Glass Bottle and Glass Packaging Market

Glass Bottle and Glass Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700784 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

Glass Bottle and Glass Packaging Market Size

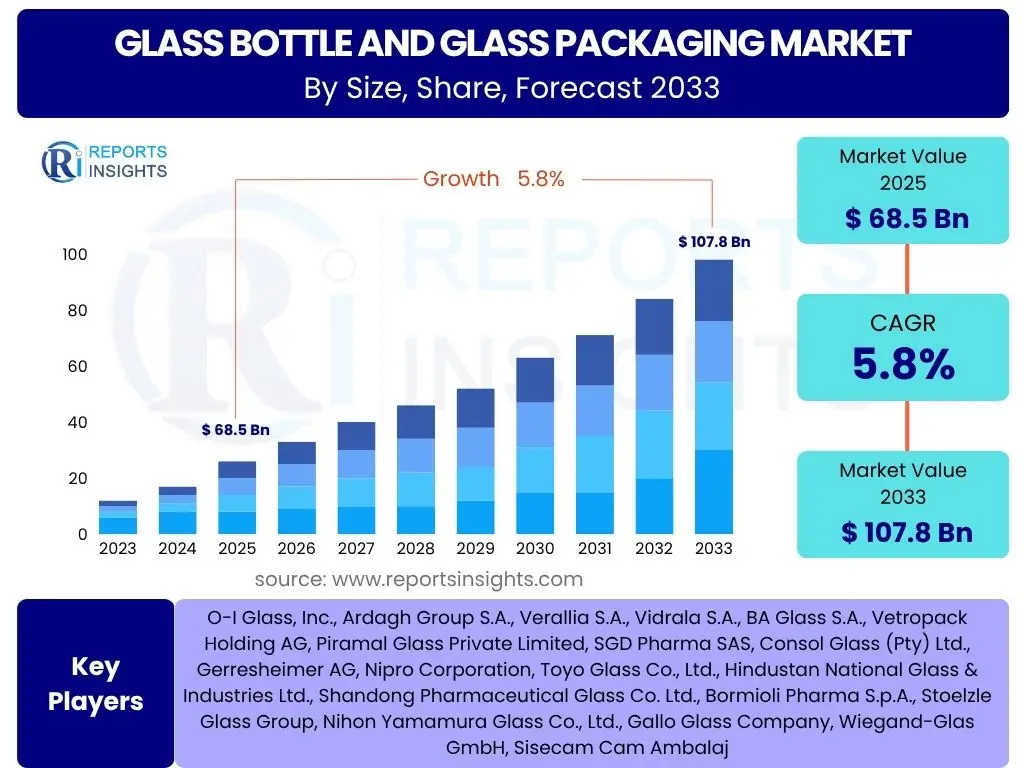

According to Reports Insights Consulting Pvt Ltd, The Glass Bottle and Glass Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 68.5 Billion in 2025 and is projected to reach USD 107.8 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by the inherent advantages of glass as a packaging material, including its inert nature, premium aesthetic, and infinite recyclability. Consumers globally are increasingly seeking sustainable and safe packaging solutions, a demand that glass perfectly addresses, contributing significantly to its market expansion across various end-use industries.

The resilience of the glass packaging market is also bolstered by its widespread adoption in critical sectors such as food and beverages, pharmaceuticals, and personal care. In the beverage industry, glass bottles are preferred for alcoholic beverages due to their ability to preserve flavor and quality, and for premium non-alcoholic drinks for their perceived elegance and health safety. The pharmaceutical sector relies on glass for its barrier properties and chemical inertness, crucial for drug integrity. These fundamental demands, coupled with continuous innovation in glass manufacturing processes, ensure a stable and expanding market for glass packaging solutions over the forecast period.

Key Glass Bottle and Glass Packaging Market Trends & Insights

Common user questions about trends in the Glass Bottle and Glass Packaging market frequently revolve around sustainability, product innovation, and the impact of evolving consumer preferences. Users are keen to understand how the industry is adapting to environmental pressures, what new technologies are emerging, and how global shifts in demand for certain products are shaping packaging choices. These queries highlight a market that is dynamic, responding to both regulatory changes and heightened environmental consciousness among consumers and businesses alike.

The insights derived from these questions reveal a strong emphasis on circular economy principles, lightweighting, and aesthetic appeal. Manufacturers are investing in advanced recycling technologies and increasing the use of recycled content (cullet) to reduce their carbon footprint. Concurrently, there is a push towards creating lighter yet durable glass bottles to lower transportation costs and environmental impact, without compromising on product safety or brand image. The premiumization trend, especially in alcoholic beverages and cosmetics, also drives demand for unique designs and customizable packaging, positioning glass as a preferred material for its versatility and perceived quality.

- Growing demand for sustainable and recyclable packaging solutions.

- Increased adoption of lightweight glass bottles to reduce carbon footprint and logistics costs.

- Rising consumer preference for premium and aesthetically appealing glass packaging.

- Innovation in glass manufacturing processes, including advanced recycling and digital printing.

- Expansion of e-commerce channels driving demand for robust and secure glass packaging.

- Shift towards smaller, single-serve glass packaging formats in certain beverage categories.

AI Impact Analysis on Glass Bottle and Glass Packaging

Common user questions related to the impact of AI on the Glass Bottle and Glass Packaging sector often center on operational efficiency, quality control, and supply chain optimization. Users are curious about how artificial intelligence can streamline production processes, enhance product integrity, and provide predictive insights into market demands or potential disruptions. There is a clear expectation that AI will bring about transformative changes, addressing long-standing challenges in manufacturing and logistics.

Based on this analysis, the key themes include the automation of complex tasks, predictive analytics for maintenance and demand forecasting, and sophisticated quality inspection systems. Users anticipate that AI will lead to significant cost reductions through optimized resource utilization and reduced waste. Furthermore, AI's ability to process vast amounts of data will facilitate more agile supply chain management and support innovative product development, allowing manufacturers to respond rapidly to market shifts and consumer trends. The integration of AI is viewed as a critical step towards creating more efficient, sustainable, and responsive glass packaging operations.

- Enhanced quality control through AI-powered visual inspection systems, reducing defects.

- Optimized production lines and predictive maintenance of machinery, minimizing downtime.

- Improved supply chain management and logistics efficiency through AI-driven demand forecasting and route optimization.

- Automated design and prototyping, accelerating new product development cycles.

- Data analytics for market insights and personalized packaging solutions.

- Energy consumption optimization in glass furnaces using AI algorithms, leading to reduced operational costs.

Key Takeaways Glass Bottle and Glass Packaging Market Size & Forecast

Common user questions about key takeaways from the Glass Bottle and Glass Packaging market size and forecast often focus on understanding the primary growth drivers, the significance of sustainability, and the implications for both established players and new entrants. Users are interested in deciphering what factors will most significantly influence market expansion and how environmental considerations are shaping industry strategies. These queries indicate a desire for actionable insights that inform business decisions and strategic planning within the sector.

The insights reveal that the market is poised for steady growth, underpinned by fundamental consumer demands and a strong push towards eco-friendly solutions. The infinite recyclability of glass positions it favorably against alternative materials, driving adoption in environmentally conscious markets. Furthermore, the market's expansion is not uniform across all regions, with emerging economies contributing significantly to overall volume growth, while developed markets focus on premiumization and advanced recycling. This duality suggests a multifaceted approach is necessary for market participants to capitalize on diverse opportunities and navigate evolving competitive landscapes effectively.

- The market demonstrates robust growth, driven by intrinsic properties of glass and consumer demand for sustainable packaging.

- Sustainability, particularly the high recyclability of glass, is a paramount driver influencing purchasing decisions and industry investments.

- Asia Pacific is expected to remain a key growth engine, propelled by expanding consumption in food, beverages, and pharmaceuticals.

- Technological advancements in manufacturing and increased adoption of recycled content (cullet) are crucial for market competitiveness and environmental performance.

- The premiumization trend continues to favor glass packaging, offering opportunities for specialized and high-value products.

Glass Bottle and Glass Packaging Market Drivers Analysis

The glass bottle and glass packaging market is significantly driven by a confluence of factors, foremost among them being the increasing consumer preference for sustainable and recyclable packaging materials. As environmental awareness intensifies globally, both consumers and regulatory bodies are advocating for packaging solutions with minimal environmental impact. Glass, being infinitely recyclable without loss of quality, aligns perfectly with these sustainability goals, making it a preferred choice for brands aiming to enhance their eco-credentials. This inherent recyclability not only appeals to environmentally conscious consumers but also supports circular economy initiatives, providing a long-term growth impetus for the market.

Furthermore, the escalating demand from key end-use industries, particularly the food and beverage sector, continues to be a primary growth catalyst. Glass is highly valued in these industries for its inertness, which ensures product purity, extends shelf life, and preserves taste without leaching chemicals. The premiumization trend across alcoholic beverages, gourmet foods, and high-end cosmetics also fuels the demand for glass packaging, as it conveys a sense of quality, luxury, and authenticity. Additionally, the rapid expansion of the pharmaceutical industry globally, driven by an aging population and increasing healthcare expenditure, reinforces the demand for glass vials and bottles due to their superior barrier properties and safety for sensitive medications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Consumer Preference for Sustainable Packaging | +1.2% | Global, particularly Europe & North America | Long-term (2025-2033) |

| Growing Demand from Food & Beverage Industry (esp. Alcoholic & Premium) | +1.0% | Global, strong in Asia Pacific & Latin America | Medium-to-Long-term (2025-2033) |

| Expansion of Pharmaceutical Sector | +0.8% | Global | Long-term (2025-2033) |

| Premiumization and Brand Image Enhancement | +0.7% | Developed Economies (Europe, North America, Japan) | Medium-term (2025-2030) |

| Innovations in Lightweighting & Design | +0.6% | Global | Short-to-Medium-term (2025-2028) |

Glass Bottle and Glass Packaging Market Restraints Analysis

Despite its numerous advantages, the glass bottle and glass packaging market faces significant restraints that can impede its growth trajectory. One primary challenge is the intense competition from alternative packaging materials, such as plastics, metals, and flexible packaging. Plastics, in particular, offer superior lightweight properties, cost-effectiveness, and ease of transport, making them attractive to manufacturers seeking to reduce logistics expenses and overall production costs. While environmental concerns are pushing consumers away from single-use plastics, innovations in recycled plastics and biodegradable polymers continue to pose a competitive threat, forcing glass manufacturers to constantly innovate and justify the higher cost of glass.

Another substantial restraint is the high energy consumption inherent in glass manufacturing. The process of melting raw materials requires extremely high temperatures, leading to significant energy costs and a considerable carbon footprint. This makes glass production sensitive to volatile energy prices and increasing carbon taxes, which can erode profit margins and make glass a less attractive option for cost-sensitive applications. Furthermore, the relatively higher weight and fragility of glass compared to other materials lead to increased transportation costs and a higher risk of breakage during transit, adding to the overall supply chain expenses and logistical complexities for companies utilizing glass packaging.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Alternative Packaging Materials | -0.8% | Global | Long-term (2025-2033) |

| High Energy Consumption in Manufacturing | -0.7% | Global, particularly Europe (due to energy costs) | Ongoing (2025-2033) |

| High Capital Investment for New Facilities | -0.5% | Global | Long-term (2025-2033) |

| Fragility and Higher Transportation Costs | -0.4% | Global | Ongoing (2025-2033) |

Glass Bottle and Glass Packaging Market Opportunities Analysis

The glass bottle and glass packaging market presents several compelling opportunities for growth and innovation. One significant opportunity lies in the burgeoning demand for premium and customized packaging solutions. As consumer preferences shift towards unique product experiences and brand differentiation becomes paramount, manufacturers are increasingly seeking distinctive packaging that reflects quality and exclusivity. Glass, with its superior aesthetic appeal, versatility in shaping, and ability to accept various decorative techniques (like embossing, debossing, and direct printing), is ideally positioned to meet this demand, particularly in the spirits, wine, perfumes, and high-end cosmetic sectors. This trend allows for higher price points and strengthens brand loyalty.

Another substantial opportunity emerges from the rapid growth of e-commerce across various industries. While glass packaging historically faced challenges in online retail due to breakage concerns, advancements in protective packaging and logistics solutions are mitigating these risks. The perceived premiumness and sustainability of glass make it attractive for consumers receiving products via e-commerce, creating a growing niche. Furthermore, expanding markets in developing economies, particularly in Asia Pacific and Latin America, offer immense potential. Rising disposable incomes, urbanization, and changing lifestyles in these regions are driving increased consumption of packaged food and beverages, pharmaceuticals, and personal care products, creating a fertile ground for glass packaging market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Economies (Asia Pacific, Latin America) | +1.0% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Rising Demand for Premium & Customized Packaging | +0.9% | Global, strong in developed markets | Medium-to-Long-term (2025-2033) |

| Technological Advancements (e.g., lightweighting, smart glass) | +0.8% | Global | Medium-term (2025-2030) |

| Expansion in Healthcare & Pharmaceutical Sector | +0.7% | Global | Long-term (2025-2033) |

Glass Bottle and Glass Packaging Market Challenges Impact Analysis

The glass bottle and glass packaging market contends with several significant challenges that require strategic responses from manufacturers. One of the primary hurdles is the volatility in raw material prices, particularly for soda ash, sand, and cullet. These materials are essential for glass production, and their price fluctuations can directly impact manufacturing costs and profit margins. Geopolitical factors, supply chain disruptions, and global demand dynamics for these commodities can lead to unpredictable pricing, making long-term cost planning difficult for glass producers and potentially hindering investment in capacity expansion or technological upgrades.

Another critical challenge is the increasingly stringent environmental regulations and waste management policies globally. While glass is highly recyclable, the collection, sorting, and processing of cullet for reuse require robust infrastructure, which is not uniformly developed across all regions. Moreover, the energy-intensive nature of glass manufacturing exposes the industry to growing pressures related to carbon emissions and air pollution. Compliance with evolving environmental standards, investment in cleaner production technologies, and the need to improve recycling rates pose significant operational and financial burdens on glass packaging manufacturers, impacting their competitiveness and market agility.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.7% | Global | Ongoing (2025-2033) |

| Stringent Environmental Regulations & Waste Management | -0.6% | Global, particularly Europe & North America | Long-term (2025-2033) |

| High Energy Intensity and Carbon Emissions | -0.5% | Global | Ongoing (2025-2033) |

| Logistics & Transportation Costs due to Weight & Fragility | -0.4% | Global | Ongoing (2025-2033) |

Glass Bottle and Glass Packaging Market - Updated Report Scope

This comprehensive market report offers an in-depth analysis of the global Glass Bottle and Glass Packaging market, providing crucial insights into its historical performance, current dynamics, and future projections. The scope encompasses detailed segmentation across various applications, capacities, and colors, examining their individual contributions to market growth and identifying emerging opportunities. It also provides a thorough regional analysis, highlighting key market trends and drivers in major geographical areas. The report further profiles leading market players, offering competitive intelligence and strategic recommendations for stakeholders to navigate the evolving market landscape successfully.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 68.5 Billion |

| Market Forecast in 2033 | USD 107.8 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | O-I Glass, Inc., Ardagh Group S.A., Verallia S.A., Vidrala S.A., BA Glass S.A., Vetropack Holding AG, Piramal Glass Private Limited, SGD Pharma SAS, Consol Glass (Pty) Ltd., Gerresheimer AG, Nipro Corporation, Toyo Glass Co., Ltd., Hindustan National Glass & Industries Ltd., Shandong Pharmaceutical Glass Co. Ltd., Bormioli Pharma S.p.A., Stoelzle Glass Group, Nihon Yamamura Glass Co., Ltd., Gallo Glass Company, Wiegand-Glas GmbH, Sisecam Cam Ambalaj |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global glass bottle and glass packaging market is meticulously segmented to provide a granular understanding of its diverse applications and product attributes. This segmentation allows for a precise analysis of demand patterns, identifying which sectors are experiencing the most significant growth and where new opportunities are emerging. Understanding these segments is crucial for manufacturers to tailor their production, marketing, and distribution strategies effectively, ensuring they meet specific industry requirements and consumer preferences.

The detailed breakdown by application, capacity, and color highlights the multifaceted nature of the market. For instance, the demand for glass packaging varies considerably between the pharmaceutical industry, which prioritizes sterility and chemical inertness, and the food and beverage sector, which focuses on shelf life, aesthetic appeal, and brand presentation. Similarly, capacity and color choices are often dictated by product type and regional consumer tastes, influencing market dynamics and competitive landscapes within each niche. This comprehensive segmentation provides a robust framework for strategic decision-making and market forecasting.

- By Application:

- Food & Beverages

- Alcoholic Beverages (Beer, Wine, Spirits)

- Non-Alcoholic Beverages (Soft Drinks, Juices, Water, Milk & Dairy)

- Food Products (Jams & Spreads, Pickles, Sauces, Baby Food, Spices)

- Pharmaceuticals

- Personal Care & Cosmetics

- Chemicals

- Others (Household & Industrial, Automotive)

- Food & Beverages

- By Capacity:

- Up to 300 ml

- 301 ml to 500 ml

- 501 ml to 750 ml

- Above 750 ml

- By Color:

- Flint (Clear)

- Amber

- Green

- Blue

- Others (Opaque, Specialty Colors)

Regional Highlights

The global glass bottle and glass packaging market exhibits significant regional variations, influenced by differing economic development, consumer preferences, regulatory frameworks, and industrial growth rates. Asia Pacific continues to emerge as the dominant and fastest-growing region, driven by its large population base, rapid urbanization, and expanding food and beverage consumption. Countries like China and India are witnessing substantial growth in packaged food, alcoholic beverages, and pharmaceutical sectors, fueling the demand for glass packaging. The region's increasing disposable incomes and evolving retail landscape further contribute to this robust growth.

Europe represents a mature yet highly innovative market, characterized by strong sustainability mandates and a preference for premium products. The region leads in glass recycling rates and is at the forefront of lightweighting technologies and circular economy initiatives. North America also maintains a stable demand, particularly in the craft beverage and pharmaceutical sectors, with a growing emphasis on recycled content and eco-friendly practices. Latin America and the Middle East & Africa regions are poised for gradual growth, stimulated by economic diversification, increasing industrialization, and rising consumer awareness regarding sustainable packaging options.

- Asia Pacific: The largest and fastest-growing market, primarily due to expanding economies, increasing population, and rising consumption of packaged food, beverages, and pharmaceuticals in countries like China, India, and Southeast Asian nations.

- Europe: A mature market characterized by stringent environmental regulations, high recycling rates, and a strong demand for premium and sustainable glass packaging, particularly in countries such as Germany, France, and the UK.

- North America: Exhibits stable demand, driven by the robust food and beverage industry, growth in craft breweries and distilleries, and an increasing focus on environmentally friendly packaging solutions, predominantly in the United States and Canada.

- Latin America: Expected to show steady growth, fueled by economic development, rising disposable incomes, and increasing consumption of alcoholic and non-alcoholic beverages, with Brazil and Mexico being key contributors.

- Middle East and Africa (MEA): An emerging market with growing industrialization, improving healthcare infrastructure, and increasing consumer awareness, leading to a gradual rise in demand for glass packaging across various applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Glass Bottle and Glass Packaging Market.- O-I Glass, Inc.

- Ardagh Group S.A.

- Verallia S.A.

- Vidrala S.A.

- BA Glass S.A.

- Vetropack Holding AG

- Piramal Glass Private Limited

- SGD Pharma SAS

- Consol Glass (Pty) Ltd.

- Gerresheimer AG

- Nipro Corporation

- Toyo Glass Co., Ltd.

- Hindustan National Glass & Industries Ltd.

- Shandong Pharmaceutical Glass Co. Ltd.

- Bormioli Pharma S.p.A.

- Stoelzle Glass Group

- Nihon Yamamura Glass Co., Ltd.

- Gallo Glass Company

- Wiegand-Glas GmbH

- Sisecam Cam Ambalaj

Frequently Asked Questions

Analyze common user questions about the Glass Bottle and Glass Packaging market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth of the glass bottle and glass packaging market?

The global glass bottle and glass packaging market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated value of USD 107.8 Billion by 2033 from USD 68.5 Billion in 2025.

What are the primary drivers for this market?

Key drivers include the increasing consumer preference for sustainable and infinitely recyclable packaging, growing demand from the food and beverage industry (especially premium and alcoholic segments), and the expanding pharmaceutical sector due to glass's inertness and barrier properties.

How does sustainability impact the glass packaging industry?

Sustainability is a core driver, with glass being favored for its infinite recyclability. This trend is pushing manufacturers to increase recycled content (cullet) use and invest in energy-efficient production, aligning with global environmental goals and consumer demand for eco-friendly products.

Which regions are key contributors to market growth?

Asia Pacific is the leading and fastest-growing region, driven by its large population and expanding industries. Europe and North America represent mature markets with a strong focus on premiumization and sustainable practices, while Latin America and MEA show emerging growth potential.

What are the main challenges facing the glass packaging market?

Major challenges include intense competition from alternative packaging materials (like plastics), high energy consumption in manufacturing leading to significant operational costs, volatility in raw material prices, and the ongoing need to comply with stringent environmental regulations and improve recycling infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted