Food Phosphate Market

Food Phosphate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704107 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

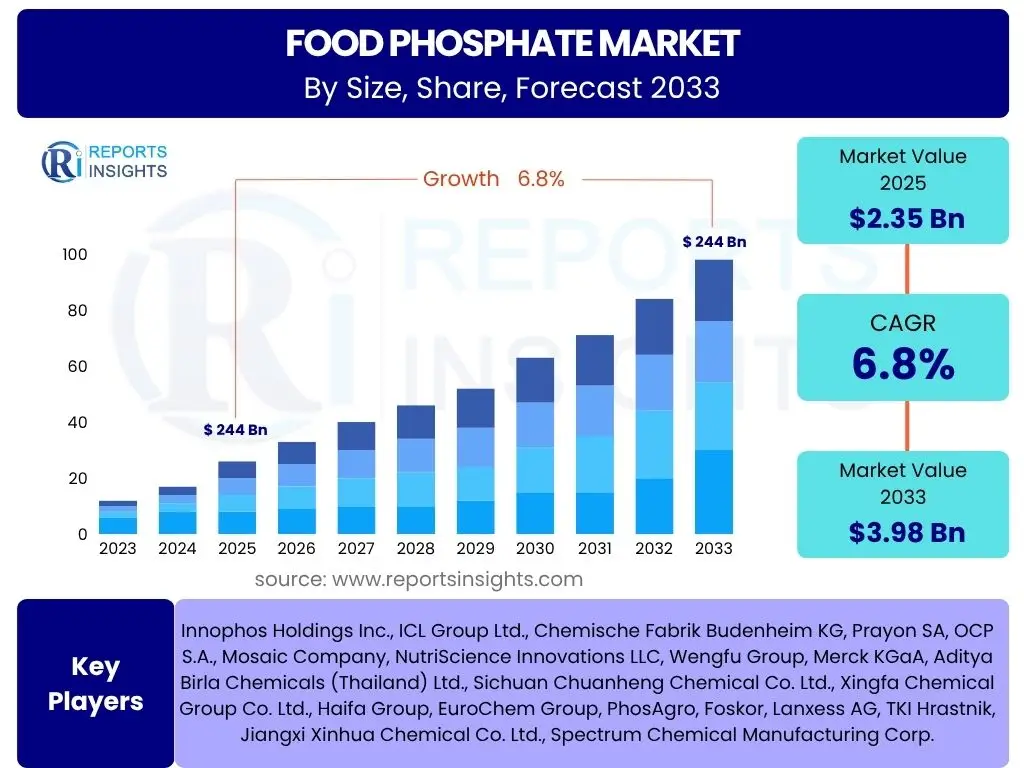

Food Phosphate Market Size

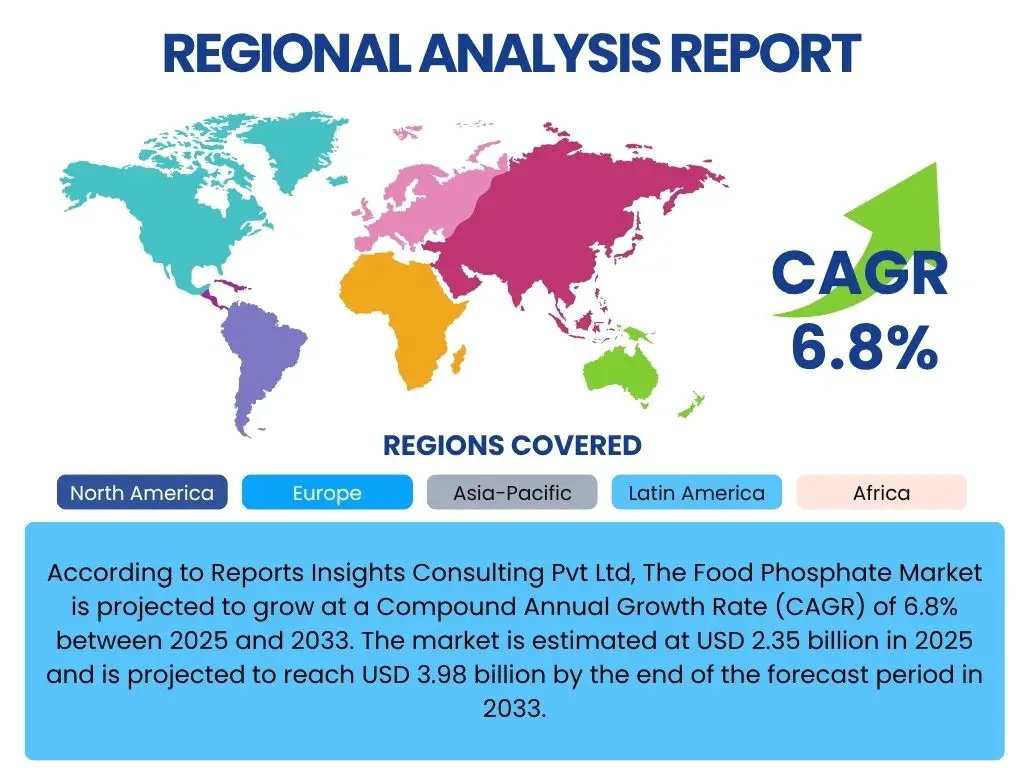

According to Reports Insights Consulting Pvt Ltd, The Food Phosphate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.35 billion in 2025 and is projected to reach USD 3.98 billion by the end of the forecast period in 2033.

Key Food Phosphate Market Trends & Insights

The food phosphate market is witnessing significant transformation driven by evolving consumer demands and technological advancements. A primary trend involves the increasing preference for convenience and processed foods, which rely heavily on phosphates for texture, preservation, and stability. Additionally, the growing global population and urbanization contribute to a higher demand for packaged and shelf-stable food products, further bolstering the market for food phosphates. Manufacturers are also focusing on developing new phosphate formulations that align with "clean label" trends, aiming to offer ingredients perceived as more natural or less processed, despite the technical necessity of phosphates in many applications.

Another crucial insight is the expanding application scope of food phosphates beyond traditional meat and dairy industries. There is a rising adoption in plant-based alternatives, baked goods, and functional beverages, where phosphates play roles in leavening, emulsification, and nutrient fortification. The market is also experiencing a shift towards more sustainable and efficient production methods for phosphates, driven by environmental concerns and the need for cost optimization. Innovation in phosphate blends that offer multi-functional benefits, such as improved solubility or enhanced mineral bioavailability, represents a key area of research and development, addressing specific formulation challenges across various food matrices.

- Rising demand for convenience and processed foods globally.

- Growing consumer preference for "clean label" and naturally derived ingredients.

- Expansion of food phosphate applications in plant-based food products.

- Increased focus on functional food products and nutritional fortification.

- Technological advancements in phosphate synthesis and blend formulation.

- Emphasis on sustainable production practices and resource efficiency.

- Urbanization and increasing disposable incomes driving consumption of packaged foods.

AI Impact Analysis on Food Phosphate

Artificial intelligence (AI) is poised to revolutionize various facets of the food phosphate industry, from raw material sourcing to final product formulation and supply chain management. Users frequently inquire about AI's potential to enhance efficiency, reduce costs, and improve product quality. AI-driven predictive analytics can optimize inventory management and demand forecasting for phosphate suppliers and food manufacturers, minimizing waste and ensuring timely availability of ingredients. Furthermore, AI algorithms can analyze complex data sets related to raw material quality, helping identify optimal sourcing strategies and ensuring consistency in phosphate characteristics, which is critical for food product performance.

In the realm of research and development, AI offers significant potential for accelerating the discovery and optimization of new food phosphate blends. Machine learning models can predict the functional properties of novel phosphate combinations, reducing the need for extensive physical prototyping and experimental trials. This allows for faster innovation in developing phosphates with enhanced emulsifying, chelating, or leavening capabilities, tailored to specific food applications. Additionally, AI-powered systems can enhance quality control processes, leveraging computer vision and sensor data to detect impurities or inconsistencies in phosphate batches, thereby ensuring product safety and compliance with stringent food regulations, which is a common user concern regarding ingredient quality.

- Optimized supply chain and logistics through AI-driven demand forecasting and inventory management.

- Enhanced quality control and impurity detection using AI-powered vision systems and data analytics.

- Accelerated research and development of new phosphate formulations via machine learning for property prediction.

- Improved process efficiency in manufacturing through AI-driven automation and predictive maintenance.

- Personalized formulation recommendations for food manufacturers based on specific product requirements and constraints.

Key Takeaways Food Phosphate Market Size & Forecast

The Food Phosphate market is set for robust expansion over the forecast period, driven by fundamental shifts in global dietary patterns and the evolving landscape of food processing. A primary takeaway is the consistent growth trajectory, indicative of phosphates' indispensable role across a wide array of food applications. The projected Compound Annual Growth Rate (CAGR) of 6.8% underscores a healthy market expansion, fueled by increasing global population, rising demand for convenience foods, and the continuous innovation in food product development that necessitates the functional properties of phosphates. This growth is not merely incremental but represents a significant market opportunity for stakeholders across the value chain, from raw material suppliers to food product manufacturers.

Another critical insight reveals the strategic importance of geographical markets, with Asia Pacific expected to emerge as a key growth engine due to its large population base, rapid urbanization, and burgeoning processed food industry. Furthermore, the market's resilience is notable, adapting to challenges such as regulatory scrutiny and consumer health concerns through advancements in phosphate formulations and a focus on product safety. The forecast signifies that despite potential headwinds, the foundational demand for food phosphates in improving food texture, stability, preservation, and nutritional value will continue to drive market expansion, making it a pivotal sector within the broader food ingredients industry.

- Consistent and significant market growth projected at a CAGR of 6.8% through 2033.

- Food phosphates are integral to the stability, texture, and preservation of modern food products.

- Asia Pacific is anticipated to be a primary growth driver due to rising processed food consumption.

- Continuous innovation in phosphate formulations addresses evolving consumer preferences and regulatory requirements.

- The market is driven by fundamental demographic shifts and consumer demands for convenience.

Food Phosphate Market Drivers Analysis

The global Food Phosphate market is primarily propelled by the burgeoning demand for processed and convenience foods, which heavily rely on phosphates for preservation, emulsification, and texture enhancement. Urbanization and changing lifestyles have led to increased consumption of ready-to-eat meals, processed meat products, baked goods, and dairy, all of which are significant applications for various types of food phosphates. The functional versatility of phosphates, acting as leavening agents, buffering agents, sequestrants, and nutritional supplements, makes them indispensable across a wide spectrum of food manufacturing processes, thus fueling their market growth globally.

Furthermore, the expanding global population and rising disposable incomes, particularly in emerging economies, are contributing to a greater demand for diverse and higher-quality food products. This demographic shift, coupled with an increasing awareness of food safety and shelf-life extension, accentuates the need for effective food additives like phosphates. Innovations in food product development, including the growth of plant-based foods and functional beverages, also create new avenues for phosphate applications. As food manufacturers strive to meet specific sensory and nutritional profiles, the tailored functionalities offered by different phosphate compounds become crucial, driving continuous demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for processed & convenience foods | +2.1% | Global, particularly Asia Pacific & North America | Short to Long-term (2025-2033) |

| Increasing global population & urbanization | +1.8% | Emerging Economies (e.g., China, India, Brazil) | Long-term (2025-2033) |

| Expansion of the meat and poultry processing industry | +1.5% | North America, Europe, Asia Pacific | Mid-term (2025-2030) |

| Rise in demand for bakery and dairy products | +1.3% | Global, especially Europe & Asia Pacific | Short to Mid-term (2025-2028) |

| Technological advancements in food processing & preservation | +1.0% | Developed Economies | Long-term (2028-2033) |

Food Phosphate Market Restraints Analysis

Despite robust growth, the Food Phosphate market faces several significant restraints, primarily stemming from increasing regulatory scrutiny and consumer health concerns regarding certain food additives. Governments and health organizations worldwide are implementing stricter regulations on the usage levels and types of food phosphates, driven by studies linking high phosphate intake to potential health issues, particularly in vulnerable populations. This has led to a push for reduced phosphate formulations or a search for alternative ingredients, especially in regions with stringent food safety standards, creating challenges for manufacturers.

Another key restraint is the volatility in the prices of raw materials, such as phosphoric acid and various mineral salts, which are essential for phosphate production. Geopolitical tensions, supply chain disruptions, and fluctuations in energy costs can significantly impact the cost of production, subsequently affecting the profitability of manufacturers and potentially leading to higher end-product prices. Additionally, the ongoing "clean label" movement, where consumers increasingly prefer food products with fewer artificial ingredients and a simpler ingredient list, poses a challenge for phosphates that are often perceived as industrial additives, despite their crucial functional roles. This perception issue necessitates clear communication and potential innovation in sourcing or processing to align with consumer expectations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing regulatory scrutiny & health concerns regarding phosphate intake | -1.5% | Europe, North America | Mid to Long-term (2025-2033) |

| Volatility in raw material prices (e.g., phosphoric acid) | -1.2% | Global | Short to Mid-term (2025-2029) |

| Negative consumer perception and "clean label" trend | -1.0% | Developed Countries (e.g., US, Germany, UK) | Long-term (2027-2033) |

| Competition from alternative ingredients | -0.8% | Global | Mid-term (2026-2031) |

| Environmental regulations on phosphate production waste | -0.5% | China, India, EU | Long-term (2028-2033) |

Food Phosphate Market Opportunities Analysis

The Food Phosphate market is ripe with opportunities, particularly in the burgeoning plant-based food sector. As consumer interest in vegan and vegetarian diets continues to surge globally, there is an escalating demand for plant-based meat substitutes, dairy alternatives, and baked goods, all of which require specific functional ingredients like phosphates to achieve desirable texture, stability, and nutritional profiles. Phosphates can enhance the emulsification of plant proteins, improve the leavening in gluten-free baked goods, and act as buffering agents in plant-based beverages, presenting a significant growth avenue for manufacturers capable of developing tailored phosphate solutions for these innovative product categories.

Another substantial opportunity lies in emerging markets, especially in Asia Pacific, Latin America, and Africa. These regions are experiencing rapid economic growth, increasing urbanization, and a shift towards Westernized dietary patterns that include a greater consumption of processed and packaged foods. The untapped potential in these markets, characterized by a rising middle class and evolving retail infrastructure, offers considerable scope for market penetration and expansion. Furthermore, continuous innovation in the development of new, multifunctional phosphate blends that offer enhanced efficacy at lower concentrations or align with "natural" ingredient perceptions could unlock premium market segments and differentiate products in a competitive landscape. The focus on nutrient fortification, particularly calcium and phosphorus, in various food products also provides an ongoing opportunity for specific phosphate types.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising demand for plant-based food products | +1.9% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Untapped potential in emerging economies | +1.7% | Asia Pacific (China, India), Latin America, MEA | Long-term (2026-2033) |

| Innovation in multifunctional phosphate blends | +1.4% | Developed Markets | Mid to Long-term (2027-2033) |

| Increased focus on food fortification with essential minerals | +1.1% | Global | Short to Mid-term (2025-2029) |

| Development of sustainable and eco-friendly phosphate sources | +0.9% | Europe, North America | Long-term (2028-2033) |

Food Phosphate Market Challenges Impact Analysis

The Food Phosphate market faces inherent challenges, primarily concerning the public perception and regulatory environment surrounding food additives. Despite their functional necessity, phosphates, like many E-numbers, can be viewed with skepticism by health-conscious consumers, driven by misinformation or a general preference for "clean label" products with fewer perceived artificial ingredients. This perception challenge forces manufacturers to invest in transparency and consumer education, or to explore alternative sourcing and processing methods that can align with natural ingredient trends, which adds complexity and cost to operations. Furthermore, the varying and often stringent regulatory frameworks across different countries for food additives necessitate significant compliance efforts, impacting market entry and product formulation globally.

Another significant challenge lies in managing raw material supply chain volatility and sustainability concerns. The production of phosphates relies on specific mineral resources and chemical processes, which can be susceptible to geopolitical factors, environmental regulations, and energy price fluctuations. Ensuring a stable, cost-effective, and environmentally responsible supply of phosphoric acid and other precursors is a continuous challenge. Additionally, the industry faces the ongoing technical challenge of developing phosphate solutions that deliver superior functionality while adhering to stricter usage limits and consumer preferences for reduced sodium or phosphorus content. Balancing these technical requirements with commercial viability and regulatory compliance remains a critical hurdle for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative consumer perception & demand for "clean label" products | -1.3% | Developed Markets | Long-term (2025-2033) |

| Stringent and diverse regulatory landscape across regions | -1.0% | Global | Long-term (2025-2033) |

| Volatility in raw material supply chain and pricing | -0.9% | Global | Short to Mid-term (2025-2029) |

| High R&D costs for developing new, compliant, and functional formulations | -0.7% | Global | Long-term (2027-2033) |

| Environmental sustainability concerns related to phosphate mining and waste | -0.6% | EU, China, US | Long-term (2028-2033) |

Food Phosphate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Food Phosphate market, offering a detailed understanding of its current state, historical performance, and future growth trajectories. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry across various segments and key geographical regions. It delves into the impact of emerging technologies like AI and addresses critical consumer and regulatory considerations, providing a holistic perspective for stakeholders. The report aims to equip businesses with actionable insights for strategic decision-making and market positioning within the dynamic food ingredients sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.35 Billion |

| Market Forecast in 2033 | USD 3.98 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Innophos Holdings Inc., ICL Group Ltd., Chemische Fabrik Budenheim KG, Prayon SA, OCP S.A., Mosaic Company, NutriScience Innovations LLC, Wengfu Group, Merck KGaA, Aditya Birla Chemicals (Thailand) Ltd., Sichuan Chuanheng Chemical Co. Ltd., Xingfa Chemical Group Co. Ltd., Haifa Group, EuroChem Group, PhosAgro, Foskor, Lanxess AG, TKI Hrastnik, Jiangxi Xinhua Chemical Co. Ltd., Spectrum Chemical Manufacturing Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Food Phosphate market is extensively segmented by type, application, and function, reflecting the diverse utility of these compounds across the food industry. Understanding these segmentations is crucial for identifying specific market niches, consumer preferences, and technological advancements. Each segment represents distinct market dynamics, driven by varying demand patterns from food manufacturers and end-users, highlighting the versatility and widespread integration of phosphates in modern food systems.

- By Type:

- Sodium Phosphate: Widely used for emulsification, buffering, and leavening.

- Potassium Phosphate: Often employed in dairy and beverage for buffering and mineral fortification.

- Calcium Phosphate: Key in fortifying dairy products, cereals, and as a leavening agent.

- Ammonium Phosphate: Primarily used in bakery as a leavening agent.

- Others: Includes ferric phosphate and magnesium phosphate for specific fortification needs.

- By Application:

- Meat & Seafood Processing: Enhances water retention, texture, and extends shelf life.

- Dairy Products: Stabilizes milk proteins, acts as emulsifiers in cheese, and buffers.

- Bakery & Confectionery: Functions as leavening agents, firming agents, and dough conditioners.

- Beverages: Used as buffering agents, acidulants, and mineral fortifiers.

- Processed Food: Integral for texture, stability, and preservation in various convenience foods.

- Others: Includes usage in nutritional supplements and pet food.

- By Function:

- Emulsifying Agent: Stabilizes oil-in-water or water-in-oil mixtures.

- Leavening Agent: Produces gas in dough for rising.

- Buffering Agent: Maintains pH levels in food products.

- Sequestrant: Binds metal ions to prevent spoilage.

- Gelling Agent: Contributes to gel formation and texture.

- Stabilizer: Prevents separation of ingredients.

- Nutrient Supplement: Provides essential minerals like calcium and phosphorus.

- Preservative: Extends shelf life by inhibiting microbial growth.

Regional Highlights

- Asia Pacific (APAC): Emerging as the largest and fastest-growing market, driven by rapid urbanization, increasing disposable incomes, and the booming processed food industry, particularly in China and India. The shift towards convenience foods and Western dietary habits significantly boosts demand for food phosphates in this region.

- North America: A mature market with high consumption of processed meats, dairy products, and baked goods. Stringent food safety regulations and a strong focus on functional and fortified foods continue to drive innovation and stable demand for phosphates.

- Europe: Characterized by a strong emphasis on clean label ingredients and sustainable sourcing. While a significant consumer, the market growth is moderated by strict regulatory frameworks and consumer scrutiny over food additives. Innovation in plant-based alternatives and specialty food products offers new growth avenues.

- Latin America: Experiencing consistent growth due to expanding food processing industries, increasing population, and rising consumption of packaged and convenience foods. Brazil and Mexico are key contributors to market expansion in this region.

- Middle East and Africa (MEA): A nascent but rapidly growing market, fueled by increasing investment in food processing infrastructure, population growth, and evolving dietary preferences. Opportunities exist for market penetration as the region develops its food manufacturing capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Phosphate Market.- Innophos Holdings Inc.

- ICL Group Ltd.

- Chemische Fabrik Budenheim KG

- Prayon SA

- OCP S.A.

- Mosaic Company

- NutriScience Innovations LLC

- Wengfu Group

- Merck KGaA

- Aditya Birla Chemicals (Thailand) Ltd.

- Sichuan Chuanheng Chemical Co. Ltd.

- Xingfa Chemical Group Co. Ltd.

- Haifa Group

- EuroChem Group

- PhosAgro

- Foskor

- Lanxess AG

- TKI Hrastnik

- Jiangxi Xinhua Chemical Co. Ltd.

- Spectrum Chemical Manufacturing Corp.

Frequently Asked Questions

What are food phosphates used for?

Food phosphates are versatile food additives primarily used to enhance texture, stability, preservation, and nutritional value in a wide range of food products. They function as leavening agents in baked goods, emulsifiers in dairy and processed meats, buffering agents for pH control, and sequestrants to improve shelf life by binding metal ions.

Is the Food Phosphate market growing?

Yes, the Food Phosphate market is projected for significant growth. It is estimated to reach USD 3.98 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.8% from USD 2.35 billion in 2025, driven by increasing demand for processed foods and functional ingredients.

What are the key drivers of the Food Phosphate market?

Key drivers include the rising global consumption of processed and convenience foods, increasing population and urbanization, expansion of the meat and dairy industries, and growing demand for functional food products that require phosphates for specific properties like texture, stability, and preservation.

Are there any health concerns related to food phosphates?

While generally recognized as safe (GRAS) at approved levels, some studies suggest that excessive dietary intake of certain phosphates, particularly from processed foods, could have potential health implications for specific populations. This has led to increased regulatory scrutiny and a consumer preference for "clean label" products with reduced or no artificial additives.

What regions are key to the Food Phosphate market growth?

Asia Pacific is a crucial region for market growth due to its large population, rapid urbanization, and expanding processed food sector, particularly in countries like China and India. North America and Europe also remain significant markets, driven by established food industries and innovation in functional foods, while Latin America and MEA offer emerging opportunities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted