Geotechnical Sensor Market

Geotechnical Sensor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710120 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Geotechnical Sensor Market Size

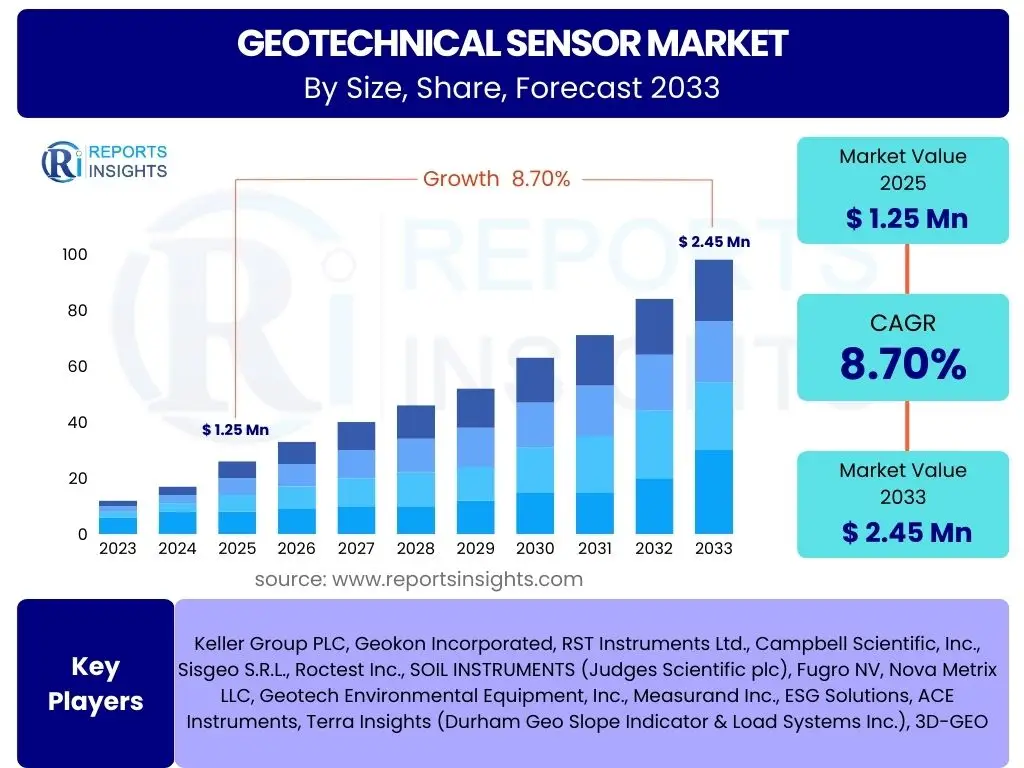

According to Reports Insights Consulting Pvt Ltd, The Geotechnical Sensor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.45 Billion by the end of the forecast period in 2033.

Key Geotechnical Sensor Market Trends & Insights

The Geotechnical Sensor market is experiencing significant evolution driven by advancements in sensor technology, increased infrastructure development, and a growing emphasis on safety and environmental monitoring. Users are frequently seeking to understand how new technologies, particularly wireless and IoT-enabled sensors, are transforming traditional geotechnical practices. There is also considerable interest in the impact of evolving regulatory frameworks and climate change initiatives on market demand, as these factors necessitate more robust and continuous monitoring solutions. Furthermore, the push for sustainable construction and smart city development is creating new niches for innovative sensor applications that can provide real-time data for proactive decision-making.

Another prominent trend attracting user attention is the integration of data analytics and cloud computing with geotechnical sensor networks. This enables more sophisticated interpretation of sensor data, moving beyond simple data collection to predictive modeling and risk assessment. The market is also witnessing a shift towards miniaturized, robust, and energy-efficient sensors capable of operating in harsh and remote environments for extended periods. This focus on durability and low maintenance is critical for large-scale infrastructure projects and long-term monitoring initiatives, addressing a key concern among professionals regarding the operational lifespan and reliability of deployed sensors.

- Increased adoption of wireless and IoT-enabled geotechnical sensors.

- Growing demand for real-time data monitoring and analytics solutions.

- Technological advancements in sensor miniaturization, durability, and energy efficiency.

- Integration of cloud computing and AI for predictive maintenance and risk assessment.

- Strict governmental regulations for infrastructure safety and environmental protection.

- Rise in infrastructure development projects in emerging economies.

- Shift towards remote monitoring and automated data collection systems.

AI Impact Analysis on Geotechnical Sensor

Artificial Intelligence (AI) is poised to significantly transform the Geotechnical Sensor market by enhancing data interpretation, predictive capabilities, and operational efficiency. Common user questions revolve around how AI can process vast amounts of sensor data more effectively than traditional methods, particularly for identifying subtle patterns and anomalies that might indicate potential structural failures or ground instability. The expectation is that AI algorithms, through machine learning, will enable more accurate and timely risk assessments, moving from reactive responses to proactive interventions in critical infrastructure and natural hazard monitoring.

Furthermore, there is keen interest in AI's role in optimizing sensor network deployment and maintenance. Users want to know if AI can help determine the most strategic placement of sensors for optimal data collection or predict sensor malfunctions, thereby reducing maintenance costs and ensuring data integrity. The integration of AI also holds the promise of automating complex data analysis tasks, making geotechnical monitoring more accessible and less reliant on highly specialized human interpretation, which could address the industry's shortage of skilled personnel. This shift towards intelligent monitoring systems represents a significant leap forward in the capabilities offered by geotechnical sensors.

- Enhanced data analysis and pattern recognition from complex sensor datasets.

- Improved predictive maintenance and early warning systems for structural integrity and ground movement.

- Optimization of sensor placement and network design using AI algorithms.

- Automation of data processing and reporting, reducing manual effort and human error.

- Development of advanced models for predicting geological behavior and mitigating risks.

- Integration of machine learning for adaptive monitoring and real-time decision support.

- Potential to address skilled labor shortages by automating interpretation tasks.

Key Takeaways Geotechnical Sensor Market Size & Forecast

The Geotechnical Sensor market is characterized by robust growth, primarily driven by global infrastructure development and increasing concerns over public safety and environmental sustainability. A key takeaway is the consistent demand for advanced monitoring solutions across diverse applications, from large-scale civil engineering projects to mining operations and critical infrastructure maintenance. The forecast indicates sustained expansion, fueled by technological innovations that enhance sensor accuracy, reliability, and ease of deployment. Stakeholders should recognize the accelerating shift towards integrated systems that combine hardware with sophisticated software for data management and analysis.

Another significant insight from the market size and forecast is the increasing emphasis on preventative measures and real-time monitoring to mitigate risks associated with geological hazards and structural degradation. This has created a strong market for sensors capable of providing continuous data streams and facilitating early detection of potential issues. The geographical distribution of growth highlights opportunities in rapidly developing regions, where massive construction and infrastructure projects are underway. Understanding these regional dynamics and the specific regulatory environments will be crucial for market participants aiming to capitalize on future growth avenues and solidify their market position.

- The market is poised for significant expansion, driven by infrastructure investment and safety regulations.

- Technological innovation, especially in wireless and IoT sensors, is a primary growth catalyst.

- Demand for real-time data and predictive analytics is creating new opportunities.

- Asia Pacific and North America are expected to be key growth regions.

- Integration of AI and cloud platforms will enhance market value proposition.

- The market focuses on preventative monitoring to reduce risks and costs.

Geotechnical Sensor Market Drivers Analysis

The Geotechnical Sensor market is propelled by a confluence of factors, foremost among them being the accelerating pace of global infrastructure development, particularly in emerging economies. Projects such as smart cities, high-speed rail networks, and large-scale mining operations inherently require comprehensive ground stability and structural health monitoring. This demand is further amplified by increasing concerns over safety and environmental protection, leading to stricter regulations and mandates for continuous surveillance of critical assets and hazardous sites. The growing frequency and intensity of natural disasters also underscore the necessity for robust geotechnical monitoring solutions.

Technological advancements play a crucial role, with innovations in sensor design, wireless communication, and data analytics making these systems more efficient, cost-effective, and easier to deploy. The integration of the Internet of Things (IoT) and cloud computing platforms enables real-time data acquisition and remote monitoring, transforming traditional practices. Moreover, the aging infrastructure in developed nations necessitates continuous monitoring and maintenance to ensure longevity and prevent catastrophic failures, creating a sustained demand for geotechnical sensors. These drivers collectively contribute to the market's positive growth trajectory by addressing critical needs in construction, mining, and civil engineering.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Infrastructure Development & Urbanization | +2.5% | Asia Pacific, North America, Middle East | Short- to Long-term |

| Increasing Focus on Safety & Environmental Regulations | +1.8% | Europe, North America, Developed APAC | Mid- to Long-term |

| Technological Advancements (IoT, Wireless, AI Integration) | +2.0% | Global | Short- to Mid-term |

| Aging Infrastructure Monitoring Needs | +1.5% | North America, Europe | Mid- to Long-term |

| Rise in Mining and Construction Activities | +1.2% | Asia Pacific, Latin America, Africa | Short- to Mid-term |

Geotechnical Sensor Market Restraints Analysis

Despite the strong growth drivers, the Geotechnical Sensor market faces several restraints that could impede its full potential. A primary challenge is the high upfront cost associated with sophisticated sensor systems, including not only the sensor units themselves but also installation, data acquisition hardware, and specialized software for analysis. This significant initial investment can deter smaller construction firms or projects with limited budgets, particularly in price-sensitive emerging markets. Additionally, the complexity involved in the installation, calibration, and maintenance of these sensors requires specialized skills, which are often in short supply, leading to higher operational costs and potential data inaccuracies if not handled properly.

Another critical restraint is the technical complexity of data interpretation. Geotechnical data can be voluminous and intricate, requiring expert knowledge to translate raw sensor readings into actionable insights. This often necessitates specialized engineering expertise, which can be expensive and difficult to retain. Furthermore, the harsh environmental conditions in which many geotechnical sensors operate can affect their longevity and reliability, leading to increased replacement costs and potential data loss. Issues such as data security and privacy, especially with cloud-based systems, also present concerns that some organizations are hesitant to address, thereby limiting wider adoption of advanced monitoring solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Cost of Sensor Systems | -1.5% | Global, particularly Emerging Markets | Short- to Mid-term |

| Lack of Skilled Personnel for Installation and Interpretation | -1.2% | Global | Short- to Long-term |

| Complexity of Data Interpretation and Analysis | -1.0% | Global | Mid-term |

| Harsh Environmental Conditions Affecting Sensor Longevity | -0.8% | Specific Application Areas (e.g., Mining, Remote Sites) | Long-term |

| Data Security and Privacy Concerns | -0.7% | Developed Regions | Mid-term |

Geotechnical Sensor Market Opportunities Analysis

The Geotechnical Sensor market is replete with significant opportunities stemming from various technological advancements and evolving societal needs. The burgeoning trend of smart cities and intelligent infrastructure projects worldwide presents a substantial avenue for growth, as these initiatives inherently rely on extensive monitoring of ground conditions and structural integrity. The increasing adoption of the Internet of Things (IoT) in construction and civil engineering is opening doors for more connected and integrated sensor networks, facilitating remote monitoring and real-time data access, which were previously challenging. This integration enhances efficiency and provides unprecedented levels of insight into environmental and structural health.

Furthermore, the growing demand for sustainable construction practices and resilient infrastructure against climate change impacts creates a distinct opportunity for geotechnical sensors that can monitor environmental parameters, such as groundwater levels, soil moisture, and subsidence. Emerging economies, undergoing rapid urbanization and infrastructure development, represent untapped markets with immense potential for initial deployment and long-term expansion. The development of more robust, autonomous, and energy-efficient sensors, coupled with AI-driven analytics, will also create new applications and reduce operational costs, making these solutions more attractive to a wider range of end-users and fostering further market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart City & IoT Infrastructure | +2.3% | Global, especially Developed Regions and Tier-1 Emerging Cities | Short- to Long-term |

| Expansion in Emerging Economies with Rapid Urbanization | +2.0% | Asia Pacific, Latin America, Africa | Mid- to Long-term |

| Development of Autonomous and Low-Power Wireless Sensors | +1.7% | Global | Short- to Mid-term |

| Increased Demand for Environmental Monitoring Applications | +1.5% | Global | Mid- to Long-term |

| Partnerships for Integrated Solutions and Service Offerings | +1.0% | Global | Short-term |

Geotechnical Sensor Market Challenges Impact Analysis

The Geotechnical Sensor market, while growing, faces several significant challenges that market participants must address. One prominent challenge is the need for standardization across different sensor types, data formats, and communication protocols. The lack of uniform standards can lead to interoperability issues, making it difficult to integrate diverse sensor systems and hindering the development of comprehensive, scalable monitoring solutions. This fragmentation can also complicate data comparison and analysis across different projects or regions, limiting the overall utility and efficiency of geotechnical data.

Another critical challenge lies in ensuring the long-term reliability and durability of sensors, especially when deployed in harsh and remote environments, such as deep underground mines, construction sites with extreme weather, or marine settings. Sensors must withstand corrosion, extreme temperatures, and mechanical stresses for extended periods without requiring frequent maintenance or replacement. Furthermore, managing and securing the vast amounts of data generated by extensive sensor networks presents a substantial challenge. Issues related to data storage, transmission bandwidth, cybersecurity threats, and data privacy need robust solutions to build trust and encourage wider adoption of advanced geotechnical monitoring systems. Overcoming these challenges will be crucial for the sustained growth and maturity of the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardization and Interoperability | -1.3% | Global | Mid- to Long-term |

| Ensuring Long-term Reliability and Durability in Harsh Environments | -1.1% | Specific Application Areas | Long-term |

| High Initial Investment and Operational Costs | -1.0% | Global, particularly Small & Medium Enterprises | Short- to Mid-term |

| Data Management, Security, and Privacy Concerns | -0.9% | Global | Mid-term |

| Integration Complexities with Existing Infrastructure | -0.8% | Developed Regions with Legacy Systems | Short- to Mid-term |

Geotechnical Sensor Market - Updated Report Scope

This comprehensive report delves into the Geotechnical Sensor market, providing an in-depth analysis of its current state, historical performance, and future growth trajectories. It encompasses a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report offers critical insights into the technological advancements shaping the industry, including the impact of AI and IoT, and profiles leading market players to provide a holistic view of the competitive landscape. It is designed to equip stakeholders with the knowledge needed for strategic decision-making and market penetration.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.45 Billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Keller Group PLC, Geokon Incorporated, RST Instruments Ltd., Campbell Scientific, Inc., Sisgeo S.R.L., Roctest Inc., SOIL INSTRUMENTS (Judges Scientific plc), Fugro NV, Nova Metrix LLC, Geotech Environmental Equipment, Inc., Measurand Inc., ESG Solutions, ACE Instruments, Terra Insights (Durham Geo Slope Indicator & Load Systems Inc.), 3D-GEO |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Geotechnical Sensor market is meticulously segmented to provide a granular view of its diverse components, offering insights into distinct product types, technological approaches, end-use applications, and primary end-user categories. This segmentation helps in identifying specific growth pockets and understanding the varying demands across different sectors. Each segment is influenced by unique drivers and faces distinct challenges, contributing to a varied market landscape that requires tailored strategies for effective engagement. The comprehensive breakdown allows for a deeper analysis of market dynamics, competitive intensity, and potential for innovation within each category.

- By Type: Extensometers, Inclinometers, Piezometers, Strain Gauges, Load Cells, Thermometers & Thermistors, Pressure Transducers, Settlement Systems, Tiltmeters, Vibration Sensors, Other Sensors.

- By Technology: Wired Sensors, Wireless Sensors.

- By Application: Infrastructure Monitoring, Mining & Excavation, Oil & Gas Exploration & Production, Environmental Monitoring, Construction & Foundation Engineering, Others.

- By End-User: Government & Public Sector, Private Enterprises, Research & Academia.

Regional Highlights

- North America: A mature market characterized by significant investments in aging infrastructure upgrades, robust regulatory frameworks for safety, and early adoption of advanced monitoring technologies including IoT and AI. The presence of key market players and a strong R&D ecosystem drive innovation and market growth.

- Europe: Driven by stringent environmental regulations, extensive civil engineering projects, and a strong focus on sustainable development. Countries like Germany and the UK are at the forefront of adopting advanced geotechnical solutions for structural health monitoring and landslide prevention.

- Asia Pacific (APAC): The fastest-growing region, fueled by massive infrastructure development projects, rapid urbanization, and industrialization in countries such as China, India, and Southeast Asian nations. This region represents immense potential for new installations and technological adoption in construction, mining, and smart city initiatives.

- Latin America: Emerging market with growing investments in mining, oil and gas, and public infrastructure. The region presents opportunities for cost-effective and robust geotechnical monitoring solutions, particularly in areas prone to seismic activity and geological instability.

- Middle East & Africa (MEA): Characterized by large-scale construction and oil & gas projects, particularly in the GCC countries. Significant government spending on smart cities and mega-projects drives demand for advanced geotechnical sensors, alongside a growing emphasis on safety standards in resource extraction industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Geotechnical Sensor Market.- Keller Group PLC

- Geokon Incorporated

- RST Instruments Ltd.

- Campbell Scientific, Inc.

- Sisgeo S.R.L.

- Roctest Inc.

- SOIL INSTRUMENTS (Judges Scientific plc)

- Fugro NV

- Nova Metrix LLC

- Geotech Environmental Equipment, Inc.

- Measurand Inc.

- ESG Solutions

- ACE Instruments

- Terra Insights (Durham Geo Slope Indicator & Load Systems Inc.)

- 3D-GEO

Frequently Asked Questions

What is the projected growth rate of the Geotechnical Sensor market?

The Geotechnical Sensor market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033, reaching an estimated USD 2.45 Billion by 2033.

How is AI impacting the Geotechnical Sensor industry?

AI significantly enhances data interpretation, predictive analysis for structural integrity, and optimizes sensor deployment. It enables early warning systems and automates complex data processing, transforming geotechnical monitoring from reactive to proactive.

What are the primary drivers for the Geotechnical Sensor market?

Key drivers include global infrastructure development, increasing safety and environmental regulations, technological advancements such as IoT and wireless integration, and the critical need for monitoring aging infrastructure worldwide.

Which regions are expected to show the most significant growth?

Asia Pacific is anticipated to be the fastest-growing region due to extensive infrastructure projects and rapid urbanization, while North America and Europe will continue to be strong markets driven by regulatory compliance and aging infrastructure maintenance.

What challenges does the Geotechnical Sensor market face?

Challenges include high upfront costs, a shortage of skilled personnel for installation and data interpretation, complexities in data management and security, and ensuring sensor reliability in harsh operating environments, along with a lack of standardization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted