Gypsum and Anhydrite Market

Gypsum and Anhydrite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709922 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

Gypsum and Anhydrite Market Size

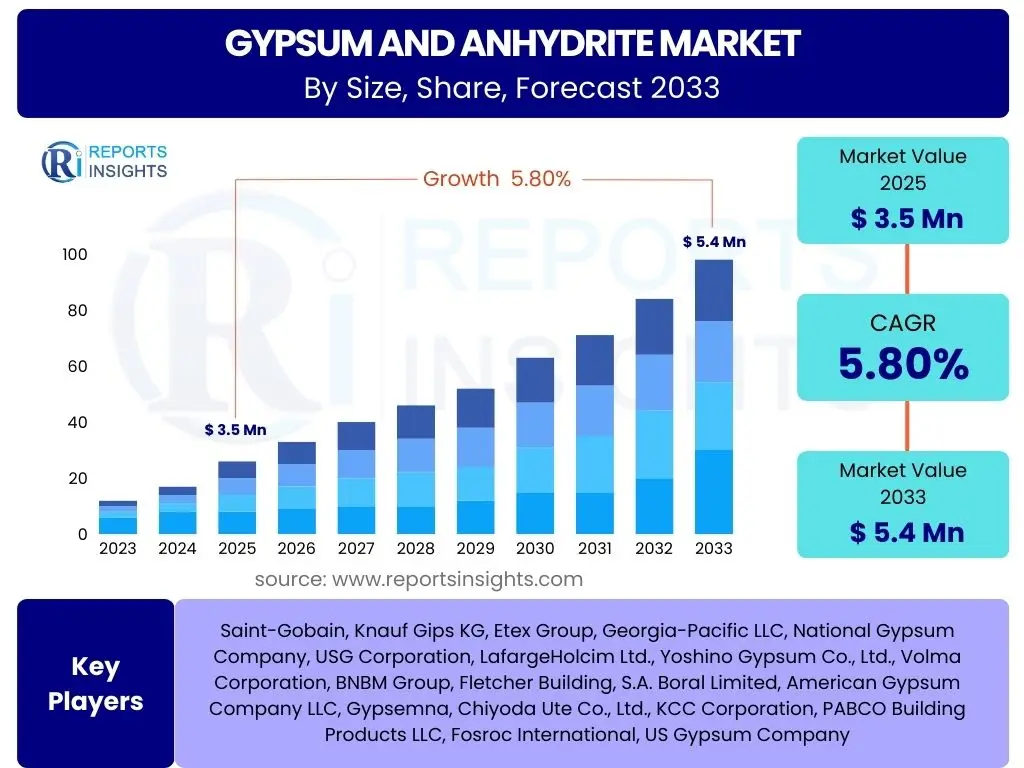

According to Reports Insights Consulting Pvt Ltd, The Gypsum and Anhydrite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 5.4 Billion by the end of the forecast period in 2033. This growth trajectory is primarily driven by consistent demand from the global construction industry, particularly for plasterboards, plasters, and cement manufacturing, alongside expanding applications in agriculture and industrial sectors.

The consistent expansion of urban infrastructure projects, residential and commercial building construction, and renovation activities across emerging and developed economies are key factors underpinning this market's resilience and growth. Furthermore, increasing awareness and adoption of sustainable building materials contribute significantly to the market's positive outlook. The market benefits from both natural reserves and the increasing availability of synthetic gypsum, particularly as a by-product of industrial processes, which offers a more environmentally friendly alternative.

Key Gypsum and Anhydrite Market Trends & Insights

The Gypsum and Anhydrite market is currently witnessing several transformative trends driven by evolving industry demands, technological advancements, and heightened environmental consciousness. Users frequently inquire about the shift towards sustainable materials, the impact of prefabrication, and innovations in gypsum-based product formulations. Key insights indicate a significant movement towards green building solutions, alongside increased adoption of synthetic gypsum due to its environmental benefits and consistent quality. Furthermore, the integration of advanced manufacturing techniques and the exploration of novel applications are reshaping market dynamics, moving beyond traditional construction uses.

A notable trend is the escalating demand for gypsum products in the context of circular economy principles. This includes initiatives for recycling gypsum waste from construction and demolition, as well as the increasing utilization of industrial by-products to produce synthetic gypsum. This not only addresses waste management concerns but also reduces reliance on virgin natural resources. Moreover, advancements in gypsum board technology, such as enhanced fire resistance, moisture resistance, and acoustic properties, are expanding their utility and appeal in diverse construction projects, fostering market innovation and competitive differentiation.

- Growing adoption of green building practices and certifications globally.

- Increased demand for synthetic gypsum, especially Flue Gas Desulfurization (FGD) gypsum, driven by environmental regulations and resource efficiency.

- Technological advancements in gypsum product manufacturing, leading to lightweight and high-performance materials.

- Expansion of prefabrication and modular construction methods, enhancing demand for standardized gypsum panels.

- Diversification of gypsum applications beyond traditional construction, including agriculture and niche industrial uses.

- Focus on recycling and circular economy principles for gypsum waste management.

AI Impact Analysis on Gypsum and Anhydrite

Common user questions regarding AI's impact on the Gypsum and Anhydrite market often revolve around efficiency improvements, quality control, and supply chain optimization. The integration of Artificial Intelligence (AI) and machine learning technologies is poised to significantly enhance operational efficiency and productivity across the entire value chain of gypsum and anhydrite production. From optimizing mining operations and raw material processing to improving manufacturing precision and logistics, AI offers capabilities that can reduce costs, minimize waste, and improve product quality. Predictive analytics, for instance, can forecast equipment failures, optimize energy consumption, and manage inventory more effectively.

AI's influence extends to enabling smarter decision-making in market forecasting and resource allocation. By analyzing vast datasets related to construction trends, economic indicators, and regulatory changes, AI algorithms can provide more accurate market predictions, allowing producers to adapt their strategies proactively. Furthermore, in product development, AI can accelerate the formulation of new gypsum-based materials with enhanced properties, simulating material behaviors and identifying optimal compositions. This technological integration is expected to foster innovation, create more resilient supply chains, and ultimately contribute to the market's sustainable growth by promoting resource efficiency and waste reduction.

- Predictive maintenance for mining and processing equipment, reducing downtime and operational costs.

- Enhanced quality control systems using AI-powered sensors and computer vision to monitor product consistency.

- Optimized logistics and supply chain management through AI algorithms for demand forecasting and route optimization.

- Improved raw material resource management and extraction efficiency through data analytics.

- Smart manufacturing processes, including automation and robotic applications in gypsum board production.

- Accelerated research and development of new gypsum composites and specialty products.

Key Takeaways Gypsum and Anhydrite Market Size & Forecast

Users frequently seek insights into the primary drivers and long-term outlook of the Gypsum and Anhydrite market, particularly concerning its stability and growth potential. The market is set for consistent expansion, primarily fueled by the global construction boom, particularly in residential and commercial infrastructure. This robust demand is complemented by the increasing adoption of sustainable building practices, which favors gypsum's inherent eco-friendly characteristics and the growing availability of synthetic gypsum. The market demonstrates resilience, underpinned by diverse applications ranging from essential building materials to specialized agricultural and industrial uses, ensuring a broad demand base.

Furthermore, technological advancements in material science and manufacturing processes are expected to introduce more efficient and high-performance gypsum products, opening new avenues for market penetration and value creation. While regional growth rates may vary, with developing economies showing higher expansion, the overall market trend is positive, supported by ongoing urbanization and infrastructure development worldwide. The forecast period highlights opportunities for innovation in product development and sustainable practices, which will be crucial for sustained market leadership and addressing evolving industry standards.

- Steady market growth projected at a 5.8% CAGR from 2025 to 2033, driven by construction and sustainability trends.

- Increasing global urbanization and infrastructure development are the primary demand drivers.

- Significant shift towards synthetic gypsum, offering environmental and economic benefits.

- Technological innovations are enhancing product performance and expanding application scopes.

- Asia Pacific and Middle East & Africa are expected to exhibit strong growth due to rapid development.

- Focus on circular economy principles and recycling of gypsum waste gaining prominence.

Gypsum and Anhydrite Market Drivers Analysis

The Gypsum and Anhydrite market is propelled by several robust drivers that reflect global economic and industrial trends. The most significant among these is the sustained growth in the construction sector worldwide, encompassing both residential and commercial infrastructure development. As populations expand and urbanization accelerates, the demand for building materials like plasterboards, plasters, and cement, all of which utilize gypsum, remains consistently high. Additionally, the increasing emphasis on sustainable and green building practices is favoring gypsum due to its non-toxic, fire-resistant, and recyclable properties, positioning it as a preferred material in modern construction.

Beyond traditional construction, the agricultural sector also presents a noteworthy driver. Anhydrite and gypsum are widely used as soil conditioners to improve soil structure, reduce alkalinity, and enhance nutrient absorption, particularly in regions with problematic soil compositions. The growing global focus on food security and agricultural productivity is therefore contributing to the demand for these minerals. Furthermore, the increasing availability and utilization of synthetic gypsum, derived from industrial processes such as Flue Gas Desulfurization (FGD), is offering a cost-effective and environmentally friendly alternative to natural gypsum, mitigating supply concerns and boosting overall market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing global construction activities (residential, commercial, infrastructure) | +1.8% | Asia Pacific, Middle East & Africa, Latin America, Global | Long-term (2025-2033) |

| Rising demand for green building materials and sustainable construction practices | +1.2% | Europe, North America, Global | Medium to Long-term (2025-2033) |

| Growth in the agricultural sector for soil conditioning and fertilizers | +0.7% | Asia Pacific, Latin America, North America | Long-term (2025-2033) |

| Increasing availability and utilization of synthetic gypsum from industrial by-products | +0.9% | North America, Europe, Asia Pacific | Medium to Long-term (2025-2033) |

Gypsum and Anhydrite Market Restraints Analysis

Despite its robust growth drivers, the Gypsum and Anhydrite market faces several significant restraints that could impede its full potential. One primary concern is the increasing stringency of environmental regulations, particularly concerning mining activities and industrial waste disposal. These regulations often lead to higher operational costs for extraction and processing of natural gypsum, and stringent requirements for managing synthetic gypsum by-products, thereby affecting profitability and potentially limiting supply. Furthermore, the volatility in energy and transportation costs directly impacts the cost of production and distribution, as gypsum is a bulk material, and its mining and manufacturing processes are energy-intensive.

Another restraint stems from the availability and adoption of substitute building materials. While gypsum boasts unique properties, alternative materials like cement boards, plywood, and other lightweight construction panels can sometimes offer competitive advantages in specific applications or cost-sensitive markets. Intense competition from these substitutes can limit market penetration and growth for gypsum products. Moreover, concerns related to health and safety, particularly concerning airborne dust during the handling and installation of gypsum products, necessitate adherence to strict safety protocols, adding to operational complexities and costs for manufacturers and end-users alike.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental regulations on mining and industrial by-product management | -1.0% | Europe, North America, Global | Ongoing (2025-2033) |

| Volatility in raw material (energy, transportation) prices | -0.8% | Global | Short to Medium-term (2025-2028) |

| Availability of substitute building materials (e.g., cement boards, wood) | -0.6% | Global | Long-term (2025-2033) |

| Health and safety concerns related to airborne gypsum dust during handling | -0.4% | Global | Ongoing (2025-2033) |

Gypsum and Anhydrite Market Opportunities Analysis

Numerous opportunities are emerging within the Gypsum and Anhydrite market, promising significant avenues for growth and innovation. A key opportunity lies in the expanding demand for synthetic gypsum, particularly as global industries increasingly focus on waste valorization and circular economy models. The effective utilization of by-products from power generation and chemical manufacturing to produce high-quality synthetic gypsum not only addresses waste disposal challenges but also provides a sustainable and consistent supply source, reducing reliance on natural reserves. This trend is further bolstered by governmental incentives and regulations promoting industrial symbiosis and resource efficiency.

Innovation in product development also presents a fertile ground for market expansion. The development of advanced gypsum-based products with enhanced properties such as superior moisture resistance, fire protection, sound insulation, and lightweight characteristics caters to modern construction demands for higher performance and greater energy efficiency. These specialty products command premium pricing and open new application segments in diverse construction environments, from high-rise buildings to specialized healthcare facilities. Furthermore, the burgeoning infrastructure development and urbanization in emerging economies, particularly in Asia Pacific, Latin America, and the Middle East & Africa, offer untapped markets with substantial growth potential for both traditional and innovative gypsum products, driven by large-scale public and private sector projects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing adoption and utilization of synthetic gypsum (e.g., FGD gypsum) | +1.5% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Innovation in gypsum-based product development (e.g., high-performance, lightweight, moisture-resistant) | +1.0% | Global | Medium to Long-term (2025-2033) |

| Expansion into emerging economies with significant infrastructure development and urbanization | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Growing demand for gypsum in niche applications such as industrial fillers, medical casts, and chemical processes | +0.6% | Global | Medium-term (2025-2030) |

Gypsum and Anhydrite Market Challenges Impact Analysis

The Gypsum and Anhydrite market faces several notable challenges that require strategic navigation by industry players. One significant challenge is the ongoing issue of supply chain disruptions, which can stem from geopolitical events, natural disasters, or global health crises. Such disruptions impact the availability and timely delivery of raw materials and finished products, leading to production delays and increased operational costs. The bulk nature of gypsum products also makes them susceptible to logistics bottlenecks, especially in regions with underdeveloped transportation infrastructure, thereby affecting market reach and competitiveness.

Another crucial challenge involves the effective management and recycling of gypsum waste. While gypsum is recyclable, the collection, sorting, and processing of construction and demolition waste containing gypsum can be complex and expensive. Insufficient recycling infrastructure and a lack of standardized practices contribute to landfilling, which not only poses environmental concerns but also represents a lost resource. Furthermore, the market faces competition from a growing array of alternative eco-friendly building materials, which, while sometimes higher in initial cost, are marketed aggressively on their sustainability credentials. This necessitates continuous innovation and clear communication of gypsum's own environmental benefits to maintain market share against these emerging alternatives.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain disruptions and logistics bottlenecks | -0.9% | Global | Short to Medium-term (2025-2028) |

| Effective management and recycling of gypsum waste from construction and demolition | -0.7% | Europe, North America, Global | Ongoing (2025-2033) |

| High energy consumption and associated carbon footprint in gypsum production | -0.5% | Global | Ongoing (2025-2033) |

| Competition from alternative and emerging eco-friendly building materials | -0.4% | Global | Long-term (2025-2033) |

Gypsum and Anhydrite Market - Updated Report Scope

This market research report provides an in-depth, comprehensive analysis of the global Gypsum and Anhydrite market, offering strategic insights into its size, growth trajectory, key trends, and future outlook. The scope encompasses detailed market segmentation, regional dynamics, competitive landscape analysis, and an assessment of key drivers, restraints, opportunities, and challenges influencing the industry. It aims to equip stakeholders with critical information for informed decision-making and strategic planning within this dynamic market. The report also highlights the impact of technological advancements, including AI, and the growing importance of sustainability across the value chain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.4 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Saint-Gobain, Knauf Gips KG, Etex Group, Georgia-Pacific LLC, National Gypsum Company, USG Corporation, LafargeHolcim Ltd., Yoshino Gypsum Co., Ltd., Volma Corporation, BNBM Group, Fletcher Building, S.A. Boral Limited, American Gypsum Company LLC, Gypsemna, Chiyoda Ute Co., Ltd., KCC Corporation, PABCO Building Products LLC, Fosroc International, US Gypsum Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global Gypsum and Anhydrite market is meticulously segmented to provide a granular view of its diverse components, allowing for targeted analysis and strategic planning. These segmentations categorize the market based on the origin of the material (type), its end-use applications, and the physical form in which it is primarily utilized. Understanding these distinctions is crucial for identifying specific growth pockets, competitive landscapes, and evolving consumer preferences across various industrial and geographical domains. Each segment reflects unique market dynamics driven by technological advancements, regulatory frameworks, and economic development, offering comprehensive insights into the industry's structure and potential.

The segmentation by type differentiates between natural gypsum, directly mined from deposits, and synthetic gypsum, which is a by-product of industrial processes such as flue gas desulfurization (FGD), phosphogypsum from fertilizer production, and citric acid gypsum. Application-wise, the market is broadly divided into building and construction, agriculture, industrial uses, and medical applications, with building and construction being the dominant segment. Within these, specific sub-segments like plasterboards, cement manufacturing, soil conditioners, and dental plasters highlight the varied utility of gypsum and anhydrite. Finally, the form segmentation distinguishes between powder, blocks/panels, and other processed forms, reflecting different stages of value addition and end-product formats.

- By Type: Natural Gypsum, Synthetic Gypsum (Flue Gas Desulfurization (FGD) Gypsum, Phosphogypsum, Citric Acid Gypsum, Others)

- By Application: Building & Construction (Plaster, Plasterboard/Drywall, Cement Manufacturing, Insulation Materials, Decorative Products, Others), Agriculture (Soil Conditioner, Fertilizer, Pest Control), Industrial (Filler Material, Desiccant, Chemical Processes, Glass Manufacturing, Paper & Pulp Industry), Medical (Dental Plaster, Orthopedic Casts), Others

- By Form: Powder, Blocks/Panels, Aggregates, Other Forms

Regional Highlights

- Asia Pacific (APAC): Positioned as the largest and fastest-growing market for Gypsum and Anhydrite, driven by rapid urbanization, significant infrastructure development, and a booming construction sector in countries like China, India, and Southeast Asian nations. The region's expanding population and industrialization fuel demand across all application segments, especially in residential and commercial building.

- North America: A mature market characterized by robust demand for renovation and remodeling activities, alongside new commercial construction. The region exhibits high adoption rates of synthetic gypsum, particularly FGD gypsum, due to stringent environmental regulations and well-established industrial infrastructure for its production and utilization. Emphasis on sustainable construction practices further drives market evolution.

- Europe: This region is marked by stringent environmental regulations, a strong focus on green building initiatives, and advanced recycling practices for gypsum waste. While construction growth might be moderate compared to APAC, the demand for high-performance, sustainable, and energy-efficient gypsum products remains strong. Germany, France, and the UK are key markets, focusing on innovation and circular economy principles.

- Latin America: An emerging market demonstrating significant growth potential, primarily propelled by increasing residential and commercial construction activities, coupled with growing investments in infrastructure projects. Countries like Brazil and Mexico are leading the demand, also showing rising interest in gypsum for agricultural applications to improve soil quality and crop yields.

- Middle East & Africa (MEA): This region is experiencing substantial growth in the Gypsum and Anhydrite market due to extensive investments in large-scale infrastructure projects, diversification efforts away from oil economies, and rapid urbanization. Countries in the GCC region, such as Saudi Arabia and the UAE, are major consumers, driving demand for high-quality building materials for ambitious construction endeavors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gypsum and Anhydrite Market.- Saint-Gobain

- Knauf Gips KG

- Etex Group

- Georgia-Pacific LLC

- National Gypsum Company

- USG Corporation

- LafargeHolcim Ltd.

- Yoshino Gypsum Co., Ltd.

- Volma Corporation

- BNBM Group

- Fletcher Building

- S.A. Boral Limited

- American Gypsum Company LLC

- Gypsemna

- Chiyoda Ute Co., Ltd.

- KCC Corporation

- PABCO Building Products LLC

- Fosroc International

- US Gypsum Company

Frequently Asked Questions

What are the primary applications of gypsum and anhydrite?

Gypsum and anhydrite are primarily used in the building and construction sector for manufacturing plasterboards (drywall), plasters, and as an additive in cement production. Beyond construction, they find significant applications in agriculture as soil conditioners to improve soil structure and nutrient absorption, and in various industrial processes as fillers, desiccants, and in chemical manufacturing. Anhydrite also has specific uses in floor screeds and as an industrial filler.

What is the difference between natural and synthetic gypsum?

Natural gypsum is a mineral (hydrous calcium sulfate) extracted from mines, formed by the evaporation of saline water. Synthetic gypsum, conversely, is a by-product of industrial processes, predominantly Flue Gas Desulfurization (FGD) in coal-fired power plants, but also from phosphoric acid production (phosphogypsum) and citric acid manufacturing. Both forms are chemically similar and possess comparable properties, making synthetic gypsum a viable and increasingly preferred alternative due to its sustainable origin and consistent quality.

How is the global Gypsum and Anhydrite market segmented?

The global market is segmented primarily by Type (Natural Gypsum, Synthetic Gypsum including FGD, Phosphogypsum, Citric Acid Gypsum, and others), by Application (Building & Construction, Agriculture, Industrial, Medical, and Others, with sub-segments like plasterboard, cement, soil conditioner, dental plaster), and by Form (Powder, Blocks/Panels, Aggregates, and Other Forms). This detailed segmentation helps analyze market dynamics and growth across diverse product categories and end-use industries.

What factors are driving the growth of the Gypsum and Anhydrite market?

The primary drivers include the robust growth of the global construction industry, particularly in residential and commercial sectors, increasing urbanization, and significant infrastructure development in emerging economies. Additionally, the rising adoption of sustainable and green building practices favors gypsum's environmentally friendly properties. The growing use of gypsum in agriculture as a soil conditioner and the increasing availability of synthetic gypsum also contribute substantially to market expansion.

What is the role of sustainability in the Gypsum and Anhydrite industry?

Sustainability plays a crucial role in the gypsum and anhydrite industry, driving innovation and market trends. It encompasses the increased utilization of synthetic gypsum, which reduces reliance on virgin resources and valorizes industrial waste. Furthermore, efforts are focused on improving energy efficiency in production, reducing carbon emissions, and developing advanced recycling technologies for gypsum waste from construction and demolition. These initiatives align with circular economy principles, promoting resource efficiency and minimizing environmental impact throughout the product lifecycle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted