Gas Turbine Service Market

Gas Turbine Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702773 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Gas Turbine Service Market Size

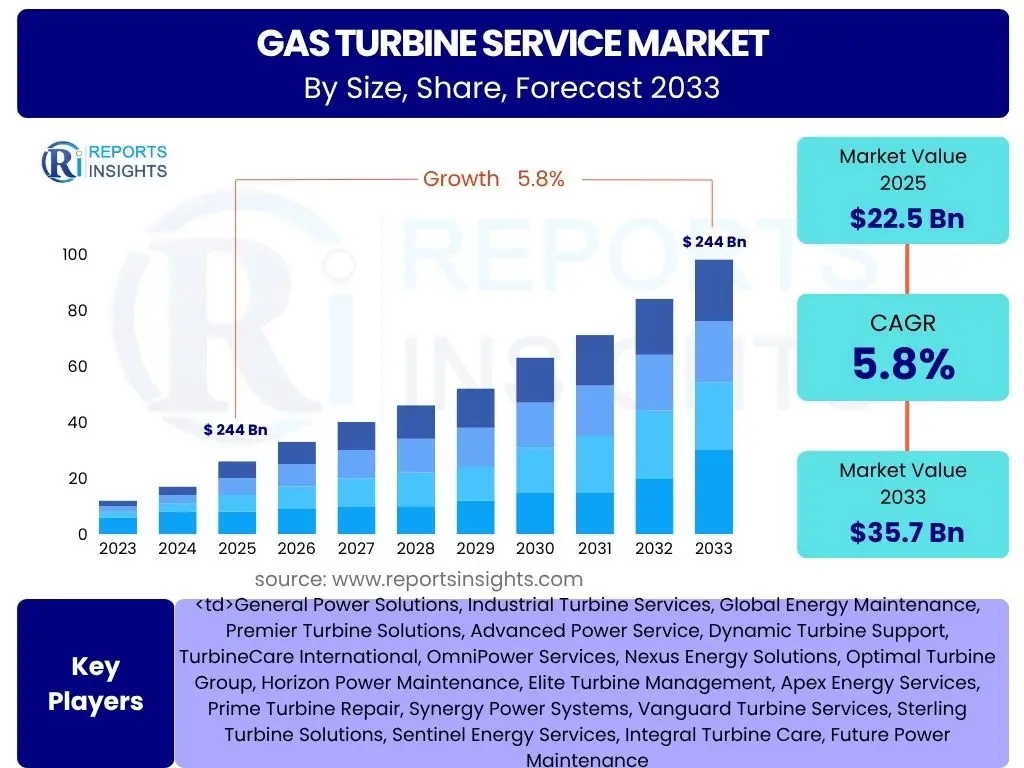

According to Reports Insights Consulting Pvt Ltd, The Gas Turbine Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. This robust growth trajectory is underpinned by increasing global energy demand, the need for enhanced operational efficiency, and the expanding installed base of gas turbines across various industries. The market's expansion is also significantly influenced by the lifecycle management requirements of aging turbine fleets, which necessitate continuous maintenance, repair, and overhaul (MRO) services to ensure reliability and performance.

The market is estimated at USD 22.5 billion in 2025 and is projected to reach USD 35.7 billion by the end of the forecast period in 2033. This substantial increase reflects the critical role of gas turbines in power generation, oil and gas, and industrial applications. The valuation further highlights the growing investment in advanced service solutions, including predictive maintenance, digital twin technology, and performance optimization services, which contribute to extended asset life and reduced operational downtime. The shift towards long-term service agreements (LTSAs) also plays a pivotal role in stabilizing market revenue and fostering consistent growth.

Key Gas Turbine Service Market Trends & Insights

User inquiries frequently highlight the transformative shifts occurring within the Gas Turbine Service market, with common questions revolving around how digital technologies, sustainability efforts, and operational efficiency demands are reshaping the industry. These concerns point to a strong interest in understanding the adoption of advanced analytics, artificial intelligence, and remote monitoring capabilities that are becoming standard for optimizing turbine performance and minimizing downtime. Furthermore, the drive towards decarbonization and the integration of hydrogen-ready turbine solutions are emerging as critical areas of inquiry, reflecting the industry's commitment to environmental responsibility and future-proofing energy infrastructure. The emphasis is increasingly on proactive, data-driven service models that extend asset life and enhance overall operational reliability in a dynamically evolving energy landscape.

- Digitalization and Industry 4.0 Integration: Increasing adoption of IoT, AI, and big data analytics for predictive maintenance, remote monitoring, and operational optimization, leading to reduced downtime and increased asset efficiency.

- Shift Towards Long-Term Service Agreements (LTSAs): Growing preference for comprehensive, multi-year service contracts that offer predictable maintenance costs, enhanced operational reliability, and performance guarantees.

- Focus on Decarbonization and Hydrogen-Ready Turbines: Rising demand for services that support the transition to lower-carbon fuels, including upgrades and maintenance for hydrogen-blending and carbon capture readiness.

- Asset Life Extension and Modernization: Significant investment in upgrading and retrofitting existing gas turbine fleets to extend their operational lifespan, improve efficiency, and meet evolving environmental standards.

- Increased Demand for Performance Optimization Services: Emphasis on improving fuel efficiency, reducing emissions, and enhancing the overall output of gas turbines through specialized service offerings and advanced control systems.

- Supply Chain Resilience and Localization: Efforts to diversify and localize supply chains for spare parts and service expertise to mitigate geopolitical risks and improve response times.

AI Impact Analysis on Gas Turbine Service

Common user questions regarding the impact of Artificial Intelligence (AI) on Gas Turbine Services frequently center on its practical applications in improving operational efficiency, predicting potential failures, and optimizing maintenance schedules. Stakeholders are keen to understand how AI algorithms can process vast amounts of sensor data to identify anomalies before they escalate into critical issues, thereby shifting from reactive to predictive maintenance paradigms. There is also significant interest in AI's role in enhancing troubleshooting capabilities and providing real-time performance insights, leading to more informed decision-making and reduced human intervention in routine tasks. Concerns also touch upon the data security implications and the need for specialized skills to effectively implement and manage AI-driven solutions.

- Predictive Maintenance Enhancement: AI algorithms analyze real-time operational data from gas turbines to predict potential component failures, enabling proactive maintenance scheduling and significantly reducing unscheduled downtime.

- Operational Efficiency Optimization: AI-driven systems fine-tune turbine parameters for optimal fuel consumption and power output, adapting to varying operational conditions and maximizing performance.

- Fault Detection and Diagnostics: AI models quickly identify subtle anomalies and diagnose the root causes of performance degradation or equipment malfunctions, often faster and more accurately than traditional methods.

- Automated Data Analysis and Reporting: AI tools automate the collection, processing, and interpretation of complex turbine data, generating actionable insights and comprehensive reports for maintenance teams and operators.

- Digital Twin Integration: AI enhances digital twin capabilities by providing more accurate simulations and predictive models, allowing for virtual testing of maintenance strategies and performance upgrades without physical intervention.

- Workforce Augmentation and Training: AI-powered tools assist technicians with intelligent troubleshooting guides, augmented reality overlays for repairs, and personalized training modules, upskilling the workforce.

- Remote Monitoring and Control: AI facilitates advanced remote monitoring, allowing expert teams to oversee and, in some cases, remotely adjust turbine operations and troubleshoot issues from a centralized location.

Key Takeaways Gas Turbine Service Market Size & Forecast

Key user questions concerning market size and forecast consistently underscore the underlying drivers of growth, specifically querying how aging infrastructure and increasing energy demands globally contribute to the expanding service market. There is a strong interest in understanding the strategic implications of this growth for service providers, original equipment manufacturers (OEMs), and end-users, particularly regarding investment in advanced technologies and long-term partnerships. Furthermore, inquiries often delve into the regional variations in market expansion, seeking insights into which geographical areas are poised for the most significant growth and what factors—such as regulatory environments or industrial development—are influencing these trends. The overall sentiment reflects a strategic focus on capitalizing on the sustained demand for reliable and efficient gas turbine operations.

- Significant Market Expansion: The Gas Turbine Service market is poised for substantial growth, driven by the expanding installed base of turbines and the critical need for their continuous, efficient operation.

- Service-Centric Business Models: There is a clear shift towards comprehensive service offerings and long-term agreements, highlighting a move from transactional sales to enduring service partnerships.

- Technology as a Growth Enabler: Digitalization, AI, and advanced analytics are not just trends but fundamental drivers of service market innovation, improving efficiency and enabling predictive capabilities.

- Decarbonization Impact: Sustainability initiatives are increasingly influencing service demand, with a growing need for upgrades and maintenance supporting lower-carbon and hydrogen-ready solutions.

- Regional Growth Disparities: While global growth is strong, specific regions, particularly emerging economies, are expected to exhibit higher growth rates due to industrialization and infrastructure development.

- Investment in MRO and Modernization: The market forecast underscores continued investment in maintenance, repair, and overhaul (MRO) activities, alongside significant capital expenditure on modernizing existing assets to extend their operational life.

Gas Turbine Service Market Drivers Analysis

The Gas Turbine Service market is primarily propelled by a confluence of factors that underscore the critical need for maintaining and enhancing the performance of gas turbine assets worldwide. A significant driver is the increasing global energy demand, especially in regions undergoing rapid industrialization and urbanization, which necessitates the continuous operation and high availability of power generation assets. This demand places a direct emphasis on robust service support to ensure uninterrupted power supply. Furthermore, the aging infrastructure of existing gas turbine fleets globally creates a sustained requirement for maintenance, repair, and overhaul (MRO) services, as asset owners seek to extend the operational life and efficiency of their investments rather than incur the substantial capital costs of new installations.

Another pivotal driver is the growing emphasis on improving operational efficiency and reducing emissions across various industries. Stricter environmental regulations compel operators to invest in services that optimize fuel consumption, minimize pollutant output, and ensure compliance. This includes upgrades, retrofits, and performance tuning services. The adoption of advanced digital technologies, such as the Industrial Internet of Things (IIoT), artificial intelligence (AI), and machine learning (ML), also acts as a significant catalyst. These technologies enable predictive maintenance, remote monitoring, and data-driven decision-making, leading to enhanced asset reliability and reduced unplanned downtime, thereby driving the demand for specialized digital services and analytics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Gas Turbine Fleet and Asset Life Extension | +1.5% | North America, Europe, Developed Asia Pacific | Long-term (2025-2033) |

| Increasing Global Energy Demand and Power Generation Needs | +1.2% | Asia Pacific (China, India), Middle East & Africa, Latin America | Mid-to-Long Term (2025-2033) |

| Growing Emphasis on Operational Efficiency and Performance Optimization | +1.0% | Global, particularly developed economies | Mid-term (2025-2030) |

| Strict Environmental Regulations and Decarbonization Initiatives | +0.8% | Europe, North America, Japan | Mid-to-Long Term (2025-2033) |

| Technological Advancements in Predictive Maintenance and Digitalization | +0.7% | Global, particularly high-tech industrial regions | Short-to-Mid Term (2025-2030) |

Gas Turbine Service Market Restraints Analysis

Despite its growth potential, the Gas Turbine Service market faces several significant restraints that could temper its expansion. One prominent challenge is the substantial capital expenditure associated with new gas turbine installations and major overhauls. While service contracts provide operational expenditure predictability, the upfront cost of comprehensive maintenance solutions or the decision to replace rather than service an aging asset can be a deterrent, particularly for smaller operators or those facing budget constraints. This high initial investment can lead some clients to opt for minimal or reactive maintenance, thereby limiting the adoption of more advanced and comprehensive service offerings.

Another critical restraint is the fluctuating and volatile prices of natural gas and other fossil fuels. Since gas turbines primarily rely on these fuels, significant price instability can impact the profitability of gas-fired power plants and industrial operations, leading to reduced operational hours or delayed maintenance schedules. This economic uncertainty directly affects the demand for gas turbine services. Furthermore, the accelerating global shift towards renewable energy sources, such as solar and wind power, presents a long-term restraint. As more countries commit to decarbonization and invest heavily in renewable infrastructure, the reliance on gas-fired power generation may gradually decrease, potentially leading to a slower rate of new gas turbine installations and a gradual decline in the overall installed base requiring services in the distant future.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Major Overhauls and Upgrades | -0.9% | Global, particularly emerging markets | Mid-to-Long Term (2025-2033) |

| Volatile Fuel Prices and Economic Uncertainties | -0.8% | Global, especially regions dependent on imported fuels | Short-to-Mid Term (2025-2030) |

| Increasing Shift Towards Renewable Energy Sources | -0.7% | Europe, North America, parts of Asia Pacific | Long-term (2028-2033) |

| Stringent Regulatory Compliance and Permitting Processes | -0.6% | Developed economies with mature environmental regulations | Mid-term (2025-2030) |

| Availability of Skilled Labor and Specialized Expertise | -0.5% | Global, particularly remote or less developed regions | Mid-to-Long Term (2025-2033) |

Gas Turbine Service Market Opportunities Analysis

The Gas Turbine Service market is ripe with opportunities driven by technological advancements, evolving energy landscapes, and the increasing sophistication of asset management strategies. One significant area of opportunity lies in the continued development and adoption of digital solutions, including advanced analytics, AI, machine learning, and digital twin technology. These innovations enable service providers to offer highly predictive, data-driven maintenance, optimizing asset performance, reducing unplanned outages, and extending equipment lifespans. Companies that can effectively integrate and leverage these digital tools will gain a competitive edge and unlock new revenue streams through enhanced service offerings, such as performance as a service or outcome-based contracts.

Another substantial opportunity emerges from the global push towards decarbonization and the transition to cleaner energy sources. As industries explore hydrogen blending, carbon capture, and other sustainable fuel options, there is a growing demand for services related to the modernization and retrofitting of existing gas turbines to accommodate these changes. This includes upgrades for hydrogen-ready capabilities, installation of advanced emission control systems, and specialized maintenance for new fuel types. Furthermore, the expansion of industrial and power generation infrastructure in emerging economies, particularly in Asia Pacific and the Middle East, presents lucrative growth avenues. These regions require comprehensive service support for their rapidly growing installed bases, covering everything from initial commissioning and installation to long-term operational maintenance and performance upgrades, often through bundled long-term service agreements that offer significant value.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Digitalization, AI, and Predictive Analytics | +1.3% | Global, especially technologically advanced markets | Mid-to-Long Term (2025-2033) |

| Growth in Emerging Economies and Industrialization | +1.1% | Asia Pacific (India, Southeast Asia), Middle East, Africa, Latin America | Long-term (2025-2033) |

| Modernization and Retrofit for Hydrogen-Ready and Low-Carbon Solutions | +1.0% | Europe, North America, Japan | Mid-to-Long Term (2026-2033) |

| Expansion of Long-Term Service Agreements (LTSA) | +0.9% | Global, across all end-use sectors | Mid-term (2025-2030) |

| Development of Advanced Diagnostics and Remote Monitoring Services | +0.8% | Global, particularly in remote and critical infrastructure sites | Short-to-Mid Term (2025-2030) |

Gas Turbine Service Market Challenges Impact Analysis

The Gas Turbine Service market, despite its growth, contends with several notable challenges that require strategic navigation by market participants. One significant hurdle is the persistent shortage of highly skilled technical personnel and specialized engineers capable of performing complex maintenance, troubleshooting, and upgrade tasks on advanced gas turbine systems. This scarcity of expertise can lead to increased labor costs, delays in service delivery, and potential compromises in service quality, particularly in remote or rapidly developing regions. Companies must invest heavily in training and talent retention programs to mitigate this challenge and ensure a steady supply of qualified professionals.

Another critical challenge involves the complexities and vulnerabilities within the global supply chain for gas turbine components and spare parts. Geopolitical tensions, trade disputes, and unforeseen global events can disrupt the availability and increase the cost of essential parts, leading to extended repair times and higher operational expenses for both service providers and end-users. Ensuring supply chain resilience through diversification and regional sourcing strategies becomes paramount. Additionally, the increasing stringency of environmental regulations and the need for continuous compliance pose ongoing challenges. Adapting service offerings to meet evolving emissions standards, noise restrictions, and waste disposal regulations requires continuous research, development, and investment in compliant technologies and practices, adding layers of complexity to service delivery.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Technicians and Specialized Workforce | -0.8% | Global, prominent in emerging and remote regions | Long-term (2025-2033) |

| Supply Chain Disruptions and Volatility of Component Costs | -0.7% | Global, particularly vulnerable to geopolitical events | Short-to-Mid Term (2025-2030) |

| Intense Competition from OEM and Independent Service Providers (ISPs) | -0.6% | Global, more pronounced in mature markets | Mid-to-Long Term (2025-2033) |

| High Research & Development Costs for Advanced Service Technologies | -0.5% | Global, for companies aiming for technological leadership | Mid-term (2025-2030) |

| Cybersecurity Risks Associated with Connected Turbine Systems | -0.4% | Global, critical infrastructure sectors | Ongoing (2025-2033) |

Gas Turbine Service Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Gas Turbine Service Market, providing a detailed analysis of its size, historical performance, and future growth projections from 2025 to 2033. It meticulously examines key market trends, significant drivers, inherent restraints, emerging opportunities, and prevailing challenges shaping the industry landscape. The scope includes an in-depth segmentation analysis across various parameters such as service type, turbine type, end-use application, and capacity, offering granular insights into market behavior. Furthermore, the report provides a thorough regional breakdown, highlighting key country-level developments and growth prospects, alongside profiles of major market players to offer a holistic view of the competitive environment. Special attention is given to the impact of digitalization, AI, and sustainability initiatives on service demand.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 22.5 billion |

| Market Forecast in 2033 | USD 35.7 billion |

| Growth Rate | 5.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | General Power Solutions, Industrial Turbine Services, Global Energy Maintenance, Premier Turbine Solutions, Advanced Power Service, Dynamic Turbine Support, TurbineCare International, OmniPower Services, Nexus Energy Solutions, Optimal Turbine Group, Horizon Power Maintenance, Elite Turbine Management, Apex Energy Services, Prime Turbine Repair, Synergy Power Systems, Vanguard Turbine Services, Sterling Turbine Solutions, Sentinel Energy Services, Integral Turbine Care, Future Power Maintenance |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Gas Turbine Service market is extensively segmented to provide a granular view of its diverse operational landscape and varying demand patterns across different applications and turbine types. This segmentation is crucial for understanding specific market niches, identifying high-growth areas, and tailoring service offerings to meet precise industry requirements. The primary segmentation categories include service type, which distinguishes between routine maintenance, complex repairs, full overhauls, and specialized field services. Turbine type differentiates between heavy-duty and aeroderivative models, each requiring unique service approaches due to their distinct design and operational characteristics. End-use segmentation provides insights into the varying service demands from the power generation, oil and gas, and diverse industrial sectors, reflecting their operational priorities and regulatory environments. Additionally, segmentation by capacity highlights service needs across different power output ranges, from smaller industrial turbines to large utility-scale units, influencing service complexity and contract values.

- By Service Type:

- Maintenance: Encompasses routine inspections, preventive care, and scheduled checks to ensure continuous operation and prevent breakdowns.

- Planned Maintenance: Pre-scheduled service activities based on operational hours or calendar intervals to optimize performance and extend asset life.

- Unplanned Maintenance: Reactive services addressing unexpected failures or emergency repairs, often critical for minimizing downtime.

- Repair: Specific corrective actions to fix malfunctioning or damaged components, restoring functionality.

- Overhaul: Comprehensive dismantling, inspection, repair, and reassembly of major turbine components to return them to a like-new condition.

- Installation & Commissioning: Services related to the setup, testing, and operational handover of new gas turbines.

- Field Services: On-site support, troubleshooting, and minor repairs performed directly at the client's location.

- Consulting & Training: Expert advice on turbine operations, maintenance strategies, and training programs for client personnel.

- By Turbine Type:

- Heavy Duty Gas Turbines: Larger, more robust turbines typically used for continuous power generation and industrial applications, known for durability and long operational hours.

- Aeroderivative Gas Turbines: Lighter, more flexible turbines derived from aircraft engines, often used for peak power generation, mechanical drive, and offshore applications due to their quick startup and shutdown capabilities.

- By End-Use:

- Power Generation:

- Utilities: Large-scale power providers requiring consistent and reliable service for their extensive turbine fleets.

- Independent Power Producers (IPPs): Private entities generating power for sale to grids or direct consumers, focused on efficiency and uptime.

- Oil & Gas:

- Upstream: Services for turbines used in exploration and production, including drilling and wellhead operations.

- Midstream: Support for turbines in pipelines, compression stations, and liquefied natural gas (LNG) terminals.

- Downstream: Maintenance for turbines in refineries and petrochemical plants.

- Industrial:

- Chemicals: Service for turbines used in chemical processing plants for power and heat.

- Manufacturing: Support for turbines in various manufacturing facilities providing power or mechanical drive.

- Metals: Maintenance for turbines in steel mills and other metal production facilities.

- Pulp & Paper: Services for turbines providing power and steam in pulp and paper mills.

- Data Centers: Critical service for turbines providing reliable backup or primary power for data infrastructure.

- Marine: Maintenance and overhaul for gas turbines used in naval vessels and commercial ships for propulsion and auxiliary power.

- Power Generation:

- By Capacity:

- Up to 40 MW: Typically smaller industrial or aeroderivative turbines used for distributed power or mechanical drive.

- 40-120 MW: Mid-range turbines often found in industrial cogeneration plants or smaller utility applications.

- 120-300 MW: Medium-to-large utility-scale turbines for base load or peaker power generation.

- Above 300 MW: Very large, heavy-duty turbines primarily used in large-scale combined cycle power plants.

Regional Highlights

- North America: The market in North America is characterized by a mature installed base of gas turbines, leading to a strong demand for MRO services and life extension programs. Regulatory frameworks focused on emissions reduction and efficiency improvements drive the adoption of advanced service technologies and upgrades. The region also sees significant investment in digital transformation for asset management, with a high uptake of predictive maintenance and remote monitoring solutions. Key drivers include aging infrastructure and the need for grid stability.

- Europe: Europe is at the forefront of decarbonization efforts, significantly influencing its gas turbine service market. There is a strong emphasis on modernizing existing fleets for hydrogen readiness and reducing carbon emissions, leading to high demand for specialized retrofit and upgrade services. Strict environmental regulations and a move towards greater energy efficiency also fuel the adoption of advanced service contracts. The region's focus on sustainable energy transitions provides unique opportunities for innovative service providers.

- Asia Pacific (APAC): APAC represents the fastest-growing market for gas turbine services, primarily driven by rapid industrialization, increasing energy demand, and significant investments in new power generation capacity. Countries like China, India, and Southeast Asian nations are expanding their industrial and utility sectors, leading to a substantial increase in the installed base of gas turbines. This growth translates into a surging demand for installation, commissioning, and long-term maintenance services. The region also presents opportunities for technology transfer and localized service partnerships.

- Latin America: The Latin American gas turbine service market is influenced by ongoing economic development and infrastructure projects, particularly in countries with robust oil and gas sectors. Demand for services is driven by the operational needs of existing power plants and industrial facilities, coupled with the expansion of new energy projects. Political and economic stability can impact investment, but the long-term need for reliable power and industrial operations sustains service demand.

- Middle East and Africa (MEA): The MEA region is a significant market for gas turbine services, largely due to its substantial oil and gas operations and increasing power generation requirements driven by population growth and urbanization. Countries in the Middle East, with their vast hydrocarbon resources, have a large installed base of gas turbines in both upstream and downstream operations, demanding consistent and reliable service. Africa's emerging economies are investing in power infrastructure, creating new opportunities for installation and maintenance services, often influenced by long-term strategic energy plans.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gas Turbine Service Market.- General Power Solutions

- Industrial Turbine Services

- Global Energy Maintenance

- Premier Turbine Solutions

- Advanced Power Service

- Dynamic Turbine Support

- TurbineCare International

- OmniPower Services

- Nexus Energy Solutions

- Optimal Turbine Group

- Horizon Power Maintenance

- Elite Turbine Management

- Apex Energy Services

- Prime Turbine Repair

- Synergy Power Systems

- Vanguard Turbine Services

- Sterling Turbine Solutions

- Sentinel Energy Services

- Integral Turbine Care

- Future Power Maintenance

Frequently Asked Questions

Analyze common user questions about the Gas Turbine Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Gas Turbine Service market?

The Gas Turbine Service market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching USD 35.7 billion by 2033 from an estimated USD 22.5 billion in 2025.

How is AI impacting Gas Turbine Services?

AI is significantly impacting Gas Turbine Services by enabling advanced predictive maintenance, optimizing operational efficiency, enhancing fault detection and diagnostics, and facilitating remote monitoring, leading to reduced downtime and improved asset performance.

What are the primary drivers for the Gas Turbine Service market?

Key drivers include the aging global fleet of gas turbines necessitating life extension, increasing global energy demand, a strong focus on enhancing operational efficiency, stricter environmental regulations, and the widespread adoption of digitalization and predictive maintenance technologies.

Which regions are showing significant growth in Gas Turbine Services?

Asia Pacific (APAC) is projected to be the fastest-growing region due to rapid industrialization and increasing energy demand. North America and Europe continue to be strong markets driven by modernization and decarbonization initiatives, while the Middle East and Africa show robust demand from oil & gas and power infrastructure development.

What challenges does the Gas Turbine Service market face?

The market faces challenges such as a shortage of skilled technicians, potential disruptions in global supply chains for parts, intense competition among service providers, high capital expenditure for major overhauls, and the complexities associated with complying with evolving environmental regulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted