GIS in Disaster Management Market

GIS in Disaster Management Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708297 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

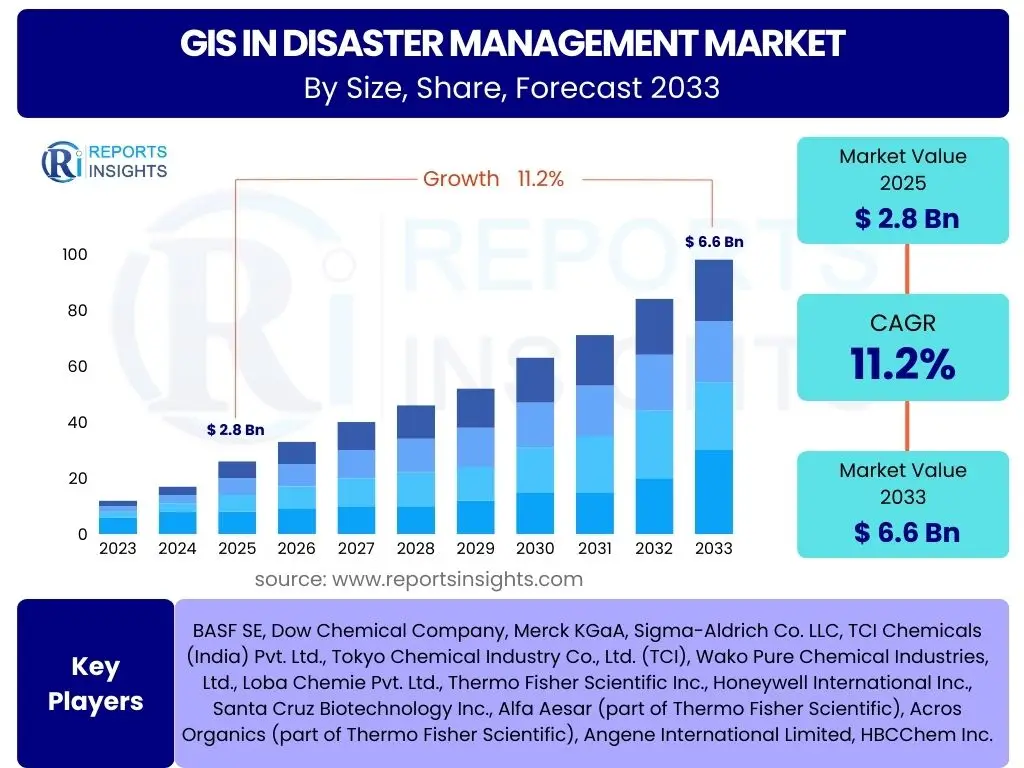

GIS in Disaster Management Market Size

According to Reports Insights Consulting Pvt Ltd, The GIS in Disaster Management Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.2% between 2025 and 2033. The market is estimated at USD 2.8 Billion in 2025 and is projected to reach USD 6.6 Billion by the end of the forecast period in 2033.

Key GIS in Disaster Management Market Trends & Insights

The GIS in Disaster Management market is experiencing significant transformation driven by the escalating frequency and intensity of natural and man-made disasters, coupled with rapid technological advancements. Users frequently inquire about the emerging technologies and methodologies that are shaping disaster response and mitigation efforts. Key trends indicate a strong shift towards integrating real-time data from diverse sources, including satellite imagery, IoT sensors, and social media, to create more dynamic and accurate situational awareness platforms. This integration enables swifter decision-making and more efficient resource allocation during critical events.

Another prominent trend involves the increasing adoption of cloud-based GIS solutions, which offer enhanced scalability, accessibility, and collaboration capabilities. This allows various stakeholders, from government agencies to emergency services and NGOs, to share and access critical spatial data seamlessly, irrespective of their geographical location. Furthermore, there is a growing emphasis on predictive analytics and AI-driven insights within GIS platforms, moving beyond reactive responses to proactive risk assessment and early warning systems. This forward-looking approach aims to minimize potential damage and loss of life by anticipating disaster events and preparing communities more effectively.

The convergence of mobile GIS applications with field operations is also a critical insight, empowering first responders and field personnel with immediate access to crucial maps, hazard information, and operational plans on their handheld devices. This enhances operational efficiency and safety during complex disaster scenarios. These trends collectively underscore a market evolving towards more sophisticated, integrated, and intelligent solutions for comprehensive disaster management.

- Integration of real-time sensor data and IoT for dynamic situational awareness.

- Increased adoption of cloud-based GIS platforms for enhanced collaboration and scalability.

- Expansion of predictive analytics and AI for early warning and risk assessment.

- Proliferation of mobile GIS applications for on-site data collection and decision support.

- Utilization of UAVs (drones) for rapid damage assessment and mapping.

- Development of sophisticated 3D and 4D GIS for intricate urban disaster modeling.

- Emphasis on geospatial data interoperability and standardization across agencies.

AI Impact Analysis on GIS in Disaster Management

User queries regarding the impact of Artificial Intelligence (AI) on GIS in disaster management frequently center on its potential to revolutionize data processing, predictive capabilities, and decision support. AI algorithms are significantly enhancing the efficiency and accuracy with which vast amounts of geospatial data are analyzed, moving beyond traditional manual methods. This enables faster identification of patterns, anomalies, and critical insights from satellite imagery, social media feeds, and sensor networks, which are invaluable during the dynamic phases of disaster response and recovery. The integration of AI allows for automated feature extraction, object recognition, and change detection, which can rapidly assess damage or identify affected areas with minimal human intervention.

Furthermore, AI-driven models are empowering GIS platforms with advanced predictive capabilities, such as forecasting disaster trajectories, estimating impact zones, and modeling evacuation routes with greater precision. Machine learning techniques are being applied to historical disaster data, weather patterns, and demographic information to develop more robust early warning systems. This proactive capability shifts the paradigm from reactive disaster management to preventative and anticipatory strategies, allowing authorities to pre-position resources, issue timely warnings, and mitigate potential harm more effectively. The synergy between AI and GIS is creating intelligent systems that can adapt to evolving disaster scenarios and provide actionable intelligence in real-time.

The impact also extends to optimizing resource allocation and logistics, where AI can analyze real-time demand and supply chains to direct aid and emergency personnel to areas of greatest need, minimizing delays and maximizing impact. AI-powered chatbots and virtual assistants, integrated with GIS, can also enhance public communication by providing personalized, location-specific information to affected populations. While the benefits are substantial, concerns often arise regarding data quality, algorithmic bias, and the need for skilled personnel to manage and interpret these advanced systems. Despite these challenges, AI's transformative potential in making GIS an even more powerful tool for disaster resilience is undeniable, leading to more intelligent, efficient, and life-saving operations.

- Enhanced predictive modeling for disaster forecasting and early warning systems.

- Automated analysis of geospatial data, including satellite imagery and drone footage, for rapid damage assessment.

- Improved resource allocation and logistics optimization through intelligent routing and demand prediction.

- Real-time situational awareness platforms powered by AI for dynamic decision-making.

- Development of AI-driven tools for risk assessment and vulnerability mapping.

- Smart communication systems integrated with GIS to disseminate targeted information.

- Increased efficiency in data processing and pattern recognition from diverse data sources.

Key Takeaways GIS in Disaster Management Market Size & Forecast

Common user questions about the GIS in Disaster Management market size and forecast reveal a strong interest in understanding the underlying drivers of growth, the long-term investment opportunities, and the critical role technology plays in shaping future resilience efforts. The primary takeaway is the market's robust growth trajectory, propelled by the increasing global frequency and severity of natural disasters, necessitating advanced tools for effective management. This trend underscores a sustained demand for sophisticated GIS solutions, making it an attractive sector for technological innovation and strategic investment. The consistent rise in market valuation reflects a fundamental recognition of GIS as an indispensable component of modern disaster preparedness, response, and recovery frameworks.

Another significant insight is that technological advancements, particularly in areas like real-time data analytics, cloud computing, and AI integration, are not merely enhancing existing capabilities but are creating entirely new possibilities for disaster management. The forecast growth indicates that stakeholders across government, non-governmental organizations, and private sectors are increasingly prioritizing investments in these advanced solutions to build more resilient communities and infrastructure. This continuous technological evolution is a key determinant of the market's expansion, driving both solution providers and end-users towards more innovative and integrated systems. The focus is shifting towards comprehensive lifecycle management of disasters, from prevention and mitigation to response and long-term recovery, all underpinned by geospatial intelligence.

Finally, the market’s expansion is also heavily influenced by heightened public awareness, evolving regulatory landscapes, and the increasing complexity of global supply chains, all of which demand more sophisticated spatial intelligence for risk assessment and operational planning. The anticipated growth reflects a collective global effort to minimize the human and economic toll of disasters, positioning GIS as a foundational technology in this endeavor. Investors and strategic planners should recognize the long-term imperative for improved disaster resilience, which will continue to fuel innovation and adoption in this critical market.

- The GIS in Disaster Management market exhibits a strong and consistent growth trajectory.

- Increasing global disaster frequency is a primary driver for market expansion.

- Technological advancements, including AI and cloud, are pivotal for future growth.

- Significant investment opportunities exist in innovative geospatial solutions.

- GIS is becoming an indispensable tool across all phases of disaster management.

- Government and NGO initiatives are key catalysts for adoption and market development.

- The market is driven by both reactive response needs and proactive mitigation strategies.

GIS in Disaster Management Market Drivers Analysis

The GIS in Disaster Management market is significantly propelled by several powerful drivers that collectively underscore its growing importance in global resilience strategies. A primary driver is the alarming increase in the frequency and intensity of natural disasters worldwide, including floods, earthquakes, wildfires, and extreme weather events. This escalating trend necessitates more robust and technologically advanced systems for accurate monitoring, prediction, and response, making GIS an essential tool for authorities and organizations. The economic and human toll of these events puts immense pressure on governments and emergency services to invest in solutions that can mitigate damage and save lives.

Additionally, the rapid advancements in geospatial technologies, such as high-resolution satellite imagery, drone technology, and remote sensing, have dramatically improved the accuracy and timeliness of data available for GIS applications. These technological improvements enable more precise damage assessments, better real-time situational awareness, and more effective resource deployment. Furthermore, the growing emphasis on smart city initiatives and resilient infrastructure development globally is integrating GIS as a foundational component for urban planning and emergency preparedness. This proactive approach ensures that new developments are designed with disaster mitigation in mind, further driving market demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Frequency and Intensity of Natural Disasters | +3.5% | Global, particularly Asia Pacific, North America | Short to Long-Term |

| Advancements in Geospatial Technologies (Satellite, Drone, IoT) | +2.8% | North America, Europe, Asia Pacific | Mid to Long-Term |

| Growing Government and Regulatory Initiatives for Disaster Preparedness | +2.2% | Europe, North America, Developing Economies | Mid to Long-Term |

| Rising Adoption of Smart City and Resilient Infrastructure Projects | +1.7% | Global, especially urbanized regions | Mid to Long-Term |

GIS in Disaster Management Market Restraints Analysis

Despite its significant growth potential, the GIS in Disaster Management market faces several notable restraints that could temper its expansion. One primary restraint is the high initial investment cost associated with implementing sophisticated GIS software, hardware, and data infrastructure. This significant upfront expenditure can be a barrier for smaller organizations, local governments, or developing economies with limited budgets, hindering widespread adoption. The complexity of integrating these systems with existing legacy infrastructure also adds to the financial and operational burden, requiring substantial resources for training and customization.

Another significant challenge revolves around data interoperability and standardization. Disaster management often involves multiple agencies, each with its own data formats, systems, and protocols. The lack of universal standards for geospatial data sharing can create significant hurdles in aggregating information from diverse sources, leading to delays and inefficiencies during critical response phases. Ensuring seamless data exchange and collaboration across disparate platforms remains a persistent technical and organizational challenge. Additionally, the shortage of skilled professionals capable of effectively operating, maintaining, and interpreting complex GIS data further acts as a restraint, limiting the full utilization of these advanced tools.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Implementation Costs and Infrastructure Requirements | -2.0% | Developing Economies, Local Governments | Short to Mid-Term |

| Data Interoperability and Standardization Challenges | -1.5% | Global, Multi-Agency Operations | Mid-Term |

| Lack of Skilled Professionals and Technical Expertise | -1.0% | Global, particularly emerging markets | Short to Mid-Term |

GIS in Disaster Management Market Opportunities Analysis

The GIS in Disaster Management market is characterized by numerous promising opportunities that are poised to accelerate its growth and innovation. A key opportunity lies in the continuous advancement and integration of emerging technologies such as Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT). These technologies can significantly enhance GIS capabilities by enabling predictive analytics, automated data processing, and real-time sensor integration, leading to more intelligent and responsive disaster management systems. The development of sophisticated algorithms for risk modeling and early warning presents a substantial area for innovation and market expansion.

Furthermore, the increasing focus on public-private partnerships (PPPs) in disaster resilience offers significant opportunities. Collaborations between government agencies, technology providers, and private sector entities can pool resources, expertise, and innovative solutions to develop and deploy advanced GIS applications. This cooperative approach can address funding gaps, accelerate technology adoption, and ensure solutions are tailored to specific regional needs. The expansion of GIS applications into emerging economies, which are often highly vulnerable to natural disasters but possess nascent disaster management infrastructure, represents a vast untapped market. These regions present significant potential for scalable and cost-effective GIS deployments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of AI/ML and IoT for Predictive Analytics | +3.0% | Global, Technology-Advanced Regions | Mid to Long-Term |

| Expansion into Emerging Economies and Developing Regions | +2.5% | Asia Pacific, Latin America, Africa | Long-Term |

| Growth of Public-Private Partnerships and Collaborative Initiatives | +2.0% | Global | Mid to Long-Term |

| Development of Customized Solutions for Specific Disaster Types | +1.8% | Global, Region-Specific | Mid to Long-Term |

GIS in Disaster Management Market Challenges Impact Analysis

The GIS in Disaster Management market, while growing, faces several complex challenges that require strategic solutions to overcome. One significant challenge is ensuring the accuracy and reliability of real-time data, particularly from diverse and often unstructured sources such as social media, crowd-sourced information, and rapidly deployed sensors. The sheer volume and velocity of this data can be overwhelming, making it difficult to filter out noise, verify information, and integrate it seamlessly into GIS platforms without compromising the integrity of situational awareness. Maintaining data quality under pressure during emergency events is a continuous struggle.

Another critical challenge is the inherent complexity of integrating GIS systems with existing disparate legacy systems and emergency communication networks. Many organizations operate on older technologies, and achieving full interoperability for real-time data exchange can be technically demanding and resource-intensive. This fragmentation can impede coordinated response efforts and create information silos, diminishing the overall effectiveness of GIS in a multi-agency disaster scenario. Overcoming these integration hurdles requires significant investment in standardized protocols and collaborative system development. Furthermore, funding constraints, especially for local governmental bodies and non-profit organizations, represent a persistent challenge in acquiring and maintaining state-of-the-art GIS solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Real-Time Data Accuracy and Reliability | -1.8% | Global, Complex Disaster Scenarios | Ongoing |

| Integration with Legacy Systems and Interoperability Issues | -1.5% | Global, Established Agencies | Mid to Long-Term |

| Cybersecurity Risks and Data Privacy Concerns | -1.2% | Global | Ongoing |

| Funding Limitations and Resource Scarcity for Implementation | -1.0% | Developing Economies, Local Governments | Short to Mid-Term |

GIS in Disaster Management Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the GIS in Disaster Management market, offering critical insights into its current landscape and future growth trajectory. The scope encompasses detailed market sizing, forecasting, and a thorough examination of key drivers, restraints, opportunities, and challenges influencing the industry. The report also segments the market by component, application, end-user, and deployment, providing a granular view of market dynamics across various categories. Furthermore, it includes a regional analysis highlighting key geographical trends and competitive landscape assessment, profiling major industry players and their strategic initiatives to deliver a holistic market perspective for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 6.6 Billion |

| Growth Rate | 11.2% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Esri, Hexagon AB, Trimble Inc., Maxar Technologies, RMS (Risk Management Solutions), Accenture, Harris Corporation, Fugro N.V., BlackSky, Planet Labs, Google, Microsoft, Amazon Web Services, SAP, IBM, Oracle, Tata Consultancy Services, Capgemini, Wipro Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The GIS in Disaster Management market is comprehensively segmented to provide a detailed understanding of its various facets and operational domains. This segmentation allows for a granular analysis of market dynamics, revealing specific growth areas, key user requirements, and technological preferences. The primary segmentation categories include component, application, end-user, and deployment model, each offering unique insights into how GIS solutions are developed, adopted, and utilized across the disaster management lifecycle. Understanding these segments is crucial for stakeholders to tailor strategies, innovate solutions, and target specific market needs effectively.

The "By Component" segment differentiates between software and services, highlighting the increasing demand for specialized GIS software alongside expert consulting, implementation, and maintenance services. The "By Application" segment further breaks down the market based on specific disaster management phases, such as risk assessment, early warning, emergency response, and post-disaster recovery, reflecting the diverse utility of GIS across the entire disaster continuum. "By End-User" categorizes the market based on the types of organizations leveraging GIS, including government agencies, NGOs, and various private sector entities, showcasing the broad applicability of these solutions. Finally, "By Deployment" distinguishes between on-premise, cloud-based, and hybrid models, indicating the evolving preferences for scalability, accessibility, and data security among users. This detailed segmentation is instrumental in deciphering complex market trends and identifying strategic opportunities for growth.

- By Component: This segment distinguishes between the core software platforms and the essential services that support their implementation and operation.

- Software: Includes GIS platforms, spatial databases, and analytical tools.

- Services: Comprises consulting, implementation, training, data integration, and maintenance services.

- By Application: This segmentation focuses on the specific phases and functions within the disaster management lifecycle where GIS is utilized.

- Risk Assessment & Vulnerability Mapping: Identifying potential hazards and at-risk populations.

- Early Warning & Monitoring: Real-time tracking of environmental conditions and impending threats.

- Emergency Response & Operations: Directing rescue efforts, managing logistics, and coordinating personnel.

- Damage Assessment & Recovery: Evaluating post-disaster impact and planning reconstruction.

- Mitigation & Preparedness: Long-term planning to reduce disaster impact and enhance readiness.

- By End-User: This segment classifies the market based on the types of organizations that adopt GIS for disaster management.

- Government & Public Safety Agencies: Federal, state, and local governments, police, fire departments.

- Non-Governmental Organizations (NGOs): Humanitarian aid and relief organizations.

- Emergency Medical Services (EMS): Health departments and ambulance services.

- Healthcare & Lifesciences: Hospitals and research institutions for public health crises.

- Utilities & Infrastructure: Power, water, telecommunications, and transportation sectors.

- Defense & Military: Strategic planning and operational support.

- Insurance: Risk assessment and claims management.

- Agriculture: Monitoring crop health and land use in disaster-prone areas.

- Energy & Mining: Assessing risks to critical infrastructure.

- By Deployment: This category differentiates solutions based on their hosting and accessibility models.

- On-Premise: Software hosted on local servers within an organization's infrastructure.

- Cloud-Based: Solutions delivered over the internet, offering scalability and remote access.

- Hybrid: A combination of both on-premise and cloud elements, balancing control and flexibility.

Regional Highlights

- North America: This region leads the GIS in Disaster Management market due to its advanced technological infrastructure, high adoption rates of cutting-edge solutions, and significant investments in disaster preparedness by government agencies. The presence of major technology providers and a strong focus on public safety initiatives further contribute to its dominance. Frequent occurrences of severe weather events like hurricanes and wildfires also drive continuous innovation and demand.

- Europe: Characterized by stringent regulatory frameworks for disaster risk reduction and environmental protection, Europe demonstrates a robust market for GIS in disaster management. Emphasis on cross-border cooperation for emergency response and well-established smart city initiatives foster the adoption of integrated geospatial solutions. Countries like Germany, France, and the UK are key contributors to market growth, driven by both national and EU-level policies.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, the APAC region is highly vulnerable to a wide range of natural disasters, including tsunamis, earthquakes, and monsoons. Rapid urbanization, increasing population density, and developing economies are driving substantial investments in GIS solutions for early warning systems, urban planning, and infrastructure resilience. Countries such as Japan, China, India, and Australia are at the forefront of this regional expansion.

- Latin America: This region faces significant challenges from natural disasters like seismic activity, volcanic eruptions, and tropical storms, which are increasingly driving the demand for effective disaster management solutions. While still developing, the market here shows promising growth potential as governments and international aid organizations increase efforts to enhance disaster resilience through the adoption of GIS technology.

- Middle East & Africa (MEA): The MEA region is witnessing growing awareness and investment in GIS for disaster management, particularly in areas prone to floods, droughts, and seismic activities. Economic diversification, smart city projects in the Middle East, and increasing international humanitarian aid efforts in Africa are key factors stimulating market growth. However, challenges related to infrastructure and funding remain.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the GIS in Disaster Management Market.- Esri

- Hexagon AB

- Trimble Inc.

- Maxar Technologies

- RMS (Risk Management Solutions)

- Accenture

- Harris Corporation

- Fugro N.V.

- BlackSky

- Planet Labs

- Microsoft

- Amazon Web Services

- SAP

- IBM

- Oracle

- Tata Consultancy Services

- Capgemini

- Wipro Limited

Frequently Asked Questions

Analyze common user questions about the GIS in Disaster Management market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is GIS in disaster management and why is it important?

GIS (Geographic Information Systems) in disaster management involves using spatial data and analytical tools to visualize, analyze, and manage information related to disasters. It is crucial for enhancing situational awareness, supporting decision-making, optimizing resource allocation, and improving overall preparedness, response, and recovery efforts by providing a geographic context to critical data.

How does GIS contribute to early warning systems for natural disasters?

GIS integrates real-time data from weather sensors, satellites, and seismic monitors to create dynamic maps that predict disaster trajectories and impact zones. It provides critical spatial insights for issuing timely warnings, identifying vulnerable populations, and planning evacuation routes, thereby minimizing potential harm and enabling proactive measures.

What are the primary challenges in implementing GIS solutions for disaster management?

Key challenges include high initial implementation costs, issues with data interoperability and standardization across different agencies, and a shortage of skilled personnel. Ensuring the accuracy and real-time reliability of diverse data sources, alongside addressing cybersecurity and data privacy concerns, also presents significant hurdles.

What role does AI play in the future of GIS in disaster management?

AI is set to revolutionize GIS by enhancing predictive modeling for forecasting, automating the analysis of vast datasets for rapid damage assessment, and optimizing resource allocation. AI-driven insights will lead to more intelligent early warning systems, personalized communication during crises, and more efficient disaster recovery planning, making systems more adaptive and powerful.

Which sectors are the primary end-users of GIS in disaster management?

The primary end-users include government and public safety agencies (e.g., emergency services, defense), Non-Governmental Organizations (NGOs) involved in humanitarian aid, utilities and infrastructure companies for network protection, and increasingly, healthcare, insurance, and agricultural sectors for risk assessment and impact mitigation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted