Fuel Cell Market

Fuel Cell Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708492 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Fuel Cell Market Size

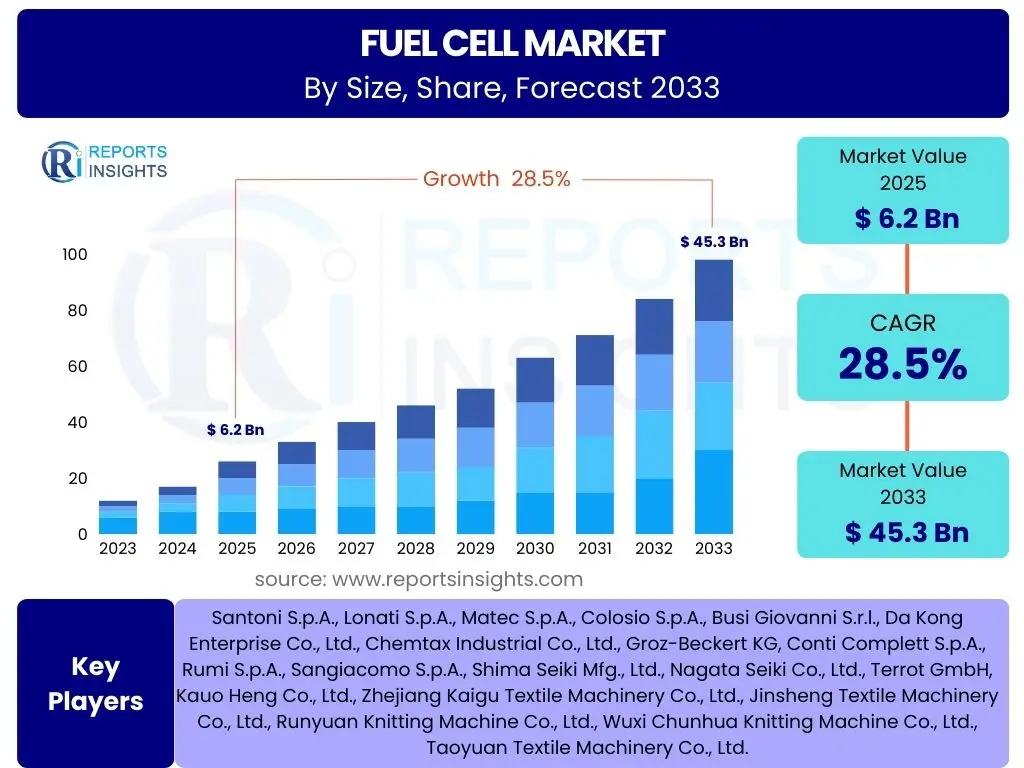

According to Reports Insights Consulting Pvt Ltd, The Fuel Cell Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 45.3 Billion by the end of the forecast period in 2033.

The substantial growth in the fuel cell market is driven by increasing global emphasis on sustainable energy solutions and the imperative to reduce carbon emissions across various sectors. Fuel cell technology offers a clean, efficient alternative to traditional fossil fuel combustion, generating electricity through electrochemical reactions without combustion, primarily producing water as a byproduct. This inherent environmental advantage positions fuel cells as a critical component in the transition towards a low-carbon economy, attracting significant investment and policy support worldwide.

Furthermore, the expanding applications of fuel cells, from powering passenger vehicles and heavy-duty transportation to providing stationary power for industrial facilities and residential areas, are contributing to its accelerated market expansion. Advancements in material science and manufacturing processes are continuously improving the efficiency, durability, and cost-effectiveness of fuel cell systems, making them increasingly competitive with conventional energy sources. As the infrastructure for hydrogen production, storage, and distribution matures, the economic viability and widespread adoption of fuel cell technology are expected to further propel this market's impressive growth trajectory.

Key Fuel Cell Market Trends & Insights

The fuel cell market is currently experiencing dynamic shifts driven by technological innovation, evolving regulatory landscapes, and increasing public and private sector investment in clean energy. Key trends reveal a strong emphasis on enhancing fuel cell efficiency and durability, alongside efforts to scale up manufacturing for cost reduction. There is a noticeable push towards hydrogen infrastructure development, which is critical for the widespread adoption of fuel cell electric vehicles (FCEVs) and stationary power systems. Furthermore, market players are increasingly focusing on diversification of fuel cell types and applications, exploring solutions for marine, aviation, and heavy-duty transportation sectors, beyond the traditional automotive and stationary power segments.

Another significant insight points to the growing integration of fuel cells into hybrid power systems, combining with batteries or other renewable energy sources to offer more resilient and optimized energy solutions. This hybridization enhances performance and addresses intermittency challenges, particularly in grid-tied and off-grid applications. The development of advanced catalysts and membrane materials continues to be a priority, aimed at reducing reliance on expensive rare earth metals and improving operational lifespans. Policy incentives and government mandates for zero-emission vehicles and clean power generation are also playing a crucial role in shaping market direction, fostering innovation and accelerating market penetration globally.

- Advancements in hydrogen production, storage, and distribution infrastructure.

- Increasing adoption of fuel cell electric vehicles (FCEVs) in passenger and commercial segments.

- Growing deployment of stationary fuel cells for backup power, combined heat and power (CHP), and primary power generation.

- Development of fuel cells for heavy-duty transportation, marine, and aviation applications.

- Integration of artificial intelligence (AI) and machine learning (ML) for optimized fuel cell performance and predictive maintenance.

- Focus on solid oxide fuel cell (SOFC) technology for high-temperature industrial applications and large-scale power generation.

- Diversification of fuel cell types to reduce dependence on specific fuels and broaden application scope.

AI Impact Analysis on Fuel Cell

Artificial Intelligence (AI) is poised to significantly transform the fuel cell industry by optimizing various stages of the value chain, from materials discovery and system design to operational efficiency and predictive maintenance. Users frequently inquire about how AI can accelerate the development of new fuel cell materials, improve diagnostic capabilities, and extend the lifespan of fuel cell stacks. AI-driven simulations and data analytics can dramatically reduce the time and cost associated with research and development, enabling rapid screening of novel catalysts, electrolytes, and membrane materials to identify optimal compositions and structures for enhanced performance and durability.

In operational contexts, AI algorithms are being deployed to monitor fuel cell system health in real-time, predict potential failures, and optimize energy management strategies for improved efficiency and reliability. This includes intelligent control systems that adapt to varying load demands and environmental conditions, ensuring peak performance and minimizing energy waste. Furthermore, AI contributes to the design of more compact and efficient fuel cell systems by analyzing complex thermodynamic and electrochemical interactions, allowing for predictive modeling that identifies ideal operating parameters and configurations. The integration of AI also supports the development of smart manufacturing processes for fuel cell components, enabling higher precision, quality control, and automation, thereby driving down production costs and accelerating market adoption.

- Accelerated discovery and development of advanced fuel cell materials (catalysts, membranes, electrolytes) through AI-driven simulations and machine learning.

- Optimization of fuel cell system design and performance parameters, leading to higher efficiency and power density.

- Real-time monitoring and predictive maintenance of fuel cell stacks and systems, enhancing reliability and extending operational lifespan.

- Improved energy management and load balancing in hybrid fuel cell systems and smart grids.

- Enhanced quality control and automation in fuel cell manufacturing processes, reducing production costs.

- Intelligent fault diagnosis and anomaly detection, minimizing downtime and maintenance expenses.

- Data-driven insights for hydrogen infrastructure planning and optimization.

Key Takeaways Fuel Cell Market Size & Forecast

The Fuel Cell Market is on the cusp of significant expansion, presenting substantial opportunities for innovation and investment across various sectors. A primary takeaway is the compelling growth trajectory, with projections indicating a robust Compound Annual Growth Rate (CAGR) and a multi-fold increase in market valuation by 2033. This growth is fundamentally underpinned by the global decarbonization agenda, intensifying governmental support through policy incentives, and rapid technological advancements that are improving the efficiency, durability, and cost-effectiveness of fuel cell systems. Stakeholders should recognize the critical role of hydrogen infrastructure development as a prerequisite for unlocking the full market potential, particularly in transportation and large-scale stationary power applications.

Another crucial insight is the increasing diversification of fuel cell applications beyond traditional automotive uses, with burgeoning demand in heavy-duty vehicles, marine, rail, aviation, and critical backup power for data centers and telecommunications. This broadens the market's resilience and reduces dependence on any single end-use sector. Furthermore, the integration of artificial intelligence and advanced analytics is emerging as a powerful enabler, promising to revolutionize fuel cell material science, system optimization, and predictive maintenance. Companies prioritizing these technological integrations are likely to gain a competitive edge. The market forecast underscores a clear imperative for sustained investment in research and development, strategic partnerships for infrastructure build-out, and the cultivation of a skilled workforce to capitalize on the profound transformation fuel cells are bringing to the global energy landscape.

- The Fuel Cell Market is projected for substantial growth, reaching USD 45.3 Billion by 2033, driven by sustainable energy mandates.

- Government policies and incentives for clean energy are critical drivers for market acceleration.

- Technological advancements are continuously improving fuel cell efficiency, durability, and cost-effectiveness.

- Diversification of applications, including heavy-duty transportation and critical infrastructure, is a key growth area.

- Hydrogen infrastructure development remains pivotal for widespread adoption and market expansion.

- Integration of AI and machine learning will be crucial for optimizing performance, extending lifespan, and reducing R&D costs.

Fuel Cell Market Drivers Analysis

The accelerating global imperative to mitigate climate change and reduce carbon emissions stands as a paramount driver for the fuel cell market. Governments and international bodies are enacting stringent emission regulations and setting ambitious renewable energy targets, compelling industries and consumers alike to seek cleaner energy alternatives. Fuel cells, with their zero-emission or near-zero-emission operation, particularly when powered by green hydrogen, offer an attractive solution that aligns perfectly with these environmental objectives. This regulatory push, combined with increasing public awareness and demand for sustainable technologies, creates a favorable market environment for fuel cell adoption across various applications, from transportation to stationary power generation.

Technological advancements and economies of scale are also significantly propelling market growth. Continuous research and development efforts are leading to improvements in fuel cell performance, durability, and energy density, while simultaneously driving down manufacturing costs. Innovations in catalyst materials, membrane technologies, and stack designs are making fuel cell systems more efficient and competitive with conventional power sources. As production volumes increase, the associated manufacturing costs are expected to decline further, enhancing the economic viability of fuel cell solutions and making them more accessible for broader commercial and industrial deployment. This cycle of innovation and cost reduction is crucial for overcoming initial market barriers and accelerating widespread adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for clean energy and decarbonization goals | +7.5% | Global, especially EU, North America, APAC (China, Japan, South Korea) | Long-term (2025-2033) |

| Supportive government policies, subsidies, and incentives for fuel cells and hydrogen infrastructure | +6.8% | Germany, Japan, South Korea, California (USA), UK, Australia | Mid to Long-term (2025-2033) |

| Technological advancements leading to improved efficiency and reduced costs | +5.2% | Global | Mid to Long-term (2025-2033) |

| Increasing adoption in automotive (FCEVs) and heavy-duty transportation | +4.9% | Japan, South Korea, China, Germany, USA | Mid-term (2025-2030) |

| Rising demand for reliable backup and primary power solutions in data centers and telecom | +4.1% | North America, Europe, APAC | Short to Mid-term (2025-2028) |

Fuel Cell Market Restraints Analysis

Despite the promising growth trajectory, the fuel cell market faces significant restraints, primarily stemming from the high initial capital expenditure required for both fuel cell systems and the associated hydrogen infrastructure. The cost of manufacturing fuel cell stacks, particularly those utilizing precious metals like platinum as catalysts, remains a considerable barrier for widespread commercial adoption. This high upfront cost, coupled with the need for specialized materials and complex manufacturing processes, makes fuel cells less competitive in certain applications compared to established energy technologies. For end-users, the substantial initial investment often outweighs the long-term operational savings, particularly without adequate governmental subsidies or incentives.

Furthermore, the nascent state of hydrogen production, storage, and distribution infrastructure presents a critical bottleneck. The lack of readily available, affordable, and widespread green hydrogen refueling stations limits the practical deployment of fuel cell electric vehicles and impedes the scalability of stationary power solutions. While progress is being made in this area, the build-out of a comprehensive hydrogen ecosystem requires massive investments and coordinated efforts across industries and governments, which takes considerable time. Additionally, public perception and lack of awareness regarding fuel cell technology, along with safety concerns associated with hydrogen handling, contribute to slower market penetration and hinder consumer acceptance.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial cost of fuel cell systems and hydrogen infrastructure | -4.5% | Global | Mid-term (2025-2030) |

| Limited hydrogen refueling infrastructure and production capacity | -3.8% | Global, less impactful in early adopter regions like Japan, South Korea | Mid to Long-term (2025-2033) |

| Storage and safety concerns associated with hydrogen fuel | -2.1% | Global | Long-term (2025-2033) |

| Competition from other advanced battery technologies (e.g., Li-ion, solid-state batteries) | -1.7% | Global, especially automotive sector | Short to Mid-term (2025-2028) |

Fuel Cell Market Opportunities Analysis

The expanding interest in green hydrogen production presents a monumental opportunity for the fuel cell market. As renewable energy sources become more prevalent, the potential to generate hydrogen through electrolysis powered by wind, solar, or hydropower offers a truly clean fuel pathway for fuel cells. This transition towards green hydrogen not only enhances the environmental credentials of fuel cell technology but also addresses concerns regarding the carbon footprint of hydrogen derived from fossil fuels. Significant investments in renewable hydrogen projects globally are expected to lower production costs and increase availability, thereby bolstering the economic viability and scalability of fuel cell applications across various sectors.

Furthermore, the diversification of fuel cell applications into new and underserved markets represents another key growth opportunity. Beyond passenger vehicles and stationary power, there is burgeoning demand for fuel cell solutions in heavy-duty transportation (trucks, buses), marine vessels, rail, and even aviation, where battery-electric solutions face limitations due to weight and range requirements. Portable fuel cells for consumer electronics, military equipment, and remote sensors also offer niche but significant market segments. The growing need for resilient and off-grid power solutions in emerging economies, coupled with the increasing adoption of microgrids, further opens avenues for fuel cell deployment. These varied applications not only expand the total addressable market but also foster innovation and customization of fuel cell technologies to meet diverse operational demands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of green hydrogen production and infrastructure | +6.2% | Global, particularly in regions with abundant renewable resources (e.g., Australia, Chile, Middle East, North Africa, EU) | Long-term (2027-2033) |

| Expansion into new applications: marine, rail, aviation, and heavy-duty vehicles | +5.5% | Global, particularly Europe and APAC for marine/heavy-duty | Mid to Long-term (2026-2033) |

| Integration with renewable energy systems and smart grids for hybrid power solutions | +4.8% | North America, Europe, APAC | Mid-term (2025-2030) |

| Emerging markets and off-grid power solutions in developing regions | +3.9% | Africa, Southeast Asia, Latin America | Long-term (2028-2033) |

Fuel Cell Market Challenges Impact Analysis

One of the primary challenges facing the fuel cell market is the significant cost of hydrogen production and storage. While green hydrogen offers an environmentally superior option, its current production methods, largely through electrolysis, are energy-intensive and can be expensive without sufficient access to cheap renewable electricity. The cost of compressing or liquefying hydrogen for storage and transport also adds to the overall expense, making it challenging for fuel cells to compete on price with conventional fuels in many sectors. Furthermore, the energy density of hydrogen, especially in its gaseous state, necessitates large and heavy storage tanks, which can be a constraint for certain mobile applications, impacting vehicle design and range.

Another critical challenge involves the durability and lifespan of fuel cell stacks. Despite advancements, issues such as catalyst degradation, membrane performance decline, and susceptibility to impurities in hydrogen fuel can limit the operational life of fuel cell systems, particularly in demanding applications. The need for high-purity hydrogen also poses a challenge, as even trace amounts of contaminants can significantly impair fuel cell performance and longevity. Addressing these durability concerns and developing more robust and long-lasting components is essential to enhance consumer confidence and reduce the total cost of ownership, which is crucial for broad market acceptance and sustained growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High cost and energy intensity of green hydrogen production | -3.2% | Global | Mid to Long-term (2025-2033) |

| Durability and degradation issues of fuel cell components (e.g., catalysts, membranes) | -2.5% | Global | Short to Mid-term (2025-2029) |

| Complexity of hydrogen storage and distribution logistics | -2.0% | Global | Mid-term (2025-2030) |

| Public perception and safety concerns regarding hydrogen fuel | -1.5% | Global | Long-term (2025-2033) |

Fuel Cell Market - Updated Report Scope

This report provides a comprehensive analysis of the global Fuel Cell Market, delving into market size, growth drivers, restraints, opportunities, and challenges. It offers detailed segmentation by fuel cell type, application, and end-use industry, alongside an in-depth regional analysis. The scope encompasses current market dynamics, emerging trends, the impact of artificial intelligence, and a competitive landscape profiling key industry players, furnishing strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 45.3 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | FuelCell Innovations Ltd., PowerGen Systems Corp., Hydrogenics Solutions Inc., ElectroChem Power Systems, Green Energy Technologies, Advanced Fuel Cell Corp., NextGen Fuel Cell Group, EcoPower Solutions, Proton Energy Systems, Global Fuel Cell Dynamics, Renewable Power Integrators, Sustainable Energy Innovations, Universal Fuel Cell Co., Delta Energy Systems, TeraVolt Power Solutions, Quantum Fuel Cell Technologies, Apex Clean Energy, Synergy Fuel Cell Research, Pioneering Hydrogen Solutions, FutureGen Power |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fuel Cell Market is segmented to provide granular insights into various technologies, applications, and end-use sectors, reflecting the diverse landscape of fuel cell adoption. This detailed segmentation helps in understanding specific market dynamics, growth pockets, and competitive landscapes within each category. Analyzing these segments is crucial for stakeholders to identify promising areas for investment, product development, and market entry strategies, ensuring a targeted approach to capitalize on emerging opportunities.

- By Type: Covers various fuel cell technologies such as Polymer Electrolyte Membrane Fuel Cells (PEMFC) known for low-temperature operation, Solid Oxide Fuel Cells (SOFC) for high-temperature stationary applications, Phosphoric Acid Fuel Cells (PAFC), Molten Carbonate Fuel Cells (MCFC), Alkaline Fuel Cells (AFC), and Direct Methanol Fuel Cells (DMFC), each with distinct operational characteristics and best-fit applications.

- By Application: Encompasses the primary uses of fuel cell technology, including Transportation (passenger vehicles, commercial vehicles, buses, forklifts, marine, rail, aviation), Stationary Power (combined heat and power (CHP), backup power, primary power), and Portable Power (consumer electronics, remote sensors, military equipment), highlighting the versatility of fuel cells across mobile and static deployments.

- By End-Use Industry: Addresses the specific industries adopting fuel cell solutions, such as Automotive for vehicle propulsion, Residential for home power, Commercial for buildings, Industrial processes, Data Centers for critical backup power, Telecommunications for remote tower power, Utilities for grid support, Military for field operations, and Aerospace for specialized power needs, demonstrating broad industrial applicability.

Regional Highlights

- North America: Driven by increasing investments in hydrogen infrastructure, government incentives for clean energy, and a strong focus on fuel cell electric vehicles (FCEVs) and stationary power for critical infrastructure like data centers.

- Europe: Leading in green hydrogen initiatives, with ambitious decarbonization targets and significant R&D funding for fuel cell technology. Germany, UK, and the Nordic countries are at the forefront of adopting fuel cells in transportation and industrial applications.

- Asia Pacific (APAC): The largest and fastest-growing market, primarily fueled by strong government support in countries like Japan, South Korea, and China. These nations are heavily investing in FCEV development, hydrogen infrastructure, and large-scale stationary power projects.

- Latin America: Emerging market with increasing interest in sustainable energy solutions, particularly for remote power generation and heavy-duty transportation in countries like Chile and Brazil, focusing on renewable hydrogen production.

- Middle East and Africa (MEA): Growing potential driven by abundant renewable energy resources for green hydrogen production and the need for reliable off-grid power solutions in remote areas. Countries like Saudi Arabia and UAE are exploring large-scale hydrogen export and domestic use.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fuel Cell Market.- FuelCell Innovations Ltd.

- PowerGen Systems Corp.

- Hydrogenics Solutions Inc.

- ElectroChem Power Systems

- Green Energy Technologies

- Advanced Fuel Cell Corp.

- NextGen Fuel Cell Group

- EcoPower Solutions

- Proton Energy Systems

- Global Fuel Cell Dynamics

- Renewable Power Integrators

- Sustainable Energy Innovations

- Universal Fuel Cell Co.

- Delta Energy Systems

- TeraVolt Power Solutions

- Quantum Fuel Cell Technologies

- Apex Clean Energy

- Synergy Fuel Cell Research

- Pioneering Hydrogen Solutions

- FutureGen Power

Frequently Asked Questions

What is a fuel cell and how does it work?

A fuel cell is an electrochemical device that converts the chemical energy of a fuel (often hydrogen) and an oxidant (often oxygen from air) into electricity, water, and heat through a chemical reaction, without combustion. Unlike batteries, fuel cells produce electricity continuously as long as fuel and oxidant are supplied.

What are the primary types of fuel cells?

The main types include Polymer Electrolyte Membrane Fuel Cells (PEMFCs), popular for vehicles; Solid Oxide Fuel Cells (SOFCs), known for high-temperature stationary power; Phosphoric Acid Fuel Cells (PAFCs); Molten Carbonate Fuel Cells (MCFCs); Alkaline Fuel Cells (AFCs); and Direct Methanol Fuel Cells (DMFCs), each suited for different applications based on operating temperature and fuel requirements.

What are the key applications of fuel cell technology?

Fuel cells are applied across diverse sectors including transportation (fuel cell electric vehicles, buses, forklifts, marine, rail), stationary power generation (combined heat and power, backup power for critical infrastructure), and portable power for consumer electronics, military devices, and remote sensors, offering clean and efficient energy solutions.

What are the main advantages of fuel cells over traditional energy sources?

Fuel cells offer significant advantages such as zero or near-zero emissions (producing only water and heat when using hydrogen), high energy efficiency, quiet operation, and the ability to provide continuous power as long as fuel is supplied. They are also highly scalable and can be integrated with renewable energy sources for sustainable energy systems.

What is the role of hydrogen infrastructure in the fuel cell market?

A robust hydrogen infrastructure, encompassing production, storage, and distribution networks, is critical for the widespread adoption and growth of the fuel cell market. It ensures the availability of fuel for FCEVs and stationary fuel cells, addressing range anxiety and operational logistics, thereby enhancing the economic viability and scalability of fuel cell solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted