Food Metal Can Market

Food Metal Can Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706697 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

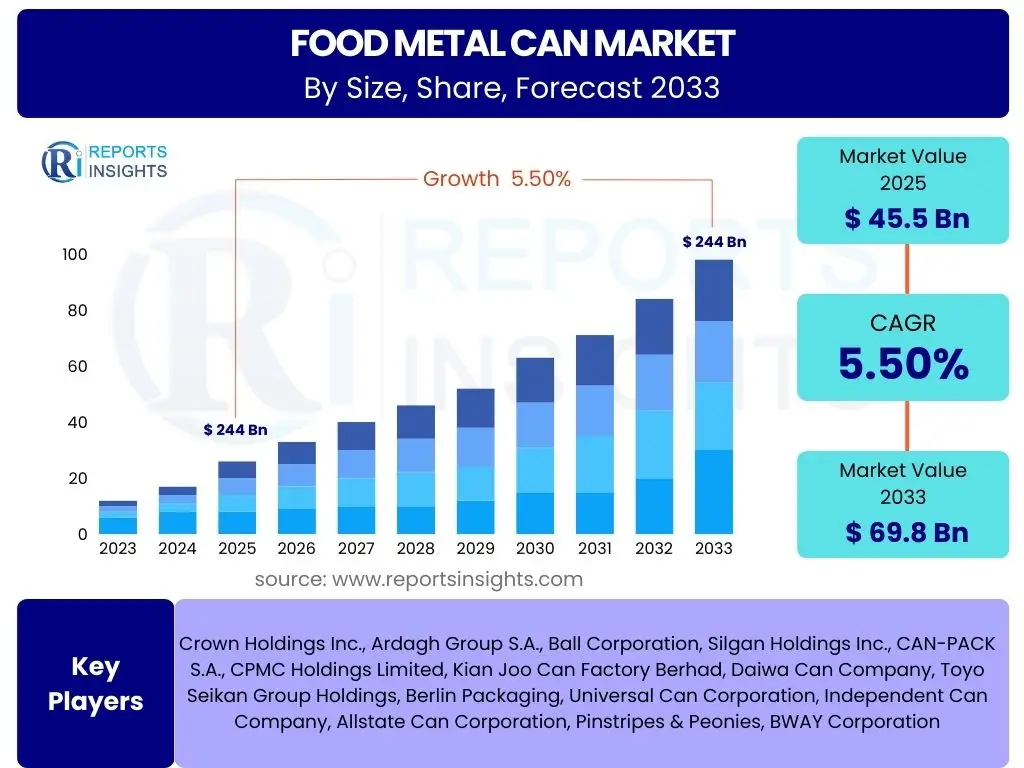

Food Metal Can Market Size

According to Reports Insights Consulting Pvt Ltd, The Food Metal Can Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 45.5 Billion in 2025 and is projected to reach USD 69.8 Billion by the end of the forecast period in 2033.

Key Food Metal Can Market Trends & Insights

The Food Metal Can Market is witnessing significant transformations driven by evolving consumer preferences, technological advancements, and a heightened focus on sustainability. User queries frequently revolve around how packaging innovations are addressing environmental concerns, what new functionalities cans offer for food preservation, and the impact of lightweighting initiatives on the industry. There is a strong emphasis on understanding how manufacturers are responding to the demand for more eco-friendly and convenient packaging solutions, while also maintaining the core benefits of metal cans such as extended shelf life and robust protection.

Consumers are increasingly seeking packaging that aligns with their values, prioritizing recyclability and reduced environmental footprint. This demand is prompting manufacturers to invest in advanced recycling technologies and to promote the circularity of metal packaging. Additionally, the proliferation of ready-to-eat meals and on-the-go food options is driving innovation in can formats, including easy-open ends and portion-controlled sizes, enhancing consumer convenience. The market is also seeing a shift towards more aesthetically appealing designs and customization options, reflecting brands' efforts to capture consumer attention and differentiate products on crowded shelves.

- Increased demand for sustainable and recyclable packaging solutions.

- Focus on lightweighting technologies to reduce material usage and transportation costs.

- Innovation in can designs, including easy-open ends and reclosable features.

- Growth in demand for portion-controlled and single-serving food products.

- Development of advanced coatings to enhance food safety and prevent material migration.

- Adoption of digital printing for customized and engaging can aesthetics.

- Expansion into new food categories, including plant-based and functional foods.

AI Impact Analysis on Food Metal Can

The integration of Artificial Intelligence (AI) in the Food Metal Can Market is a topic of growing interest, with common user questions focusing on its potential to revolutionize manufacturing efficiency, supply chain management, and quality control. Stakeholders are keen to understand how AI can lead to cost reductions, improve operational precision, and enable more data-driven decision-making within production facilities. The primary concerns often relate to the initial investment required for AI infrastructure, the need for skilled labor to manage these advanced systems, and the security of proprietary data. However, the anticipated benefits in terms of enhanced productivity and waste reduction largely outweigh these concerns for many industry players.

AI's influence is particularly notable in areas such as predictive maintenance, where algorithms analyze sensor data from machinery to anticipate equipment failures, thereby minimizing downtime and extending asset lifespan. In quality assurance, AI-powered vision systems can detect microscopic defects on can surfaces or within internal coatings with unprecedented accuracy, ensuring product integrity and safety. Furthermore, AI contributes significantly to optimizing energy consumption in manufacturing processes and streamlining complex supply chains through advanced demand forecasting and logistics optimization. These applications are poised to transform the traditional operational models within the food metal can industry, making it more agile and responsive to market dynamics.

- Enhanced predictive maintenance in manufacturing, reducing downtime and operational costs.

- Improved quality control through AI-powered visual inspection systems for defect detection.

- Optimized supply chain management and demand forecasting, leading to reduced waste and improved logistics.

- Increased energy efficiency in production processes through AI-driven process optimization.

- Automated material handling and sorting, boosting factory throughput and consistency.

Key Takeaways Food Metal Can Market Size & Forecast

Insights into the Food Metal Can Market size and forecast reveal a stable and resilient growth trajectory, primarily driven by the fundamental need for durable and safe food packaging. Common user questions highlight a desire to understand the underlying factors contributing to this consistent growth, the market's stability amidst global economic fluctuations, and its long-term investment viability. The market's foundational role in food preservation and distribution, combined with ongoing innovations in sustainability and convenience, underpins its positive outlook. This stability makes it an attractive sector for both established players and new entrants seeking to leverage its inherent advantages.

The projected growth indicates a continuous reliance on metal cans for a wide array of food products, from processed fruits and vegetables to ready meals and pet food. This enduring demand is complemented by strategic advancements such as lightweighting and enhanced recyclability, which address contemporary environmental concerns without compromising performance. Furthermore, the market's ability to adapt to changing consumer lifestyles, particularly the rise of convenience foods and global food trade, positions it for sustained expansion. The forecast reflects an industry that is not only mature but also continuously innovating to meet the evolving needs of the food sector and consumer expectations.

- The market demonstrates consistent growth, driven by indispensable food preservation and safety requirements.

- Innovation in sustainable materials and manufacturing processes is a key enabler of market expansion.

- Rising global population and increasing demand for processed and convenience foods fuel market demand.

- Metal cans offer superior shelf life and protection, maintaining their competitive edge over alternative packaging.

- Investment in research and development for lighter, more efficient, and aesthetically appealing cans is ongoing.

Food Metal Can Market Drivers Analysis

The Food Metal Can Market is propelled by several robust drivers that underpin its growth and resilience. A significant factor is the escalating global demand for packaged and processed food, driven by urbanization, changing lifestyles, and increasing disposable incomes, particularly in emerging economies. As more consumers opt for convenience and longer shelf-life products, the need for reliable, protective packaging solutions like metal cans intensifies. The inherent properties of metal cans—such as their excellent barrier protection against light, oxygen, and moisture—make them ideal for preserving nutritional content and extending product freshness, which is a critical consideration for both manufacturers and consumers.

Furthermore, the high recyclability rate of metal cans provides a substantial environmental advantage, aligning with global sustainability initiatives and consumer preferences for eco-friendly packaging. Governments and regulatory bodies worldwide are increasingly promoting circular economy principles, further bolstering the appeal of metal as a infinitely recyclable material. Innovations in can manufacturing, including lightweighting technologies and enhanced internal coatings, are also driving adoption by improving efficiency, reducing transportation costs, and ensuring food safety. These combined factors create a strong impetus for the continued expansion and technological evolution within the Food Metal Can Market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Packaged & Processed Foods | +0.7% | Global, particularly Asia Pacific, Latin America, Africa | 2025-2033 |

| High Recyclability & Sustainability Profile of Metal | +0.6% | Europe, North America, Developed Asia | 2025-2033 |

| Superior Barrier Protection & Extended Shelf Life | +0.5% | Global | 2025-2033 |

| Rising Disposable Incomes & Urbanization | +0.4% | Emerging Economies | 2025-2033 |

| Convenience & Portability of Canned Foods | +0.3% | Global | 2025-2033 |

Food Metal Can Market Restraints Analysis

Despite its inherent advantages, the Food Metal Can Market faces several notable restraints that could temper its growth trajectory. One significant challenge is the intense competition from alternative packaging materials, such as plastic, glass, and flexible packaging. These materials often offer cost advantages, aesthetic versatility, or lightweight properties that appeal to certain segments of the food industry and consumer preferences, potentially diverting market share away from metal cans. The continuous innovation in these competing materials, especially in areas like bio-based plastics and high-barrier flexibles, poses an ongoing threat to metal can dominance in specific applications.

Another key restraint is the volatility in raw material prices, particularly for aluminum and steel. Fluctuations in commodity markets directly impact the production costs of metal cans, which can erode profit margins for manufacturers and lead to higher prices for end-users, potentially making alternative packaging more attractive. Furthermore, the energy-intensive nature of metal can production, despite ongoing efforts towards efficiency, can also be a cost burden, especially in regions with high energy prices. While metal cans boast high recyclability, the upfront energy consumption for primary metal production and the logistical complexities of collection and sorting for recycling also present challenges that the industry must continuously address to remain competitive and environmentally appealing.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Alternative Packaging Materials | -0.5% | Global | 2025-2033 |

| Volatility in Raw Material Prices (Aluminum, Steel) | -0.4% | Global | 2025-2033 |

| High Energy Consumption in Manufacturing | -0.3% | Europe, Asia Pacific | 2025-2033 |

| Perceived Consumer Preference for Fresh/Less Processed Foods | -0.2% | North America, Europe | 2025-2033 |

| Regulatory Scrutiny on Certain Can Coatings (e.g., BPA) | -0.1% | Europe, North America | 2025-2028 |

Food Metal Can Market Opportunities Analysis

The Food Metal Can Market is poised to capitalize on several emerging opportunities that could significantly boost its growth trajectory. A primary opportunity lies in the burgeoning global demand for sustainable and circular packaging solutions. As environmental awareness intensifies, the inherent recyclability of metal cans—which can be recycled infinitely without loss of quality—positions them as a highly attractive option for brands committed to reducing their ecological footprint. This aligns perfectly with consumer and regulatory pressures for more environmentally responsible packaging choices, offering a distinct competitive advantage over materials with less favorable environmental profiles.

Furthermore, the expansion of e-commerce and the rising popularity of online grocery shopping present new avenues for market growth. Metal cans offer superior product protection during transit, making them ideal for shipping without damage, which is a critical concern for online retailers. Innovations in can design, such as lightweighting, advanced printing techniques for enhanced branding, and the development of intelligent packaging features (e.g., QR codes for traceability), also open up new market segments and applications. The continuous evolution of food consumption patterns, including the rise of plant-based foods, functional foods, and convenient meal solutions, further creates diverse opportunities for metal can manufacturers to innovate and expand their product offerings to cater to these specialized and growing niches.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable & Circular Packaging | +0.7% | Global, particularly Europe, North America | 2025-2033 |

| Expansion of E-commerce & Online Grocery Sales | +0.6% | Global | 2025-2033 |

| Technological Advancements in Can Manufacturing (Lightweighting, Coatings) | +0.5% | Global | 2025-2033 |

| Emergence of New Food Categories (Plant-Based, Functional Foods) | +0.4% | North America, Europe, Asia Pacific | 2025-2033 |

| Market Expansion in Developing Countries | +0.3% | Asia Pacific, Latin America, Africa | 2025-2033 |

Food Metal Can Market Challenges Impact Analysis

The Food Metal Can Market confronts several significant challenges that demand strategic responses from industry participants. One prominent challenge involves the complex regulatory landscape, particularly concerning food contact materials and coatings. Compliance with varying national and international standards, such as those related to BPA alternatives and other chemical substances, requires continuous research and development investments to ensure product safety and market access. Navigating these evolving regulations can be costly and time-consuming, posing a barrier to rapid innovation and market entry for some players.

Another critical challenge is the optimization of the recycling infrastructure. While metal cans are highly recyclable, ensuring efficient collection, sorting, and reprocessing requires robust infrastructure and consumer participation. In some regions, inadequate recycling facilities or low consumer awareness about proper disposal can hinder the full realization of metal's circularity potential. Additionally, managing the perception of canned foods, which can sometimes be viewed as less "fresh" or "natural" compared to refrigerated or unpackaged alternatives, represents a marketing challenge. Overcoming this perception requires educational campaigns and continued innovation to highlight the quality and convenience benefits of canned products, directly impacting consumer acceptance and overall market demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Regulatory Environment for Food Contact Materials | -0.4% | Global, particularly Europe, North America | 2025-2033 |

| Optimizing & Expanding Recycling Infrastructure | -0.3% | Global | 2025-2033 |

| Consumer Perception & Preference for Fresh Foods | -0.2% | Developed Markets | 2025-2033 |

| Supply Chain Disruptions & Logistics Costs | -0.2% | Global | 2025-2027 (Short to Mid-Term) |

| Pressure to Reduce Carbon Footprint of Production | -0.1% | Global | 2025-2033 |

Food Metal Can Market - Updated Report Scope

This report provides a comprehensive analysis of the Food Metal Can Market, encompassing historical data, current market trends, and future growth projections. It delves into the market size, segmentations, competitive landscape, and key factors influencing market dynamics, offering valuable insights for stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.5 Billion |

| Market Forecast in 2033 | USD 69.8 Billion |

| Growth Rate | 5.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Crown Holdings Inc., Ardagh Group S.A., Ball Corporation, Silgan Holdings Inc., CAN-PACK S.A., CPMC Holdings Limited, Kian Joo Can Factory Berhad, Daiwa Can Company, Toyo Seikan Group Holdings, Berlin Packaging, Universal Can Corporation, Independent Can Company, Allstate Can Corporation, Pinstripes & Peonies, BWAY Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Food Metal Can Market is extensively segmented to provide a granular view of its various components and underlying dynamics. This segmentation facilitates a deeper understanding of market trends, consumer preferences, and strategic opportunities across different categories. Analyzing the market by material, type, capacity, and application allows for precise identification of growth areas and challenges, enabling stakeholders to tailor their strategies effectively. Each segment reflects distinct characteristics, driven by factors such as material availability, manufacturing processes, specific food preservation needs, and consumer usage patterns, collectively shaping the market's comprehensive landscape.

For instance, the material segmentation highlights the dominance and specific applications of aluminum, steel, and tin-plated cans, driven by their respective properties like lightweighting potential, strength, and cost-effectiveness. The type segmentation differentiates between 2-piece and 3-piece cans, each having unique manufacturing efficiencies and suitability for different product types. Capacity segmentation caters to diverse serving sizes and product volumes, while the application segment maps the market across a broad spectrum of food categories, from staples like fruits and vegetables to specialized items such as pet food and ready meals. This detailed breakdown ensures a thorough market assessment, critical for both market entry and expansion strategies.

- By Material:

- Aluminum: Favored for lightweight properties and high recyclability, often used for smaller capacity cans.

- Steel: Known for its strength and cost-effectiveness, widely used for a variety of food products including larger cans.

- Tin-plated: A type of steel can, offering excellent corrosion resistance and barrier properties.

- By Type:

- 2-Piece Cans: Manufactured from a single piece of metal for the body and a separate end, known for integrity and lightweighting.

- 3-Piece Cans: Composed of a cylindrical body and two separate ends, highly versatile for various sizes and products.

- By Capacity:

- Less than 250 ml: Typically for single-serving portions, specialty foods, or concentrated products.

- 250 ml to 500 ml: Common for everyday processed foods, vegetables, and soups.

- More than 500 ml: Used for bulk packaging, large family sizes, or specific industrial applications.

- By Application:

- Fruits & Vegetables: A traditional and major segment due to long shelf-life requirements.

- Meat & Seafood: Utilizes cans for preservation and distribution, ensuring safety and convenience.

- Pet Food: A significant and growing segment, relying on cans for product integrity and storage.

- Soups & Sauces: Demands robust barrier properties for extended freshness.

- Dairy Products: Includes condensed milk and certain dairy-based ready-to-eat products.

- Ready Meals: Growing segment driven by convenience and busy lifestyles.

- Other Food Products: Includes specialty items, baby food, and various processed goods.

Regional Highlights

The Food Metal Can Market exhibits diverse regional dynamics, each influenced by unique economic, cultural, and regulatory factors. North America and Europe represent mature markets characterized by high awareness of sustainability, stringent food safety regulations, and a demand for premium, convenient, and aesthetically pleasing packaging. These regions are at the forefront of adopting lightweighting technologies, advanced coatings, and circular economy initiatives, pushing for higher recycling rates and reduced environmental impact. Consumer preferences for organic and healthy processed foods also shape product offerings, driving innovation in smaller, single-serve can formats and specialized food categories.

Asia Pacific (APAC) stands out as the fastest-growing market, propelled by rapid urbanization, increasing disposable incomes, and the burgeoning demand for packaged and convenience foods. Countries like China, India, and Southeast Asian nations are witnessing a significant shift from traditional fresh markets to supermarket and online retail models, escalating the need for shelf-stable food packaging. Latin America and the Middle East & Africa (MEA) are also emerging as key growth regions, driven by expanding middle-class populations, increased access to processed food products, and improvements in cold chain logistics leading to greater consumption of packaged goods. These regions present substantial opportunities for market expansion, with a focus on cost-effective solutions and reliable supply chains to meet growing consumer needs.

- North America: Mature market with high adoption of sustainable practices and demand for convenience foods. Strong emphasis on lightweighting and advanced material coatings.

- Europe: Leading in circular economy initiatives and strict food safety regulations. Focus on high recyclability, premiumization, and innovative can designs for diverse food applications.

- Asia Pacific (APAC): Rapidly expanding market driven by urbanization, rising disposable incomes, and increasing consumption of packaged foods. Significant growth potential in emerging economies.

- Latin America: Growing demand for processed and convenience foods due to changing lifestyles. Market expansion driven by increased modern retail penetration.

- Middle East & Africa (MEA): Emerging market with increasing consumption of packaged foods, supported by population growth and economic development. Opportunities for basic and cost-effective metal can solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Metal Can Market.- Crown Holdings Inc.

- Ardagh Group S.A.

- Ball Corporation

- Silgan Holdings Inc.

- CAN-PACK S.A.

- CPMC Holdings Limited

- Kian Joo Can Factory Berhad

- Daiwa Can Company

- Toyo Seikan Group Holdings

- Berlin Packaging

- Universal Can Corporation

- Independent Can Company

- Allstate Can Corporation

- Pinstripes & Peonies

- BWAY Corporation

Frequently Asked Questions

What is the projected growth rate of the Food Metal Can Market?

The Food Metal Can Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033, indicating a steady and robust expansion.

What are the primary drivers of growth in the Food Metal Can Market?

Key drivers include the increasing global demand for packaged and processed foods, the high recyclability and sustainability profile of metal, and the superior barrier protection and extended shelf life offered by metal cans.

How is AI impacting the Food Metal Can industry?

AI is significantly impacting the industry by enabling enhanced predictive maintenance, improving quality control through advanced visual inspection, and optimizing supply chain management and energy efficiency in production processes.

What are the main challenges facing the Food Metal Can Market?

The primary challenges include intense competition from alternative packaging materials, volatility in raw material prices, complex regulatory environments for food contact materials, and the need to expand and optimize recycling infrastructure.

Which regions are expected to show significant growth in the Food Metal Can Market?

Asia Pacific is anticipated to be the fastest-growing market due to rapid urbanization and increasing demand for packaged foods, while Latin America and the Middle East & Africa also present substantial growth opportunities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted