Food Cold Chain Market

Food Cold Chain Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705553 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

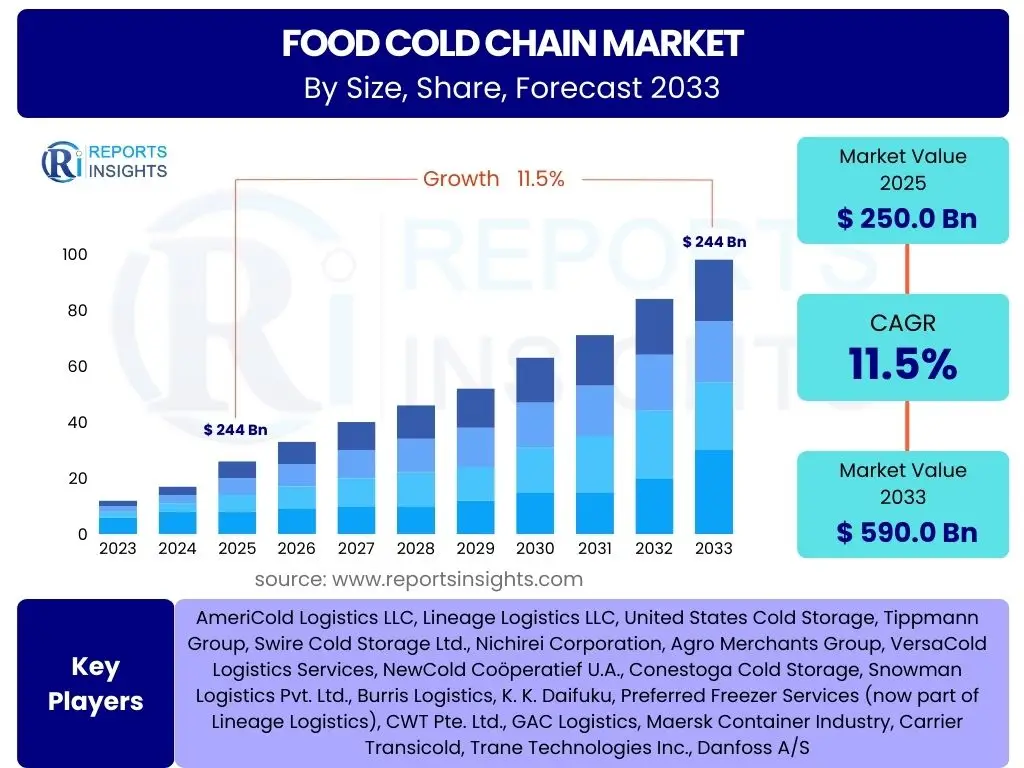

Food Cold Chain Market Size

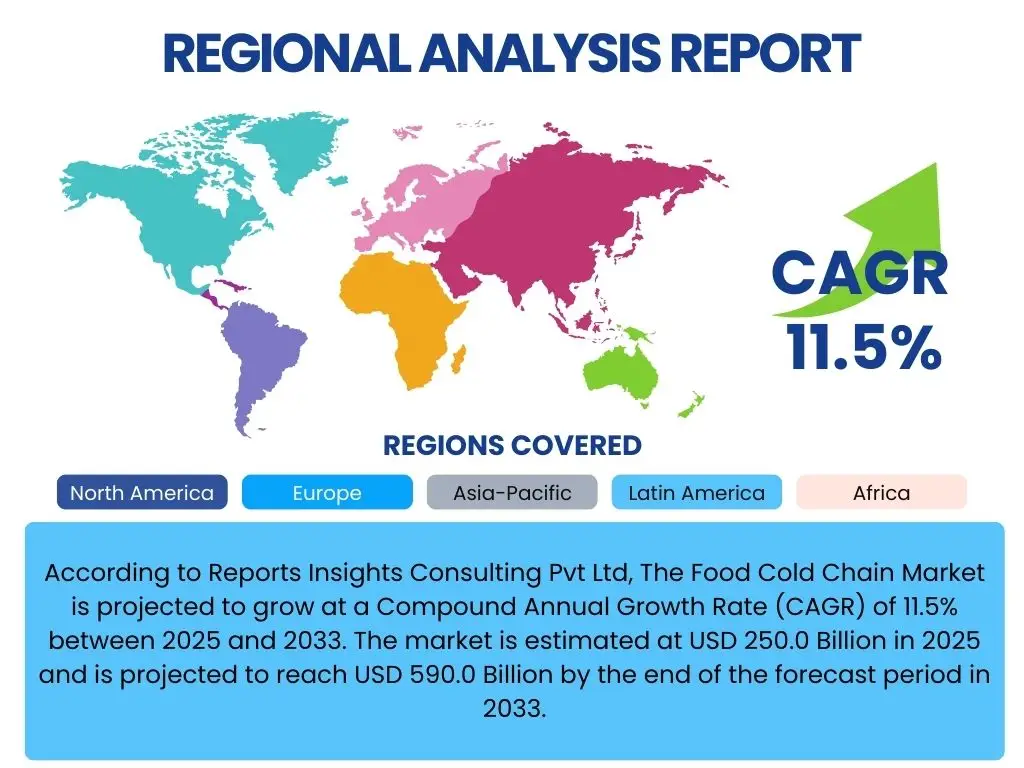

According to Reports Insights Consulting Pvt Ltd, The Food Cold Chain Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2025 and 2033. The market is estimated at USD 250.0 Billion in 2025 and is projected to reach USD 590.0 Billion by the end of the forecast period in 2033.

Key Food Cold Chain Market Trends & Insights

The Food Cold Chain market is undergoing significant transformation driven by evolving consumer preferences, technological advancements, and a heightened focus on food safety and waste reduction. A key trend is the increasing consumer demand for perishable goods, including fresh produce, dairy, and frozen foods, particularly through online retail channels which necessitate robust cold chain infrastructure. Simultaneously, there is a growing emphasis on sustainability, leading to the adoption of energy-efficient refrigeration technologies and environmentally friendly refrigerants to reduce the carbon footprint of cold chain operations. Furthermore, the integration of advanced digital technologies like IoT, AI, and blockchain is revolutionizing tracking, monitoring, and transparency across the entire cold supply chain, enhancing efficiency and minimizing spoilage.

Another prominent insight is the expansion of international trade in temperature-sensitive food products, which mandates seamless cross-border cold chain logistics and adherence to diverse regulatory standards. This globalized trade, coupled with rising disposable incomes in emerging economies, is fueling investment in new cold storage facilities and refrigerated transportation networks. The market is also witnessing a trend towards modular and flexible cold storage solutions, enabling businesses to scale operations efficiently and adapt to fluctuating demand. The imperative for precise temperature control from farm to fork remains paramount, pushing innovators to develop more sophisticated monitoring systems and predictive analytics to ensure product integrity and safety throughout the cold chain journey.

- Rising global demand for perishable food products and processed foods.

- Expansion of e-commerce and online grocery delivery services.

- Increasing adoption of advanced technologies like IoT, AI, and blockchain for enhanced visibility and efficiency.

- Growing focus on food safety regulations and quality assurance.

- Shift towards energy-efficient and eco-friendly cold chain solutions.

- Development of integrated and end-to-end cold chain logistics services.

- Globalization of food trade requiring robust cross-border cold chain infrastructure.

- Emergence of specialized cold chain services for niche food segments.

AI Impact Analysis on Food Cold Chain

Artificial Intelligence (AI) is fundamentally transforming the Food Cold Chain by introducing unprecedented levels of efficiency, predictability, and safety. Users frequently inquire about how AI can optimize operational costs, improve real-time monitoring, and mitigate risks associated with temperature excursions. AI algorithms are being deployed for predictive maintenance of refrigeration units, anticipating equipment failures before they occur, thereby preventing costly downtimes and product spoilage. Furthermore, AI-driven demand forecasting models enable more accurate inventory management, reducing waste and ensuring optimal stock levels for perishable goods. The ability of AI to process vast datasets from sensors and logistics systems allows for dynamic route optimization, minimizing fuel consumption and transit times while maintaining critical temperature parameters.

The impact of AI extends to enhancing food quality and reducing spoilage through sophisticated temperature monitoring and anomaly detection. AI-powered vision systems can inspect produce for ripeness and defects, further automating quality control. While there is considerable excitement about these advancements, user concerns often revolve around the initial investment costs, the complexity of integrating AI solutions with existing legacy systems, and the need for skilled personnel to manage and interpret AI-generated insights. Data privacy and security, given the sensitive nature of supply chain information, are also frequently raised as crucial considerations. Despite these challenges, the consensus is that AI will continue to be a pivotal technology in creating more resilient, transparent, and sustainable food cold chains, addressing long-standing pain points like food waste and operational inefficiencies.

- Optimized route planning and logistics for refrigerated transport, reducing fuel consumption and delivery times.

- Predictive maintenance for cold storage equipment, minimizing breakdowns and ensuring continuous temperature control.

- Enhanced demand forecasting, leading to reduced food waste and improved inventory management.

- Real-time temperature monitoring and anomaly detection, ensuring product integrity and food safety.

- Automated quality control and sorting of perishable goods through computer vision.

- Improved energy efficiency in cold storage facilities through AI-driven environmental controls.

- Data-driven decision-making for supply chain resilience and risk management.

Key Takeaways Food Cold Chain Market Size & Forecast

The Food Cold Chain market is poised for substantial growth over the next decade, reflecting a global recognition of its critical role in food security, quality, and waste reduction. Users are particularly interested in understanding the foundational drivers behind this expansion and the long-term viability of investments in this sector. A primary takeaway is the indispensable nature of cold chain logistics for a burgeoning global population with increasingly diversified dietary preferences, alongside the growing prevalence of organized retail and e-commerce platforms. The market's robust Compound Annual Growth Rate signifies a sustained momentum, underpinned by continuous technological innovation aimed at enhancing efficiency, traceability, and sustainability across the entire cold supply chain.

Furthermore, the forecast underscores the market's resilience against economic fluctuations, as the demand for fresh and frozen foods remains relatively inelastic. The anticipated significant increase in market value by 2033 highlights the ongoing expansion of cold storage capacities and refrigerated transportation networks, particularly in emerging economies where infrastructure development is accelerating. Strategic investments in smart cold chain technologies, such as IoT sensors and AI-driven analytics, are key to unlocking further growth and addressing operational challenges. The market's future will be characterized by a greater emphasis on end-to-end solutions that guarantee temperature integrity from farm to consumer, reinforcing the cold chain as a cornerstone of modern food systems.

- Significant growth projected, driven by increasing demand for perishable goods.

- Market expansion is global, with strong development in emerging economies.

- Technological integration is crucial for efficiency and competitive advantage.

- Food safety and waste reduction are core market imperatives.

- Investments in infrastructure and digital solutions are paramount.

- Sustainable practices are becoming a major differentiator.

- The market is resilient and essential for global food supply chains.

Food Cold Chain Market Drivers Analysis

The Food Cold Chain market's expansion is fundamentally propelled by several interconnected factors that create sustained demand for temperature-controlled logistics. The increasing consumer preference for fresh, frozen, and processed food items globally, coupled with a rising disposable income, directly translates into a higher volume of perishable goods requiring specialized handling. This demand is further amplified by the rapid growth of the organized retail sector and e-commerce platforms, which necessitate efficient cold chain networks to deliver temperature-sensitive products directly to consumers while maintaining quality and safety. Additionally, stringent food safety regulations and quality control standards imposed by governments and international bodies compel food producers and distributors to adopt robust cold chain solutions to comply with health guidelines and minimize spoilage, thus reducing financial losses and public health risks.

Beyond consumer and regulatory pressures, the globalization of the food trade is a significant driver. As countries increasingly import and export a wider variety of perishable food products, the need for seamless, reliable, and standardized cold chain logistics across borders becomes paramount. This global interconnectedness requires advanced refrigeration technologies and sophisticated supply chain management systems to ensure product integrity over long distances and varied climatic conditions. Furthermore, advancements in refrigeration technologies, including more energy-efficient and environmentally friendly cooling systems, are making cold chain operations more sustainable and economically viable, encouraging wider adoption across various segments of the food industry. These combined forces create a powerful impetus for continuous investment and innovation within the Food Cold Chain market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Perishable & Processed Foods | +3.0% | Global, particularly Asia Pacific, Latin America | Short to Long Term |

| Growth of Organized Retail and E-commerce | +2.5% | North America, Europe, Asia Pacific | Short to Mid Term |

| Stringent Food Safety Regulations & Quality Standards | +2.0% | Europe, North America, Developed Asia | Mid to Long Term |

| Technological Advancements in Refrigeration & Logistics | +2.0% | Global, especially developed economies | Mid to Long Term |

| Globalization of Food Trade | +2.0% | Global, cross-continental routes | Short to Mid Term |

Food Cold Chain Market Restraints Analysis

Despite robust growth prospects, the Food Cold Chain market faces several significant restraints that could impede its full potential. One primary challenge is the high operational and capital expenditure associated with establishing and maintaining cold chain infrastructure. This includes the cost of refrigerated warehouses, specialized transport vehicles, energy-intensive cooling systems, and advanced monitoring technologies, which can be prohibitive for smaller businesses or in regions with limited investment capital. The substantial energy consumption of refrigeration also contributes to high operating costs, making profitability challenging, especially amidst fluctuating energy prices. These economic barriers can slow down the adoption of comprehensive cold chain solutions, particularly in developing markets where financial resources are often constrained.

Another major restraint is the lack of adequate infrastructure in many developing and underdeveloped regions. This includes insufficient cold storage facilities, unreliable power grids, and poorly developed road networks, which make it difficult to maintain continuous temperature control from the point of origin to the final destination. This infrastructure gap leads to significant post-harvest losses and spoilage, undermining the efficiency of the cold chain. Furthermore, the complexity of managing a diverse range of perishable products, each with specific temperature requirements, adds to operational challenges. Issues such as a shortage of skilled labor for specialized cold chain management and the difficulty in standardizing processes across a fragmented supply chain also present ongoing hurdles. Addressing these multifaceted restraints requires strategic investments, policy support, and collaborative efforts across the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital & Operational Costs | -2.5% | Global, especially developing regions | Short to Mid Term |

| Infrastructure Deficiencies in Emerging Economies | -2.0% | Africa, parts of Asia Pacific, Latin America | Long Term |

| Fluctuating Energy Prices | -1.5% | Global | Short Term |

| Lack of Skilled Personnel & Standardization | -1.0% | Global | Mid Term |

Food Cold Chain Market Opportunities Analysis

Despite existing restraints, the Food Cold Chain market is rich with significant opportunities for growth and innovation. The expansion into emerging markets, particularly in Asia Pacific, Latin America, and Africa, presents a vast untapped potential. These regions are experiencing rapid urbanization, rising middle-class populations, and increasing demand for diverse food products, yet often lack sufficient cold chain infrastructure. This creates a fertile ground for new investments in cold storage facilities, refrigerated logistics, and advanced monitoring technologies. International development initiatives and foreign direct investments are also contributing to bridging this infrastructure gap, opening avenues for cold chain providers to establish new operations and partnerships in these developing economies, thereby enhancing food security and reducing post-harvest losses.

Another crucial opportunity lies in the integration of advanced digital technologies. The widespread adoption of IoT, AI, big data analytics, and blockchain offers transformative potential for enhancing transparency, traceability, and efficiency throughout the cold chain. These technologies enable real-time temperature monitoring, predictive analytics for demand and equipment maintenance, and immutable records for food safety compliance. Furthermore, the growing focus on sustainability and environmental responsibility is driving demand for green cold chain solutions, including energy-efficient refrigeration systems, renewable energy integration, and eco-friendly refrigerants. Companies that invest in these sustainable practices can differentiate themselves, attract environmentally conscious clients, and potentially benefit from government incentives, positioning them for long-term growth and market leadership in a rapidly evolving landscape. The rise of specialized cold chain services for niche markets, such as organic foods, gourmet products, or specific dietary requirements, also represents a growing segment within the overall market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Economies (APAC, LATAM, MEA) | +3.0% | Asia Pacific, Latin America, Middle East & Africa | Long Term |

| Integration of Advanced Technologies (IoT, AI, Blockchain) | +2.5% | Global | Mid to Long Term |

| Development of Green & Sustainable Cold Chain Solutions | +2.0% | Europe, North America | Mid to Long Term |

| Growth in Specialized & Value-Added Cold Chain Services | +1.5% | North America, Europe, Developed Asia | Short to Mid Term |

Food Cold Chain Market Challenges Impact Analysis

The Food Cold Chain market, while experiencing significant growth, is not without its inherent challenges that necessitate strategic navigation from industry players. Maintaining precise and continuous temperature control across the entire supply chain, from producer to consumer, remains a paramount and complex challenge. Temperature deviations, even minor ones, can lead to product spoilage, quality degradation, and significant financial losses, making consistent monitoring and immediate intervention crucial. This challenge is exacerbated by factors such as equipment malfunctions, human error, and external environmental conditions, demanding robust and redundant systems. Additionally, the increasing stringency of global food safety regulations requires meticulous adherence to standards, adding layers of compliance complexity and operational costs for businesses operating across multiple jurisdictions.

Another substantial challenge stems from the high energy consumption of refrigeration systems, contributing to significant operating expenses and environmental concerns. Companies are under increasing pressure to adopt more energy-efficient and sustainable cooling technologies, which often involves considerable initial investment and technological upgrades. Furthermore, the fragmentation of the cold chain logistics landscape, particularly in developing regions, makes it difficult to achieve seamless integration and end-to-end visibility. This fragmentation can lead to inefficiencies, communication gaps, and increased risks of product damage or spoilage. Addressing these challenges requires continuous innovation in technology, strategic partnerships, and a commitment to sustainable practices to ensure the long-term viability and efficiency of the food cold chain. Managing the 'last mile' delivery of temperature-sensitive goods, especially in urban areas, also presents unique logistical hurdles related to traffic congestion and rapid delivery demands.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Temperature Integrity Throughout the Chain | -2.0% | Global | Ongoing |

| High Energy Consumption & Sustainability Concerns | -1.8% | Global, particularly developed economies | Mid to Long Term |

| Fragmented Supply Chains & Lack of End-to-End Visibility | -1.5% | Developing regions | Short to Mid Term |

| Regulatory Compliance & Standardization Across Borders | -1.2% | Global, cross-border trade | Ongoing |

Food Cold Chain Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Food Cold Chain market, offering a detailed overview of market dynamics, growth drivers, restraints, opportunities, and challenges. It encompasses a thorough segmentation analysis across various categories, including type, application, and technology, providing granular insights into the market's structure. The report also features a comprehensive regional analysis, highlighting the unique market trends and growth prospects in key geographical areas. Furthermore, it includes profiles of leading market players, offering competitive intelligence and strategic insights. The scope is designed to equip stakeholders with actionable data for informed decision-making, covering historical performance and future projections to present a holistic view of the market's evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 250.0 Billion |

| Market Forecast in 2033 | USD 590.0 Billion |

| Growth Rate | 11.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AmeriCold Logistics LLC, Lineage Logistics LLC, United States Cold Storage, Tippmann Group, Swire Cold Storage Ltd., Nichirei Corporation, Agro Merchants Group, VersaCold Logistics Services, NewCold Coöperatief U.A., Conestoga Cold Storage, Snowman Logistics Pvt. Ltd., Burris Logistics, K. K. Daifuku, Preferred Freezer Services (now part of Lineage Logistics), CWT Pte. Ltd., GAC Logistics, Maersk Container Industry, Carrier Transicold, Trane Technologies Inc., Danfoss A/S |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Food Cold Chain market is extensively segmented to provide a granular understanding of its diverse components and dynamics, reflecting the varied requirements of perishable goods and the technological solutions employed. This segmentation allows for targeted analysis of specific market niches, identifying key growth areas and competitive landscapes within each category. The primary segmentation distinguishes between Refrigerated Storage and Refrigerated Transport, recognizing the critical roles played by fixed cold warehouses and mobile logistics in maintaining the cold chain integrity. Further layers of segmentation delineate market performance based on the type of food products handled, the specific temperature ranges required, the technological solutions implemented, and the end-user industries served, each contributing uniquely to the overall market growth and evolution.

Understanding these distinct segments is crucial for stakeholders aiming to develop tailored strategies and investments. For instance, the 'By Application' segment highlights the varying cold chain demands of different food categories, from fruits and vegetables requiring precise humidity control to frozen desserts needing consistent ultra-low temperatures. The 'By Technology' segment illustrates the increasing reliance on advanced monitoring devices and software platforms for enhanced visibility and efficiency, signifying a shift towards smart cold chain solutions. Each segment is influenced by its own set of drivers and challenges, ranging from infrastructure development in emerging markets to regulatory compliance in mature economies, collectively painting a comprehensive picture of the market's intricate structure and potential for innovation across its many facets.

- By Type:

- Refrigerated Storage (Cold Warehouses, Cold Rooms)

- Refrigerated Transport (Road, Rail, Sea, Air)

- By Application:

- Fruits & Vegetables

- Meat & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Beverages

- Processed Food

- Others (e.g., Flowers, Chemicals)

- By Temperature Type:

- Chilled (0°C to 15°C)

- Frozen (-18°C to 0°C)

- Deep Frozen (Below -18°C)

- By Technology:

- Monitoring Devices (Sensors, RFID, GPS)

- Software & Platforms (Cloud-based, On-premise)

- Refrigeration Systems (Compressors, Evaporators)

- By End User:

- Food Manufacturing

- Food Service (Restaurants, Catering)

- Retail & Supermarkets

- Pharmaceuticals (Relevant for cross-industry tech transfer)

- Agriculture

Regional Highlights

- North America: This region is characterized by a mature and highly developed cold chain infrastructure, driven by high consumer demand for fresh and processed foods, the widespread presence of large retail chains, and a robust e-commerce penetration. The market benefits from significant investments in advanced technologies like IoT and AI for supply chain optimization. Stringent food safety regulations also contribute to the adoption of sophisticated cold chain solutions. Growth here is primarily driven by technological upgrades, sustainability initiatives, and the expansion of specialized services for diverse product categories.

- Europe: Europe exhibits strong growth owing to stringent food safety standards, increasing cross-border trade of perishable goods within the EU, and a significant focus on reducing food waste. The region is a leader in adopting energy-efficient and eco-friendly refrigeration technologies. Key trends include the consolidation of cold chain service providers, the emphasis on integrated logistics solutions, and the growing demand for organic and specialty food products requiring precise temperature control. Sustainability regulations significantly influence market development and technological adoption.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the Food Cold Chain market, propelled by rapid urbanization, a burgeoning middle class, and increasing disposable incomes driving demand for high-quality perishable foods. Significant government initiatives and private investments in infrastructure development, particularly in emerging economies like China, India, and Southeast Asian nations, are fostering the expansion of cold storage capacities and refrigerated transport networks. The growth of organized retail and e-commerce platforms is also a major catalyst.

- Latin America: This region presents considerable growth opportunities, albeit from a lower base compared to developed markets. Increasing demand for processed and frozen foods, expanding export-oriented agriculture, and improving trade relations are driving the need for better cold chain infrastructure. Challenges include fragmented logistics networks and varying levels of infrastructure development across countries, but ongoing investments in modernization and the adoption of new technologies are poised to accelerate market expansion.

- Middle East and Africa (MEA): The MEA region is a nascent but rapidly developing market for food cold chain. Growing populations, rising tourism, and increasing imports of temperature-sensitive food products are fueling demand. Significant investments in new ports, logistics hubs, and cold storage facilities, particularly in the GCC countries, are aimed at enhancing food security and establishing regional distribution centers. Challenges include harsh climatic conditions and the need for significant infrastructure upgrades, but the long-term potential for growth is substantial.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Food Cold Chain Market.- AmeriCold Logistics LLC

- Lineage Logistics LLC

- United States Cold Storage

- Tippmann Group

- Swire Cold Storage Ltd.

- Nichirei Corporation

- Agro Merchants Group

- VersaCold Logistics Services

- NewCold Coöperatief U.A.

- Conestoga Cold Storage

- Snowman Logistics Pvt. Ltd.

- Burris Logistics

- K. K. Daifuku

- Carrier Transicold

- Trane Technologies Inc.

- Danfoss A/S

- CSafe Global

- Envirotainer

- Kuehne + Nagel

- DHL Global Forwarding

Frequently Asked Questions

What is the Food Cold Chain and why is it important?

The Food Cold Chain is a temperature-controlled supply chain for perishable food products, maintaining optimal conditions from production to consumption. It is crucial for preserving food quality, extending shelf life, ensuring food safety by preventing bacterial growth, and reducing food waste. Its importance is amplified by global trade and consumer demand for fresh and frozen goods.

What key technologies are transforming the Food Cold Chain?

Key technologies include the Internet of Things (IoT) for real-time temperature monitoring and asset tracking, Artificial Intelligence (AI) for demand forecasting and route optimization, and Blockchain for enhanced traceability and transparency. These innovations improve efficiency, reduce spoilage, and bolster compliance with safety standards.

What are the main challenges faced by the Food Cold Chain market?

Challenges include high operational and capital costs associated with maintaining refrigerated infrastructure and energy consumption, significant infrastructure gaps in developing regions, and the complexity of ensuring consistent temperature control across diverse product types and long distances. Regulatory compliance and fragmentation of the supply chain also pose hurdles.

How is e-commerce impacting the Food Cold Chain market?

E-commerce is a major driver, intensifying the demand for efficient last-mile cold chain logistics. The growth of online grocery delivery services necessitates robust refrigerated transport networks and urban cold storage solutions, pushing for faster, more flexible, and highly reliable temperature-controlled deliveries directly to consumers.

What is the future outlook for the Food Cold Chain market?

The market is poised for robust growth, driven by increasing global demand for perishable foods, continuous technological innovation (especially in smart cold chain solutions), and a heightened focus on food safety and sustainability. Expansion into emerging markets and the development of greener cold chain practices are expected to define its future trajectory.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted