GNSS and GPS Antenna Market

GNSS and GPS Antenna Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709996 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

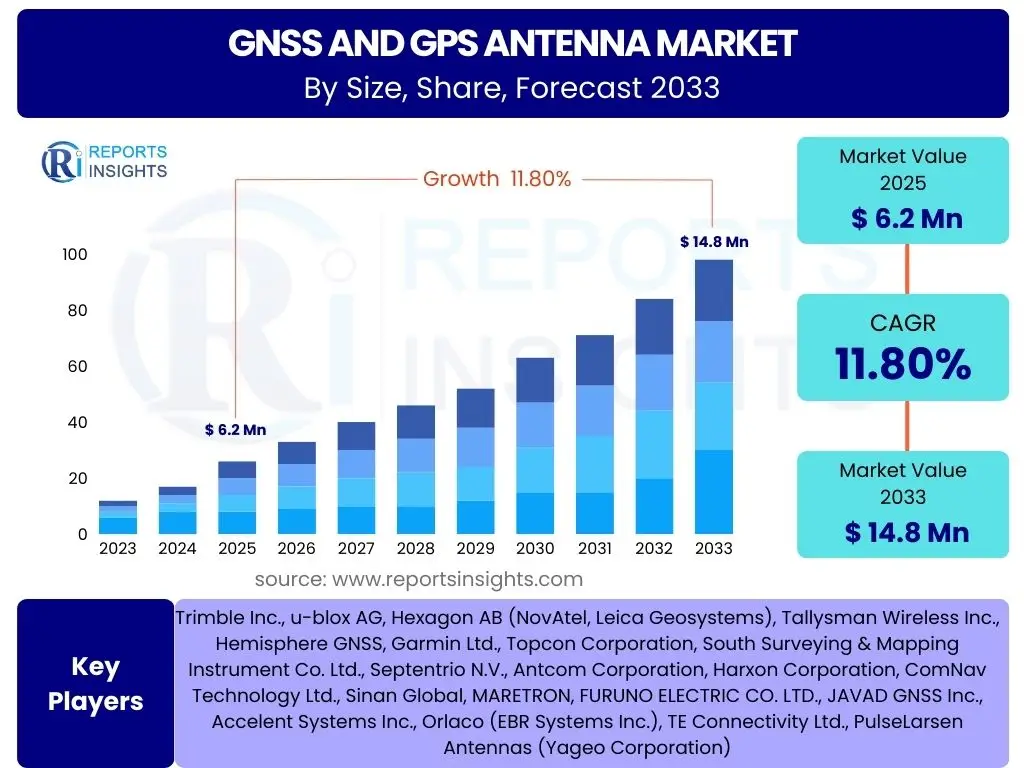

GNSS and GPS Antenna Market Size

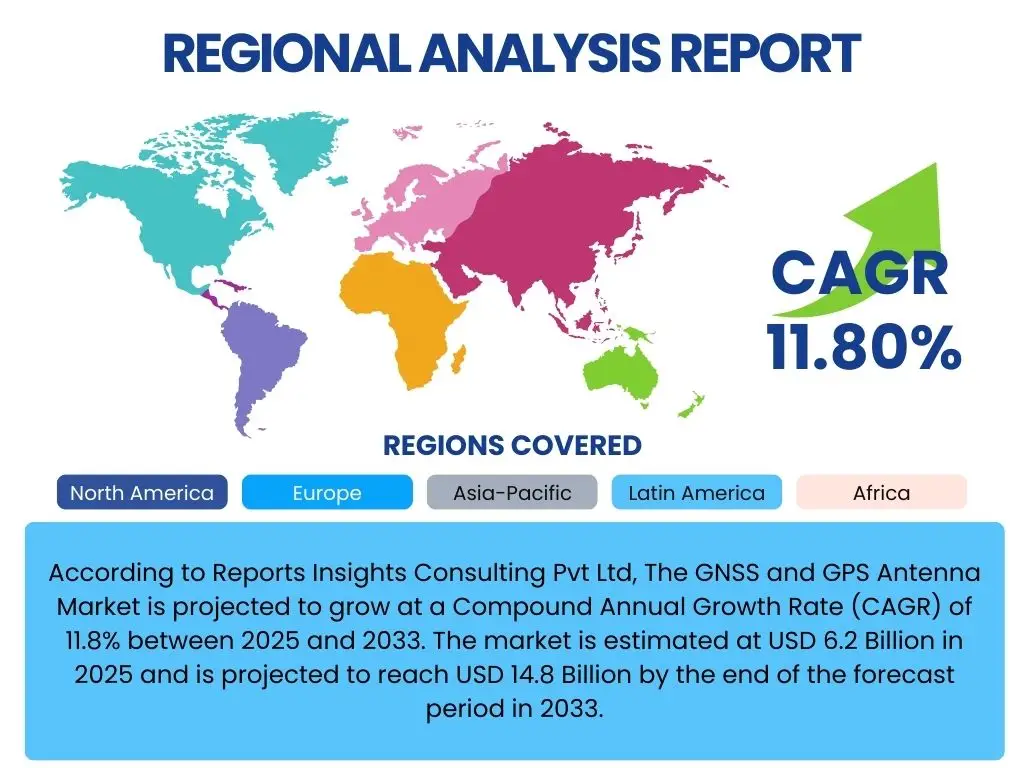

According to Reports Insights Consulting Pvt Ltd, The GNSS and GPS Antenna Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 14.8 Billion by the end of the forecast period in 2033.

Key GNSS and GPS Antenna Market Trends & Insights

User queries frequently highlight an increasing demand for enhanced accuracy, reliability, and miniaturization within the GNSS and GPS antenna market. There is significant interest in understanding how technological advancements, particularly multi-constellation and multi-frequency support, are shaping the industry. Furthermore, the integration of these antennas into new and emerging applications, such as autonomous systems and advanced IoT devices, represents a core area of inquiry, alongside the continuous evolution towards more robust and interference-resistant solutions. These trends collectively underscore a market driven by the need for superior positioning, navigation, and timing (PNT) capabilities across a diverse range of sectors.

- Proliferation of multi-constellation and multi-frequency antennas for improved accuracy and reliability.

- Growing adoption of high-precision GNSS antennas in autonomous vehicles and robotics.

- Miniaturization and integration of antennas into compact IoT devices and wearables.

- Increased demand for robust anti-jamming and anti-spoofing capabilities in critical applications.

- Emergence of smart antennas with integrated processing and communication capabilities.

AI Impact Analysis on GNSS and GPS Antenna

Common user questions regarding AI's impact on GNSS and GPS antennas often revolve around how artificial intelligence can enhance signal processing, mitigate interference, and improve overall positioning accuracy. Users are keen to understand AI's role in predictive maintenance for antenna systems, its potential in advanced data fusion from multiple sensor inputs, and its contribution to the development of more intelligent and adaptive antenna designs. The general expectation is that AI will unlock new levels of performance and resilience for GNSS and GPS solutions, addressing long-standing challenges in signal integrity and environmental robustness, ultimately leading to more sophisticated and reliable navigation and timing systems.

- Enhanced signal processing and noise reduction for improved accuracy in challenging environments.

- Development of adaptive beamforming and nulling techniques to counter interference and jamming.

- Predictive analytics for antenna performance, enabling proactive maintenance and system optimization.

- Advanced sensor fusion algorithms, combining GNSS data with IMUs, cameras, and lidar for robust positioning.

- Real-time anomaly detection and health monitoring of antenna systems, increasing operational reliability.

Key Takeaways GNSS and GPS Antenna Market Size & Forecast

Analysis of user inquiries indicates a strong interest in the overall growth trajectory and the underlying factors contributing to the GNSS and GPS antenna market's expansion. Key takeaways reveal that the market is experiencing robust growth driven by technological advancements and the proliferation of location-based services across various industries. The forecast suggests a sustained upward trend, underpinned by the increasing integration of high-precision positioning in emerging applications. Stakeholders are particularly interested in understanding the long-term potential for market expansion and the strategic implications of evolving market dynamics, emphasizing the critical role these antennas play in modern infrastructure and next-generation technologies.

- Significant market expansion anticipated, primarily fueled by demand from autonomous systems and IoT.

- Technological innovation, particularly in multi-constellation and multi-frequency capabilities, will drive adoption.

- Growing need for highly accurate and reliable positioning, navigation, and timing (PNT) solutions globally.

- Key regions like Asia Pacific and North America are expected to lead market growth due to industrial and consumer demand.

- Increased investment in satellite infrastructure and advanced antenna research underpins long-term market vitality.

GNSS and GPS Antenna Market Drivers Analysis

The GNSS and GPS antenna market is significantly propelled by the escalating demand for precise positioning, navigation, and timing (PNT) data across diverse sectors. The widespread adoption of location-based services (LBS) in consumer electronics, coupled with the rapid expansion of the Internet of Things (IoT) ecosystem, inherently requires robust and accurate GNSS capabilities. Furthermore, the burgeoning market for autonomous vehicles, drones, and robotics heavily relies on high-fidelity GNSS antennas for safe and efficient operation. These factors collectively create a strong upward trajectory for the market, as industries increasingly integrate sophisticated positioning solutions into their operational frameworks to enhance efficiency, safety, and reliability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Location-Based Services (LBS) | +3.5% | Global, particularly Asia Pacific (Consumer Electronics) | Short to Mid-term (2025-2029) |

| Growth of IoT and Connected Devices | +3.0% | North America, Europe, Asia Pacific (Industrial IoT) | Mid to Long-term (2027-2033) |

| Rise in Autonomous Vehicles and Robotics | +4.0% | North America, Europe, China, Japan | Mid to Long-term (2028-2033) |

| Adoption in Agriculture and Construction | +2.5% | North America, Europe, Latin America (Precision Agriculture) | Short to Mid-term (2025-2030) |

| Expansion of GNSS Constellations and Multi-Frequency Support | +2.8% | Global | Short to Mid-term (2025-2031) |

GNSS and GPS Antenna Market Restraints Analysis

Despite robust growth, the GNSS and GPS antenna market faces several significant restraints that could temper its expansion. High initial investment costs for advanced, high-precision antenna systems, particularly for smaller enterprises, can hinder widespread adoption. Furthermore, the susceptibility of GNSS signals to interference, jamming, and spoofing remains a critical concern, impacting performance and reliability in challenging environments. Regulatory complexities and varying spectrum allocation policies across different regions also pose a challenge, leading to fragmentation and potential delays in market entry for new technologies. Addressing these factors is crucial for ensuring sustained market development and broader integration of GNSS antenna solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced GNSS Antennas | -1.8% | Developing Regions, Small & Medium Enterprises (SMEs) | Short to Mid-term (2025-2028) |

| Signal Interference, Jamming, and Spoofing Vulnerabilities | -2.2% | Global (Defense, Critical Infrastructure) | Continuous |

| Regulatory Hurdles and Spectrum Allocation Issues | -1.5% | Europe, Asia Pacific (Varying National Regulations) | Mid-term (2026-2030) |

| Cybersecurity Concerns and Data Privacy Risks | -1.0% | Global (Enterprise, Government) | Mid to Long-term (2027-2033) |

| Limited Accuracy in Urban Canyons and Indoor Environments | -0.9% | Dense Urban Areas, Indoor Locations (Global) | Short to Mid-term (2025-2029) |

GNSS and GPS Antenna Market Opportunities Analysis

Significant opportunities exist within the GNSS and GPS antenna market, driven by evolving technological landscapes and expanding application areas. The increasing integration of 5G networks presents a synergistic opportunity for enhanced positioning capabilities, enabling ultra-reliable low-latency communication (URLLC) for precise PNT data transmission. Furthermore, the rapidly growing drone and UAV market, spanning commercial and defense applications, creates a substantial demand for lightweight, high-performance GNSS antennas. Advancements in precision agriculture and smart city initiatives also offer fertile ground for market penetration, as these sectors increasingly rely on highly accurate geospatial data. These emerging domains represent key avenues for innovation and market expansion for antenna manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with 5G Technology and IoT Ecosystems | +3.2% | Global, particularly advanced economies | Mid to Long-term (2027-2033) |

| Expansion of the Drone and UAV Market | +2.9% | North America, Europe, Asia Pacific (Commercial & Defense) | Short to Mid-term (2025-2030) |

| Advancements in Precision Agriculture | +2.5% | North America, Europe, Latin America | Short to Mid-term (2025-2029) |

| Smart City Development and Infrastructure Monitoring | +2.0% | Asia Pacific, Europe, Middle East | Mid to Long-term (2028-2033) |

| Development of Robust Anti-Jamming and Anti-Spoofing Solutions | +1.8% | Global (Defense, Critical Infrastructure) | Continuous |

GNSS and GPS Antenna Market Challenges Impact Analysis

The GNSS and GPS antenna market encounters several critical challenges that demand strategic responses from industry players. The rapid pace of technological innovation, while a driver, also presents the challenge of rapid obsolescence for existing products, requiring continuous R&D investment. Moreover, the increasing complexity of multi-constellation and multi-frequency antenna designs necessitates specialized expertise, potentially leading to a shortage of skilled professionals. Global supply chain disruptions, exacerbated by geopolitical tensions and pandemics, can significantly impact manufacturing and delivery timelines. Addressing these complexities through robust innovation, talent development, and diversified supply chains is essential for navigating the evolving market landscape and maintaining competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -1.5% | Global (High-tech Manufacturing Regions) | Continuous |

| Intellectual Property (IP) Infringement and Counterfeit Products | -0.8% | Asia Pacific, Emerging Markets | Continuous |

| Environmental Factors Affecting Antenna Performance (e.g., weather) | -0.7% | Global (Extreme Weather Zones) | Continuous |

| Shortage of Skilled Workforce in GNSS Technology | -1.2% | North America, Europe (R&D, Manufacturing) | Mid to Long-term (2027-2033) |

| Global Supply Chain Disruptions and Component Shortages | -1.0% | Global (Electronics Manufacturing Hubs) | Short to Mid-term (2025-2028) |

GNSS and GPS Antenna Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global GNSS and GPS Antenna Market, covering historical data, current market conditions, and future projections. The scope encompasses detailed segmentation by type, frequency band, constellation, application, and end-use industry, offering a granular view of market dynamics. It further provides a thorough regional analysis, identifying key growth opportunities and challenges across major geographical markets. The report aims to furnish stakeholders with critical insights into market size, growth drivers, restraints, opportunities, and the competitive landscape to inform strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 14.8 Billion |

| Growth Rate | 11.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Trimble Inc., u-blox AG, Hexagon AB (NovAtel, Leica Geosystems), Tallysman Wireless Inc., Hemisphere GNSS, Garmin Ltd., Topcon Corporation, South Surveying & Mapping Instrument Co. Ltd., Septentrio N.V., Antcom Corporation, Harxon Corporation, ComNav Technology Ltd., Sinan Global, MARETRON, FURUNO ELECTRIC CO. LTD., JAVAD GNSS Inc., Accelent Systems Inc., Orlaco (EBR Systems Inc.), TE Connectivity Ltd., PulseLarsen Antennas (Yageo Corporation) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The GNSS and GPS Antenna market is extensively segmented to provide a granular understanding of its diverse components and evolving landscape. This segmentation allows for precise analysis of market dynamics across various technological specifications, functional applications, and end-user industries. By breaking down the market into these distinct categories, the report facilitates targeted strategic planning and identifies niche opportunities for stakeholders. Understanding these segments is crucial for manufacturers to tailor product development, for service providers to identify specific market needs, and for investors to pinpoint high-growth areas within the complex PNT ecosystem.

- By Type: Patch Antenna, Helical Antenna, Quadrifilar Helix Antenna, Dipole Antenna, Array Antenna, Smart Antenna, Others. This segmentation highlights the various physical configurations and design principles employed, with patch antennas being common for compact devices and array antennas offering advanced signal processing.

- By Frequency Band: L1 Band, L2 Band, L5 Band, L-band, Dual-band, Multi-band. This categorizes antennas based on the specific frequencies they support, which directly impacts accuracy, robustness, and the ability to leverage multiple GNSS constellations.

- By Constellation: GPS, GLONASS, Galileo, BeiDou, QZSS, IRNSS/NavIC, Others. This segment details compatibility with global and regional navigation satellite systems, crucial for multi-GNSS receivers seeking enhanced coverage and accuracy.

- By Application: Automotive, Consumer Electronics, Marine, Aviation, Agriculture, Construction, Mining, Surveying & Mapping, Defense, Energy & Utilities, Environmental Monitoring, Geospatial. This covers the wide array of industries and specific uses cases where GNSS and GPS antennas are deployed, from navigation to precision operations.

- By End-Use Industry: Commercial, Government, Defense. This distinguishes between the primary sectors utilizing GNSS antenna technology, often with differing requirements for security, ruggedness, and regulatory compliance.

Regional Highlights

- North America: This region is a significant market for GNSS and GPS antennas, driven by substantial investments in autonomous vehicle research, defense applications, and the widespread adoption of precision agriculture. The presence of key technology developers and a mature industrial base further contributes to its market leadership, particularly in high-precision and robust solutions.

- Europe: Characterized by strong growth in industrial automation, smart city initiatives, and the development of the Galileo constellation, Europe presents a robust market. Demand for GNSS antennas is high in sectors like construction, maritime, and aerospace, alongside a strong focus on regulatory compliance and advanced urban mobility solutions.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, APAC is propelled by the rapid expansion of consumer electronics, automotive manufacturing, and significant government investments in infrastructure development (e.g., smart cities, 5G networks). Countries like China, India, and Japan are major contributors, with increasing demand for affordable and multi-constellation compatible antennas.

- Latin America: This region shows promising growth, especially in precision agriculture, mining, and logistics. The adoption of GNSS technology for fleet management and resource optimization is increasing, though market penetration is still developing compared to more mature economies.

- Middle East and Africa (MEA): Growth in MEA is largely influenced by government-led infrastructure projects, defense spending, and emerging applications in oil & gas, mining, and smart city developments. The need for robust navigation solutions in challenging environments drives demand for high-performance antennas.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the GNSS and GPS Antenna Market.- Trimble Inc.

- u-blox AG

- Hexagon AB (NovAtel, Leica Geosystems)

- Tallysman Wireless Inc.

- Hemisphere GNSS

- Garmin Ltd.

- Topcon Corporation

- South Surveying & Mapping Instrument Co. Ltd.

- Septentrio N.V.

- Antcom Corporation

- Harxon Corporation

- ComNav Technology Ltd.

- Sinan Global

- MARETRON

- FURUNO ELECTRIC CO. LTD.

- JAVAD GNSS Inc.

- Accelent Systems Inc.

- Orlaco (EBR Systems Inc.)

- TE Connectivity Ltd.

- PulseLarsen Antennas (Yageo Corporation)

Frequently Asked Questions

What is the current market size of the GNSS and GPS Antenna Market?

The GNSS and GPS Antenna Market is estimated at USD 6.2 Billion in 2025. This market value reflects the current demand and adoption rates across various applications globally.

What is the projected growth rate for the GNSS and GPS Antenna Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033, indicating robust expansion driven by technological advancements and increasing applications.

Which factors are primarily driving the growth of the GNSS and GPS Antenna Market?

Key drivers include the rising demand for location-based services, the proliferation of IoT and connected devices, the growth of autonomous vehicles and robotics, and increasing adoption in precision agriculture and construction industries.

How is AI impacting the GNSS and GPS Antenna Market?

AI is significantly impacting the market by enhancing signal processing, improving interference mitigation, enabling advanced sensor fusion, and supporting predictive maintenance for antenna systems, leading to more robust and accurate positioning solutions.

Which regions are leading the market in terms of revenue contribution?

North America and Europe currently hold substantial market shares due to high adoption in defense and industrial applications. However, the Asia Pacific region is expected to demonstrate the highest growth, driven by expanding consumer electronics and automotive sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted