Floating Offshore Wind Power Market

Floating Offshore Wind Power Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700376 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

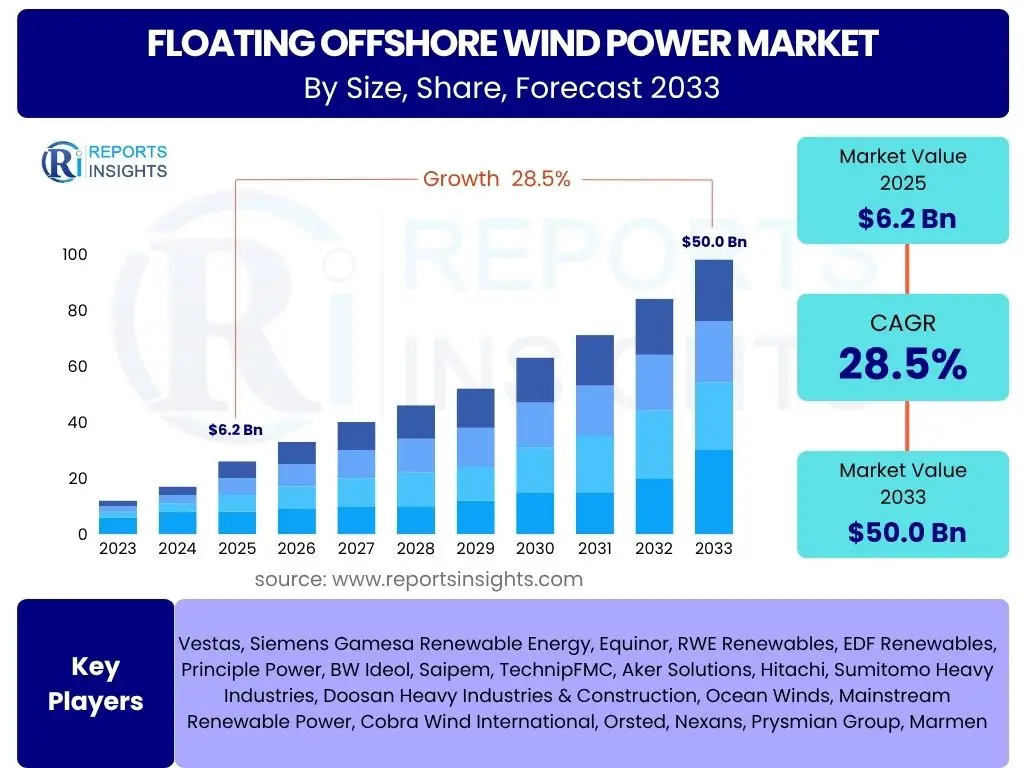

Floating Offshore Wind Power Market Size

The global Floating Offshore Wind Power Market is undergoing a transformative period, poised for exponential growth as nations prioritize renewable energy sources and seek to unlock deeper offshore wind resources. This market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. Valued at an estimated USD 6.2 billion in 2025, the market is projected to expand significantly, reaching an impressive USD 50.0 billion by the end of the forecast period in 2033.

This remarkable growth trajectory is a testament to the increasing viability and strategic importance of floating offshore wind technology. Traditional fixed-bottom offshore wind installations are limited to water depths typically less than 60 meters, leaving vast swathes of the ocean, particularly those with strong, consistent wind resources, untapped. Floating platforms overcome this limitation, enabling deployment in depths ranging from 60 meters to over 1,000 meters, thereby dramatically expanding the global potential for offshore wind energy generation. The technological advancements in platform design, mooring systems, and installation techniques are rapidly driving down costs and enhancing performance, making floating offshore wind an increasingly attractive option for energy security and decarbonization goals worldwide.

The market's expansion is not merely a reflection of technological progress but also a direct response to global climate change imperatives and ambitious national renewable energy targets. Governments and energy developers are investing heavily in research, development, and commercialization of floating offshore wind projects. Policy support, including subsidies, tax incentives, and dedicated auction mechanisms for floating wind, is creating a favorable investment climate. Furthermore, the integration of floating offshore wind with other emerging technologies, such as green hydrogen production and energy storage solutions, is expected to further bolster its market value and strategic importance in the evolving global energy landscape.

Key Floating Offshore Wind Power Market Trends & Insights

The Floating Offshore Wind Power Market is characterized by dynamic trends and critical insights shaping its rapid evolution. These include a strong emphasis on technological innovation and cost reduction strategies, significant policy support and regulatory frameworks, and an expanding global geographical footprint. The market is also witnessing increasing industry collaboration and the integration of digital solutions for enhanced efficiency, all contributing to its accelerated growth trajectory. Key trends and insights transforming the market are:

- Technological Advancements in Platform Design: Ongoing innovation in semi-submersible, spar, and tension-leg platform (TLP) designs, focusing on stability, modularity, and reduced material usage to cut capital expenditure and operational costs.

- Industrialization and Supply Chain Maturation: Efforts to standardize components, streamline manufacturing processes, and establish dedicated port infrastructure to support large-scale project deployment, addressing supply chain bottlenecks.

- Policy and Regulatory Tailwinds: Robust government support through Contracts for Difference (CfDs), tax credits, and specific targets for floating offshore wind capacity, particularly in Europe, Asia, and North America.

- Cost Reduction Pathways: Continued progress on learning curves, economies of scale, and optimized installation techniques driving down the Levelized Cost of Energy (LCOE) for floating wind, making it more competitive with other energy sources.

- Integration with Green Hydrogen Production: Emerging trend of coupling floating wind farms directly with offshore hydrogen electrolyzers, enabling large-scale production of green hydrogen and unlocking new energy vectors.

- Development of Deeper Water Projects: Focus on deploying projects in increasingly deeper waters (beyond 100 meters) where fixed-bottom solutions are unfeasible, accessing richer and more consistent wind resources.

- Enhanced Digitalization and Predictive Maintenance: Adoption of advanced analytics, IoT sensors, and digital twin technology for real-time monitoring, predictive maintenance, and optimized asset management, improving operational efficiency and reducing downtime.

AI Impact Analysis on Floating Offshore Wind Power

Artificial Intelligence (AI) is set to play a pivotal role in accelerating the development and operational efficiency of the Floating Offshore Wind Power Market. By leveraging sophisticated algorithms and machine learning capabilities, AI can optimize various stages of the project lifecycle, from site selection and design to construction, operation, and maintenance. This integration promises to reduce costs, enhance performance, and mitigate risks, ultimately contributing to the faster deployment and greater profitability of floating offshore wind farms. The impact of AI on this market can be observed through several key applications and benefits.

- Optimized Site Selection and Resource Assessment: AI algorithms analyze vast datasets, including wind patterns, wave heights, seabed conditions, and environmental factors, to identify optimal sites for floating wind farms, reducing uncertainty and improving energy yield predictions.

- Predictive Maintenance and Anomaly Detection: Machine learning models monitor turbine performance, structural integrity of platforms, and component health in real-time, predicting potential failures before they occur, minimizing downtime and maintenance costs.

- Enhanced Operational Efficiency and Grid Integration: AI-powered systems optimize power output by dynamically adjusting turbine pitch and yaw based on real-time wind conditions, and facilitate seamless integration with national grids by forecasting supply and demand.

- Automated Design and Engineering: AI tools can iterate through countless design variations for floating foundations, mooring systems, and electrical infrastructure, identifying the most efficient, cost-effective, and robust configurations for specific site conditions.

- Improved Project Management and Logistics: AI applications can optimize logistics for transportation, installation, and decommissioning, including vessel scheduling and resource allocation, leading to significant time and cost savings.

- Risk Management and Environmental Monitoring: AI assists in assessing and mitigating risks related to extreme weather events, marine life interaction, and operational hazards, enhancing safety and ensuring compliance with environmental regulations.

- Intelligent Supply Chain Optimization: AI can forecast demand for components, optimize inventory levels, and identify potential disruptions in the global supply chain, ensuring timely delivery and reducing project delays.

Key Takeaways Floating Offshore Wind Power Market Size & Forecast

- The Floating Offshore Wind Power Market is projected for substantial growth, driven by deep-water resource access and decarbonization targets.

- Market value expected to surge from USD 6.2 billion in 2025 to USD 50.0 billion by 2033, demonstrating a robust CAGR of 28.5%.

- Technological advancements in platform designs and mooring systems are key enablers for cost reduction and scalability.

- Strong governmental policies, incentives, and dedicated auction mechanisms are crucial in de-risking investments and accelerating deployment.

- Increasing industrialization and maturation of the supply chain are critical to achieving commercial scale and reducing Levelized Cost of Energy (LCOE).

- AI and digital technologies are enhancing site selection, operational efficiency, predictive maintenance, and overall project management.

- Integration with green hydrogen production presents a significant opportunity for market expansion and energy vector diversification.

- Addressing challenges like port infrastructure limitations, grid capacity, and skilled workforce availability is vital for sustained growth.

- Europe and Asia Pacific are leading the market, with North America rapidly emerging as a significant growth region.

- Long-term outlook remains highly positive, positioning floating offshore wind as a cornerstone of future global energy systems.

Floating Offshore Wind Power Market Drivers Analysis

The Floating Offshore Wind Power Market is propelled by a confluence of powerful drivers that underscore its immense potential and strategic importance in the global energy transition. These drivers range from urgent environmental imperatives to groundbreaking technological advancements and robust policy support, collectively fostering an environment conducive to rapid growth and widespread adoption. The ability of floating platforms to unlock vast, previously inaccessible deep-water wind resources is fundamentally reshaping the landscape of renewable energy, offering a solution to land scarcity and near-shore environmental constraints often associated with conventional wind projects. As global energy demand continues to rise and climate change concerns intensify, the imperative to diversify energy portfolios with scalable and sustainable alternatives becomes paramount, positioning floating offshore wind as a critical component of future energy security and decarbonization strategies.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Push for Decarbonization and Net-Zero Targets | +7.5% | Global, particularly EU, UK, US, Japan, South Korea | Short to Long Term |

| Technological Advancements and Cost Reduction | +6.8% | Global, especially R&D hubs in Europe and Asia | Medium to Long Term |

| Increasing Energy Demand and Energy Security Concerns | +5.5% | Globally, with emphasis on energy-importing nations | Short to Medium Term |

| Access to Deeper Water Wind Resources | +4.2% | Europe (Atlantic), US (Pacific), Japan, South Korea, Taiwan | Medium to Long Term |

| Supportive Government Policies and Regulatory Frameworks | +4.5% | UK, Norway, France, Portugal, US, Japan, South Korea | Short to Medium Term |

Floating Offshore Wind Power Market Restraints Analysis

Despite the immense potential and strong growth trajectory, the Floating Offshore Wind Power Market faces several significant restraints that could temper its expansion if not adequately addressed. These challenges primarily revolve around the nascent stage of the technology, requiring substantial upfront investment and sophisticated logistical operations. The development of a robust and localized supply chain capable of supporting large-scale commercial projects is still in its infancy, leading to potential bottlenecks and increased costs. Furthermore, the inherent complexities of operating in harsh marine environments, coupled with the need for extensive port infrastructure upgrades, present formidable hurdles that require coordinated efforts from industry, government, and financial institutions to overcome. Overcoming these restraints will be crucial for the floating offshore wind sector to fully realize its potential and achieve commercial viability at scale.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Project Financing Challenges | -6.0% | Global, particularly emerging markets | Short to Medium Term |

| Limited Port Infrastructure and Supply Chain Bottlenecks | -5.5% | Global, with acute issues in new market entrants | Short to Medium Term |

| Grid Connection and Transmission Limitations | -4.8% | Regions with aging grid infrastructure (e.g., some parts of Europe, US) | Medium to Long Term |

| Environmental Permitting and Stakeholder Opposition | -3.7% | Specific coastal regions with high ecological sensitivity | Short to Medium Term |

| Technology Standardization and Certification | -2.0% | Global, impacting insurance and financing | Short to Medium Term |

Floating Offshore Wind Power Market Opportunities Analysis

The Floating Offshore Wind Power Market is rich with promising opportunities that extend beyond mere electricity generation, positioning it as a cornerstone of the future energy ecosystem. These opportunities are rooted in the technology's inherent flexibility and its capacity to integrate with other emerging green technologies, creating new value chains and diversifying revenue streams. The expansive global deep-water potential, coupled with the increasing political will to invest in large-scale renewable projects, opens doors for significant market expansion into previously untapped regions. Furthermore, the drive towards circular economy principles and enhanced digitalization presents avenues for operational efficiencies and sustainable practices, ensuring the long-term viability and attractiveness of floating offshore wind as a premier clean energy solution.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Green Hydrogen Production | +6.0% | Europe, Asia Pacific (Japan, South Korea), North America | Medium to Long Term |

| Emerging Markets and Untapped Deep-Water Regions | +5.5% | US (California, Hawaii), Japan, South Korea, Taiwan, Brazil, India | Medium to Long Term |

| Development of Hybrid Projects (e.g., with Wave/Tidal Energy) | +4.0% | Europe (UK, Portugal), East Asia | Long Term |

| Advancements in Materials and Manufacturing Processes | +3.5% | Global, especially advanced manufacturing hubs | Short to Medium Term |

| Development of Digital Solutions and AI for O&M | +3.0% | Global, cross-sector application | Short to Medium Term |

Floating Offshore Wind Power Market Challenges Impact Analysis

The Floating Offshore Wind Power Market, while promising, is navigating a complex landscape of challenges that demand innovative solutions and concerted efforts from all stakeholders. These challenges are often intertwined, ranging from the need for massive infrastructure upgrades to the scarcity of specialized labor and the intricacies of operating in extreme offshore conditions. The relatively nascent stage of commercial deployment means that financial de-risking mechanisms and robust regulatory frameworks are still evolving, potentially slowing down investment decisions. Addressing these hurdles effectively will require significant public and private sector collaboration, sustained investment in research and development, and a strategic focus on building a resilient and localized supply chain capable of meeting the ambitious global deployment targets. Overcoming these challenges is paramount for the floating offshore wind industry to scale efficiently and cost-effectively.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Specialized Port and Fabrication Infrastructure | -5.0% | Global, especially new development regions | Short to Medium Term |

| Skilled Workforce Shortage and Training Needs | -4.5% | Global, impacting project timelines | Short to Medium Term |

| Extreme Weather Conditions and Operational Risks | -3.8% | North Sea, Pacific Ocean, North Atlantic | Long Term |

| Regulatory Harmonization and Permitting Delays | -3.2% | Cross-border projects, new policy environments | Short to Medium Term |

| Securing Long-Term Offtake Agreements and De-risking | -2.5% | Global, impacting investor confidence | Short to Medium Term |

Floating Offshore Wind Power Market - Updated Report Scope

This updated report provides a comprehensive and in-depth analysis of the Floating Offshore Wind Power Market, offering critical insights into its current landscape, future projections, and the underlying dynamics shaping its evolution. It delineates the market size, growth trajectory, key trends, and the strategic implications of technological advancements and policy shifts. The report’s scope is meticulously defined to provide stakeholders with actionable intelligence, covering market segmentation, regional performance, competitive landscape, and the impact of transformative factors like AI. This detailed assessment serves as an invaluable resource for investors, policymakers, developers, and technology providers seeking to navigate and capitalize on opportunities within this rapidly expanding sector.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 billion |

| Market Forecast in 2033 | USD 50.0 billion |

| Growth Rate | 28.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vestas, Siemens Gamesa Renewable Energy, Equinor, RWE Renewables, EDF Renewables, Principle Power, BW Ideol, Saipem, TechnipFMC, Aker Solutions, Hitachi, Sumitomo Heavy Industries, Doosan Heavy Industries & Construction, Ocean Winds, Mainstream Renewable Power, Cobra Wind International, Orsted, Nexans, Prysmian Group, Marmen |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Floating Offshore Wind Power Market is intricately segmented across various dimensions to provide a granular understanding of its structure, dynamics, and growth pockets. These segmentations are critical for stakeholders to identify specific market niches, tailor strategies, and assess competitive landscapes with greater precision. Analyzing the market through these lenses reveals the interplay of technological preferences, operational scales, and geographical concentrations, enabling a comprehensive view of the industry's multifaceted evolution. Each segment and sub-segment represents a distinct area of focus, collectively painting a complete picture of the market's current state and future potential, guiding investment and development decisions in this rapidly evolving sector.- By Foundation Type: This segment categorizes floating offshore wind platforms based on their structural design and stability mechanisms, crucial for adapting to varying water depths and seabed conditions.

- Semi-submersible: Characterized by a buoyant substructure partially submerged, providing stability through water ballast and large spacing between columns. Widely adopted for its stability and ease of assembly.

- Spar: A tall, slender, buoyant cylinder moored vertically, with most of its mass below the water surface, offering stability through deep draft and ballast. Ideal for very deep waters.

- Tension-leg Platform (TLP): A floating platform moored by vertical tensioned tethers to the seabed, providing high stability and minimal motion. Suitable for challenging wave conditions.

- Barge: A simpler, flat-bottomed platform often used in shallower floating wind applications, offering ease of fabrication and transport.

- Others: Includes emerging and hybrid concepts such as hinged barges, multi-body platforms, and other innovative designs aimed at cost reduction and improved performance.

- By Component: This segmentation details the various critical parts and systems that constitute a floating offshore wind farm, highlighting the supply chain and manufacturing focus.

- Turbines: The wind turbine generators (WTGs) that convert wind energy into electricity, including blades, nacelle, and tower. Modern turbines are increasingly powerful.

- Substructures: The floating foundations themselves, including the primary structure that supports the turbine and provides buoyancy.

- Mooring and Anchoring Systems: The chains, ropes, connectors, and anchors that secure the floating platform to the seabed, crucial for stability and station-keeping.

- Electrical Infrastructure: Encompasses subsea cables, offshore substations, and onshore grid connections necessary to transmit power from the wind farm to consumers.

- Others: Includes balance of plant components, control systems, navigation aids, and various auxiliary equipment essential for operation.

- By Depth: This segmentation reflects the water depth at which floating offshore wind platforms are deployed, directly influencing foundation choice and technological requirements.

- Shallow (60m-100m): Depths where floating solutions begin to be more viable or competitive than fixed-bottom alternatives, often transitional areas.

- Medium (100m-200m): The predominant depth range for many current and planned floating offshore wind projects, balancing accessibility and resource quality.

- Deep (>200m): Ultramaritime depths where floating technology is the only viable option, offering access to vast, high-quality wind resources far offshore.

- By Application: This segment categorizes the primary use cases and strategic objectives for floating offshore wind power, illustrating its diverse potential.

- Utility-scale Power Generation: Large-scale floating wind farms designed to feed electricity directly into national grids for widespread consumption.

- Research & Development Projects: Pilot and demonstration projects focused on testing new technologies, materials, and methodologies to advance the industry.

- Offshore Green Hydrogen Production: Projects where floating wind energy is directly used to power offshore electrolysis for the production of green hydrogen, offering a new energy carrier.

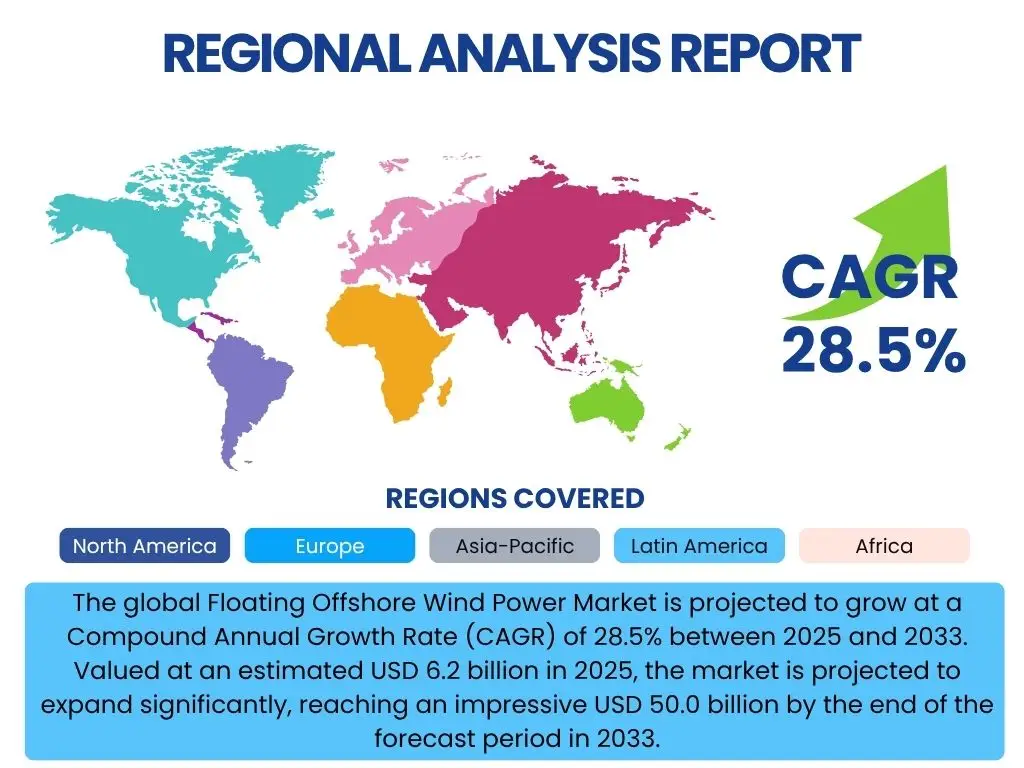

Regional Highlights

The global Floating Offshore Wind Power Market exhibits distinct regional dynamics, with certain geographies leading in terms of project development, policy support, and technological innovation. These regions are characterized by specific drivers, challenges, and strategic initiatives that define their prominence in the emerging floating offshore wind landscape. Understanding these regional nuances is crucial for market participants to identify growth opportunities, tailor investment strategies, and navigate local regulatory environments. The concentration of deep-water resources, coupled with ambitious renewable energy targets and robust policy frameworks, underpins the leadership of key countries and zones in advancing this nascentbut rapidly expanding industry.- Europe: Europe remains the undisputed global leader in floating offshore wind development, particularly the United Kingdom, Norway, France, Portugal, and Spain. This dominance is driven by pioneering R&D, strong political support through dedicated auction rounds and subsidies (e.g., UK's Contracts for Difference, France's tenders), extensive deep-water coastlines, and a mature offshore oil and gas industry providing transferable skills and infrastructure. The North Sea and Atlantic seaboard offer exceptional wind resources, making floating wind a strategic asset for decarbonization and energy independence.

- Asia Pacific (APAC): The APAC region is rapidly emerging as a significant growth hub, propelled by countries like Japan, South Korea, and Taiwan. These nations possess extensive coastlines with deep waters unsuitable for fixed-bottom installations but excellent for floating wind. Strong government commitments to carbon neutrality, energy security, and industrial development are fostering an accelerating market. Large-scale projects are planned, and local content requirements are driving the development of indigenous supply chains and technological capabilities. China is also investing in floating wind, aiming to scale up its renewable energy capacity.

- North America: The United States, particularly its Pacific coast states (California, Oregon, Hawaii), is poised for substantial growth in floating offshore wind. The vast deep-water areas off its coasts, combined with ambitious state-level renewable energy mandates and federal initiatives (e.g., Department of Energy funding, Bureau of Ocean Energy Management leasing), are creating a powerful impetus. Challenges like grid interconnection and port infrastructure are being addressed through significant investment plans, signaling a strong long-term commitment. Canada also holds potential, especially off its Atlantic and Pacific coasts.

- Middle East and Africa (MEA): While still in nascent stages, the MEA region presents long-term potential for floating offshore wind, particularly in countries with suitable deep-water coastlines and growing energy demands, alongside ambitious clean energy targets. Interest is growing in regions that can leverage floating wind for green hydrogen production, aligning with future export strategies. Pilot projects and feasibility studies are beginning to emerge, indicating future market entry.

- Latin America: Similar to MEA, Latin America is an emerging market with significant deep-water potential, especially off the coasts of Brazil, Chile, and Colombia. These countries possess strong wind resources and are exploring floating offshore wind as part of their renewable energy diversification strategies. The development is contingent on supportive regulatory frameworks, attracting international investment, and developing local expertise.

Top Key Players:

The market research report covers the analysis of key stakeholders of the Floating Offshore Wind Power Market. Some of the leading players profiled in the report include -- Vestas

- Siemens Gamesa Renewable Energy

- Equinor

- RWE Renewables

- EDF Renewables

- Principle Power

- BW Ideol

- Saipem

- TechnipFMC

- Aker Solutions

- Hitachi

- Sumitomo Heavy Industries

- Doosan Heavy Industries & Construction

- Ocean Winds

- Mainstream Renewable Power

- Cobra Wind International

- Orsted

- Nexans

- Prysmian Group

- Marmen

Frequently Asked Questions:

What is floating offshore wind power?

Floating offshore wind power refers to wind turbines mounted on floating platforms anchored to the seabed, allowing for deployment in deep waters where traditional fixed-bottom foundations are not feasible. This technology enables access to stronger, more consistent wind resources far from shore, unlocking vast new areas for renewable energy generation.Why is floating offshore wind power important?

Floating offshore wind power is crucial for several reasons: it expands access to high-quality wind resources in deep waters, facilitates large-scale clean energy generation where coastal land is scarce, contributes significantly to decarbonization goals, enhances energy security by diversifying power sources, and fosters innovation in marine engineering and renewable energy technologies.What are the main types of floating offshore wind foundations?

The main types of floating offshore wind foundations include:- Semi-submersible: Partially submerged, providing stability through buoyancy and water ballast.

- Spar: A tall, slender cylinder with deep draft, relying on ballast for stability.

- Tension-leg Platform (TLP): Secured by vertical tensioned tethers, offering high stability with minimal motion.

- Barge: A simpler, flat-bottomed platform, often used in shallower floating applications.

What is the forecast for the floating offshore wind market?

The global Floating Offshore Wind Power Market is projected to grow significantly. It is forecast to increase from an estimated USD 6.2 billion in 2025 to USD 50.0 billion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of 28.5% during this period. This growth is driven by increasing global demand for renewable energy, technological advancements, and supportive government policies.What are the key challenges in deploying floating offshore wind?

Key challenges in deploying floating offshore wind include high capital expenditure, the need for specialized port infrastructure and supply chain development, limitations in grid connection and transmission, environmental permitting complexities, and the shortage of a skilled workforce. Overcoming these hurdles requires significant investment and collaborative efforts across the industry and government.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted