Foundry Equipment Market

Foundry Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710107 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

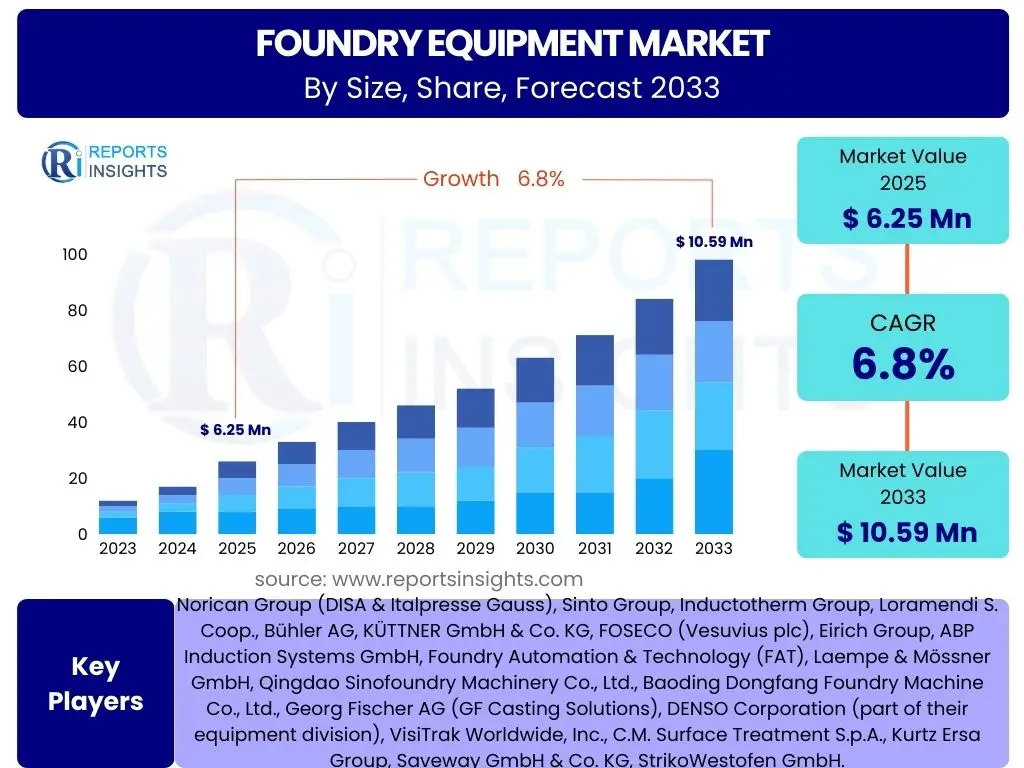

Foundry Equipment Market Size

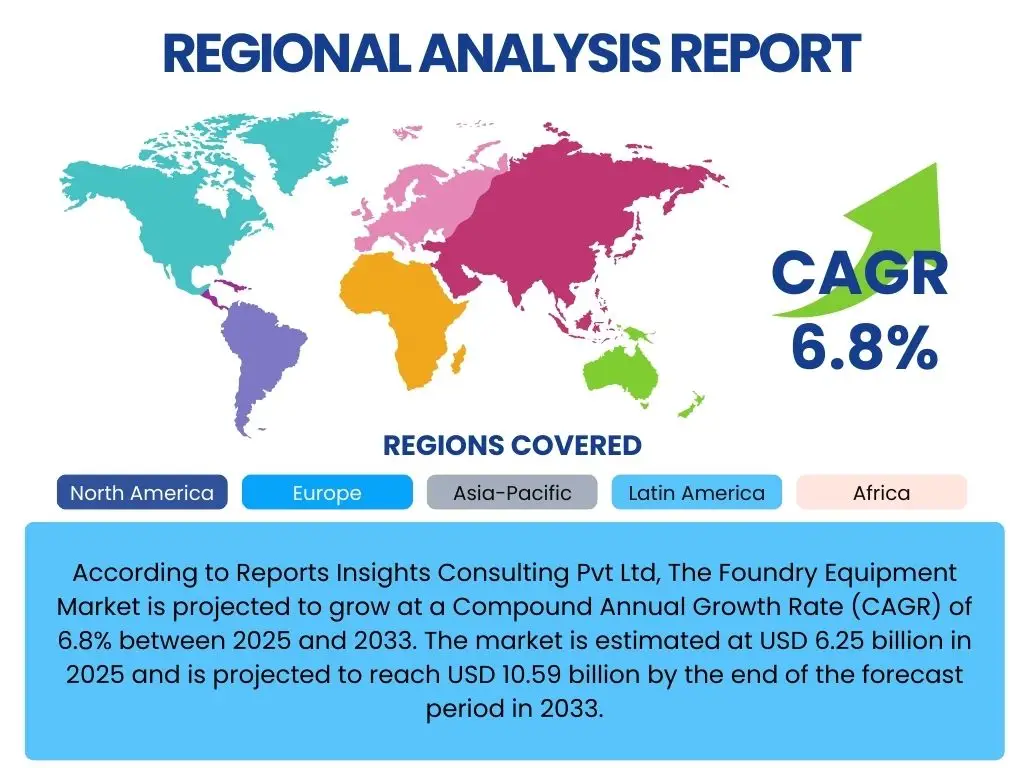

According to Reports Insights Consulting Pvt Ltd, The Foundry Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 6.25 billion in 2025 and is projected to reach USD 10.59 billion by the end of the forecast period in 2033.

Key Foundry Equipment Market Trends & Insights

The Foundry Equipment Market is experiencing a transformative phase, driven by a confluence of technological advancements and evolving industry demands. User inquiries frequently center on the adoption of automation, digitalization, and sustainable practices within foundry operations, reflecting a keen interest in how these elements are reshaping the manufacturing landscape. There is a growing emphasis on precision, efficiency, and environmental compliance, pushing equipment manufacturers to innovate. Furthermore, discussions often highlight the impact of material science advancements on casting processes and the necessity for equipment that can handle a wider range of alloys and complex geometries. This dynamic environment necessitates continuous upgrades and integration of smart technologies to remain competitive.

A significant trend observed is the increasing investment in smart factory initiatives, where foundry equipment is interconnected through the Internet of Things (IoT). This integration facilitates real-time data collection, remote monitoring, and predictive maintenance, thereby minimizing downtime and optimizing production schedules. Foundries are seeking solutions that not only enhance operational efficiency but also reduce energy consumption and waste generation, aligning with global sustainability goals. The push for lightweighting in industries like automotive and aerospace also drives demand for advanced casting techniques and specialized equipment capable of processing high-strength, low-density materials.

Moreover, the market is witnessing a shift towards customized and flexible production systems, moving away from mass production towards smaller batch, high-mix manufacturing. This requires modular and adaptable foundry equipment that can be reconfigured quickly to meet changing product specifications. The integration of advanced robotics for material handling, pouring, and finishing operations is also becoming more prevalent, addressing labor shortages and improving workplace safety. These trends collectively underscore an industry in pursuit of higher productivity, improved quality, and reduced environmental footprint through sophisticated equipment solutions.

- Automation and Robotics Integration: Increased adoption of automated systems for material handling, pouring, and finishing processes to enhance efficiency and safety.

- Digitalization and IoT Integration: Implementation of smart sensors, real-time monitoring, and data analytics for predictive maintenance and operational optimization.

- Sustainable Manufacturing Practices: Growing demand for energy-efficient furnaces, reduced waste generation, and eco-friendly casting processes.

- Advanced Material Processing: Development of equipment capable of handling complex alloys and advanced materials for lightweighting and high-performance applications.

- Customization and Flexibility: Shift towards modular equipment and flexible production lines to support high-mix, low-volume manufacturing.

AI Impact Analysis on Foundry Equipment

The integration of Artificial Intelligence (AI) into the foundry equipment market represents a paradigm shift, as indicated by numerous user inquiries focusing on its transformative potential. Users are keen to understand how AI can improve process control, enhance quality assurance, and optimize resource utilization. The primary themes emerging from these questions revolve around AI's ability to automate complex decision-making, learn from production data, and predict potential issues before they escalate. Expectations are high for AI to reduce operational costs, minimize defects, and accelerate innovation in casting technologies, thereby making foundry operations more resilient and competitive.

AI's influence extends across various stages of the casting process, from design and simulation to post-casting inspection. For instance, AI-driven simulations can optimize mold designs, predict solidification patterns, and identify potential defects virtually, significantly reducing prototyping costs and time. During production, machine learning algorithms analyze sensor data from melting furnaces, molding machines, and casting units to fine-tune parameters in real-time, ensuring consistent quality and maximizing yield. This capability to adapt and optimize dynamically is a core expectation from users, anticipating a substantial leap in operational precision and material efficiency.

However, concerns also exist regarding the initial investment in AI infrastructure, the availability of skilled personnel to manage and interpret AI systems, and data security. Despite these challenges, the overwhelming sentiment is one of optimism, with users envisioning AI as a critical enabler for predictive maintenance, advanced quality control, and intelligent automation that addresses the industry's need for higher productivity, lower defect rates, and greater operational intelligence. The long-term impact is expected to foster a more adaptive, self-optimizing, and sustainable foundry ecosystem.

- Predictive Maintenance: AI algorithms analyze equipment performance data to forecast potential failures, enabling proactive maintenance and reducing downtime.

- Process Optimization: Machine learning models optimize parameters for melting, pouring, and molding, leading to improved material utilization and energy efficiency.

- Quality Control: AI-powered vision systems and sensors detect defects with higher accuracy and speed than manual inspection, enhancing product quality.

- Design and Simulation: AI assists in simulating casting processes and optimizing mold designs, reducing development cycles and material waste.

- Enhanced Workforce Efficiency: AI tools can automate repetitive tasks, allowing human operators to focus on more complex decision-making and problem-solving.

Key Takeaways Foundry Equipment Market Size & Forecast

The Foundry Equipment Market is poised for robust growth over the forecast period, driven by sustained demand from key end-use industries and a strong emphasis on technological modernization. User inquiries consistently highlight the importance of understanding the underlying growth drivers, such as the increasing adoption of lightweight materials in automotive and aerospace, and the broader push towards industrial automation. A key insight is that market expansion is not solely volume-driven but significantly influenced by the value proposition of advanced, efficient, and environmentally compliant equipment. This indicates a premium placed on solutions that offer long-term operational savings and improved product quality.

Another critical takeaway is the increasing geographical diversification of growth, with emerging economies playing a progressively larger role. While established markets continue to invest in upgrading existing facilities, rapid industrialization and infrastructure development in regions like Asia Pacific are creating new avenues for market entry and expansion. The forecast underscores a strategic shift towards integrated solutions that combine hardware with software, data analytics, and service support, reflecting a holistic approach to foundry operations. This integrated approach is expected to unlock further efficiencies and cost reductions for foundry operators globally.

Furthermore, the market's resilience is bolstered by continuous innovation aimed at addressing persistent industry challenges, including energy consumption, environmental impact, and labor shortages. The projected growth trajectory reflects a confident outlook on the industry's ability to adapt and leverage new technologies, such as additive manufacturing and advanced process controls, to meet evolving customer expectations. Stakeholders are advised to focus on sustainable practices and smart manufacturing solutions to capitalize on these growth opportunities and solidify their market position.

- Significant Growth Trajectory: The market is set for substantial expansion, reaching over USD 10 billion by 2033, indicating strong investment potential.

- Technology-Driven Evolution: Adoption of automation, digitalization, and AI will be critical for achieving operational excellence and market competitiveness.

- Sustainability as a Core Driver: Demand for energy-efficient and eco-friendly equipment will increasingly influence purchasing decisions and product development.

- Emerging Markets Leading Expansion: Asia Pacific and other developing regions are expected to be primary growth engines due to industrialization and infrastructure projects.

- Focus on Integrated Solutions: Manufacturers offering comprehensive equipment, software, and service packages will gain a competitive advantage.

Foundry Equipment Market Drivers Analysis

The Foundry Equipment Market is profoundly influenced by several key drivers that are propelling its growth and technological evolution. One of the most significant factors is the continuous expansion of the automotive industry, particularly the global shift towards electric vehicles (EVs) and the demand for lighter, more fuel-efficient components. This necessitates advanced casting processes capable of producing intricate, high-integrity parts from aluminum and other lightweight alloys, directly driving the demand for state-of-the-art melting, molding, and casting equipment. The stringent requirements for component quality and reliability in the automotive sector push foundry equipment manufacturers to innovate constantly, providing more precise and automated solutions.

Another crucial driver is the rapid industrialization and infrastructure development occurring across emerging economies, particularly in Asia Pacific. Countries like China, India, and Southeast Asian nations are investing heavily in manufacturing, construction, and transportation sectors, which in turn fuels the demand for castings. This surge in industrial activity requires new foundries to be established and existing ones to be modernized, leading to increased procurement of foundry equipment. The growing middle class and rising disposable incomes in these regions also contribute to the demand for manufactured goods, further stimulating the foundry industry.

Furthermore, the increasing global emphasis on automation and smart manufacturing practices is a powerful catalyst for the foundry equipment market. Foundries are adopting automated systems to combat labor shortages, improve workplace safety, and enhance productivity and efficiency. The integration of Industry 4.0 technologies, such as IoT, AI, and advanced robotics, into foundry equipment allows for real-time monitoring, predictive maintenance, and optimized production processes. This technological push is not only improving operational performance but also enabling foundries to meet increasingly complex production requirements and higher quality standards.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Automotive Industry Growth & Lightweighting Trends | +1.5% | Global, particularly Asia Pacific, Europe, North America | Long-term |

| Increasing Industrialization in Emerging Economies | +1.2% | Asia Pacific (China, India), Latin America | Medium to Long-term |

| Adoption of Automation & Industry 4.0 Technologies | +1.0% | Global, particularly developed economies | Medium-term |

| Demand for High-Precision and Complex Castings | +0.8% | Global | Medium to Long-term |

| Urbanization and Infrastructure Development | +0.7% | Asia Pacific, Africa, Middle East | Long-term |

Foundry Equipment Market Restraints Analysis

Despite the positive growth outlook, the Foundry Equipment Market faces several significant restraints that could impede its expansion. One prominent challenge is the substantial capital investment required for purchasing and installing new foundry equipment. Modern, automated, and technologically advanced machinery often comes with a high price tag, which can be a barrier for small and medium-sized enterprises (SMEs) or foundries operating with limited financial resources. This high initial outlay, coupled with the long payback periods, can deter investment in necessary upgrades or capacity expansion, especially during periods of economic uncertainty or fluctuating raw material costs.

Another critical restraint is the increasingly stringent environmental regulations and compliance costs. Foundries are typically energy-intensive operations that can generate significant emissions and waste. Governments worldwide are imposing stricter rules regarding air pollution, water discharge, and waste management, compelling foundries to invest in expensive abatement technologies and cleaner production processes. While these measures are crucial for sustainability, they add considerable operational costs and complexity for foundry operators, which can translate into reduced investment in core production equipment or lead to the closure of older, non-compliant facilities.

Furthermore, the persistent shortage of skilled labor poses a significant challenge to the foundry equipment market. Modern foundry equipment requires operators with specialized skills in automation, robotics, and digital control systems. The aging workforce in many industrialized nations, coupled with a lack of new entrants into the manufacturing sector, creates a substantial gap in the skilled labor pool. This shortage not only impacts the efficient operation and maintenance of advanced equipment but also slows down the adoption of new technologies, as foundries may lack the personnel to effectively implement and manage them. This human capital challenge limits the potential for innovation and operational efficiency.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment & Maintenance Costs | -0.8% | Global | Long-term |

| Stringent Environmental Regulations & Compliance Costs | -0.7% | Europe, North America, parts of Asia Pacific | Medium to Long-term |

| Shortage of Skilled Labor and Technical Expertise | -0.6% | Global, particularly developed economies | Long-term |

| Volatility in Raw Material Prices (e.g., metals, energy) | -0.5% | Global | Short to Medium-term |

| Economic Downturns and Geopolitical Instability | -0.4% | Global | Short-term |

Foundry Equipment Market Opportunities Analysis

Despite the challenges, the Foundry Equipment Market is rich with opportunities stemming from technological advancements and evolving industry landscapes. One significant opportunity lies in the burgeoning demand for energy-efficient and environmentally friendly equipment. As global environmental awareness increases and regulations tighten, foundries are actively seeking solutions that reduce their carbon footprint and operational costs. This creates a strong market for innovative melting furnaces, regenerative burners, and waste heat recovery systems, as well as advanced filtration and emission control technologies. Equipment manufacturers that can offer certified green solutions stand to gain a competitive edge and tap into a growing segment of environmentally conscious buyers.

Another major opportunity is presented by the ongoing digital transformation within manufacturing, particularly the wider adoption of Industry 4.0 and smart factory concepts. This includes the integration of IoT sensors, AI-driven analytics, and cloud computing into foundry equipment, enabling predictive maintenance, real-time process control, and supply chain optimization. The ability to offer interconnected systems that provide actionable insights into production processes represents a substantial value proposition for foundries aiming to enhance efficiency, reduce defects, and improve overall productivity. Developing comprehensive software and hardware packages tailored for smart foundries offers a significant growth avenue.

Furthermore, the rise of additive manufacturing (3D printing) presents a unique opportunity for synergy rather than pure competition. While additive manufacturing offers an alternative for complex parts, it can also complement traditional casting processes, particularly in tooling, pattern making, and prototyping. Foundry equipment manufacturers can explore integrating 3D printing technologies into their offerings or developing hybrid solutions that combine the strengths of both methods. This could lead to faster product development cycles, increased design flexibility, and the ability to produce highly customized components. Collaborations with additive manufacturing specialists could unlock new markets and applications for the foundry equipment sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Energy-Efficient & Eco-friendly Equipment | +1.0% | Global, particularly Europe, North America | Long-term |

| Expansion of Industry 4.0 & Smart Foundry Solutions | +0.9% | Global | Medium to Long-term |

| Integration of Additive Manufacturing for Tooling & Prototyping | +0.7% | Global | Medium-term |

| Market Expansion in Untapped Developing Regions | +0.6% | Africa, parts of Latin America, Southeast Asia | Long-term |

| Demand for Specialized Equipment for Advanced Materials | +0.5% | Global | Medium to Long-term |

Foundry Equipment Market Challenges Impact Analysis

The Foundry Equipment Market is confronted by several complex challenges that require strategic responses from manufacturers and operators alike. One significant hurdle is the intense global competition, particularly from manufacturers in Asia, who often offer cost-effective solutions. This competitive pressure forces established players to constantly innovate, reduce production costs, and enhance the value proposition of their equipment. Maintaining a competitive edge requires substantial investment in research and development, as well as efficient supply chain management, to balance technological superiority with affordability. The market is also fragmented, with many regional players catering to specific needs, making it difficult for new entrants to gain significant traction.

Another critical challenge is the rapid pace of technological obsolescence. As industries demand higher precision, greater efficiency, and more sophisticated materials, foundry equipment must evolve quickly to meet these new standards. Equipment purchased today might become outdated within a few years due to advancements in automation, digital controls, or material science. This creates pressure on foundries to make frequent capital investments, which can be financially burdensome. For equipment manufacturers, it means a continuous cycle of innovation and product development to stay relevant, requiring substantial R&D expenditure and the ability to quickly adapt to market shifts.

Furthermore, supply chain disruptions, as experienced during recent global events, pose a substantial challenge to the manufacturing and delivery of foundry equipment. Reliance on a global network for components, raw materials, and specialized parts makes the production process vulnerable to geopolitical tensions, trade restrictions, and natural disasters. These disruptions can lead to increased lead times, higher production costs, and delays in equipment delivery, impacting customer satisfaction and market stability. Manufacturers must invest in supply chain resilience strategies, including diversification of suppliers and increased localization, to mitigate these risks and ensure operational continuity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Global Competition & Price Pressures | -0.7% | Global | Long-term |

| Rapid Technological Obsolescence | -0.6% | Global | Medium to Long-term |

| Supply Chain Disruptions and Volatility | -0.5% | Global | Short to Medium-term |

| High Energy Costs for Foundry Operations | -0.4% | Global | Short to Medium-term |

| Integration Complexity of New Technologies | -0.3% | Global | Medium-term |

Foundry Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Foundry Equipment Market, segmenting it by equipment type, application, and geographical region to offer a holistic view of the industry landscape. It delves into the market dynamics, identifying key drivers, restraints, opportunities, and challenges that shape market growth. Furthermore, the report incorporates a thorough examination of the competitive landscape, profiling key market players and their strategic initiatives, alongside an impact assessment of emerging technologies like AI and Industry 4.0 on the market's trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.25 Billion |

| Market Forecast in 2033 | USD 10.59 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Norican Group (DISA & Italpresse Gauss), Sinto Group, Inductotherm Group, Loramendi S. Coop., Bühler AG, KÜTTNER GmbH & Co. KG, FOSECO (Vesuvius plc), Eirich Group, ABP Induction Systems GmbH, Foundry Automation & Technology (FAT), Laempe & Mössner GmbH, Qingdao Sinofoundry Machinery Co., Ltd., Baoding Dongfang Foundry Machine Co., Ltd., Georg Fischer AG (GF Casting Solutions), DENSO Corporation (part of their equipment division), VisiTrak Worldwide, Inc., C.M. Surface Treatment S.p.A., Kurtz Ersa Group, Saveway GmbH & Co. KG, StrikoWestofen GmbH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Foundry Equipment Market is meticulously segmented to provide a granular understanding of its diverse components and evolving consumer preferences. This detailed segmentation allows for a precise analysis of market dynamics across different equipment types, applications, and end-use materials. Understanding these segments is crucial for stakeholders to identify lucrative niche markets, tailor product offerings, and develop targeted marketing strategies that resonate with specific industry needs. The intricate interplay between these segments often dictates regional growth patterns and technological adoption rates.

The segmentation by equipment type highlights the varying technological demands across the casting process, from the initial melting of metals to the final finishing of products. Each equipment category, such as molding machines, melting furnaces, and casting machines, represents a distinct sub-market driven by its own set of innovation cycles and operational requirements. Similarly, segmenting by application elucidates which industries are the primary consumers of foundry products, thereby indicating the key demand drivers for equipment. For instance, the automotive sector's demand for lightweight components significantly influences innovation in aluminum casting equipment.

Furthermore, the breakdown by end-use material, distinguishing between ferrous and non-ferrous castings, reveals critical insights into material processing trends. The increasing preference for non-ferrous metals like aluminum and magnesium, especially in sectors prioritizing weight reduction, is a significant factor shaping equipment design and capabilities. This multi-faceted segmentation structure ensures a comprehensive market overview, aiding in strategic decision-making and fostering a deeper understanding of the market's complex ecosystem and future growth trajectories.

- By Type:

- Molding Machines (Green Sand Molding, Core Making, Shell Molding)

- Melting Furnaces (Induction Furnaces, Arc Furnaces, Cupola Furnaces)

- Casting Machines (Die Casting, Gravity Die Casting, Centrifugal Casting)

- Shot Blasting Machines

- Sand Preparation Equipment

- Material Handling Equipment

- Others (Degassing Units, Trim Presses)

- By Application:

- Automotive

- Heavy Machinery (Construction, Mining, Agricultural)

- Aerospace & Defense

- Railway

- Pumps & Valves

- Electrical & Electronics

- General Manufacturing

- Others

- By End-Use Material:

- Ferrous Castings (Iron, Steel)

- Non-Ferrous Castings (Aluminum, Magnesium, Copper, Zinc)

Regional Highlights

- Asia Pacific (APAC): Dominates the Foundry Equipment Market, primarily driven by rapid industrialization, extensive manufacturing activities, and significant infrastructure development in countries like China, India, and Southeast Asian nations. The region benefits from lower labor costs, a growing automotive industry, and increasing foreign direct investment in manufacturing.

- Europe: A mature market characterized by stringent environmental regulations and a strong focus on advanced, energy-efficient, and automated foundry equipment. Germany, Italy, and France are key contributors, driven by their robust automotive, machinery, and aerospace industries, emphasizing precision engineering and sustainable practices.

- North America: Marked by significant investment in technology upgrades and automation to enhance productivity and address labor shortages. The United States and Canada are leading the adoption of Industry 4.0 solutions, particularly in the automotive, aerospace, and heavy equipment sectors, with a growing emphasis on high-quality and lightweight castings.

- Latin America: Experiences steady growth, influenced by the automotive and construction sectors in Brazil and Mexico. The region shows potential for modernization of existing foundries and increasing demand for cost-effective and durable equipment.

- Middle East and Africa (MEA): An emerging market with increasing investments in infrastructure, oil & gas, and manufacturing diversification initiatives. Countries in the GCC (Gulf Cooperation Council) are expected to drive demand for modern foundry equipment as they expand their industrial base and reduce reliance on oil exports.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Foundry Equipment Market.- Norican Group (DISA & Italpresse Gauss)

- Sinto Group

- Inductotherm Group

- Loramendi S. Coop.

- Bühler AG

- KÜTTNER GmbH & Co. KG

- FOSECO (Vesuvius plc)

- Eirich Group

- ABP Induction Systems GmbH

- Foundry Automation & Technology (FAT)

- Laempe & Mössner GmbH

- Qingdao Sinofoundry Machinery Co., Ltd.

- Baoding Dongfang Foundry Machine Co., Ltd.

- Georg Fischer AG (GF Casting Solutions)

- DENSO Corporation

- VisiTrak Worldwide, Inc.

- C.M. Surface Treatment S.p.A.

- Kurtz Ersa Group

- Saveway GmbH & Co. KG

- StrikoWestofen GmbH

Frequently Asked Questions

Analyze common user questions about the Foundry Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current estimated size and projected growth rate of the Foundry Equipment Market?

The Foundry Equipment Market is estimated at USD 6.25 billion in 2025 and is projected to reach USD 10.59 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period.

Which key trends are shaping the Foundry Equipment Market?

Key trends include the increasing adoption of automation and robotics, digitalization and IoT integration for smart factories, a strong emphasis on sustainable manufacturing practices, the development of equipment for advanced material processing, and a shift towards customization and flexibility in production.

How is Artificial Intelligence (AI) impacting the Foundry Equipment Market?

AI significantly impacts the market through predictive maintenance, process optimization, enhanced quality control via vision systems, assistance in design and simulation, and improved workforce efficiency by automating complex tasks and providing data-driven insights.

What are the primary drivers and restraints affecting market growth?

Primary drivers include the growth of the automotive industry and lightweighting trends, increasing industrialization in emerging economies, and the adoption of Industry 4.0 technologies. Key restraints involve high capital investment, stringent environmental regulations, and a shortage of skilled labor.

Which region holds the largest share in the Foundry Equipment Market?

Asia Pacific (APAC) currently holds the largest market share, driven by rapid industrialization, extensive manufacturing activities, and significant infrastructure development in countries such as China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted