Food Service Packaging Market

Food Service Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710344 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

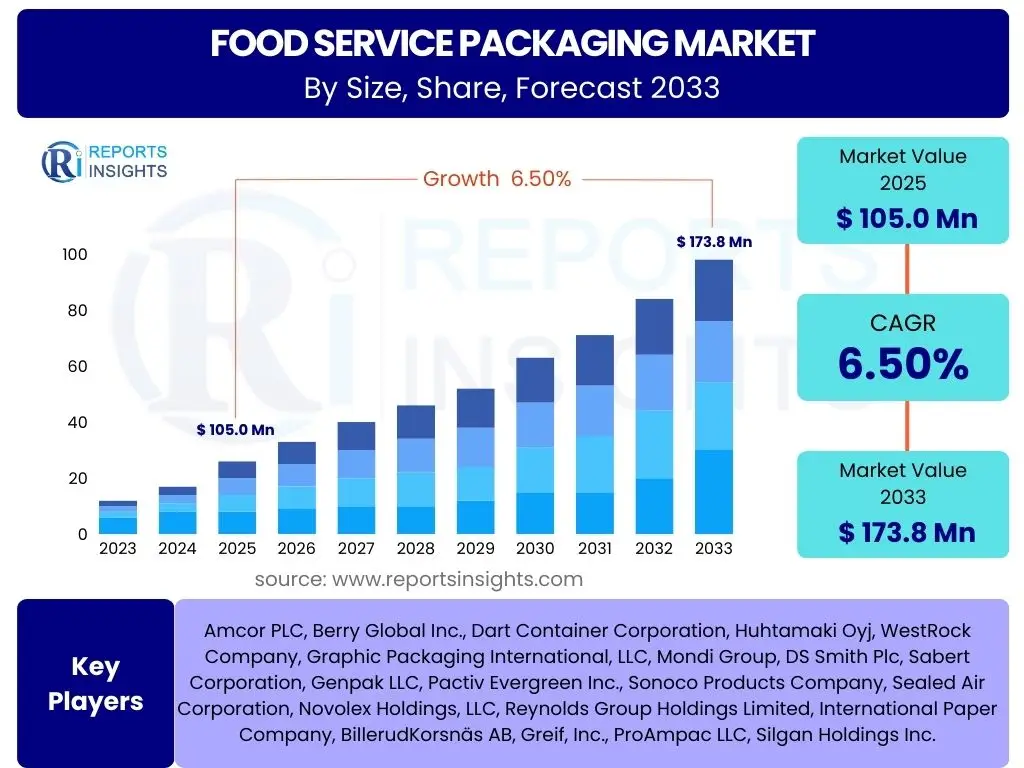

Food Service Packaging Market Size

According to Reports Insights Consulting Pvt Ltd, The Food Service Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 105.0 billion in 2025 and is projected to reach USD 173.8 billion by the end of the forecast period in 2033.

Key Food Service Packaging Market Trends & Insights

The food service packaging market is currently experiencing a dynamic shift, largely driven by evolving consumer preferences and increasing environmental consciousness. Users frequently inquire about the prevalent trends shaping this sector, particularly focusing on the balance between convenience, sustainability, and technological advancements. There is a clear interest in understanding how packaging solutions are adapting to the rise of food delivery services, on-the-go consumption, and stringent regulatory landscapes.

Major insights reveal that innovation is concentrated on developing materials that are both functional and eco-friendly, addressing public concern over waste. Additionally, the integration of digital features and smart technologies is emerging as a critical trend, aiming to enhance customer engagement, improve supply chain efficiency, and ensure food safety. These developments are not just about compliance but also about creating a competitive edge and meeting the demands of a more informed consumer base.

- Escalating demand for sustainable and eco-friendly packaging materials (e.g., compostable, recyclable, biodegradable).

- Surge in convenience-driven packaging solutions for on-the-go consumption and ready-to-eat meals.

- Rapid growth of food delivery and takeaway services necessitating specialized, robust, and insulated packaging.

- Increased focus on food safety, hygiene, and tamper-evident packaging.

- Adoption of lightweighting strategies and material reduction to minimize environmental impact and transportation costs.

- Premiumization of packaging to enhance brand perception and consumer experience.

- Integration of smart packaging technologies like QR codes, NFC tags, and temperature indicators for traceability and engagement.

AI Impact Analysis on Food Service Packaging

Common user questions related to the impact of AI on food service packaging often center on automation, efficiency gains, and predictive capabilities. Consumers and industry professionals alike are keen to understand how artificial intelligence can revolutionize the entire packaging lifecycle, from design and production to supply chain management and waste reduction. Key themes emerging from these inquiries include the potential for AI to optimize material usage, personalize packaging solutions, and streamline operational processes, thereby addressing both economic and environmental objectives.

The analysis indicates that AI is poised to significantly transform the food service packaging landscape by introducing unprecedented levels of precision, speed, and intelligence. Concerns often revolve around the initial investment costs and the need for skilled personnel to manage AI systems, yet the long-term benefits in terms of cost savings, reduced waste, and enhanced customer satisfaction are compelling. Expectations are high for AI to create more responsive, sustainable, and consumer-centric packaging solutions.

- Enhanced predictive analytics for demand forecasting, optimizing inventory and reducing overproduction.

- Automated quality control systems for improved consistency and defect detection during manufacturing.

- Optimization of packaging design processes, including material selection and structural integrity, for sustainability and cost efficiency.

- Intelligent supply chain management, enabling real-time tracking, route optimization, and cold chain monitoring.

- Personalized packaging solutions through AI-driven design tools, catering to individual consumer preferences.

- Robotics and automation in packaging lines, increasing speed, accuracy, and reducing labor costs.

- AI-powered waste management and recycling sorting technologies to improve material recovery rates.

Key Takeaways Food Service Packaging Market Size & Forecast

Insights derived from user questions regarding the Food Service Packaging market size and forecast consistently point to a strong and sustained growth trajectory. Users are particularly interested in understanding the underlying factors propelling this expansion, as well as the segments poised for the most significant development. The forecast indicates that despite economic fluctuations, the fundamental drivers of convenience, urbanization, and changing lifestyles will continue to fuel market progression.

A crucial takeaway is the increasing emphasis on innovation in sustainable materials and production methods, which will not only meet regulatory requirements but also satisfy growing consumer demand for environmentally responsible products. The market's resilience is further supported by the burgeoning food delivery sector and the continuous evolution of food service models, ensuring a robust future for packaging solutions. Stakeholders are keen to leverage these trends for strategic investments and product development.

- The food service packaging market is projected for substantial growth, driven by global shifts in consumer behavior and the expansion of the hospitality sector.

- Sustainability is no longer a niche but a core requirement, influencing material innovation and regulatory frameworks across all market segments.

- The rise of e-commerce and food delivery platforms is a primary catalyst, creating increased demand for specialized and protective packaging.

- Asia Pacific and emerging economies are expected to be key growth engines due to rapid urbanization and increasing disposable incomes.

- Technological advancements, including smart packaging and AI integration, will play a critical role in enhancing efficiency, safety, and consumer engagement.

- Strategic partnerships and mergers and acquisitions are anticipated to consolidate market leadership and foster innovation in sustainable solutions.

Food Service Packaging Market Drivers Analysis

The food service packaging market is primarily propelled by several macroeconomic and societal factors that collectively contribute to its robust expansion. Key among these drivers is the global rise in urbanization and the associated shift towards convenience-oriented lifestyles, which inherently increase the demand for ready-to-eat meals, takeaway options, and food delivery services. This paradigm shift requires packaging solutions that are not only practical and protective but also aesthetically pleasing and reflective of brand values.

Additionally, the burgeoning e-commerce sector, particularly within the food and beverage industry, has amplified the need for specialized packaging designed for transit and delivery, ensuring product integrity and safety. Consumer awareness regarding food hygiene and safety has also spurred innovation in tamper-evident and protective packaging. Furthermore, the increasing disposable incomes in emerging economies are leading to greater indulgence in out-of-home dining and convenience foods, creating a fertile ground for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Convenience Foods & Ready-to-Eat Meals | +2.0% | Global, particularly urban centers | Short to Mid-term (2025-2029) |

| Expansion of Food Delivery & Takeaway Services | +1.8% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Increasing Consumer Preference for Sustainable Packaging | +1.5% | Europe, North America, parts of Asia | Mid to Long-term (2026-2033) |

| Rising Disposable Incomes & Changing Dietary Habits | +1.2% | Emerging economies, Asia Pacific | Mid to Long-term (2027-2033) |

Food Service Packaging Market Restraints Analysis

Despite significant growth potential, the food service packaging market faces several notable restraints that can impede its progress. A primary challenge stems from the increasing stringency of environmental regulations, particularly concerning single-use plastics. Many governments globally are implementing bans and taxes on plastic packaging, compelling manufacturers to invest heavily in alternative materials, which often come with higher production costs and complex supply chains.

Another significant restraint is the volatile pricing of raw materials, including polymers, paper pulp, and metals. Fluctuations in these commodity prices directly impact manufacturing costs, subsequently affecting profit margins for packaging producers and increasing end-user prices. Furthermore, the limited availability and high cost of advanced recycling infrastructure, especially for multi-material packaging, pose considerable barriers to achieving a truly circular economy within the industry, limiting the widespread adoption of certain sustainable solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations & Bans on Single-Use Plastics | -1.5% | Europe, specific states in North America | Short to Long-term (2025-2033) |

| High Cost of Sustainable Packaging Materials | -1.0% | Global | Short to Mid-term (2025-2030) |

| Supply Chain Disruptions & Raw Material Price Volatility | -0.8% | Global | Short-term (2025-2027) |

| Limited Recycling Infrastructure for Complex Packaging | -0.7% | Global, particularly developing regions | Long-term (2025-2033) |

Food Service Packaging Market Opportunities Analysis

The food service packaging market is rich with opportunities, primarily driven by ongoing innovations and evolving consumer expectations. A significant avenue for growth lies in the continuous development of novel biodegradable and compostable packaging solutions. As environmental concerns escalate and regulatory pressures increase, companies that invest in and commercialize truly sustainable alternatives will gain a substantial competitive advantage, appealing to a growing segment of eco-conscious consumers and businesses.

Moreover, the untapped potential in emerging markets presents another major opportunity. Regions in Asia Pacific, Latin America, and Africa are experiencing rapid economic growth, urbanization, and an expansion of their food service sectors. These markets are ripe for the adoption of modern packaging solutions, offering lucrative prospects for manufacturers willing to tailor products to local needs and economic capacities. Furthermore, the integration of smart packaging technologies, such as advanced traceability features and interactive elements, opens new pathways for enhancing food safety, improving supply chain transparency, and fostering deeper consumer engagement.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Innovation in Biodegradable & Compostable Packaging | +2.2% | Global, high demand in environmentally conscious regions | Mid to Long-term (2026-2033) |

| Growth in Emerging Markets with Expanding Food Service | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Development of Smart Packaging for Enhanced Food Safety & Traceability | +1.0% | North America, Europe | Long-term (2028-2033) |

| Strategic Partnerships for R&D in Sustainable Materials | +0.9% | Global | Mid to Long-term (2026-2033) |

Food Service Packaging Market Challenges Impact Analysis

The food service packaging market, while dynamic, encounters several formidable challenges that necessitate strategic responses from industry players. One significant challenge is the inherent complexity and cost associated with transitioning from traditional, often cheaper, plastic-based packaging to more sustainable alternatives. Manufacturers face dilemmas in balancing the demand for eco-friendly materials with the need to maintain cost-effectiveness and operational efficiency, especially in a price-sensitive market where consumers and businesses seek affordable solutions.

Another major hurdle involves the limitations of existing recycling infrastructure globally. Many innovative multi-material and compostable packaging solutions cannot be effectively processed by current recycling facilities, leading to confusion among consumers and ultimately undermining the intended environmental benefits. This gap between material innovation and end-of-life management systems presents a systemic challenge that requires collaborative efforts across the value chain, from producers to waste management authorities and policymakers, to establish viable circular pathways.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Recycling Infrastructure Limitations for Complex Packaging | -1.2% | Global, particularly developing regions | Long-term (2025-2033) |

| Balancing Cost-Effectiveness with Sustainability Requirements | -0.9% | Global | Short to Mid-term (2025-2030) |

| Consumer Education & Perception Regarding New Materials | -0.7% | Global | Mid to Long-term (2026-2033) |

| Maintaining Food Integrity & Shelf-Life with Eco-Friendly Alternatives | -0.6% | Global | Ongoing (2025-2033) |

Food Service Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Food Service Packaging Market, offering a detailed examination of its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges. The scope encompasses a thorough evaluation of various material types, product categories, and applications across key geographical regions, providing a holistic view of the market's current state and future prospects. It includes a competitive landscape analysis, profiling leading players and highlighting their strategies and market positions to offer actionable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 105.0 Billion |

| Market Forecast in 2033 | USD 173.8 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor PLC, Berry Global Inc., Dart Container Corporation, Huhtamaki Oyj, WestRock Company, Graphic Packaging International, LLC, Mondi Group, DS Smith Plc, Sabert Corporation, Genpak LLC, Pactiv Evergreen Inc., Sonoco Products Company, Sealed Air Corporation, Novolex Holdings, LLC, Reynolds Group Holdings Limited, International Paper Company, BillerudKorsnäs AB, Greif, Inc., ProAmpac LLC, Silgan Holdings Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Food Service Packaging Market is intricately segmented across various dimensions to provide a granular understanding of its dynamics and growth prospects. This segmentation allows for precise analysis of consumer preferences, material demands, and application-specific requirements, highlighting areas of high potential and competitive intensity. The market is primarily broken down by material type, product form, and end-use application, each exhibiting distinct growth drivers and trends that collectively shape the overall market landscape.

Analyzing these segments provides clarity on where innovation is most concentrated and where investment opportunities lie. For instance, the shift towards sustainable materials is evident across all product types, while the rapid expansion of food delivery services is significantly impacting the demand for specialized container solutions. Understanding these segment-specific nuances is critical for stakeholders to develop targeted strategies and capitalize on emerging market opportunities.

- By Material: This segment includes Plastic (Polypropylene (PP), Polyethylene (PE), Polyethylene Terephthalate (PET), Polystyrene (PS), and Other Plastics), Paper & Paperboard, Metal, Glass, Bio-plastic, and Other materials. Paper & paperboard and bio-plastics are experiencing rapid growth due to sustainability mandates.

- By Product: Categorization covers Cups & Bowls, Containers (Clamshells, Trays, Deli Containers), Plates, Cutlery (Forks, Spoons, Knives), Trays, Wraps & Films, Bags, and Other products such as napkins, lids, and straws. Containers and cups & bowls dominate due to their widespread use in takeaway and delivery.

- By Application: This segment differentiates demand from Restaurants (Full-Service Restaurants (FSR) and Quick Service Restaurants (QSR)), Catering services, Cafes & Bakeries, Institutional Food Service (e.g., hospitals, schools, corporate canteens), Vending Machines, and the rapidly expanding Delivery & Takeaway Services. The delivery & takeaway segment is a major growth catalyst.

Regional Highlights

- North America: This region represents a mature and significant market for food service packaging, characterized by high demand for convenience, a strong emphasis on brand differentiation, and increasing adoption of sustainable packaging solutions. Strict regulations and strong consumer awareness drive innovation towards eco-friendly alternatives. The robust food delivery ecosystem further fuels market expansion.

- Europe: Europe is at the forefront of sustainable packaging innovation, driven by stringent environmental regulations, particularly concerning single-use plastics, and a strong consumer preference for eco-friendly products. The region is actively transitioning towards a circular economy model, encouraging the development and adoption of recyclable, compostable, and reusable packaging.

- Asia Pacific (APAC): Positioned as the fastest-growing region, APAC benefits from rapid urbanization, rising disposable incomes, and the swift expansion of its food service industry. Countries like China and India are witnessing a surge in quick-service restaurants and food delivery platforms, leading to substantial demand for cost-effective and innovative packaging solutions, with an increasing focus on sustainability.

- Latin America: This region exhibits promising growth, propelled by evolving consumer lifestyles, increasing urbanization, and the expansion of the organized retail and food service sectors. While price sensitivity remains a factor, there is a growing recognition and demand for modern, convenient, and increasingly sustainable packaging options across various applications.

- Middle East & Africa (MEA): The MEA region is experiencing rapid development in its food service and hospitality sectors, fueled by tourism, urbanization, and a young demographic. This growth generates substantial demand for food service packaging. There is a burgeoning interest in sustainable solutions, though cost-effectiveness and infrastructure development remain key considerations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Service Packaging Market.- Amcor PLC

- Berry Global Inc.

- Dart Container Corporation

- Huhtamaki Oyj

- WestRock Company

- Graphic Packaging International, LLC

- Mondi Group

- DS Smith Plc

- Sabert Corporation

- Genpak LLC

- Pactiv Evergreen Inc.

- Sonoco Products Company

- Sealed Air Corporation

- Novolex Holdings, LLC

- Reynolds Group Holdings Limited

- International Paper Company

- BillerudKorsnäs AB

- Greif, Inc.

- ProAmpac LLC

- Silgan Holdings Inc.

Frequently Asked Questions

What are the main growth drivers for the Food Service Packaging Market?

The primary growth drivers include the increasing global demand for convenience foods, the rapid expansion of food delivery and takeaway services, rising urbanization and changing consumer lifestyles, and growing disposable incomes, particularly in emerging markets. These factors collectively boost the need for efficient and accessible packaging solutions.

How is sustainability impacting the Food Service Packaging Market?

Sustainability is profoundly impacting the market by driving innovation towards eco-friendly materials such as biodegradable, compostable, and recyclable options. It is also leading to stricter environmental regulations, consumer demand for greener products, and a shift towards circular economy models, influencing product development and market strategies significantly.

What role does technology play in the future of Food Service Packaging?

Technology, including AI and smart packaging, is crucial for the future. It enables enhanced food safety through traceability and monitoring, optimizes supply chain logistics, allows for personalized packaging designs, and improves efficiency in manufacturing and waste management. Digital integration is key for consumer engagement and operational excellence.

Which regions are showing the most significant growth in this market?

The Asia Pacific (APAC) region is currently exhibiting the most significant growth due to rapid urbanization, increasing disposable incomes, and the burgeoning food service and e-commerce sectors in countries like China and India. Latin America and the Middle East & Africa are also emerging as high-growth markets.

What are the primary challenges faced by the Food Service Packaging Industry?

Key challenges include stringent environmental regulations on single-use plastics, the high cost of sustainable packaging materials compared to traditional options, volatility in raw material prices, and the limitations of existing recycling and waste management infrastructure, particularly for complex multi-material packaging.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted