G CSF and G CSF Biosimilar Market

G CSF and G CSF Biosimilar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710085 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

G CSF and G CSF Biosimilar Market Size

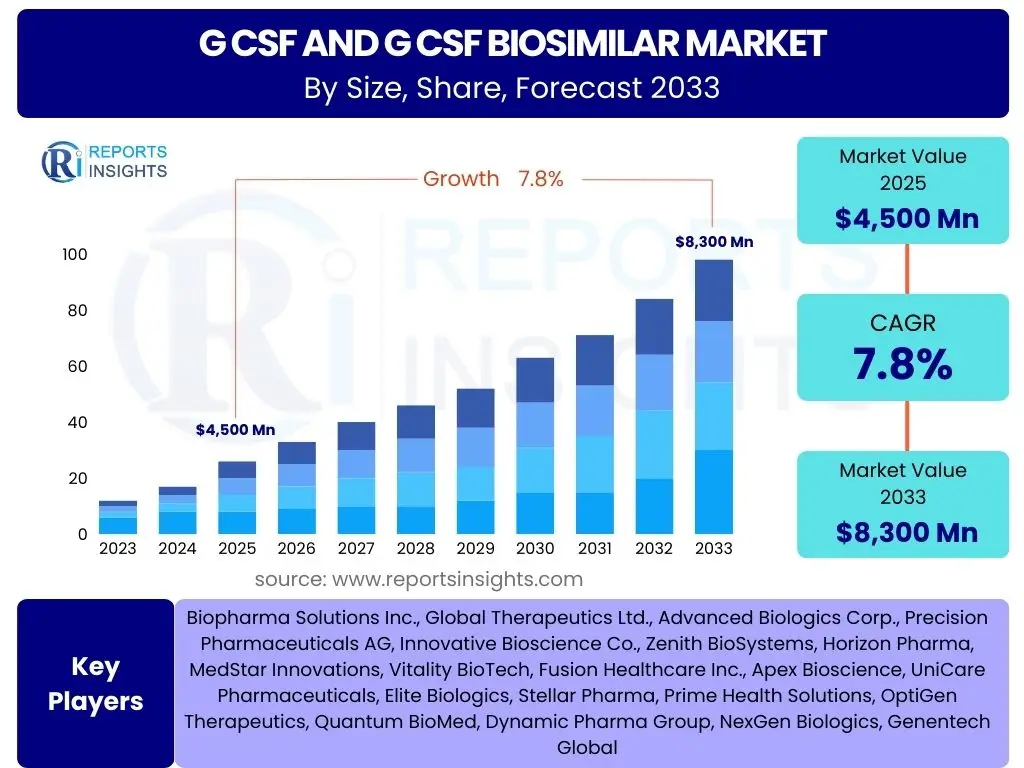

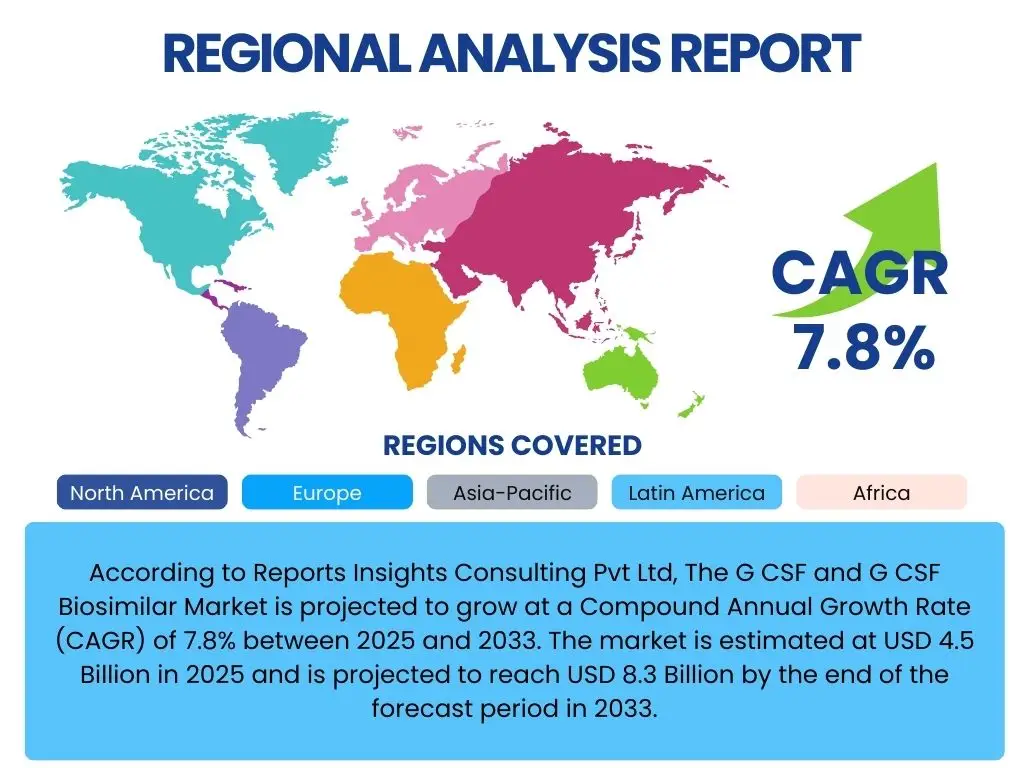

According to Reports Insights Consulting Pvt Ltd, The G CSF and G CSF Biosimilar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 8.3 Billion by the end of the forecast period in 2033.

Key G CSF and G CSF Biosimilar Market Trends & Insights

The G CSF and G CSF biosimilar market is undergoing significant transformation, driven by a confluence of medical, economic, and technological factors. Users frequently inquire about the trajectory of biosimilar adoption, the impact of evolving healthcare policies, and the role of innovation in product development. A primary trend observed is the increasing acceptance and integration of biosimilars into clinical practice, stemming from their cost-effectiveness and demonstrated efficacy, which are crucial for sustainable healthcare systems globally. This shift is particularly pronounced in regions striving to manage escalating healthcare expenditures while maintaining high standards of patient care.

Furthermore, there is a growing emphasis on optimizing treatment regimens and enhancing patient outcomes through personalized medicine approaches, even within established therapeutic areas like G-CSF administration. The expansion of indications for G-CSF therapies, alongside continuous research into new formulations and delivery methods, signals a dynamic market landscape. Stakeholders are keen to understand how regulatory frameworks will adapt to facilitate quicker market entry for biosimilars without compromising safety and quality, thereby encouraging further investment in this competitive sector.

- Increasing adoption of G-CSF biosimilars due to cost-effectiveness.

- Growing prevalence of cancer and associated chemotherapy-induced neutropenia.

- Expansion of G-CSF applications beyond oncology, including stem cell mobilization.

- Favorable regulatory policies promoting biosimilar development and market entry.

- Focus on patient-centric care and convenience through novel drug delivery systems.

AI Impact Analysis on G CSF and G CSF Biosimilar

Common user questions regarding AI's impact on the G CSF and G CSF biosimilar market often center on its potential to revolutionize drug discovery, optimize manufacturing processes, and personalize patient treatment. Artificial intelligence and machine learning algorithms hold significant promise in accelerating the identification of novel drug candidates and optimizing existing G-CSF molecules for improved efficacy or reduced side effects. This involves analyzing vast datasets of biological information to predict protein structures, drug-target interactions, and potential toxicity, thereby streamlining the early stages of drug development and reducing time-to-market.

Moreover, AI can play a crucial role in enhancing the efficiency and cost-effectiveness of biosimilar manufacturing. By optimizing fermentation processes, purification steps, and quality control, AI-driven solutions can lead to higher yields, lower production costs, and improved product consistency, which are critical for competitive pricing in the biosimilar space. In patient care, AI algorithms could assist in predicting individual patient responses to G-CSF therapy, guiding dosage adjustments, and identifying patients at higher risk of neutropenia, thereby enabling more personalized and effective treatment strategies. While the direct impact on G-CSF and its biosimilars is still nascent, the foundational technologies are rapidly advancing towards practical applications across the biopharmaceutical industry.

- Accelerated drug discovery and development for novel G-CSF analogs.

- Optimization of G-CSF biosimilar manufacturing processes for efficiency and cost reduction.

- Enhanced personalized medicine approaches for G-CSF dosing and patient response prediction.

- Improved clinical trial design and patient stratification for G-CSF-related studies.

- Advanced pharmacovigilance and real-world data analysis for G-CSF safety and efficacy monitoring.

Key Takeaways G CSF and G CSF Biosimilar Market Size & Forecast

Users frequently seek concise summaries of the G-CSF and G-CSF biosimilar market's future outlook and critical insights derived from market forecasts. A key takeaway is the robust growth trajectory projected for this market, fueled predominantly by the increasing global cancer incidence and the subsequent demand for supportive care therapies to manage chemotherapy-induced neutropenia. The significant growth rate indicates sustained investment and innovation within the sector, promising expanding accessibility to vital treatments.

Another crucial insight is the growing dominance of biosimilars, which are poised to capture a larger market share due to their affordability and proven efficacy, offering a sustainable solution for healthcare systems globally. This shift is expected to intensify competition, potentially driving down overall costs for patients and providers. Strategic partnerships, regulatory advancements, and technological innovations in drug delivery will be pivotal in shaping the competitive landscape and ensuring continued market expansion through the forecast period.

- Strong market growth anticipated driven by rising cancer rates.

- Biosimilars are key growth drivers, offering cost-effective alternatives.

- Increasing global demand for supportive care in oncology treatments.

- Technological advancements in drug formulation and delivery systems.

- Expansion into emerging markets presents significant growth opportunities.

G CSF and G CSF Biosimilar Market Drivers Analysis

The G-CSF and G-CSF biosimilar market is propelled by several significant factors that underscore its projected growth and strategic importance in global healthcare. A primary driver is the escalating prevalence of cancer worldwide, which directly correlates with an increased number of patients undergoing chemotherapy. Chemotherapy often leads to neutropenia, a severe reduction in white blood cells, necessitating G-CSF administration to stimulate neutrophil production and prevent life-threatening infections. As cancer incidence continues to rise across age groups and regions, the demand for G-CSF therapies naturally expands, forming a foundational driver for market expansion.

Furthermore, the growing adoption and acceptance of biosimilars play a pivotal role in market acceleration. G-CSF biosimilars offer a cost-effective alternative to expensive originator biologics, making essential treatments more accessible to a broader patient population and easing the financial burden on healthcare systems. This affordability is particularly attractive in developing economies and in developed nations striving to optimize healthcare spending. Favorable regulatory pathways established by agencies such as the FDA and EMA for biosimilar approval also encourage manufacturers to invest in this segment, facilitating quicker market entry and fostering competition.

Technological advancements in drug manufacturing and formulation, along with an expanding scope of applications for G-CSF beyond oncology, also contribute significantly. Innovations in drug delivery systems, such as longer-acting formulations, improve patient compliance and convenience. Additionally, the use of G-CSF in stem cell mobilization for transplantation, severe chronic neutropenia, and other immunodeficiency disorders diversifies its market base, solidifying its position as a critical therapeutic agent.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Cancer Incidence & Chemotherapy Use | +2.5% | Global, particularly Asia Pacific, North America | Long-term (2025-2033) |

| Increasing Adoption of Biosimilars | +2.0% | Europe, North America, Emerging Markets | Mid to Long-term (2025-2033) |

| Favorable Regulatory Policies for Biosimilars | +1.5% | Global, particularly U.S., EU, Japan | Mid-term (2025-2030) |

| Expanding Applications of G-CSF | +1.0% | North America, Europe, Asia Pacific | Long-term (2028-2033) |

| Growing Healthcare Expenditure & Access | +0.8% | Emerging Markets (China, India, Brazil) | Long-term (2025-2033) |

G CSF and G CSF Biosimilar Market Restraints Analysis

Despite its robust growth prospects, the G-CSF and G-CSF biosimilar market faces several significant restraints that could impede its full potential. A primary challenge is the high cost associated with the research, development, and manufacturing of biologics and biosimilars. Developing a biosimilar requires extensive clinical trials to demonstrate comparability in terms of safety, efficacy, and quality to the originator product. These rigorous processes, coupled with the need for specialized manufacturing facilities and highly skilled personnel, translate into substantial upfront investments, which can be a barrier for smaller companies and slow down market entry.

Moreover, skepticism among healthcare providers and patients regarding the interchangeability and long-term efficacy of biosimilars, despite regulatory assurances, presents a notable restraint. Physicians may hesitate to switch stable patients from an originator biologic to a biosimilar due to concerns about potential immunogenicity or subtle differences in clinical outcomes. Overcoming this perception requires continuous education, robust post-marketing surveillance data, and sustained efforts from regulatory bodies and manufacturers to build trust and confidence in biosimilar products.

Furthermore, the complex intellectual property landscape and patent litigation surrounding originator biologics and their biosimilar counterparts can create significant delays and legal costs. Patent battles can restrict market entry for biosimilars, prolonging the market exclusivity of innovator products and hindering cost-saving opportunities. Additionally, pricing pressures from healthcare payers and intense competition among biosimilar manufacturers, while beneficial for cost reduction, can erode profit margins and reduce incentives for future innovation in the long term.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Manufacturing Costs | -1.5% | Global | Long-term (2025-2033) |

| Physician & Patient Skepticism towards Biosimilars | -1.0% | North America, Europe | Mid-term (2025-2030) |

| Complex Intellectual Property & Patent Landscape | -0.8% | U.S., Europe | Short to Mid-term (2025-2028) |

| Intense Pricing Pressure & Competition | -0.7% | Global | Mid to Long-term (2025-2033) |

| Strict Regulatory Requirements & Approval Timelines | -0.5% | Global | Short to Mid-term (2025-2028) |

G CSF and G CSF Biosimilar Market Opportunities Analysis

Despite existing restraints, the G-CSF and G-CSF biosimilar market is characterized by numerous opportunities that can significantly accelerate its growth. One of the most promising avenues lies in the untapped potential of emerging markets. Regions such as Asia Pacific, Latin America, and the Middle East & Africa are experiencing a rapid increase in cancer incidence, coupled with improving healthcare infrastructure and growing disposable incomes. These markets often face significant challenges in affording high-cost originator biologics, making cost-effective biosimilars highly attractive and creating a vast, underserved patient population for G-CSF therapies. Strategic entry and localized distribution in these regions can unlock substantial growth.

Another key opportunity stems from the development of novel indications and therapeutic areas for G-CSF. While oncology applications remain dominant, ongoing research explores G-CSF's potential in treating various other conditions, including certain infectious diseases, inflammatory disorders, and even neurological conditions, though these are largely in early stages of investigation. Expanding the clinical utility of G-CSF beyond its traditional roles could significantly broaden its market base and provide new revenue streams for manufacturers. Continued investment in research and development to explore these new applications will be crucial for capturing these opportunities.

Furthermore, advancements in manufacturing technologies, such as continuous manufacturing and single-use bioreactors, offer opportunities to reduce production costs and improve efficiency for biosimilar developers. These technological innovations can streamline processes, reduce contamination risks, and accelerate batch turnaround times, making biosimilar production more agile and cost-effective. Strategic collaborations and partnerships between biosimilar manufacturers, research institutions, and distribution networks also present avenues for market expansion, allowing companies to leverage complementary expertise and market access to accelerate product commercialization and penetrate new geographical segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Emerging Markets (Asia Pacific, Latin America) | +2.0% | China, India, Brazil, Southeast Asia | Long-term (2026-2033) |

| Development of Novel G-CSF Indications | +1.2% | Global (Research-intensive regions) | Long-term (2028-2033) |

| Advancements in Biosimilar Manufacturing Technology | +1.0% | Global | Mid to Long-term (2025-2033) |

| Strategic Collaborations & Partnerships | +0.9% | Global | Mid-term (2025-2030) |

| Government Initiatives to Promote Biosimilar Adoption | +0.7% | Europe, Canada, Japan | Short to Mid-term (2025-2028) |

G CSF and G CSF Biosimilar Market Challenges Impact Analysis

The G-CSF and G-CSF biosimilar market, despite its growth, must navigate several persistent challenges that could influence its trajectory. One significant challenge is the ongoing pricing pressure and intense competition within the biosimilar segment. As more biosimilars enter the market following the expiration of originator patents, price erosion becomes inevitable. While beneficial for healthcare systems and patients, this can significantly impact the profitability of manufacturers, potentially reducing the incentive for future investment in research and development for new biosimilar versions or novel G-CSF therapies. Maintaining a balance between market share and sustainable pricing is a constant struggle.

Another critical challenge involves the complexities of the supply chain and manufacturing scalability. Producing biologics and biosimilars requires highly specialized facilities, stringent quality control, and robust logistics to ensure product integrity from manufacturing to patient administration. Any disruption in the supply chain, such as raw material shortages, manufacturing delays, or distribution bottlenecks, can lead to product unavailability, impacting patient care and market reputation. Ensuring consistent, high-quality supply at a global scale remains a complex operational hurdle, particularly for products with high demand.

Furthermore, evolving regulatory landscapes and varying guidelines across different countries present a compliance challenge for global manufacturers. While harmonization efforts are underway, significant differences in data requirements, approval processes, and post-marketing surveillance exist, demanding tailored strategies for each market. This regulatory fragmentation can increase the time and cost associated with global market entry. Finally, the threat of emerging novel therapies or alternative treatments that might reduce the reliance on G-CSF, though currently limited, poses a long-term strategic challenge that requires continuous monitoring and adaptation from market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Erosion & Competition | -1.8% | Global | Long-term (2025-2033) |

| Supply Chain Vulnerabilities & Manufacturing Scalability | -1.0% | Global | Mid-term (2025-2030) |

| Evolving & Divergent Regulatory Landscape | -0.8% | Global (especially emerging vs. developed markets) | Mid-term (2025-2030) |

| Intellectual Property Disputes & Litigation | -0.7% | U.S., Europe | Short to Mid-term (2025-2028) |

| Development of Alternative & Novel Therapies | -0.5% | Global | Long-term (2030-2033) |

G CSF and G CSF Biosimilar Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the G-CSF and G-CSF Biosimilar market, covering its historical performance, current dynamics, and future projections. The scope encompasses detailed segmentation by product type, application, and distribution channel, providing granular insights into market trends, drivers, restraints, opportunities, and challenges. It also includes a thorough regional analysis and profiles of key industry players to offer a holistic understanding of the market landscape and strategic implications for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | $4,500 Million |

| Market Forecast in 2033 | $8,300 Million |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Biopharma Solutions Inc., Global Therapeutics Ltd., Advanced Biologics Corp., Precision Pharmaceuticals AG, Innovative Bioscience Co., Zenith BioSystems, Horizon Pharma, MedStar Innovations, Vitality BioTech, Fusion Healthcare Inc., Apex Bioscience, UniCare Pharmaceuticals, Elite Biologics, Stellar Pharma, Prime Health Solutions, OptiGen Therapeutics, Quantum BioMed, Dynamic Pharma Group, NexGen Biologics, Genentech Global |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The G-CSF and G-CSF biosimilar market is meticulously segmented to provide granular insights into its diverse components and understand the varied dynamics across different product types, applications, and distribution channels. This segmentation allows for a detailed assessment of market share, growth potential, and competitive intensity within each category, enabling stakeholders to identify specific areas of opportunity and risk. Understanding these segments is crucial for strategic planning, product development, and market entry strategies, as each segment responds to unique market drivers and faces distinct challenges.

The market is broadly categorized into biologics and biosimilars, reflecting the shift towards more affordable therapeutic options. Further breakdown by application highlights the critical role of G-CSF in oncology, particularly for managing chemotherapy-induced neutropenia, alongside its growing importance in stem cell mobilization and the treatment of chronic neutropenia. Distribution channels also delineate market access and penetration strategies, influencing pricing and availability across healthcare settings. This comprehensive segmentation is foundational for a nuanced market understanding.

- By Product Type:

- G-CSF Biologics (Filgrastim, Pegfilgrastim, Lenograstim, Lipegfilgrastim)

- G-CSF Biosimilars (Filgrastim Biosimilars, Pegfilgrastim Biosimilars, Lenograstim Biosimilars)

- By Application:

- Oncology (Chemotherapy-Induced Neutropenia, Myelodysplastic Syndromes)

- Stem Cell Mobilization

- Chronic Neutropenia

- Other Applications

- By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East & Africa (MEA)

Regional Highlights

The global G-CSF and G-CSF biosimilar market exhibits distinct regional dynamics, influenced by varying healthcare infrastructures, regulatory environments, disease prevalence, and economic factors. Each region presents unique opportunities and challenges that shape its contribution to the overall market growth.

- North America: This region holds a significant market share due to its advanced healthcare infrastructure, high cancer incidence, and robust reimbursement policies. The U.S. remains a dominant market, driven by substantial R&D investments, a strong presence of key market players, and a well-established regulatory framework for biosimilar adoption. Canada also contributes to growth with increasing biosimilar uptake initiatives.

- Europe: Europe represents a mature market with a strong emphasis on biosimilar adoption to manage healthcare costs. Countries like Germany, France, and the UK have been at the forefront of biosimilar integration, benefiting from supportive regulatory pathways from the European Medicines Agency (EMA). The region experiences steady growth, bolstered by an aging population and high prevalence of chronic diseases requiring G-CSF therapies.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by the increasing incidence of cancer, improving healthcare access, and rising healthcare expenditure, particularly in populous countries like China and India. The growing awareness of biosimilars, coupled with government initiatives to promote their use for affordability, makes this region a high-potential market. Japan and South Korea also contribute significantly with their advanced biopharmaceutical sectors.

- Latin America: This region is an emerging market for G-CSF and biosimilars, characterized by improving healthcare infrastructure and an increasing focus on expanding access to affordable treatments. Countries like Brazil and Argentina are experiencing growth due to rising cancer rates and government efforts to include biosimilars in public health programs, although economic instability can sometimes pose a challenge.

- Middle East & Africa (MEA): The MEA region is witnessing gradual growth, primarily fueled by increasing healthcare investments and a growing understanding of biosimilars. Saudi Arabia and the UAE are leading the adoption due to their developed healthcare systems and willingness to invest in advanced medical treatments, including supportive care for oncology patients. However, market penetration remains lower in less developed parts of Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the G CSF and G CSF Biosimilar Market.- Biopharma Solutions Inc.

- Global Therapeutics Ltd.

- Advanced Biologics Corp.

- Precision Pharmaceuticals AG

- Innovative Bioscience Co.

- Zenith BioSystems

- Horizon Pharma

- MedStar Innovations

- Vitality BioTech

- Fusion Healthcare Inc.

- Apex Bioscience

- UniCare Pharmaceuticals

- Elite Biologics

- Stellar Pharma

- Prime Health Solutions

- OptiGen Therapeutics

- Quantum BioMed

- Dynamic Pharma Group

- NexGen Biologics

- Genentech Global

Frequently Asked Questions

Analyze common user questions about the G CSF and G CSF Biosimilar market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is G-CSF and how does it work?

Granulocyte Colony-Stimulating Factor (G-CSF) is a naturally occurring protein that stimulates the bone marrow to produce white blood cells, specifically neutrophils. These neutrophils are crucial for fighting infection. G-CSF therapies are primarily used to prevent or treat neutropenia, a condition characterized by low neutrophil counts, often caused by chemotherapy, stem cell transplantation, or chronic conditions, thereby reducing the risk of serious infections in patients.

What are G-CSF biosimilars and why are they important?

G-CSF biosimilars are highly similar versions of an approved G-CSF originator biologic, with no clinically meaningful differences in terms of safety, purity, and potency. They are important because they offer a more affordable alternative to the original biologic, increasing patient access to essential treatment while reducing healthcare costs. Biosimilars promote market competition and can alleviate the financial burden on healthcare systems and individual patients.

How large is the G-CSF and G-CSF biosimilar market?

The G-CSF and G-CSF biosimilar market is substantial and projected for robust growth. It is estimated at USD 4.5 Billion in 2025 and is forecasted to reach USD 8.3 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 7.8%. This growth is driven by the increasing prevalence of cancer, expanding applications for G-CSF, and the rising adoption of cost-effective biosimilar options globally.

What are the main applications of G-CSF therapies?

The primary application of G-CSF therapies is in oncology, specifically for the prevention and treatment of chemotherapy-induced neutropenia (CIN) in cancer patients, which helps reduce the risk of febrile neutropenia and associated complications. Other significant applications include mobilization of hematopoietic stem cells for autologous or allogeneic transplantation, and treatment of severe chronic neutropenia, which can be congenital, idiopathic, or cyclic in nature.

What are the future trends in the G-CSF and G-CSF biosimilar market?

Future trends include sustained growth in biosimilar adoption due to cost pressures and increased access, further expansion of G-CSF applications into new therapeutic areas, and advancements in drug delivery systems such as longer-acting or more convenient formulations. There will also be a continued focus on market penetration in emerging economies and strategic collaborations among pharmaceutical companies to enhance research, development, and distribution capabilities. Regulatory support for biosimilars will also remain a key trend.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted