GNSS Receiver Market

GNSS Receiver Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705511 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

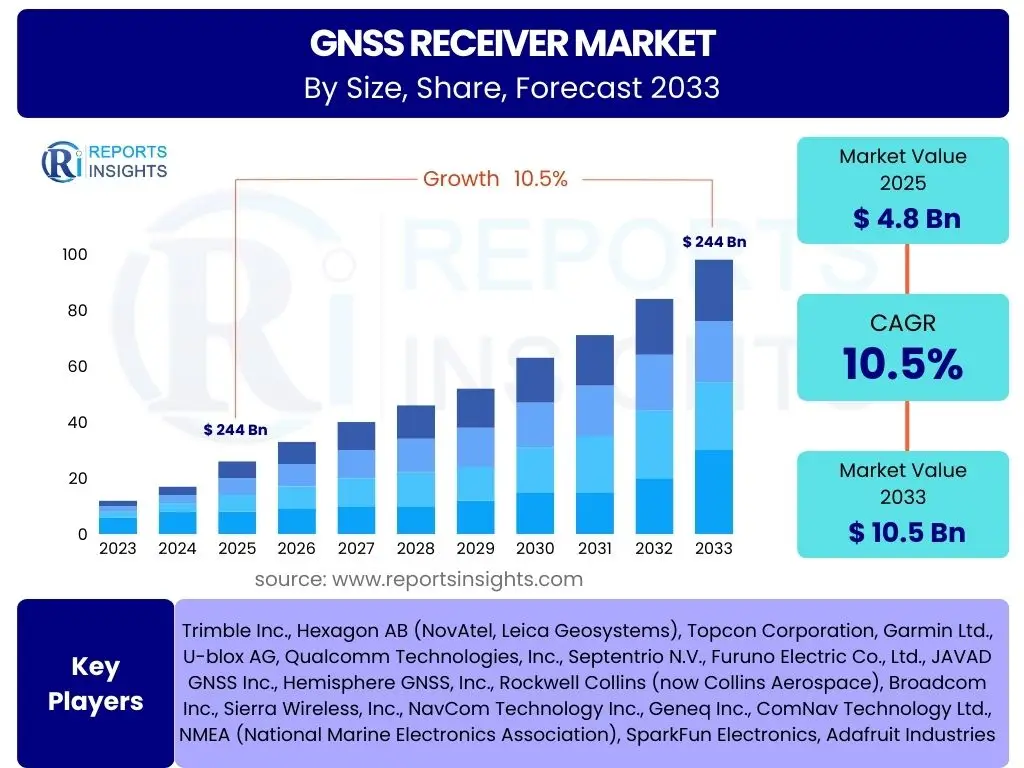

GNSS Receiver Market Size

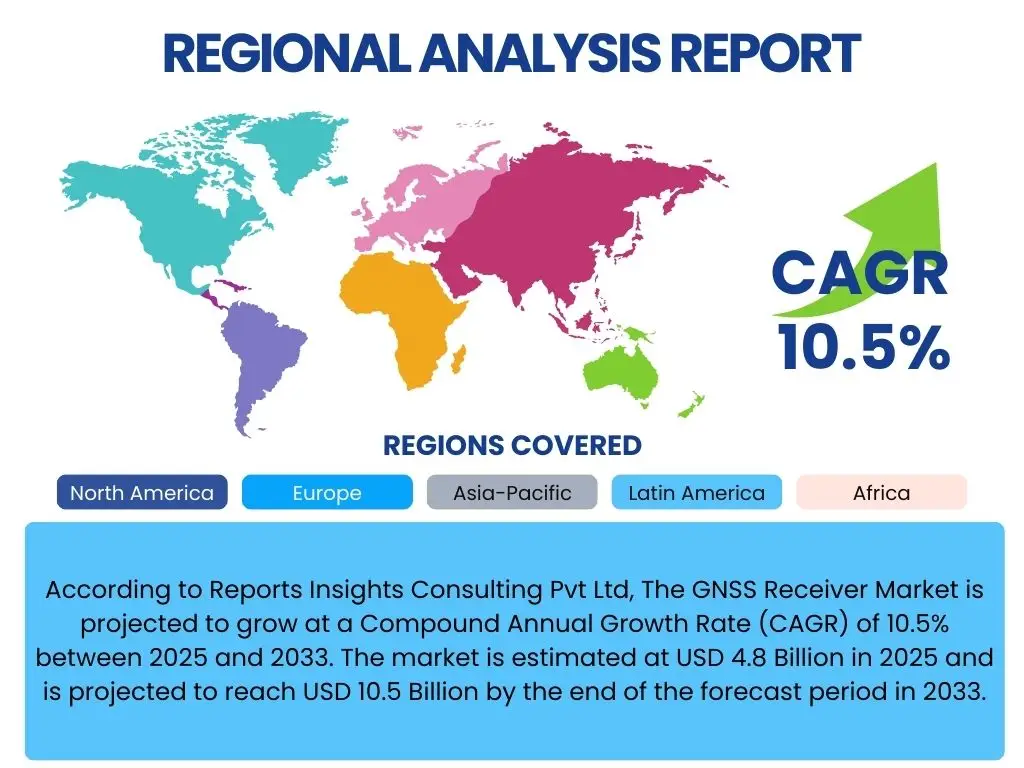

According to Reports Insights Consulting Pvt Ltd, The GNSS Receiver Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 10.5 Billion by the end of the forecast period in 2033.

Key GNSS Receiver Market Trends & Insights

The global GNSS receiver market is currently undergoing significant transformation, driven by an escalating demand for high-precision positioning across various sectors. Users are frequently inquiring about the technological advancements that are shaping this market, specifically focusing on how new constellations, multi-frequency capabilities, and improved accuracy are impacting adoption and application development. A key trend is the transition from single-constellation, single-frequency receivers to multi-constellation, multi-frequency devices, which significantly enhance positioning accuracy, reliability, and availability, particularly in challenging environments like urban canyons or under dense foliage. This advancement is crucial for emerging applications that demand centimeter-level precision.

Another prominent trend is the miniaturization and cost reduction of GNSS receivers, making them more accessible for integration into a broader range of consumer and industrial devices. This trend addresses user questions about the feasibility of incorporating GNSS technology into compact and affordable solutions, such as wearables, IoT devices, and drones. Furthermore, the convergence of GNSS with other positioning technologies, like Inertial Measurement Units (IMUs) and vision systems, is creating robust PNT (Positioning, Navigation, and Timing) solutions. This hybrid approach mitigates the limitations of standalone GNSS, providing seamless and uninterrupted positioning even when satellite signals are obstructed or unavailable, thereby improving overall system resilience and performance.

The increasing sophistication of software-defined GNSS receivers is also a notable development, allowing for greater flexibility, upgradability, and adaptability to evolving GNSS signals and standards. This trend aligns with user interest in future-proof technologies that can be updated remotely, reducing hardware replacement cycles and supporting new functionalities. Moreover, the expansion of commercial GNSS augmentation services, such as SBAS (Satellite-Based Augmentation Systems) and PPP (Precise Point Positioning) services, is democratizing access to high-accuracy positioning, enabling a wider array of applications beyond traditional surveying and military uses. These services are crucial for sectors like agriculture, construction, and autonomous vehicles, where precise real-time positioning is paramount.

- Multi-constellation and multi-frequency support for enhanced accuracy and reliability.

- Miniaturization and cost reduction of GNSS modules for broader integration.

- Convergence with IMUs and other sensors for robust PNT solutions.

- Growth of software-defined GNSS (SD-GNSS) for flexibility and upgradability.

- Expansion of commercial augmentation services (SBAS, PPP) for high-accuracy positioning.

- Integration into IoT devices and autonomous systems.

- Development of robust anti-jamming and anti-spoofing capabilities.

AI Impact Analysis on GNSS Receiver

User queries regarding the impact of Artificial Intelligence (AI) on GNSS receivers frequently center on how AI can improve performance, especially in challenging environments, and enable new functionalities. AI and machine learning (ML) are significantly enhancing GNSS receiver capabilities by enabling more sophisticated signal processing. AI algorithms can effectively filter out noise, mitigate interference (including jamming and spoofing), and detect weak signals that traditional processing methods might miss. This leads to higher accuracy, greater reliability, and improved signal availability, particularly in urban canyons, dense foliage, or environments with deliberate interference, which are common pain points for GNSS users.

Furthermore, AI is pivotal in improving the integration and fusion of GNSS data with data from other sensors, such as IMUs, cameras, lidar, and radar. By employing advanced AI-driven sensor fusion techniques, receivers can create more accurate and resilient positioning solutions. AI models can learn patterns from diverse sensor inputs, predict signal availability, and compensate for GNSS outages or inaccuracies, leading to seamless navigation and precise localization for autonomous vehicles, drones, and robotics. This addresses the critical need for continuous and highly reliable positioning in safety-critical applications, reducing dependence on a single positioning source.

AI also contributes to the predictive maintenance and self-optimization of GNSS receivers. Machine learning algorithms can analyze receiver performance data over time, identify potential issues, and suggest adjustments to optimize signal acquisition and tracking. Moreover, AI is enabling adaptive GNSS systems that can learn from their environment and adjust their operational parameters dynamically, such as selecting the best combination of satellite signals or adjusting tracking loops based on real-time conditions. This level of intelligent operation minimizes human intervention, improves operational efficiency, and extends the effective lifespan of GNSS equipment, delivering significant value to end-users concerned with system uptime and performance stability.

- Enhanced signal processing and noise reduction for improved accuracy.

- Advanced interference mitigation (jamming, spoofing) through intelligent filtering.

- Improved sensor fusion for robust and continuous positioning in multi-sensor systems.

- Predictive modeling for signal availability and performance optimization.

- Enabling adaptive GNSS receivers that learn from environmental conditions.

- Facilitating autonomous navigation and robotic control through precise localization.

- Automated fault detection and diagnostic capabilities for proactive maintenance.

Key Takeaways GNSS Receiver Market Size & Forecast

User inquiries about key takeaways from the GNSS receiver market size and forecast consistently highlight the drivers of growth, the segments experiencing the most significant expansion, and the long-term viability of the technology. A primary takeaway is the robust growth trajectory, driven by the escalating demand for highly accurate and reliable positioning, navigation, and timing (PNT) solutions across a multitude of industries. This growth is not merely incremental but represents a fundamental shift towards integrating advanced GNSS capabilities into critical infrastructure and emerging technologies, underscoring its foundational role in the digital economy.

Another significant insight is the diversification of applications beyond traditional surveying and military uses. Sectors such as autonomous vehicles, precision agriculture, smart cities, and IoT are rapidly adopting GNSS technology, each contributing substantially to market expansion. This broad adoption is facilitated by ongoing innovations in receiver technology, including miniaturization, multi-frequency support, and enhanced robustness against interference, which collectively address the diverse needs and operational environments of these new application areas. The market's resilience is further bolstered by continuous investment in satellite constellations and augmentation systems, ensuring global coverage and improved signal quality.

The forecast also underscores the increasing strategic importance of GNSS technology, moving from a niche component to a critical enabler of automation and digitalization. The market's projected growth is a clear indicator of its indispensability in modern industrial and consumer ecosystems, with a strong emphasis on achieving higher levels of precision and integrity. This evolution necessitates ongoing research and development in areas like anti-spoofing and anti-jamming technologies, as well as the integration with other PNT sources, to maintain security and reliability, reinforcing the market's long-term potential for innovation and expansion.

- Strong market growth driven by demand for high-precision PNT solutions.

- Diversification of applications, notably in autonomous systems, agriculture, and IoT.

- Technological advancements like multi-frequency and miniaturization fueling adoption.

- Increasing integration of GNSS with other sensor technologies for robust solutions.

- Strategic importance of GNSS as a critical enabler for automation and digitalization.

- Continuous investment in global satellite constellations and augmentation services.

GNSS Receiver Market Drivers Analysis

The GNSS receiver market is propelled by a confluence of powerful drivers, primarily stemming from the increasing global demand for precise positioning, navigation, and timing data across a broad spectrum of industries. The proliferation of autonomous systems, including self-driving vehicles, drones for delivery and surveillance, and robotic process automation in manufacturing, critically relies on highly accurate and reliable GNSS signals for their operational integrity and safety. These systems necessitate real-time, centimeter-level positioning, which advanced GNSS receivers are increasingly capable of providing, thus driving their widespread adoption.

Furthermore, the rapid expansion of the Internet of Things (IoT) and the subsequent demand for location-based services (LBS) in various consumer and industrial applications significantly contribute to market growth. From asset tracking and smart city infrastructure to wearable devices and personal navigation, the integration of GNSS modules enables a vast array of functionalities that enhance efficiency, safety, and user experience. This broad applicability, coupled with the miniaturization and cost-effectiveness of GNSS chipsets, makes the technology accessible for mass-market deployment, fostering innovation in new LBS offerings.

Government initiatives and significant investments in infrastructure development, particularly in emerging economies, also act as key market drivers. Projects related to smart cities, intelligent transportation systems, critical infrastructure monitoring, and advanced agricultural practices are increasingly incorporating GNSS technology for planning, execution, and ongoing management. Additionally, the modernization and expansion of global satellite navigation systems (e.g., GPS, GLONASS, Galileo, BeiDou) and the development of regional augmentation systems ensure enhanced signal availability and accuracy worldwide, bolstering confidence in GNSS as a primary source for critical positioning data.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Autonomous Systems (Vehicles, Drones, Robotics) | +2.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Demand for High-Precision Positioning (Agriculture, Construction, Surveying) | +2.0% | Global, particularly Asia Pacific, North America, Europe | Mid to Long-term (2025-2033) |

| Expansion of IoT and Location-Based Services | +1.8% | Global, especially urbanized regions | Mid-term (2025-2030) |

| Modernization and Development of Global and Regional GNSS Constellations | +1.5% | Global | Continuous |

GNSS Receiver Market Restraints Analysis

Despite robust growth, the GNSS receiver market faces several restraints that could potentially impede its full growth potential. One significant restraint is the vulnerability of GNSS signals to environmental factors and deliberate interference. Signals can be degraded or lost in urban canyons, dense forests, or during adverse weather conditions, leading to accuracy issues or complete outages. More critically, signals are susceptible to jamming (intentional disruption) and spoofing (imitation of genuine signals), posing substantial security risks, particularly for critical infrastructure, military applications, and autonomous systems where PNT integrity is paramount. These vulnerabilities necessitate costly mitigation strategies and can undermine user confidence, especially in sensitive applications.

The high cost associated with advanced, high-precision GNSS receivers and their integration into complex systems represents another notable restraint. While consumer-grade GNSS modules have become affordable, industrial and professional-grade receivers capable of centimeter-level accuracy still carry a significant price tag due to sophisticated hardware, advanced signal processing algorithms, and proprietary software. This cost can be prohibitive for small and medium-sized enterprises (SMEs) or for widespread deployment in low-margin applications, limiting market penetration in certain segments. Furthermore, the specialized expertise required for installation, calibration, and maintenance of these advanced systems adds to the overall operational expenses, creating a barrier to entry for some potential users.

Regulatory complexities and spectrum allocation challenges also pose restraints. Different regions and countries have varying regulations concerning GNSS signal use, data privacy, and the deployment of related infrastructure, which can complicate global market expansion for manufacturers and service providers. Additionally, the allocation of radio frequency spectrum for GNSS signals is a finite resource, and increasing demand from other wireless technologies can lead to spectrum congestion and potential interference issues. These regulatory and technical hurdles necessitate careful navigation and ongoing collaboration between industry stakeholders and regulatory bodies to ensure a stable operating environment for GNSS technology.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Vulnerability to Signal Jamming and Spoofing | -1.2% | Global, particularly high-security and critical infrastructure regions | Continuous |

| High Cost of High-Precision GNSS Receivers and Integration | -1.0% | Emerging markets, cost-sensitive applications | Mid-term (2025-2030) |

| Signal Obstruction in Challenging Environments (Urban Canyons, Indoors) | -0.8% | Urban areas globally | Continuous |

| Regulatory Complexities and Spectrum Allocation Challenges | -0.7% | Global, especially new markets | Long-term (2025-2033) |

GNSS Receiver Market Opportunities Analysis

The GNSS receiver market is ripe with opportunities driven by technological advancements and the emergence of new application domains. A significant opportunity lies in the development and deployment of next-generation satellite constellations, particularly Low Earth Orbit (LEO) constellations. Unlike traditional Medium Earth Orbit (MEO) GNSS systems, LEO satellites can offer stronger signals, lower latency, and potentially higher accuracy due to their proximity to Earth. This presents an opportunity for manufacturers to develop LEO-compatible receivers and for service providers to offer enhanced real-time kinematic (RTK) and precise point positioning (PPP) services, expanding the reach and reliability of high-accuracy PNT solutions to areas previously underserved.

The increasing convergence of GNSS technology with other complementary positioning technologies, such as Inertial Navigation Systems (INS), LiDAR, cameras, and 5G cellular networks, offers another substantial growth avenue. Hybrid positioning systems can overcome the inherent limitations of standalone GNSS, providing seamless and robust navigation in GNSS-denied or degraded environments, like tunnels, indoor spaces, or urban canyons. This integration fosters the creation of highly resilient and redundant PNT solutions critical for safety-of-life applications and fully autonomous systems. Manufacturers capable of developing sophisticated sensor fusion algorithms and integrated hardware solutions will capture significant market share in these advanced applications.

Furthermore, the rapid growth of emerging applications such as precision agriculture, smart infrastructure, and drone delivery services presents fertile ground for GNSS receiver innovation and adoption. Precision agriculture, for instance, leverages GNSS for automated steering, variable rate application, and yield mapping, leading to increased efficiency and reduced environmental impact. Smart infrastructure initiatives, including smart roads and utilities, rely on accurate positioning for monitoring and maintenance. The burgeoning drone industry, encompassing inspection, logistics, and mapping, demands lightweight, high-accuracy GNSS solutions. These diverse and expanding application areas promise sustained demand and open doors for specialized GNSS products and services tailored to their specific requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of LEO Satellite Constellations for Enhanced PNT | +2.0% | Global | Mid to Long-term (2027-2033) |

| Increased Adoption in Emerging Applications (Precision Agriculture, Drones, Smart Cities) | +1.8% | Global, particularly Asia Pacific, North America, Europe | Mid-term (2025-2030) |

| Integration with Other Positioning Technologies (INS, 5G, LiDAR) for Hybrid Systems | +1.5% | Global | Mid-term (2025-2030) |

| Development of Software-Defined GNSS and Cloud-Based Solutions | +1.2% | Global | Long-term (2028-2033) |

GNSS Receiver Market Challenges Impact Analysis

The GNSS receiver market faces several significant challenges that necessitate continuous innovation and strategic adaptation. One primary challenge is maintaining high accuracy and integrity in urban and indoor environments, commonly referred to as "urban canyons" and "indoor navigation." In these settings, GNSS signals are often obstructed, reflected (multi-path interference), or attenuated, leading to degraded positioning accuracy or complete signal loss. Addressing this requires sophisticated algorithms for multi-path mitigation, integration with alternative positioning technologies like Wi-Fi, UWB, or vision systems, and the development of robust filters, adding complexity and cost to receiver designs.

Another critical challenge is the persistent threat of GNSS signal jamming and spoofing, which can severely compromise the reliability and security of PNT solutions. Jamming, whether intentional or unintentional, disrupts signal reception, while spoofing involves broadcasting fake GNSS signals to deceive receivers into calculating an incorrect position or time. These threats are particularly concerning for critical infrastructure, defense, and autonomous applications where precise and trustworthy positioning is vital for operational safety and national security. Developing effective anti-jamming and anti-spoofing technologies, such as advanced signal authentication, cryptographic measures, and anomaly detection, remains a significant R&D focus and a competitive differentiator.

Furthermore, managing the increasing complexity of multi-constellation and multi-frequency GNSS signals presents a technical challenge for receiver manufacturers. While the availability of signals from multiple satellite systems (GPS, GLONASS, Galileo, BeiDou, QZSS, IRNSS) and across various frequencies (L1, L2, L5, E1, E5a, E5b, B1, B2, B3) enhances accuracy and availability, it also increases the computational burden and complexity of receiver design. Processing and combining these diverse signals efficiently, while maintaining low power consumption and small form factors, requires advanced chip design, sophisticated algorithms, and robust software, posing ongoing engineering hurdles for developers to overcome.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Accuracy in Challenging Environments (Urban Canyons, Indoors) | -1.5% | Global, particularly densely populated areas | Continuous |

| Mitigation of Signal Jamming and Spoofing Threats | -1.3% | Global, particularly security-sensitive sectors | Continuous |

| Management of Multi-Constellation/Multi-Frequency Signal Complexity | -1.0% | Global (technical challenge for manufacturers) | Continuous |

| Ensuring Cybersecurity of GNSS Receivers and Data | -0.9% | Global | Long-term (2025-2033) |

GNSS Receiver Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global GNSS receiver market, offering detailed insights into market size, growth trends, drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of various segments based on type, application, component, and end-use, providing a granular view of market dynamics across key geographical regions. It incorporates the latest technological advancements, including the impact of Artificial Intelligence and the evolution of satellite constellations, to deliver a forward-looking perspective on the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 10.5 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Trimble Inc., Hexagon AB (NovAtel, Leica Geosystems), Topcon Corporation, Garmin Ltd., U-blox AG, Qualcomm Technologies, Inc., Septentrio N.V., Furuno Electric Co., Ltd., JAVAD GNSS Inc., Hemisphere GNSS, Inc., Rockwell Collins (now Collins Aerospace), Broadcom Inc., Sierra Wireless, Inc., NavCom Technology Inc., Geneq Inc., ComNav Technology Ltd., NMEA (National Marine Electronics Association), SparkFun Electronics, Adafruit Industries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global GNSS receiver market is meticulously segmented to provide a granular understanding of its diverse landscape, reflecting variations in technological capabilities, applications, and end-user requirements. This segmentation allows for precise market analysis, identifying key growth areas and niche opportunities across different dimensions. Understanding these segments is crucial for stakeholders to tailor products, strategies, and investments effectively, addressing the specific needs of various market verticals and user groups.

- By Type:

- Single Frequency: Cost-effective, suitable for basic positioning tasks.

- Dual Frequency: Enhanced accuracy and reduced atmospheric error, common in professional applications.

- Multi-Frequency: Highest accuracy, robustness, and performance in challenging environments, essential for high-precision and safety-critical applications.

- By Component:

- Antennas: Crucial for signal reception, varying in type (patch, helix, choke ring) and performance.

- Receivers/Modules: The core processing unit, ranging from low-cost chips to high-performance boards.

- Processors: Handle complex signal processing and data calculations.

- Cables: Connect various components within the GNSS system.

- Software: Firmware, application software for data processing, analysis, and visualization.

- By Application:

- Mapping and GIS: For spatial data collection and management.

- Surveying: High-precision measurements for land, construction, and infrastructure.

- Agriculture: Precision farming, automated machinery guidance, yield mapping.

- Construction: Site preparation, machine control, asset tracking.

- Mining: Autonomous mining equipment, resource management.

- Automotive: Navigation, ADAS (Advanced Driver-Assistance Systems), autonomous driving.

- Marine: Navigation, charting, port operations, offshore exploration.

- Aviation: Aircraft navigation, air traffic management.

- Defense and Aerospace: Military applications, missile guidance, reconnaissance.

- Consumer Electronics: Smartphones, wearables, personal navigation devices.

- Location-Based Services (LBS): Mobile apps, geo-fencing, asset tracking.

- Timing and Synchronization: Critical for telecommunications, power grids, financial markets.

- By Industry Vertical:

- Transportation & Logistics: Fleet management, asset tracking, autonomous vehicles.

- Industrial: Construction, mining, agriculture, smart manufacturing.

- Consumer & Commercial: Smartphones, wearables, recreational devices, retail.

- Aerospace & Defense: Military operations, aerospace navigation, surveillance.

- Marine: Commercial shipping, leisure boating, offshore activities.

- Others: Utilities, public safety, environmental monitoring.

Regional Highlights

- North America: This region is a leading market for GNSS receivers, driven by significant investments in R&D, early adoption of advanced technologies, and a robust presence of key market players. The demand is particularly high in autonomous vehicle development, precision agriculture, and surveying sectors. Government initiatives related to infrastructure modernization and defense also contribute substantially to market growth.

- Europe: Europe demonstrates strong growth, fueled by stringent regulatory frameworks promoting safety and efficiency in sectors like automotive and aviation, coupled with significant adoption in precision farming and smart city initiatives. The Galileo satellite system, developed by the European Union, provides a crucial impetus for the region's GNSS market, ensuring independent and highly accurate positioning capabilities.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily due to rapid industrialization, extensive infrastructure development projects, and increasing demand from the automotive and consumer electronics sectors in countries like China, India, and Japan. The widespread adoption of smartphones and the rapid expansion of 5G networks further bolster the demand for GNSS-enabled devices and location-based services.

- Latin America: This region shows steady growth, largely driven by the increasing adoption of precision agriculture techniques to enhance crop yields and optimize resource utilization. Additionally, the expansion of logistics and transportation sectors, along with ongoing infrastructure projects, contributes to the demand for GNSS receivers for fleet management and construction applications.

- Middle East and Africa (MEA): The MEA region is witnessing growth spurred by large-scale construction projects, investments in smart city development, and the growing need for efficient resource management in industries such as oil and gas, and mining. Increased defense spending and the deployment of advanced surveillance systems also contribute to the adoption of GNSS technology in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the GNSS Receiver Market.- Trimble Inc.

- Hexagon AB (NovAtel, Leica Geosystems)

- Topcon Corporation

- Garmin Ltd.

- U-blox AG

- Qualcomm Technologies, Inc.

- Septentrio N.V.

- Furuno Electric Co., Ltd.

- JAVAD GNSS Inc.

- Hemisphere GNSS, Inc.

- Rockwell Collins (now Collins Aerospace)

- Broadcom Inc.

- Sierra Wireless, Inc.

- NavCom Technology Inc.

- Geneq Inc.

- ComNav Technology Ltd.

- NMEA (National Marine Electronics Association)

- SparkFun Electronics

- Adafruit Industries

Frequently Asked Questions

What is a GNSS receiver?

A GNSS receiver is an electronic device that receives signals from global navigation satellite systems (GNSS) constellations, such as GPS (USA), GLONASS (Russia), Galileo (Europe), and BeiDou (China). It uses these signals to calculate its precise position, velocity, and time anywhere on Earth or in Earth orbit, enabling navigation, timing, and mapping applications.

How does a GNSS receiver work?

A GNSS receiver works by acquiring signals transmitted by multiple satellites. Each satellite broadcasts its precise orbit information and the exact time its signal was sent. The receiver measures the time difference between receiving signals from several satellites, calculates the distance to each, and then triangulates its own position on Earth. For enhanced accuracy, it often corrects for atmospheric delays and other errors.

What are the primary applications of GNSS receivers?

GNSS receivers are vital for a wide range of applications including navigation (automotive, marine, aviation, personal), surveying and mapping (GIS data collection, land surveying), agriculture (precision farming, automated machinery), construction (machine control, site preparation), defense (guidance systems, reconnaissance), and timing/synchronization for critical infrastructure like telecommunications and financial networks.

What is the difference between GPS and GNSS?

GPS (Global Positioning System) is a specific global navigation satellite system operated by the United States. GNSS (Global Navigation Satellite System) is a broader, overarching term that refers to all global satellite navigation systems, including GPS, GLONASS, Galileo, and BeiDou. Therefore, GPS is a component of GNSS, and a GNSS receiver is designed to work with multiple satellite constellations for improved accuracy and reliability.

What are the future trends impacting the GNSS receiver market?

Key future trends include the increasing adoption of multi-constellation and multi-frequency receivers, the integration of Artificial Intelligence for enhanced signal processing and sensor fusion, the miniaturization and cost reduction of modules for IoT integration, the emergence of LEO satellite constellations for improved signal strength, and the growing demand from autonomous systems and precision applications requiring centimeter-level accuracy.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted