Gold Loan Market

Gold Loan Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701542 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

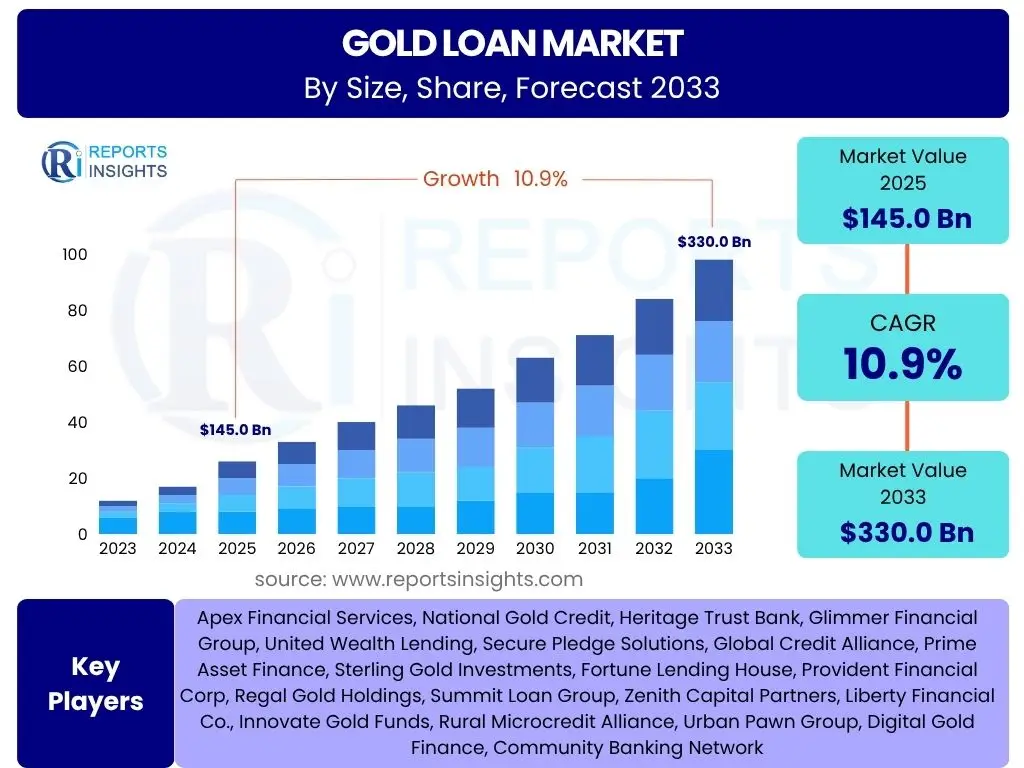

Gold Loan Market Size

According to Reports Insights Consulting Pvt Ltd, The Gold Loan Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.9% between 2025 and 2033. The market is estimated at USD 145.0 Billion in 2025 and is projected to reach USD 330.0 Billion by the end of the forecast period in 2033.

Key Gold Loan Market Trends & Insights

The Gold Loan market is currently experiencing significant shifts driven by evolving consumer financial needs, technological advancements, and a dynamic regulatory landscape. Common user inquiries often focus on the digitalization of lending processes, the increasing appeal of gold loans as a quick and accessible credit option, and the integration of advanced analytics for enhanced risk assessment. These trends highlight a market moving towards greater efficiency, transparency, and customer-centricity, adapting to modern financial ecosystems while retaining its traditional core value proposition.

- Digitization of application and disbursal processes for enhanced customer convenience.

- Rising demand for quick and hassle-free credit, particularly from underbanked populations.

- Increasing financial literacy and awareness regarding gold loans as a viable credit alternative.

- Growing integration of advanced analytics and data science for personalized offerings and risk mitigation.

- Expansion into semi-urban and rural areas, leveraging branch networks and digital outreach.

AI Impact Analysis on Gold Loan

User queries regarding AI's impact on gold loans frequently revolve around its potential to streamline operations, improve risk assessment, and personalize customer experiences. There is significant interest in how AI can automate loan application processing, reduce turnaround times, and detect fraud more effectively. Furthermore, users often inquire about AI's role in offering tailored loan products based on individual borrower profiles and predicting market trends, showcasing an expectation for more efficient, secure, and customized gold loan services in the future.

- Automated credit scoring and fraud detection, improving accuracy and reducing processing time.

- Personalized loan offers and dynamic interest rates based on AI-driven customer profiling.

- Enhanced risk management through predictive analytics for gold price fluctuations and repayment behaviors.

- Streamlined customer service via AI-powered chatbots and virtual assistants for query resolution.

- Optimized operational efficiency in loan origination, disbursal, and collection processes.

Key Takeaways Gold Loan Market Size & Forecast

The projected growth of the Gold Loan market underscores its escalating significance as a flexible and accessible credit avenue, particularly for individuals and small businesses seeking immediate liquidity against tangible assets. Key takeaways from the market size and forecast data emphasize the resilient nature of gold as collateral and the sector's adaptability to economic fluctuations. The substantial increase in market valuation is indicative of rising consumer trust, expanding financial inclusion initiatives, and the strategic embrace of digital platforms by lenders to broaden their reach and enhance service delivery.

- Robust market expansion signals increasing reliance on gold as a credible and accessible collateral.

- Digital transformation is a critical accelerator for market penetration and operational efficiency.

- Financial inclusion efforts, especially in emerging economies, are significant growth catalysts.

- Stable gold prices and economic uncertainties often drive demand for immediate liquidity through gold loans.

- Competitive landscape necessitates innovation in product offerings and customer service.

Gold Loan Market Drivers Analysis

The Gold Loan market's trajectory is primarily propelled by several macroeconomic and behavioral factors. Economic uncertainties often drive individuals and small businesses to seek quick, collateral-backed credit. The inherent ease and speed of securing a gold loan, coupled with its relatively less stringent eligibility criteria compared to traditional bank loans, make it an attractive option for immediate financial needs. Furthermore, growing financial literacy and an increasing comfort with non-banking financial institutions (NBFCs) are contributing significantly to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Quick and Accessible Credit | +2.5% | Global, particularly Emerging Economies (India, China, Southeast Asia) | Short to Medium-term (2025-2029) |

| Ease of Loan Processing and Minimal Documentation | +1.8% | Asia Pacific, Africa, Latin America | Medium-term (2026-2030) |

| Financial Inclusion Initiatives and Penetration in Rural Areas | +2.0% | India, Southeast Asia, Sub-Saharan Africa | Long-term (2027-2033) |

| Rising Gold Prices and Asset Monetization | +1.5% | Global, especially Gold-rich regions | Fluctuating, but overall positive (2025-2033) |

| Technological Advancements and Digitalization of Services | +1.2% | Global, particularly developed and rapidly digitizing emerging markets | Ongoing (2025-2033) |

Gold Loan Market Restraints Analysis

Despite its significant growth potential, the Gold Loan market faces several restraints that could impede its expansion. Volatility in gold prices poses a substantial risk, directly impacting the value of collateral and the loan-to-value (LTV) ratio, potentially leading to lower loan amounts or margin calls for borrowers. Regulatory challenges, including stringent norms on lending practices and interest rate caps, can limit the profitability and operational flexibility of lenders. Furthermore, the stigma associated with pledging gold, particularly in some traditional societies, and the increasing competition from alternative credit sources, can deter potential borrowers, presenting hurdles to sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Gold Prices | -1.5% | Global | Continuous (2025-2033) |

| Stringent Regulatory Frameworks and Compliance Costs | -1.0% | India, China, European Union | Medium to Long-term (2026-2033) |

| Competition from Formal Banking Channels and FinTech Lenders | -1.2% | Developed Markets, Urban Areas in Emerging Economies | Ongoing (2025-2033) |

| Perceived Stigma or Social Taboos Associated with Pledging Gold | -0.8% | Certain parts of Asia Pacific (e.g., India), Middle East | Long-term, Gradual Change (2025-2033) |

| Risk of Gold Theft and Security Concerns for Lenders | -0.5% | Global, particularly regions with higher crime rates | Continuous (2025-2033) |

Gold Loan Market Opportunities Analysis

The Gold Loan market is poised for significant opportunities, driven by untapped potential in underserved populations and the increasing adoption of digital financial services. Expanding into rural and semi-urban areas, where access to formal credit is limited and gold holdings are substantial, presents a vast growth avenue. The development of innovative gold loan products, such as those integrated with digital wallets or offering flexible repayment options, can attract a wider demographic. Furthermore, strategic partnerships with FinTech companies can enhance digital outreach and operational efficiency, leveraging technology to reach previously inaccessible segments and streamline the lending process.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Rural and Semi-Urban Markets | +2.0% | Asia Pacific (India, Indonesia), Latin America, Africa | Long-term (2027-2033) |

| Innovation in Digital Gold Loan Products and Services | +1.8% | Global, especially digitally mature markets | Medium-term (2026-2030) |

| Strategic Partnerships with FinTech Companies and Payment Platforms | +1.5% | Global | Short to Medium-term (2025-2029) |

| Focus on Micro and Small Enterprises (MSMEs) for Business Loans | +1.0% | Emerging Economies (India, Brazil, Nigeria) | Medium-term (2026-2030) |

| Expansion into New Geographies with High Gold Holdings | +0.8% | Middle East, North Africa, parts of Europe | Long-term (2028-2033) |

Gold Loan Market Challenges Impact Analysis

The Gold Loan market faces several significant challenges that could hinder its growth and stability. Ensuring the safety and security of pledged gold, given the inherent value and liquidity of the asset, remains a paramount concern for lenders. This includes managing storage, transportation, and insurance against theft or damage. Moreover, maintaining public trust and combating fraudulent activities are critical, as any lapse in integrity can severely impact market perception. The competitive landscape, characterized by the entry of new players and evolving consumer preferences, demands continuous innovation in product offerings and service delivery, posing a dynamic challenge for established entities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Security and Safe Custody of Gold Collateral | -1.0% | Global | Continuous (2025-2033) |

| Maintaining Customer Trust and Combating Fraudulent Activities | -0.8% | Global | Continuous (2025-2033) |

| Intense Competition and Price Wars Among Lenders | -0.7% | Urban areas, highly penetrated markets (e.g., India) | Short to Medium-term (2025-2029) |

| Managing Non-Performing Assets (NPAs) Due to Repayment Defaults | -0.5% | Global, particularly during economic downturns | Cyclical (2025-2033) |

| Talent Acquisition and Retention for Specialized Roles | -0.3% | Global, especially for digital and analytical roles | Medium to Long-term (2026-2033) |

Gold Loan Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Gold Loan market, covering historical performance, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report also includes detailed segmentation analysis by various parameters, regional breakdowns, competitive assessments of key players, and an examination of emerging trends and their impact on market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 145.0 Billion |

| Market Forecast in 2033 | USD 330.0 Billion |

| Growth Rate | 10.9% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Apex Financial Services, National Gold Credit, Heritage Trust Bank, Glimmer Financial Group, United Wealth Lending, Secure Pledge Solutions, Global Credit Alliance, Prime Asset Finance, Sterling Gold Investments, Fortune Lending House, Provident Financial Corp, Regal Gold Holdings, Summit Loan Group, Zenith Capital Partners, Liberty Financial Co., Innovate Gold Funds, Rural Microcredit Alliance, Urban Pawn Group, Digital Gold Finance, Community Banking Network |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Gold Loan market is comprehensively segmented to provide granular insights into its diverse components and dynamics. This segmentation facilitates a deeper understanding of market drivers and consumer behaviors across different lending entities, loan applications, and borrower types. Analyzing these distinct segments helps stakeholders identify specific growth opportunities, tailor financial products, and develop targeted marketing strategies to effectively serve varied customer needs and market niches.

- By Lender Type: Categorizes the market based on the primary entities offering gold loans, including traditional Banks, specialized Non-Banking Financial Companies (NBFCs), and other informal or semi-formal lenders such as Pawn Brokers and Cooperative Societies. Each type has distinct operational models and customer bases.

- By Loan Purpose: Differentiates the market by the specific reasons borrowers seek gold loans, encompassing Agricultural Loans for farmers, Personal Loans for individual needs, Business Loans for entrepreneurs and SMEs, and Other purposes like healthcare or education financing.

- By End-user: Segments the market based on the recipient of the loan, distinguishing between Individual Borrowers seeking personal credit, Small and Medium Enterprises (SMEs) utilizing gold as collateral for business expansion, and Farmers who often leverage gold assets for agricultural needs.

- By Gold Purity: Divides the market based on the fineness of the gold pledged as collateral, typically ranging from 18K to 24K. This impacts the loan-to-value ratio and the assessment process.

- By Loan Tenure: Classifies loans based on their repayment period, including Short-term (typically up to 6 months), Medium-term (6 months to 1 year), and Long-term (above 1 year) options, catering to different liquidity requirements and repayment capacities.

Regional Highlights

- Asia Pacific (APAC): Dominates the Gold Loan market, driven by cultural significance of gold, high household gold holdings, and a large unbanked or underbanked population seeking quick credit. Countries like India and China are major contributors, with robust growth in semi-urban and rural areas fueled by financial inclusion initiatives and a strong presence of NBFCs.

- North America: Exhibits a niche but growing market, primarily through pawn shops and specialized lenders. Demand is often driven by short-term liquidity needs or for individuals with limited access to conventional credit. Regulatory frameworks are stricter, influencing market structure.

- Europe: The market is relatively mature and smaller compared to APAC, with gold loans typically serving as a last resort or for niche segments. Pawn brokerage remains a traditional channel, with increasing interest in digital platforms for convenience, though cultural acceptance varies by country.

- Latin America: Showing nascent growth, propelled by economic volatility and the need for accessible credit solutions. Countries like Brazil and Mexico are witnessing a gradual rise in gold loan adoption, with potential for further expansion as financial literacy improves and digital infrastructure develops.

- Middle East and Africa (MEA): Emerging as a potential growth region, particularly in countries with significant gold reserves and cultural affinity for gold. The demand for sharia-compliant financial products, including gold-backed financing, presents a unique opportunity, alongside efforts to formalize informal lending sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gold Loan Market.- Apex Financial Services

- National Gold Credit

- Heritage Trust Bank

- Glimmer Financial Group

- United Wealth Lending

- Secure Pledge Solutions

- Global Credit Alliance

- Prime Asset Finance

- Sterling Gold Investments

- Fortune Lending House

- Provident Financial Corp

- Regal Gold Holdings

- Summit Loan Group

- Zenith Capital Partners

- Liberty Financial Co.

- Innovate Gold Funds

- Rural Microcredit Alliance

- Urban Pawn Group

- Digital Gold Finance

- Community Banking Network

Frequently Asked Questions

Analyze common user questions about the Gold Loan market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a gold loan and how does it work?

A gold loan is a secured loan where individuals pledge their gold ornaments or coins as collateral to a lender in exchange for a sum of money. The loan amount is typically a percentage of the gold's market value, known as the Loan-to-Value (LTV) ratio. Borrowers repay the principal amount along with interest over a predetermined tenure, after which their gold is returned. It's a quick and accessible way to secure funds, as eligibility is primarily based on the value of the gold rather than credit history.

What are the typical interest rates for gold loans?

Gold loan interest rates vary significantly based on the lender type (banks, NBFCs), the loan amount, tenure, and prevailing market conditions. Generally, interest rates for gold loans can range from 7% to 29% annually. NBFCs might offer quicker processing but at slightly higher rates, while banks may offer lower rates with more stringent processes. It is crucial for borrowers to compare interest rates and associated charges from various lenders before committing to a loan.

What documents are required to apply for a gold loan?

Applying for a gold loan typically requires minimal documentation compared to unsecured loans. Essential documents usually include identity proof (e.g., Aadhar card, Passport, Driving License, PAN card) and address proof (e.g., Aadhar card, Utility bills, Voter ID). Some lenders may also require proof of income, especially for larger loan amounts or specific schemes, but for most standard gold loans, the process is streamlined and quick.

How is the value of gold assessed for a loan?

The value of gold for a loan is assessed based on its weight and purity (karat). Lenders typically use a certified gold appraiser to accurately determine the gold's fineness and current market rate. The loan amount is then calculated by applying the prevailing Loan-to-Value (LTV) ratio, which is regulated by financial authorities, ensuring borrowers receive a fair and consistent valuation for their pledged gold assets.

What are the benefits of choosing a gold loan over other credit options?

Gold loans offer several distinct advantages, making them an attractive credit option. They provide quick access to funds with minimal documentation and processing time, making them ideal for urgent financial needs. Since gold loans are secured, they typically feature lower interest rates compared to unsecured personal loans. Furthermore, they do not usually require a strong credit score, making them accessible to a wider range of borrowers, and repayment options are often flexible to suit individual financial capacities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted