Food Processing Equipment Market

Food Processing Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708225 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Food Processing Equipment Market Size

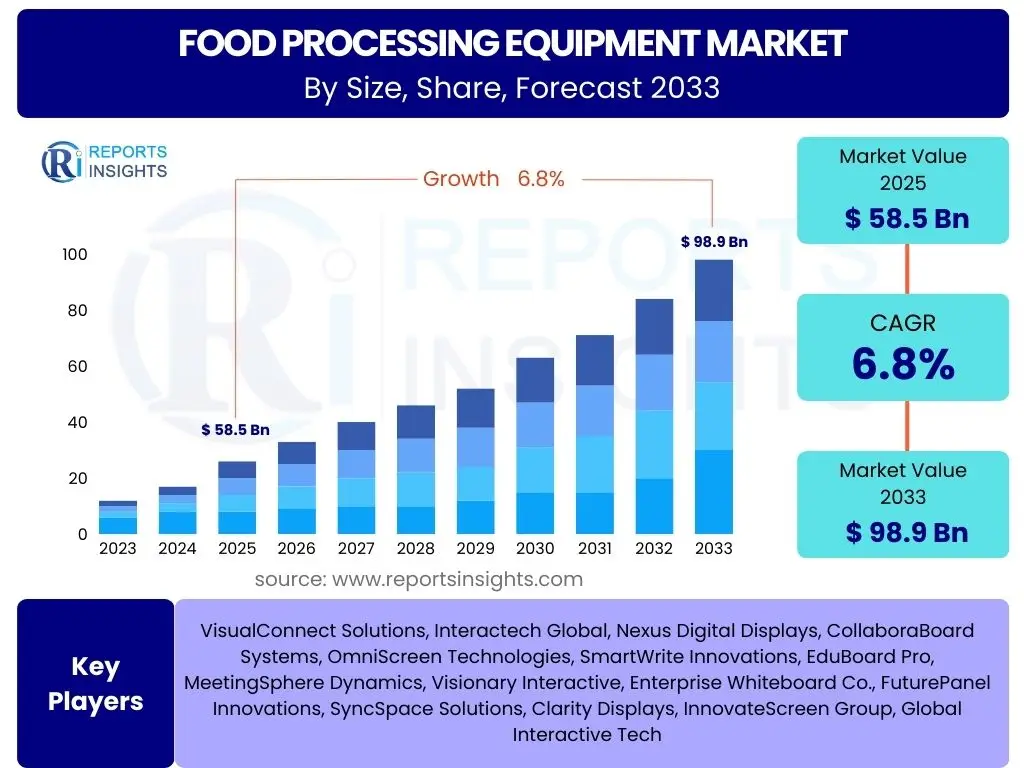

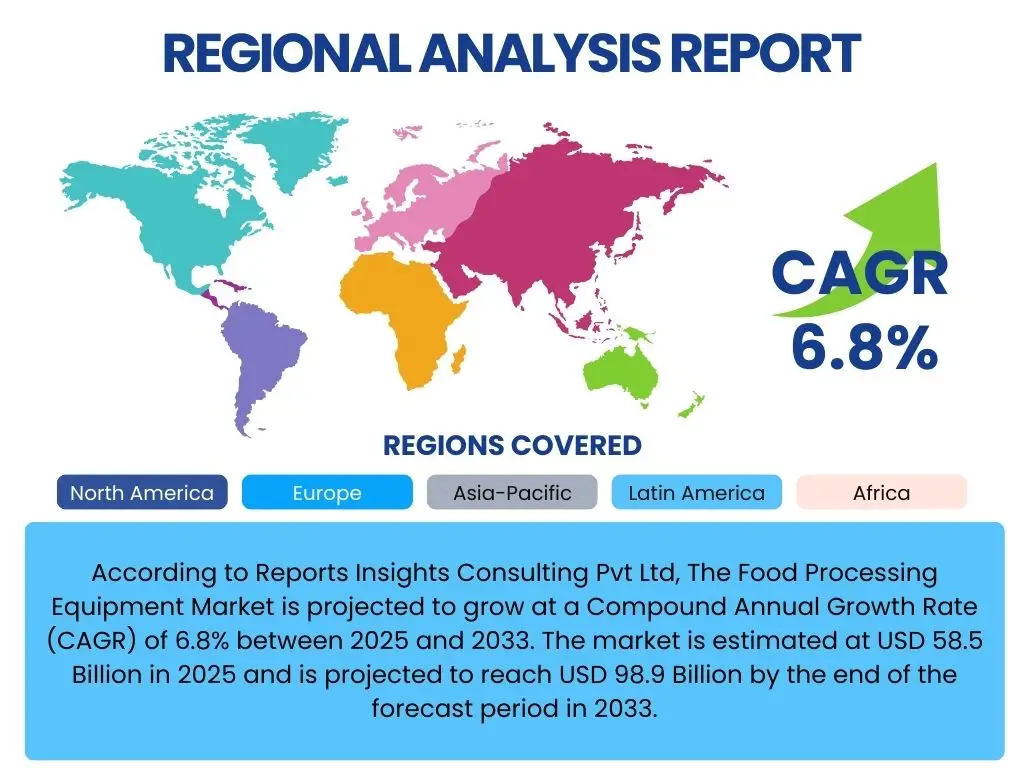

According to Reports Insights Consulting Pvt Ltd, The Food Processing Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 58.5 Billion in 2025 and is projected to reach USD 98.9 Billion by the end of the forecast period in 2033.

Key Food Processing Equipment Market Trends & Insights

User queries regarding the food processing equipment market frequently highlight an intense focus on operational efficiency, stringent food safety standards, and the increasing demand for sustainable practices. Manufacturers are continuously seeking solutions that not only enhance production output but also minimize waste and energy consumption. This has led to a notable shift towards advanced automation and integration of smart technologies throughout the processing line, aimed at reducing manual intervention and optimizing resource utilization. Furthermore, the growing global population and evolving consumer preferences for diverse and convenient food products are compelling the industry to adopt more flexible and adaptable equipment capable of handling a wider range of ingredients and production scales.

Another significant area of interest for market participants revolves around the customization and personalization of food products. This trend, driven by health-conscious consumers and specific dietary requirements, necessitates processing equipment that offers greater precision and control over ingredients and formulation. The industry is also witnessing a surge in the adoption of modular designs and smaller footprint machinery, particularly beneficial for small to medium-sized enterprises (SMEs) and specialized food production. These developments underscore a dynamic market that is rapidly responding to both technological advancements and shifting consumer demands, prioritizing innovation that supports both productivity and adaptability in food manufacturing.

- Increased adoption of automation and robotics to enhance efficiency and reduce labor costs.

- Rising demand for equipment enabling sustainable food production, including water and energy efficiency.

- Focus on advanced food safety and quality control technologies, such as hygienic design and real-time monitoring.

- Growth in plant-based food processing, driving innovation in extrusion and texture modification equipment.

- Customization and modularity in equipment design to cater to diverse production needs and market demands.

- Integration of IoT and data analytics for predictive maintenance and optimized operational performance.

AI Impact Analysis on Food Processing Equipment

User inquiries about Artificial Intelligence in food processing equipment frequently explore its potential to revolutionize operational efficiency, quality control, and predictive maintenance. Stakeholders are keen to understand how AI algorithms can interpret vast datasets from sensors and machinery to identify anomalies, optimize process parameters, and reduce downtime. The primary expectation is that AI will move beyond simple automation, enabling machines to learn, adapt, and make autonomous decisions, thereby significantly enhancing productivity and minimizing human error. Concerns often include the initial investment costs, the complexity of integration with legacy systems, and the need for a skilled workforce capable of managing and interpreting AI-driven insights.

Beyond operational improvements, the impact of AI is also being closely examined in areas such as food safety and new product development. AI-powered vision systems can detect contaminants or quality defects with unparalleled precision, far exceeding human capabilities, ensuring stricter adherence to safety regulations. Moreover, AI can analyze consumer trends and ingredient interactions to assist in the rapid development and scaling of novel food products, shortening time-to-market. The industry anticipates that AI will foster a more resilient, adaptive, and precise food processing ecosystem, albeit requiring careful strategic planning for adoption and comprehensive data infrastructure development.

- Enhanced predictive maintenance through machine learning algorithms analyzing equipment performance data.

- Optimized process control and resource management (energy, water, raw materials) via AI-driven analytics.

- Improved quality assurance and food safety with AI-powered vision systems for defect and contaminant detection.

- Automated decision-making in production lines, leading to higher throughput and reduced human intervention.

- Streamlined supply chain management and inventory optimization using AI for demand forecasting.

- Acceleration of new product development by leveraging AI for ingredient formulation and consumer trend analysis.

Key Takeaways Food Processing Equipment Market Size & Forecast

Common user questions regarding market size and forecast consistently point to an interest in understanding the primary growth catalysts and the overarching direction of the industry. The most significant takeaway is the market's robust growth trajectory, largely fueled by escalating global demand for processed and convenience foods, coupled with a relentless pursuit of operational efficiencies through technological advancements. Investors and industry players are particularly focused on the segments exhibiting the highest growth potential, such as automation, sustainable processing solutions, and equipment catering to evolving dietary preferences like plant-based alternatives. This indicates a strategic shift towards innovation that addresses both market demand and environmental responsibility.

Another crucial insight derived from market inquiries is the increasing importance of emerging economies as key growth regions. These regions are experiencing rapid urbanization, rising disposable incomes, and a concurrent expansion of their food processing capabilities, presenting substantial opportunities for equipment manufacturers. The forecast underscores a future where digital integration, artificial intelligence, and advanced sensor technologies will not just be supplementary features but fundamental components of modern food processing equipment. Consequently, companies investing in research and development to incorporate these advanced technologies are poised for sustained competitive advantage and market leadership.

- Significant market expansion anticipated due to increasing global demand for processed and convenience foods.

- Technological advancements, particularly in automation, AI, and IoT, are critical drivers of market growth.

- Emerging economies in Asia Pacific and Latin America are poised for substantial growth in food processing investments.

- Emphasis on equipment designed for enhanced food safety, traceability, and adherence to stringent regulations.

- Growing focus on sustainable and energy-efficient processing solutions to meet environmental targets.

- Rising consumer demand for diverse and specialized food products is driving innovation in flexible and customizable equipment.

Food Processing Equipment Market Drivers Analysis

The global food processing equipment market is significantly propelled by several interconnected factors that collectively enhance demand and drive innovation. A primary driver is the continuous growth in global population coupled with increasing urbanization, leading to a higher consumption of processed and convenience foods. As lifestyles become more fast-paced, consumers increasingly rely on ready-to-eat meals, packaged snacks, and other value-added food products, necessitating advanced equipment for efficient and large-scale production. This trend is particularly pronounced in developing economies, where disposable incomes are rising, and food habits are evolving towards westernized diets.

Furthermore, stringent food safety regulations and quality standards imposed by governments and international bodies worldwide are compelling food processors to invest in modern, hygienic, and precise equipment. Compliance with these standards often requires automated systems that minimize human contact, ensure consistent quality, and allow for comprehensive traceability. Technological advancements, especially in automation, robotics, and digital integration (IoT, AI), also act as powerful drivers, enabling manufacturers to achieve higher operational efficiency, reduce labor costs, and optimize resource utilization. These innovations offer substantial returns on investment by improving productivity and reducing waste, thus motivating market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Demand for Processed and Convenience Foods | +2.5% | Global, particularly Asia Pacific, Latin America | Short-term to Long-term |

| Stringent Food Safety Regulations and Quality Standards | +1.8% | North America, Europe, Developed Asia Pacific | Mid-term to Long-term |

| Advancements in Automation and Robotics Technologies | +2.0% | Global, especially developed economies | Mid-term to Long-term |

| Rising Population and Urbanization | +1.5% | Emerging Markets (China, India, Brazil) | Long-term |

| Growth in the Fast Food and Catering Industries | +1.0% | Global | Short-term to Mid-term |

Food Processing Equipment Market Restraints Analysis

Despite robust growth drivers, the food processing equipment market faces several significant restraints that could impede its expansion. One major impediment is the high capital investment required for acquiring and installing advanced processing machinery. Many small and medium-sized enterprises (SMEs), particularly in developing regions, find it challenging to allocate the substantial funds necessary for state-of-the-art equipment, often leading to reliance on older, less efficient technologies. This high entry barrier can slow down the adoption of innovative solutions and hinder market penetration in certain segments.

Another critical restraint is the fluctuating prices of raw materials and energy. Food processing is an energy-intensive industry, and volatility in energy costs directly impacts operational expenses, making it difficult for manufacturers to maintain profit margins and plan long-term investments. Similarly, the availability and cost of specialized components and raw materials for equipment manufacturing can be unpredictable, leading to production delays and increased costs. Furthermore, the shortage of skilled labor required to operate and maintain sophisticated processing equipment presents a significant challenge, especially with the increasing complexity of automated systems. This lack of expertise can lead to inefficient operation, higher maintenance costs, and reduced productivity.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment Requirements | -1.2% | Global, particularly developing regions | Long-term |

| Volatility in Raw Material and Energy Prices | -1.0% | Global | Short-term to Mid-term |

| Shortage of Skilled Labor for Operation and Maintenance | -0.8% | Developed regions, manufacturing hubs | Mid-term |

| Strict Environmental Regulations and Disposal Costs | -0.7% | Europe, North America | Long-term |

| Increasing Competition from Local Manufacturers | -0.5% | Asia Pacific, Latin America | Mid-term |

Food Processing Equipment Market Opportunities Analysis

The food processing equipment market is ripe with opportunities driven by evolving consumer preferences and technological advancements. One significant opportunity lies in the growing demand for plant-based food products, including meat alternatives, dairy substitutes, and vegan snacks. This trend necessitates specialized processing equipment capable of handling novel ingredients and achieving desired textures and flavors, creating a new niche for manufacturers to innovate and expand their product portfolios. Companies that invest in research and development for extrusion, blending, and fermentation technologies tailored to plant-based ingredients are well-positioned to capitalize on this rapidly expanding market segment.

Furthermore, the increasing focus on sustainability and waste reduction presents substantial opportunities for equipment manufacturers. Demand for energy-efficient machinery, water-saving technologies, and systems that facilitate byproduct utilization or valorization is growing. Solutions that support circular economy principles within food production, such as advanced sorting, recovery, and recycling equipment, will gain significant market traction. Additionally, the digitalization of food processing, including the integration of the Internet of Things (IoT), AI, and Big Data analytics, offers avenues for creating smart, connected factories. These technologies enable predictive maintenance, real-time process optimization, and enhanced traceability, providing competitive advantages and opening doors for new service models and revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Plant-Based and Alternative Protein Products | +1.5% | North America, Europe, Asia Pacific | Mid-term to Long-term |

| Expansion into Emerging Markets and Developing Economies | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Long-term |

| Integration of IoT, AI, and Advanced Analytics for Smart Manufacturing | +1.3% | Global | Mid-term to Long-term |

| Development of Sustainable and Eco-friendly Processing Solutions | +1.0% | Europe, North America | Mid-term to Long-term |

| Customization and Personalization of Food Products | +0.8% | Developed markets | Short-term to Mid-term |

Food Processing Equipment Market Challenges Impact Analysis

The food processing equipment market encounters several critical challenges that require strategic navigation for sustained growth. Rapid technological advancements, while offering opportunities, also pose a challenge in terms of keeping pace with innovation and managing the obsolescence of existing equipment. Manufacturers must continuously invest in research and development to remain competitive, and food processors face the dilemma of frequent upgrades to maintain efficiency and meet evolving industry standards. This can lead to increased capital expenditure and operational complexities, particularly for companies with extensive legacy systems.

Moreover, the increasing complexity of global supply chains and geopolitical instabilities presents significant challenges, impacting the availability of raw materials, components, and logistics. Disruptions such as trade wars, pandemics, or regional conflicts can lead to delays, increased costs, and uncertainties in equipment manufacturing and delivery. Furthermore, ensuring robust cybersecurity measures for increasingly connected and automated processing systems is a growing concern. As equipment integrates more IoT and AI technologies, the risk of cyber threats that could compromise operational integrity or sensitive data becomes more pronounced, requiring substantial investment in secure digital infrastructure and protocols.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Constant Upgrades | -0.9% | Global | Mid-term |

| Global Supply Chain Disruptions and Geopolitical Instabilities | -1.1% | Global | Short-term to Mid-term |

| Ensuring Cybersecurity for Connected Manufacturing Systems | -0.6% | Developed Economies | Long-term |

| Maintaining Regulatory Compliance Across Diverse Jurisdictions | -0.7% | Global | Long-term |

| High Research & Development Costs for Innovation | -0.5% | Global | Long-term |

Food Processing Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global food processing equipment sector, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers a historical period of five years, leading up to a forecast period of eight years, providing a robust framework for strategic decision-making. The report meticulously evaluates market sizing, growth drivers, restraints, opportunities, and challenges, incorporating the latest technological advancements and evolving consumer demands. Furthermore, it highlights key trends such as automation, sustainability, and digitalization impacting the industry's future trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 58.5 Billion |

| Market Forecast in 2033 | USD 98.9 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GEA Group, JBT Corporation, SPX FLOW, Krones AG, Bühler AG, Tetra Pak, Marel hf, tna solutions, Heat and Control, Inc., Alfa Laval, Reiser, ANKO Food Machine Co. Ltd., IMA Group, Robert Bosch GmbH, Hosokawa Micron Corporation, Middleby Corporation, Duravant LLC, F. H. Schule Mühlenbau GmbH, TOMRA Systems ASA, Electrolux Professional. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The food processing equipment market is meticulously segmented to provide a granular view of its diverse components and their respective growth trajectories. This segmentation helps in identifying specific areas of opportunity and understanding the varying needs across the food industry. The market is primarily categorized by type of equipment, which includes processing equipment for various stages of food transformation, packaging equipment crucial for product protection and shelf life, and ancillary equipment supporting overall operations. Each of these broad categories further breaks down into specialized machinery addressing specific functions within the food manufacturing process, reflecting the complexity and specialization required in modern food production.

Further segmentation is based on the application or end-product, encompassing major food categories such as meat, poultry & seafood, dairy products, bakery & confectionery, and beverages, among others. This categorization highlights how different food sectors drive demand for specific types of equipment, influencing design, capacity, and functionality requirements. Operational modes, distinguishing between automatic, semi-automatic, and manual systems, also form a key segment, reflecting varying levels of automation adopted by processors. The modality of operation, whether batch or continuous, offers another layer of insight into production scales and operational preferences. Collectively, these segmentations provide a comprehensive framework for analyzing market trends, competitive landscapes, and strategic entry points.

- By Type:

- Processing Equipment: Mixers, Blenders, Cutters, Slicers, Freezers, Ovens, Fryers, Homogenizers, Emulsifiers, Extruders, Separators, Heat Exchangers.

- Packaging Equipment: Fillers, Sealers, Wrappers, Labelers, Cartoners, Palletizers.

- Ancillary Equipment: Cleaning Systems (CIP/SIP), Sorting Equipment, Conveying Systems, Material Handling, Inspection Systems.

- By Application/End-Product:

- Meat, Poultry & Seafood

- Dairy Products

- Bakery & Confectionery

- Beverages (Alcoholic & Non-alcoholic)

- Fruits & Vegetables

- Grains & Pulses

- Prepared Foods

- Oils & Fats

- Snacks & Savories

- Baby Food

- By Operation:

- Automatic

- Semi-automatic

- Manual

- By Modality:

- Batch

- Continuous

Regional Highlights

The global food processing equipment market exhibits significant regional variations in growth, adoption rates, and specific demands, driven by diverse economic conditions, consumer preferences, and regulatory environments. Asia Pacific stands out as the fastest-growing region, propelled by its large and expanding population, rapid urbanization, increasing disposable incomes, and the flourishing food processing industry in countries like China, India, and Southeast Asian nations. This region is witnessing substantial investments in modernizing food production facilities, driven by both domestic consumption and export opportunities. The demand here spans a wide range of equipment, from basic processing machinery to advanced automated systems, reflecting varying stages of industrial development.

North America and Europe represent mature markets characterized by stringent food safety regulations, high labor costs, and a strong emphasis on automation, energy efficiency, and sustainable practices. In these regions, the focus is heavily on upgrading existing infrastructure with high-tech, precision equipment that integrates AI, IoT, and advanced robotics to enhance productivity, ensure food traceability, and reduce environmental impact. The demand for equipment catering to plant-based and specialized dietary products is also particularly strong here. Latin America and the Middle East & Africa, while smaller in market share, are emerging as promising regions due to growing populations, increasing foreign investments in food infrastructure, and evolving consumer tastes, creating demand for both foundational and advanced processing solutions.

- North America: Dominates in advanced automation, smart factory solutions, and equipment for health and wellness products, driven by high labor costs and stringent food safety standards.

- Europe: Strong focus on sustainable processing, energy efficiency, and high-quality, precision machinery, with significant demand for equipment for dairy, bakery, and beverage sectors.

- Asia Pacific (APAC): Fastest-growing region, characterized by massive market potential due to population growth, rising disposable incomes, and expanding domestic food processing industries, particularly in China and India.

- Latin America: Emerging market with increasing investment in food processing infrastructure, driven by urbanization and growing demand for packaged foods, offering opportunities for both basic and semi-automatic equipment.

- Middle East and Africa (MEA): Gradually developing market, with growth fueled by population increase, government initiatives in food security, and diversification of food industries, creating demand for efficient and hygienic processing solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Processing Equipment Market.- GEA Group

- JBT Corporation

- SPX FLOW

- Krones AG

- Bühler AG

- Tetra Pak (part of Tetra Laval)

- Marel hf

- tna solutions Pty Ltd.

- Heat and Control, Inc.

- Alfa Laval

- Reiser

- ANKO Food Machine Co. Ltd.

- IMA Group

- Robert Bosch GmbH (Packaging Technology division, now Syntegon Technology)

- Hosokawa Micron Corporation

- Middleby Corporation

- Duravant LLC

- F. H. Schule Mühlenbau GmbH

- TOMRA Systems ASA

- Electrolux Professional

Frequently Asked Questions

What is the projected growth rate of the Food Processing Equipment Market?

The Food Processing Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033.

What are the primary drivers of the Food Processing Equipment Market?

Key drivers include increasing global demand for processed and convenience foods, stringent food safety regulations, and technological advancements in automation and robotics.

How is AI impacting the Food Processing Equipment industry?

AI is transforming the industry through enhanced predictive maintenance, optimized process control, improved quality assurance via vision systems, and accelerated new product development.

Which region is expected to lead market growth for Food Processing Equipment?

Asia Pacific is anticipated to be the fastest-growing region, driven by its large population, rapid urbanization, and increasing investments in food processing infrastructure.

What are the main challenges faced by the Food Processing Equipment Market?

Major challenges include high capital investment requirements, volatility in raw material and energy prices, a shortage of skilled labor, and rapid technological obsolescence necessitating continuous upgrades.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted