Heavy Construction Software Market

Heavy Construction Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710378 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

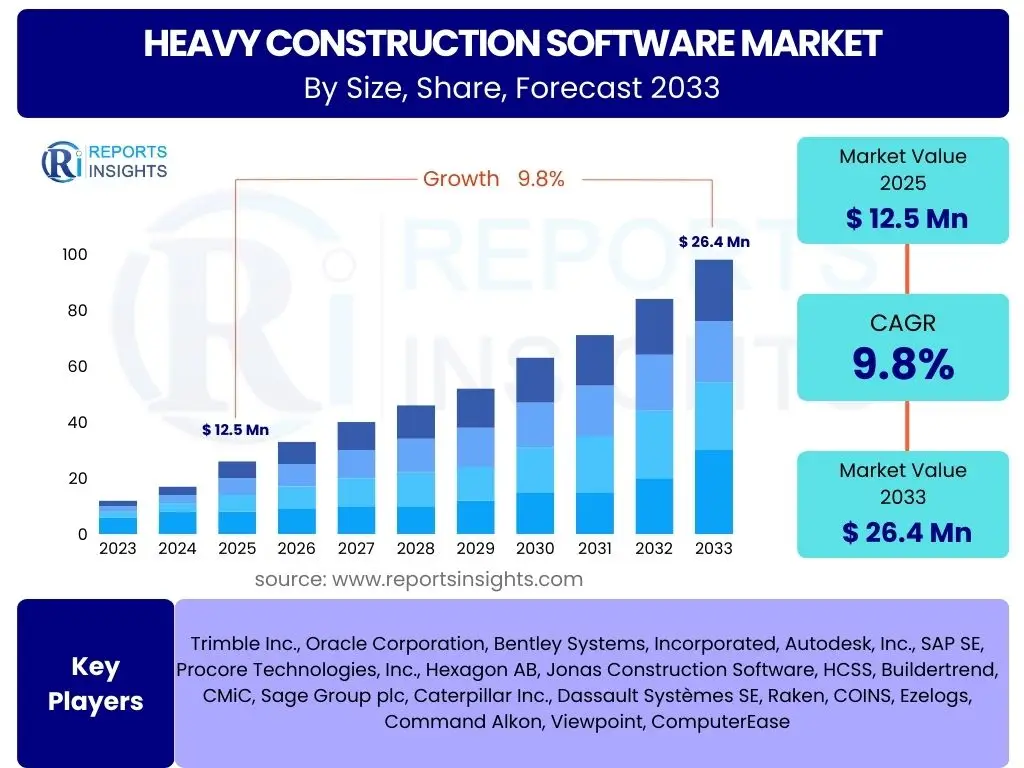

Heavy Construction Software Market Size

According to Reports Insights Consulting Pvt Ltd, The Heavy Construction Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 26.4 Billion by the end of the forecast period in 2033.

Key Heavy Construction Software Market Trends & Insights

User inquiries frequently highlight the increasing adoption of cloud-based solutions and Software-as-a-Service (SaaS) models as a pivotal trend, offering enhanced accessibility, scalability, and reduced upfront costs. Another significant area of interest revolves around the integration of advanced technologies such as Building Information Modeling (BIM) and the Internet of Things (IoT) to improve project visualization, collaboration, and real-time data collection across heavy construction sites. These advancements are driving a shift towards more data-driven decision-making and operational efficiency.

Furthermore, discussions often focus on the growing demand for mobile-first applications that enable field teams to access critical project information, submit reports, and manage tasks from remote locations, thereby boosting productivity and communication. There is also considerable attention paid to the evolving landscape of predictive analytics and artificial intelligence, which are beginning to offer solutions for equipment maintenance, risk assessment, and project scheduling optimization. These trends collectively underscore a market moving towards greater automation, connectivity, and intelligent management systems to address the complexities of modern heavy construction projects.

- Cloud and SaaS adoption for enhanced accessibility and scalability.

- Integration of BIM and IoT for improved visualization and real-time data.

- Increasing use of mobile applications for field operations and productivity.

- Rising demand for predictive analytics and AI in project optimization.

- Emphasis on data-driven decision-making and operational efficiency.

- Focus on sustainability and green construction through specialized software modules.

AI Impact Analysis on Heavy Construction Software

Common user questions regarding AI's impact on heavy construction software reveal a dual perspective: excitement for transformational benefits alongside concerns about implementation challenges. Users are eager to understand how AI can revolutionize project planning, predictive maintenance of heavy machinery, and real-time risk assessment, thereby enhancing safety and operational efficiency. There's a strong expectation that AI will streamline complex workflows, automate routine tasks, and provide deeper insights from vast datasets, leading to more informed decision-making and significant cost reductions over the project lifecycle.

Conversely, concerns frequently arise around the initial investment required for AI integration, the need for specialized skills to manage AI-powered systems, and potential data privacy issues associated with large-scale data collection. Users also question the ethical implications and the potential for job displacement, seeking clarity on how AI will augment human capabilities rather than replace them. Despite these considerations, the overarching sentiment is one of optimistic anticipation for AI to drive a new era of intelligence and efficiency in the heavy construction sector, moving beyond traditional software capabilities to truly smart construction management.

- Enhanced predictive analytics for equipment maintenance and project timelines.

- Automation of routine administrative and operational tasks.

- Improved risk assessment and mitigation through pattern recognition.

- Optimized resource allocation and supply chain management.

- Advanced safety monitoring and incident prediction on job sites.

- Development of intelligent scheduling and budget management tools.

- Potential for more accurate bidding and project cost estimation.

Key Takeaways Heavy Construction Software Market Size & Forecast

The heavy construction software market is poised for robust growth, driven by an imperative for digital transformation across the global construction industry. Key takeaways from the market size and forecast analysis underscore a significant shift towards integrated and intelligent software solutions designed to tackle the inherent complexities of large-scale infrastructure and building projects. Stakeholders are increasingly recognizing that leveraging specialized software is no longer a luxury but a necessity for competitive advantage, operational excellence, and project delivery within stringent timelines and budgets.

The forecast period projects a substantial increase in market valuation, indicating sustained investment in technologies that enhance project lifecycle management, from initial design and planning through execution, monitoring, and maintenance. This growth is particularly fueled by the adoption of cloud-based platforms and mobile applications, which offer unparalleled flexibility and collaboration capabilities. The market's trajectory highlights a clear trend towards greater digitalization, automation, and data utilization as cornerstones for future success in heavy construction.

- Significant market expansion with a projected CAGR of 9.8% by 2033.

- Increasing investment in digital tools for improved project management and efficiency.

- Cloud and mobile solutions are foundational for market growth.

- Heavy construction firms prioritize integrated software for complex projects.

- Data-driven insights are becoming critical for strategic decision-making.

- The market is transitioning towards intelligent, automated construction processes.

Heavy Construction Software Market Drivers Analysis

The heavy construction software market is primarily propelled by the escalating demand for operational efficiency and productivity improvements across large-scale projects. As project complexities increase and timelines become more stringent, construction firms are actively seeking software solutions that can streamline workflows, automate repetitive tasks, and provide real-time visibility into project progress and resource utilization. This drive for efficiency is further amplified by intense competition within the industry, where technological adoption offers a significant competitive edge.

Another crucial driver is the rapid digital transformation occurring globally, necessitating the adoption of advanced technologies to meet modern construction standards and regulatory requirements. Governments and private entities are investing heavily in infrastructure development, which in turn fuels the need for sophisticated software to manage these massive projects from conception to completion. Additionally, the growing emphasis on data-driven decision-making, coupled with the desire to mitigate risks and enhance safety, encourages firms to invest in robust software platforms that offer comprehensive analytics and reporting capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Operational Efficiency and Productivity | +2.5% | Global (North America, Europe, Asia Pacific) | Short to Medium-Term |

| Rapid Digital Transformation and Technological Advancement | +2.0% | Global (Developed and Emerging Economies) | Medium to Long-Term |

| Growth in Infrastructure Spending and Large-Scale Projects | +1.8% | Asia Pacific, North America, Middle East & Africa | Medium to Long-Term |

| Need for Improved Project Management and Collaboration | +1.5% | Global | Short to Medium-Term |

| Rising Adoption of Building Information Modeling (BIM) | +1.0% | Europe, North America, Australia | Medium to Long-Term |

Heavy Construction Software Market Restraints Analysis

Despite the significant growth potential, the heavy construction software market faces several notable restraints. A primary concern is the substantial initial investment required for acquiring and implementing advanced software solutions, particularly for smaller and medium-sized construction firms. This financial barrier can deter adoption, especially when considering the additional costs associated with training personnel and integrating new systems with existing legacy infrastructure. The perceived high cost versus immediate return on investment often leads to a cautious approach among potential adopters.

Another significant restraint involves the resistance to change within the traditionally conservative construction industry. Many firms operate using established manual processes or older, less integrated systems, and transitioning to new digital workflows can be challenging due to cultural inertia and a lack of skilled professionals capable of managing these advanced technologies. Furthermore, concerns regarding data security, privacy, and the interoperability of different software platforms can hinder widespread adoption, as companies seek assurances that their sensitive project data is protected and that various systems can seamlessly communicate with each other without compatibility issues.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Implementation Costs | -1.2% | Global (SMEs, Emerging Markets) | Short to Medium-Term |

| Resistance to Change and Lack of Skilled Workforce | -1.0% | Global (Traditional Firms) | Medium-Term |

| Data Security Concerns and Interoperability Challenges | -0.8% | Global | Short to Medium-Term |

| Economic Volatility and Project Delays | -0.7% | Global (Impact Varies by Region) | Short-Term |

Heavy Construction Software Market Opportunities Analysis

The heavy construction software market presents numerous opportunities for growth, particularly in the expansion of cloud-based and Software-as-a-Service (SaaS) offerings. These models provide greater flexibility, scalability, and cost-effectiveness, appealing to a broader range of construction companies, including those with limited IT infrastructure or budget constraints. The shift towards subscription-based services reduces upfront capital expenditure, making advanced software more accessible and fostering wider adoption across the industry. This trend is unlocking new revenue streams and enabling continuous innovation for software providers.

Further opportunities lie in the integration of emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT) into existing software platforms. These integrations can unlock new functionalities, such as predictive analytics for equipment maintenance, intelligent project scheduling, and real-time site monitoring, leading to unprecedented levels of efficiency and safety. Additionally, the growing demand for sustainable construction practices and green building initiatives creates a niche for specialized software modules that help manage environmental impacts, optimize material usage, and ensure compliance with evolving sustainability standards, opening up new market segments for innovative solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cloud-Based and SaaS Deployment Models | +1.8% | Global | Medium to Long-Term |

| Integration of AI, ML, and IoT for Advanced Analytics | +1.5% | Global (Developed Economies) | Medium to Long-Term |

| Growth in Emerging Markets and Digitalization Initiatives | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Long-Term |

| Focus on Sustainable Construction and Green Building Practices | +0.9% | Europe, North America, Australia | Medium to Long-Term |

Heavy Construction Software Market Challenges Impact Analysis

The heavy construction software market faces significant challenges, primarily stemming from the complexity of integrating diverse systems and data sources. Large-scale construction projects often involve multiple stakeholders, subcontractors, and various specialized software tools, leading to fragmented data and interoperability issues. Ensuring seamless data flow and communication across these disparate systems presents a considerable technical hurdle, often resulting in inefficiencies and errors that can undermine the benefits of software adoption. Overcoming these integration complexities requires robust, open-architecture solutions and industry-wide collaboration on data standards.

Another pressing challenge is the persistent cybersecurity threat landscape. As construction firms increasingly rely on digital platforms to manage sensitive project data, financial information, and intellectual property, they become prime targets for cyberattacks. Protecting this data from breaches, ransomware, and other malicious activities is crucial for maintaining trust and operational continuity. Furthermore, the rapid pace of technological evolution means that software solutions can quickly become outdated, necessitating continuous investment in research and development to keep up with industry demands and emerging innovations, thereby posing a challenge for long-term product relevance and competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of System Integration and Data Interoperability | -1.1% | Global | Medium-Term |

| Cybersecurity Threats and Data Protection Concerns | -0.9% | Global | Ongoing |

| Rapid Technological Evolution and Obsolescence | -0.7% | Global | Long-Term |

| Skilled Labor Shortage for Advanced Software Utilization | -0.6% | North America, Europe | Medium to Long-Term |

Heavy Construction Software Market - Updated Report Scope

This report provides a detailed analysis of the Heavy Construction Software Market, encompassing a comprehensive evaluation of market size, growth drivers, restraints, opportunities, and challenges. It includes an in-depth examination of market trends, the impact of AI, and regional dynamics, offering strategic insights for stakeholders. The scope covers various deployment models, applications, and end-user segments, providing a holistic view of the industry landscape from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 26.4 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Trimble Inc., Oracle Corporation, Bentley Systems, Incorporated, Autodesk, Inc., SAP SE, Procore Technologies, Inc., Hexagon AB, Jonas Construction Software, HCSS, Buildertrend, CMiC, Sage Group plc, Caterpillar Inc., Dassault Systèmes SE, Raken, COINS, Ezelogs, Command Alkon, Viewpoint, ComputerEase |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The heavy construction software market is intricately segmented to provide a granular view of its various facets, allowing for targeted analysis and strategic planning. These segmentations are critical for understanding market dynamics and identifying specific growth pockets within the diverse construction ecosystem. They span deployment models, the range of applications, the variety of end-users, and the different components that constitute the software solutions.

Each segment addresses distinct needs and preferences within the heavy construction industry, reflecting the varied operational requirements and technological maturity levels of different market players. For instance, the choice between cloud-based and on-premise deployment significantly impacts accessibility, cost structure, and data management strategies for construction firms. Similarly, the diverse application areas, from project management to equipment tracking, highlight the comprehensive nature of software solutions required to manage complex construction projects effectively.

- By Deployment:

- By Application:

- By End-User:

- By Component:

The deployment segment categorizes heavy construction software based on its hosting and accessibility infrastructure, primarily differentiating between cloud-based and on-premise solutions. Cloud-based software, often delivered through a Software-as-a-Service (SaaS) model, provides enhanced flexibility, scalability, and remote accessibility, making it highly attractive to firms seeking reduced IT overhead and real-time collaboration capabilities. Its rapid adoption is driven by the advantages of automatic updates, lower upfront costs, and the ability to access data from any location, crucial for field operations.

Conversely, on-premise solutions involve software installation and management on the user's local servers and infrastructure. While offering greater control over data security and customization for some large enterprises with specific regulatory or legacy system requirements, this model typically entails higher initial investment, ongoing maintenance costs, and a reliance on internal IT resources. The trend leans towards cloud-based solutions due to their operational efficiencies and suitability for distributed project teams, though on-premise options remain relevant for specific security-conscious or highly specialized applications.

The application segment delineates the diverse functional areas that heavy construction software addresses, highlighting its integral role in streamlining various aspects of project lifecycle management. Project Management applications form the core, offering tools for scheduling, task assignment, progress tracking, and overall project oversight, critical for ensuring projects stay on time and within budget. Equipment Management software is crucial for optimizing the utilization, maintenance, and tracking of heavy machinery, maximizing asset lifespan and operational efficiency while minimizing downtime.

Further specialized applications include Workforce Management for labor scheduling, payroll, and compliance; Financial Management for budgeting, invoicing, and cost control; and Safety Management for ensuring adherence to safety regulations and preventing incidents on job sites. BIM & Design applications integrate 3D modeling with project data for enhanced visualization and collaboration, while Document Management streamlines document control and versioning. Field Reporting and Risk Management tools further empower on-site teams and help mitigate unforeseen project risks, showcasing the comprehensive utility of heavy construction software across the entire operational spectrum.

The end-user segmentation examines the primary beneficiaries and adopters of heavy construction software, illustrating how different types of organizations leverage these solutions to meet their specific operational needs. General Contractors, who manage entire construction projects, are major users, relying on software for holistic project oversight, subcontractor management, and financial control. Heavy Equipment Operators and rental companies utilize specialized software for fleet management, maintenance scheduling, and telematics data analysis to optimize equipment performance and reduce operational costs.

Infrastructure Developers, involved in large-scale public and private infrastructure projects like roads, bridges, and utilities, depend on robust software for complex project planning, risk assessment, and regulatory compliance. Specialty Contractors, focusing on specific trades such as excavation, piling, or concrete work, use tailored software for precise task management, resource allocation, and specialized equipment tracking. Government Agencies also employ heavy construction software for managing public works, procurement, and ensuring project adherence to standards and timelines, underscoring the broad applicability of these solutions across the heavy construction ecosystem.

The component segment categorizes the offerings within the heavy construction software market into solutions (software) and services. The solutions component primarily encompasses the various software platforms and modules designed to address specific functions, such as project management, BIM, equipment tracking, or financial management. These software products are the core offerings, providing the technological tools necessary for digitalization and optimization of construction processes. They can range from standalone applications to integrated suites, delivered through different deployment models.

The services component includes crucial supplementary offerings that ensure the effective implementation, operation, and maintenance of the software solutions. This typically involves consulting services for strategic planning and system selection, integration services to ensure seamless connectivity with existing IT infrastructure and other platforms, and comprehensive support and maintenance services to resolve issues, provide updates, and ensure continuous system performance. The blend of robust software solutions with expert services is essential for maximizing the value and impact of heavy construction software investments for end-users.

Regional Highlights

The global heavy construction software market exhibits significant regional variations in adoption and growth, influenced by factors such as infrastructure development, technological maturity, and regulatory frameworks. North America stands as a dominant region, driven by substantial government investment in infrastructure projects, a high rate of technological adoption, and the presence of numerous key market players. The region benefits from a mature construction sector that readily embraces advanced software solutions for efficiency, safety, and compliance, with a strong focus on cloud-based platforms and integrated project management tools.

Europe represents another key market, characterized by stringent environmental regulations, a strong emphasis on BIM adoption, and ongoing efforts towards sustainable construction. Countries like Germany, the UK, and France are leading in the digitalization of their construction industries, fostering a high demand for advanced software that supports complex engineering projects and promotes energy efficiency. The Asia Pacific region is poised for the fastest growth, propelled by rapid urbanization, massive infrastructure development initiatives in emerging economies like China and India, and increasing awareness regarding the benefits of construction digitalization. Governments in this region are investing heavily in smart city projects and transportation networks, creating vast opportunities for heavy construction software providers, although the adoption rate is still catching up to Western counterparts.

- North America: Dominates the market due to robust infrastructure spending, high technological adoption, and a mature construction industry. The United States and Canada are leading, with a strong emphasis on cloud-based solutions and integrated project management systems.

- Europe: A significant market driven by strict regulatory standards, a high rate of BIM adoption, and a focus on sustainable construction practices. Countries like Germany, the UK, and France are key contributors to market growth, emphasizing efficiency and environmental compliance.

- Asia Pacific (APAC): Expected to be the fastest-growing region, fueled by rapid urbanization, large-scale infrastructure development projects (e.g., China's Belt and Road Initiative, India's smart cities), and increasing digitalization efforts in emerging economies.

- Latin America: Shows emerging potential with growing investments in public infrastructure and natural resource projects. Brazil and Mexico are key markets, slowly adopting digital solutions to improve project efficiency and overcome historical challenges.

- Middle East and Africa (MEA): Experiencing substantial growth due to mega-projects in the construction and energy sectors, particularly in the GCC countries. Government visions like Saudi Arabia's Vision 2030 are driving significant demand for advanced construction software for ambitious developments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Heavy Construction Software Market.- Trimble Inc.

- Oracle Corporation

- Bentley Systems, Incorporated

- Autodesk, Inc.

- SAP SE

- Procore Technologies, Inc.

- Hexagon AB

- Jonas Construction Software

- HCSS

- Buildertrend

- CMiC

- Sage Group plc

- Caterpillar Inc.

- Dassault Systèmes SE

- Raken

- COINS

- Ezelogs

- Command Alkon

- Viewpoint (now Trimble Company)

- ComputerEase

Frequently Asked Questions

What is heavy construction software?

Heavy construction software refers to specialized digital tools and platforms designed to manage and optimize various aspects of large-scale infrastructure projects, such as roads, bridges, dams, and commercial buildings. These solutions cover functions like project management, equipment tracking, financial management, BIM, and field reporting to enhance efficiency, reduce costs, and ensure project success.

What is the current market size and projected growth of heavy construction software?

The heavy construction software market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 26.4 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 9.8% during the forecast period. This growth is driven by digitalization, infrastructure spending, and the demand for operational efficiency.

What are the key trends shaping the heavy construction software market?

Key trends include the increasing adoption of cloud-based and SaaS solutions for scalability and accessibility, the integration of Building Information Modeling (BIM) and IoT for enhanced visualization and data collection, the rise of mobile applications for field operations, and the growing influence of AI and predictive analytics for project optimization and risk management.

How does AI impact heavy construction software?

AI significantly impacts heavy construction software by enabling advanced predictive analytics for equipment maintenance, automating routine tasks, improving risk assessment, and optimizing resource allocation. It contributes to more data-driven decision-making, enhanced safety, and overall project efficiency, transforming traditional construction workflows into intelligent processes.

What are the primary challenges in the heavy construction software market?

Major challenges include the complexity of integrating diverse systems and ensuring data interoperability, ongoing cybersecurity threats to sensitive project information, the rapid pace of technological evolution leading to potential obsolescence, and the shortage of skilled labor capable of effectively utilizing advanced software solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted