc., Gland Pharma Limited, Integra LifeSciences Corporation, Hemostasis LLC, Tissuemed Ltd., Gamma Therapeutics Inc., Stryker Corporation, Medtronic Plc, Pfizer Inc., Olympus Corporation, Zimmer Biomet, Boston Scientific Corporation, Bioceramics Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Hemostat market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth dynamics. This segmentation facilitates a detailed analysis of product types, applications, and end-user adoption patterns, offering crucial insights into market penetration and unmet needs. Each segment is influenced by specific technological advancements, regulatory environments, and clinical demands, contributing uniquely to the overall market landscape. Understanding these segments is vital for stakeholders to identify lucrative opportunities and tailor their strategies effectively.

- By Product: This segment includes Thrombin-based Hemostats, Oxidized Regenerated Cellulose (ORC)-based Hemostats, Collagen-based Hemostats, Gelatin-based Hemostats, Combination Hemostats, Fibrin Sealants, and other innovative hemostatic agents. Thrombin-based products are widely used for rapid hemostasis, while ORC and gelatin products offer absorbable solutions. Fibrin sealants are gaining traction for their strong adhesive properties and use in delicate tissues.

- By Application: The market is segmented across various surgical disciplines such as General Surgery, Cardiovascular Surgery, Orthopedic Surgery, Neurosurgery, Plastic Surgery, and Trauma & Emergency Surgery. Each application area has specific requirements for hemostatic agents based on the type of tissue, potential for bleeding, and desired healing outcomes. Cardiovascular and neurosurgeries often demand highly effective and precise hemostatic solutions.

- By End-Use: This segment categorizes consumption by primary healthcare settings, including Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Military & Disaster Settings. Hospitals represent the largest end-user segment due to the high volume of complex surgeries performed. ASCs are experiencing rapid growth driven by the shift towards outpatient procedures and cost-effectiveness.

- By Region: The geographic segmentation includes North America, Europe, Asia Pacific (APAC), Latin America, and Middle East & Africa (MEA). Each region exhibits unique market characteristics shaped by healthcare infrastructure, regulatory policies, economic development, and surgical volumes.

Regional Highlights

- North America: North America, particularly the United States and Canada, holds a dominant share in the Hemostat market. This is primarily attributed to advanced healthcare infrastructure, high healthcare expenditure, the presence of major market players, and a high adoption rate of technologically sophisticated hemostatic products. The region also benefits from a large aging population and a high incidence of chronic diseases requiring surgical intervention. Stringent regulatory standards ensure high product quality and safety, further driving demand for premium hemostats.

- Europe: Europe represents another significant market for hemostats, driven by well-established healthcare systems, increasing surgical volumes, and a strong focus on patient safety and quality of care. Countries like Germany, the UK, France, and Italy are key contributors. The region is witnessing a steady adoption of advanced hemostatic agents and fibrin sealants, supported by favorable reimbursement policies and a growing emphasis on minimally invasive surgical techniques.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for hemostats during the forecast period. This growth is fueled by rapidly developing healthcare infrastructure, increasing healthcare expenditure, a large patient pool, and rising medical tourism in countries such as China, India, Japan, and South Korea. Improving access to advanced surgical care and a growing awareness of modern hemostatic solutions are significant market accelerators. Local manufacturers are also emerging, intensifying competition and product availability.

- Latin America: The Latin American market is experiencing steady growth, primarily in countries like Brazil, Mexico, and Argentina. This growth is driven by improving economic conditions, expanding healthcare access, and an increasing number of surgical procedures. While the adoption of advanced hemostats is still in its nascent stages compared to developed regions, there is a clear trend towards upgrading surgical practices and product utilization, presenting considerable future opportunities.

- Middle East & Africa (MEA): The MEA region is characterized by moderate growth, with countries like Saudi Arabia, UAE, and South Africa leading the market. Investments in healthcare infrastructure, particularly in the Gulf Cooperation Council (GCC) countries, and increasing medical tourism are contributing to market expansion. However, disparities in healthcare access and economic development across the region present both opportunities and challenges for market penetration.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hemostat Market.- Ethicon (Johnson & Johnson)

- Baxter International Inc.

- C. R. Bard (BD)

- B. Braun Melsungen AG

- Teleflex Incorporated

- Coagulation Technologies

- Arch Therapeutics Inc.

- CryoLife Inc.

- Gland Pharma Limited

- Integra LifeSciences Corporation

- Hemostasis LLC

- Tissuemed Ltd.

- Gamma Therapeutics Inc.

- Stryker Corporation

- Medtronic Plc

- Pfizer Inc.

- Olympus Corporation

- Zimmer Biomet

- Boston Scientific Corporation

- Bioceramics Ltd.

Frequently Asked Questions

What is a hemostat and how does it work?

A hemostat is a medical device or agent used to stop or control bleeding during surgical procedures or trauma. They work by promoting blood coagulation, sealing tissue, or providing a physical barrier to staunch blood flow.

What are the primary types of hemostatic agents available in the market?

The primary types include absorbable hemostats (e.g., oxidized regenerated cellulose, gelatin, collagen), topical hemostats (e.g., thrombin-based), and fibrin sealants. Combination products that blend these mechanisms are also increasingly common.

Which surgical applications most commonly utilize hemostats?

Hemostats are extensively used across various surgical applications, including general surgery, cardiovascular surgery, orthopedic surgery, neurosurgery, and trauma & emergency surgery, where effective blood loss management is critical.

Which region currently dominates the global Hemostat market?

North America currently holds the largest share of the global Hemostat market, driven by advanced healthcare infrastructure, high surgical volumes, and rapid adoption of innovative hemostatic technologies.

What are the key factors driving the growth of the Hemostat market?

Key growth drivers include the increasing number of surgical procedures globally, the rising prevalence of chronic diseases, a growing geriatric population, and continuous technological advancements in hemostatic product development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted