Heat Resistant Polymer Market

Heat Resistant Polymer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704315 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

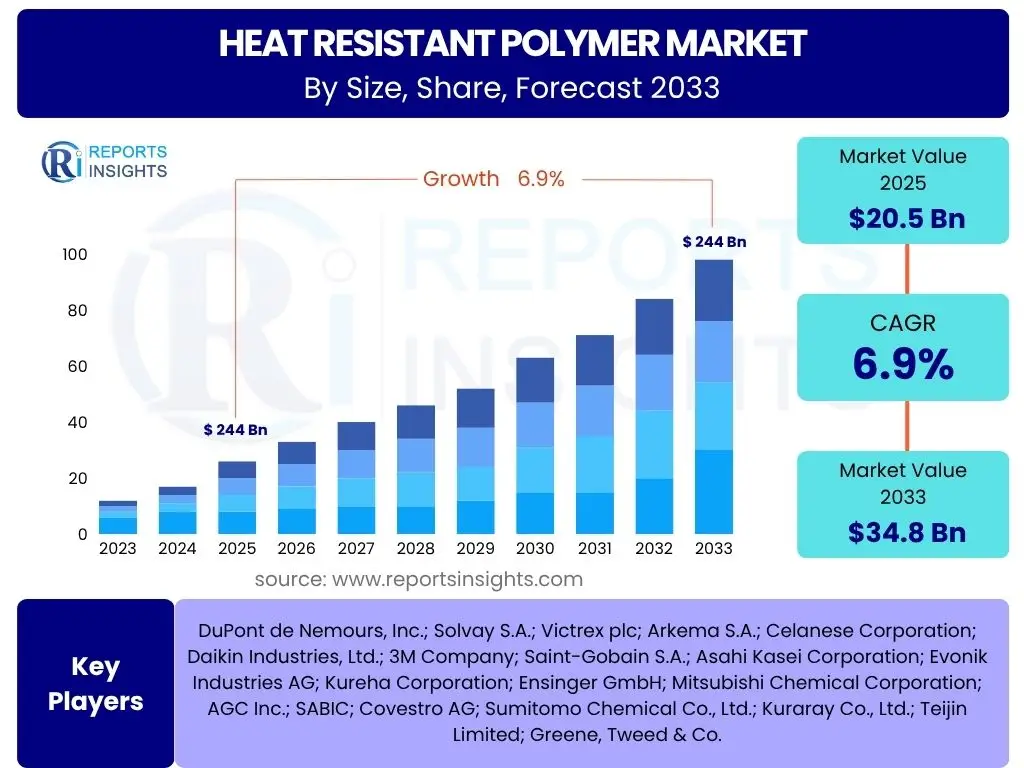

Heat Resistant Polymer Market Size

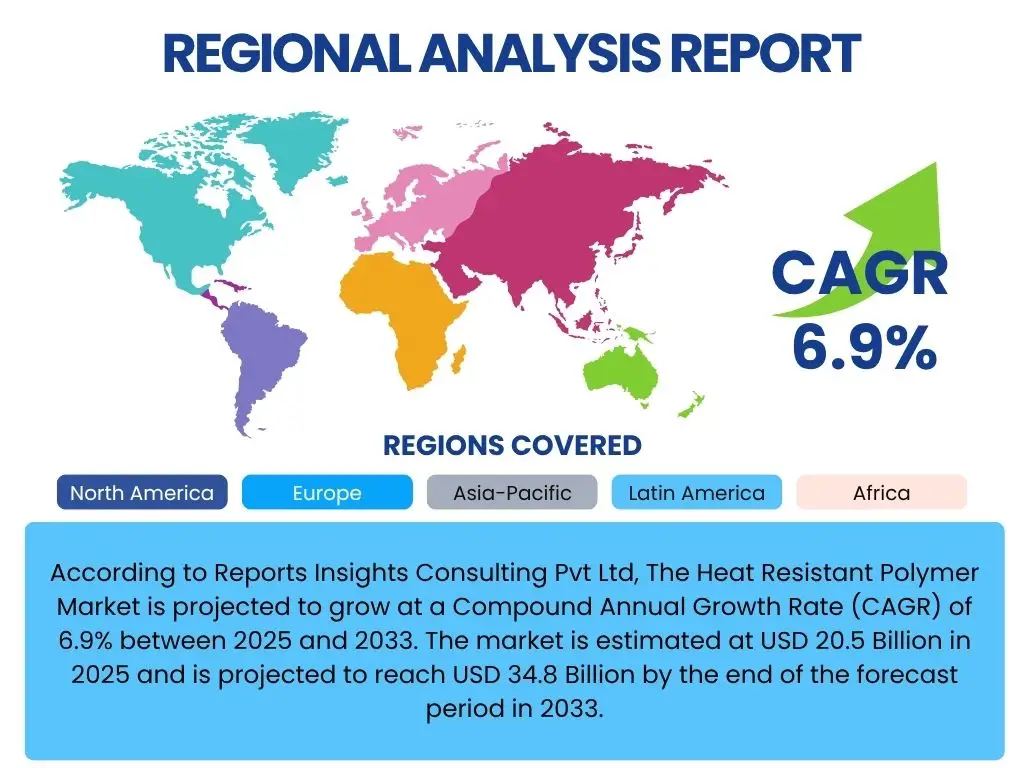

According to Reports Insights Consulting Pvt Ltd, The Heat Resistant Polymer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.9% between 2025 and 2033. The market is estimated at USD 20.5 Billion in 2025 and is projected to reach USD 34.8 Billion by the end of the forecast period in 2033.

Key Heat Resistant Polymer Market Trends & Insights

The Heat Resistant Polymer market is undergoing significant transformation, primarily driven by the escalating demand for lightweight, high-performance materials capable of operating under extreme conditions across diverse industries. A prominent trend involves the increasing integration of these advanced polymers into electric vehicle manufacturing, addressing the critical needs for thermal management, battery safety, and overall vehicle lightweighting to extend range and efficiency. Simultaneously, the aerospace and defense sectors continue to be major consumers, seeking materials that offer superior strength-to-weight ratios and exceptional thermal stability for next-generation aircraft and defense systems. This push for higher performance is often intertwined with rigorous safety standards and extended operational lifetimes.

Another pivotal insight is the growing emphasis on sustainability and the development of eco-friendly solutions within the polymer industry. There is a concerted effort to innovate processes and material compositions that reduce environmental impact, including research into recyclable, bio-based, and biodegradable heat resistant polymers. Furthermore, advancements in processing technologies, such as additive manufacturing (3D printing), are democratizing access to complex geometries and custom components, expanding the design freedom and application possibilities for these specialized polymers. These technological strides are enabling new frontiers in product design and functionality, making high-performance solutions more accessible and versatile across various industrial applications.

- Growing adoption in electric vehicle (EV) manufacturing for thermal management and lightweighting solutions.

- Increasing demand from advanced aerospace and defense sectors for high-performance components in extreme environments.

- Significant focus on research and development of sustainable, recyclable, and bio-based heat resistant polymers.

- Advancements in additive manufacturing (3D printing) enabling complex geometries and rapid prototyping for specialized applications.

- Miniaturization and enhanced performance requirements in the electronics industry driving demand for specialized insulating and encapsulating polymers.

- Expansion into new industrial applications requiring superior thermal stability and chemical resistance.

AI Impact Analysis on Heat Resistant Polymer

Artificial intelligence and machine learning are revolutionizing the heat resistant polymer market by significantly enhancing capabilities across the entire value chain, from material discovery to manufacturing and quality control. These advanced computational techniques allow for the accelerated identification and design of novel polymer structures with precise thermal and mechanical properties, drastically reducing the time and cost traditionally associated with experimental material development. By simulating molecular interactions and predicting performance characteristics, AI algorithms can pinpoint promising candidates more efficiently, leading to breakthroughs in material science. This predictive capability minimizes reliance on extensive physical testing, streamlining the R&D pipeline and fostering innovation at an unprecedented pace.

Beyond material design, AI's impact extends profoundly into manufacturing processes and operational optimization. AI-driven analytics are being deployed to monitor and control complex polymer synthesis and processing parameters in real-time, ensuring consistent product quality, reducing waste, and improving energy efficiency. Predictive maintenance facilitated by AI algorithms analyzes equipment data to anticipate failures, thereby minimizing downtime and extending the lifespan of machinery. Furthermore, AI-powered vision systems are enhancing quality control by autonomously detecting even minute defects in polymer products, ensuring adherence to stringent industry standards. The integration of AI also aids in optimizing supply chain logistics and demand forecasting for raw materials, leading to more resilient and responsive production systems within the heat resistant polymer sector.

- Accelerated material discovery and computational design of novel heat resistant polymer formulations.

- Optimization of polymer synthesis and processing parameters through machine learning algorithms for improved efficiency and yield.

- Enhanced quality control and defect detection using AI-powered vision systems and predictive analytics in manufacturing.

- Improved supply chain management and demand forecasting for raw materials and finished products.

- Development of smart heat resistant polymers with self-healing capabilities or adaptive properties through AI integration.

- Predictive performance modeling for end-use applications, reducing the need for extensive physical prototyping.

Key Takeaways Heat Resistant Polymer Market Size & Forecast

The Heat Resistant Polymer market is poised for robust and sustained growth throughout the forecast period, primarily propelled by the unwavering demand from high-growth and technologically advanced sectors such as aerospace, defense, automotive (with a particular emphasis on electric vehicles), and electronics. These industries consistently require materials capable of performing reliably under extreme thermal, mechanical, and chemical conditions, making heat resistant polymers indispensable. The expansion is significantly bolstered by continuous innovation in polymer science, leading to the development of new materials with enhanced properties, improved processing characteristics, and increasingly cost-effective production methods. This ongoing evolution in material capabilities expands the range of potential applications and strengthens the value proposition of these specialized polymers.

For market participants, understanding and leveraging these dynamics will be crucial. Strategic investments in research and development, particularly in areas like sustainable polymer solutions and advanced processing technologies (e.g., additive manufacturing), will be vital for maintaining competitive advantage and capturing emerging opportunities. Furthermore, establishing strong partnerships across the value chain, from raw material suppliers to end-use manufacturers, will facilitate collaborative innovation and market penetration. The market is also seeing a geographic diversification of demand, with significant growth potential in emerging economies that are rapidly industrializing and adopting advanced manufacturing techniques. Navigating regulatory landscapes and adhering to stringent performance and safety standards will remain paramount for success in this highly specialized and critical materials market.

- Sustained and robust market growth driven by escalating demand from high-performance industries.

- Continuous innovation in polymer chemistry and processing technologies is a key market accelerator.

- Increasing importance of sustainability and recyclability in product development and market positioning.

- Strategic investments in research and development are essential for competitive differentiation and market leadership.

- Geographic market expansion, particularly in rapidly industrializing regions, offers significant untapped potential.

- The critical role of heat resistant polymers in enabling technological advancements in next-generation applications.

Heat Resistant Polymer Market Drivers Analysis

The Heat Resistant Polymer market is significantly propelled by several powerful drivers, chief among them the escalating global demand for lightweight and high-performance materials across critical industries. The aerospace and defense sectors, for instance, continuously seek advanced polymers that offer superior strength-to-weight ratios and exceptional thermal stability, crucial for improving fuel efficiency, reducing emissions, and ensuring operational reliability in extreme atmospheric conditions. Similarly, the automotive industry, particularly with the rapid proliferation of electric vehicles, requires polymers that can withstand high temperatures for battery components, motor insulation, and structural parts while contributing to overall vehicle lightweighting for extended range and improved performance.

Another substantial driver is the continuous miniaturization and increased functionality of electronic devices, which necessitates heat resistant polymers for insulation, encapsulation, and circuit board substrates. These polymers ensure the durability and reliable operation of sensitive electronic components under elevated temperatures. Furthermore, the expansion of industrial applications, including high-temperature coatings, adhesives, and composites, driven by the need for enhanced operational efficiency and longer service life in harsh environments, consistently boosts market demand. Growth in the energy sector, particularly in oil and gas, and renewable energy, also contributes to market expansion as heat resistant polymers are vital for specialized equipment operating under extreme thermal and chemical stresses.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand from Aerospace and Defense industries for high-performance materials. | +0.8% | North America, Europe, Asia Pacific (China, India) | Long-term |

| Growing adoption in the Automotive sector, especially for Electric Vehicles (EVs) and lightweighting. | +0.7% | Asia Pacific (China, Japan, South Korea), Europe, North America | Mid-term |

| Miniaturization and performance requirements in the Electronics industry. | +0.6% | Asia Pacific (Taiwan, South Korea, China, Japan), North America | Mid-term |

| Expansion of Industrial applications requiring high-temperature resistance and chemical inertness. | +0.5% | Global, particularly developed and emerging industrial economies | Mid-term to Long-term |

| Growth in the Energy sector (Oil & Gas, Renewables) for high-performance components. | +0.4% | Middle East & Africa, North America, Europe | Long-term |

Heat Resistant Polymer Market Restraints Analysis

Despite the robust growth prospects, the Heat Resistant Polymer market faces several notable restraints that could temper its expansion. One primary concern is the relatively high production cost associated with these specialized polymers. The complex synthesis processes, stringent quality control requirements, and often expensive raw materials contribute significantly to the final product price, which can limit their widespread adoption in cost-sensitive applications or industries where more conventional, less expensive materials suffice. This cost barrier can pose a significant challenge, especially for new market entrants or smaller-scale operations seeking to integrate these advanced materials.

Furthermore, processing challenges associated with certain heat resistant polymers present another notable restraint. Many high-performance polymers require specific and often demanding processing conditions, such as high temperatures, high pressures, or specialized machinery, making manufacturing more complex and energy-intensive. This complexity can deter potential users or lead to higher manufacturing overheads. Volatility in raw material prices, often influenced by global supply chain disruptions or geopolitical factors, can also introduce instability and unpredictability in production costs, impacting profitability and strategic planning for market players. Lastly, increasingly stringent environmental regulations regarding polymer production and disposal, particularly concerning certain fluoropolymers or flame retardants, necessitate significant investment in R&D for compliant and sustainable alternatives, adding another layer of cost and complexity to market operations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High production cost and premium pricing compared to conventional polymers. | -0.7% | Global, particularly cost-sensitive markets | Mid-term |

| Complex and demanding processing techniques required for certain polymers. | -0.6% | Global, impacting manufacturing efficiency | Short-term to Mid-term |

| Volatility in raw material prices and supply chain disruptions. | -0.5% | Global, due to commodity market fluctuations | Short-term |

| Stringent environmental regulations and sustainability concerns. | -0.4% | Europe, North America, parts of Asia Pacific | Long-term |

Heat Resistant Polymer Market Opportunities Analysis

The Heat Resistant Polymer market is ripe with opportunities driven by technological advancements and evolving industrial needs. One significant opportunity lies in the burgeoning demand from emerging economies, particularly in Asia Pacific, where rapid industrialization, infrastructure development, and growing manufacturing capabilities are fueling the adoption of advanced materials across diverse sectors like automotive, electronics, and construction. These regions offer substantial untapped market potential as their industries increasingly shift towards higher performance and efficiency. Furthermore, continuous investment in research and development aimed at creating novel polymer compositions with enhanced properties presents a major avenue for growth. This includes developing next-generation materials that offer superior temperature resistance, mechanical strength, and chemical inertness, alongside improved processability and cost-effectiveness.

Another compelling opportunity arises from the accelerating global shift towards sustainable solutions. The development of recyclable, bio-based, and environmentally friendly heat resistant polymers, alongside more energy-efficient production processes, aligns with stringent environmental regulations and growing consumer preference for sustainable products. Companies that successfully innovate in this space can gain a significant competitive edge and address a critical market need. The increasing adoption of additive manufacturing (3D printing) technologies also opens new frontiers, allowing for the creation of complex geometries, customized parts, and rapid prototyping of heat resistant polymer components, thereby expanding their application scope significantly. Lastly, the expansion into new niche applications within healthcare (e.g., sterilization-resistant medical devices) and renewable energy (e.g., components for solar and wind power systems) presents specific, high-value opportunities for specialized polymer solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in emerging economies and industrialization in Asia Pacific. | +0.9% | Asia Pacific (China, India, Southeast Asia) | Long-term |

| R&D in novel and high-performance heat resistant polymer formulations. | +0.8% | Global, particularly North America, Europe, Japan | Long-term |

| Increasing focus on sustainable and recyclable heat resistant polymer solutions. | +0.7% | Europe, North America, Japan | Mid-term to Long-term |

| Expanding adoption of additive manufacturing (3D printing) for complex parts. | +0.6% | Global, particularly advanced manufacturing hubs | Mid-term |

| Untapped potential in new niche applications (e.g., healthcare, advanced sensors). | +0.5% | Global, highly specialized markets | Long-term |

Heat Resistant Polymer Market Challenges Impact Analysis

The Heat Resistant Polymer market faces several significant challenges that require strategic navigation for sustained growth. One primary concern is the intense competition among existing players, driven by continuous innovation and the introduction of new materials. This competitive landscape puts pressure on pricing, product differentiation, and market share, necessitating constant investment in R&D and efficient production processes. Maintaining a competitive edge requires not only technological superiority but also robust supply chain management and customer relationship strategies.

Another substantial challenge is the complexity of regulatory compliance, particularly concerning environmental, health, and safety standards. Different regions and countries have varying regulations on chemical production, use, and disposal, which can create barriers to market entry or increase operational costs for global manufacturers. Furthermore, ensuring consistent quality and performance across diverse applications, while simultaneously addressing the performance-cost trade-off, remains a persistent challenge. Balancing the need for cutting-edge properties with economically viable production scales is crucial for broader market adoption. Lastly, the inherent technical complexity involved in the synthesis and processing of these advanced polymers demands a highly skilled workforce and specialized infrastructure, which can be a limiting factor in certain geographies or for smaller enterprises.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense competition and pricing pressure among market players. | -0.8% | Global | Short-term to Mid-term |

| Stringent regulatory compliance and evolving environmental standards. | -0.7% | Europe, North America, rapidly developing economies | Mid-term to Long-term |

| Balancing high performance with cost-effectiveness for broader adoption. | -0.6% | Global, especially in volume-driven applications | Mid-term |

| Supply chain vulnerabilities and raw material scarcity for specialized monomers. | -0.5% | Global, impacting key manufacturing hubs | Short-term |

| Need for specialized processing equipment and skilled labor. | -0.4% | Global, impacting manufacturing scalability | Long-term |

Heat Resistant Polymer Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Heat Resistant Polymer market, offering a detailed assessment of its current landscape and future growth trajectory. The scope includes a thorough examination of market size estimations, historical trends, and precise forecasts extending through 2033. The report meticulously dissects key market attributes, including growth rates, drivers, restraints, opportunities, and challenges that collectively shape the industry's dynamics. It further provides extensive segmentation analysis across various polymer types, applications, and end-use industries, offering granular insights into specific market niches and growth segments. Crucially, the report features regional highlights, identifying key growth regions and countries, alongside a comprehensive overview of leading market players and their strategic initiatives, enabling stakeholders to make informed business decisions and capitalize on emerging trends.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 20.5 Billion |

| Market Forecast in 2033 | USD 34.8 Billion |

| Growth Rate | 6.9% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DuPont de Nemours, Inc.; Solvay S.A.; Victrex plc; Arkema S.A.; Celanese Corporation; Daikin Industries, Ltd.; 3M Company; Saint-Gobain S.A.; Asahi Kasei Corporation; Evonik Industries AG; Kureha Corporation; Ensinger GmbH; Mitsubishi Chemical Corporation; AGC Inc.; SABIC; Covestro AG; Sumitomo Chemical Co., Ltd.; Kuraray Co., Ltd.; Teijin Limited; Greene, Tweed & Co. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Heat Resistant Polymer market is comprehensively segmented to provide granular insights into its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper understanding of market niches, growth opportunities, and competitive landscapes across various product types, applications, and end-use industries. Analyzing the market by polymer type allows for an assessment of the demand and growth trajectories of specific high-performance polymers, such as Fluoropolymers, Polyimides (PI), Polyetheretherketone (PEEK), and Polyphenylene Sulfide (PPS), each possessing unique thermal, mechanical, and chemical properties suited for specialized requirements. This granular view helps identify leading material categories and emerging alternatives that are gaining traction.

Further segmentation by application provides clarity on how these polymers are being utilized across different product forms and functional roles, including coatings, adhesives, films, composites, and molded parts. This enables stakeholders to understand which application areas are experiencing the highest demand and where innovation is most impactful. Finally, the segmentation by end-use industry, encompassing critical sectors like aerospace & defense, automotive, electronics, industrial manufacturing, and healthcare, highlights the primary demand drivers and the specific performance requirements within each industry. This multi-dimensional segmentation is crucial for strategic planning, product development, and targeted market penetration, allowing businesses to tailor their offerings to precise market needs and capitalize on specific industry trends.

- By Type: Fluoropolymers (PTFE, PFA, FEP, ETFE, PVDF, ECTFE), Polyimides (PI), Polybenzimidazoles (PBI), Polyphenylene Sulfide (PPS), Polyetheretherketone (PEEK), Polysulfone (PSU), Polyketones (PK), Liquid Crystal Polymers (LCP), Polybenzoxazole (PBO), Others (Polyphthalamide (PPA), Polyamide Imide (PAI))

- By Application: Coatings, Adhesives & Sealants, Films & Foils, Composites, Fibers & Filaments, Foams, Additives, Insulators, Molded Parts, Others

- By End-Use Industry: Aerospace & Defense, Automotive (EV & ICE), Electronics & Electrical, Industrial Manufacturing, Healthcare & Medical, Energy (Oil & Gas, Renewable), Building & Construction, Consumer Goods, Packaging, Others

Regional Highlights

- North America: A mature market characterized by significant demand from the aerospace & defense, automotive, and electronics industries. The region benefits from robust R&D infrastructure and a strong focus on advanced manufacturing, with the United States being a key contributor.

- Europe: A leading region in sustainable polymer innovation and electric vehicle adoption. Germany, France, and the UK are prominent, driven by strong automotive, industrial machinery, and renewable energy sectors.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid industrialization, expanding manufacturing bases (especially in electronics and automotive), and increasing infrastructure development. China, Japan, South Korea, and India are pivotal markets.

- Latin America: An emerging market with growing industrial sectors, particularly automotive and construction. Brazil and Mexico are key countries, demonstrating increasing adoption of high-performance materials.

- Middle East and Africa (MEA): Growing demand from the oil & gas sector, along with emerging investments in infrastructure and manufacturing. Saudi Arabia, UAE, and South Africa are notable markets for specialized polymer applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Heat Resistant Polymer Market.- DuPont de Nemours, Inc.

- Solvay S.A.

- Victrex plc

- Arkema S.A.

- Celanese Corporation

- Daikin Industries, Ltd.

- 3M Company

- Saint-Gobain S.A.

- Asahi Kasei Corporation

- Evonik Industries AG

- Kureha Corporation

- Ensinger GmbH

- Mitsubishi Chemical Corporation

- AGC Inc.

- SABIC

- Covestro AG

- Sumitomo Chemical Co., Ltd.

- Kuraray Co., Ltd.

- Teijin Limited

- Greene, Tweed & Co.

Frequently Asked Questions

What are Heat Resistant Polymers?

Heat Resistant Polymers are a class of high-performance plastics designed to withstand elevated temperatures, harsh chemical environments, and mechanical stresses without significant degradation. They offer superior thermal stability, chemical resistance, and mechanical properties compared to conventional polymers, making them ideal for demanding applications in critical industries.

What are the primary applications of Heat Resistant Polymers?

These polymers are extensively used in aerospace for lightweight components, in automotive (especially EVs) for thermal management and structural parts, in electronics for insulation and encapsulation, and in various industrial applications like high-temperature coatings, adhesives, and composites, as well as in the energy and medical sectors.

Which regions are leading the Heat Resistant Polymer market?

North America and Europe are significant established markets, driven by advanced manufacturing and high R&D investments. However, Asia Pacific, particularly countries like China and India, is emerging as the fastest-growing region due to rapid industrialization and increasing demand from its booming electronics and automotive sectors.

What are the main drivers of the Heat Resistant Polymer market growth?

Key drivers include the escalating demand for lightweight, high-performance materials in aerospace, automotive (especially EVs), and electronics industries, coupled with continuous innovation in material science and the expansion of industrial applications requiring superior thermal and chemical resistance.

What challenges does the Heat Resistant Polymer market face?

Major challenges include the high production costs associated with these specialized materials, complex processing requirements, volatility in raw material prices, intense market competition, and the increasing stringency of environmental regulations requiring sustainable alternatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted