Flat Display Panel Market

Flat Display Panel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705588 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

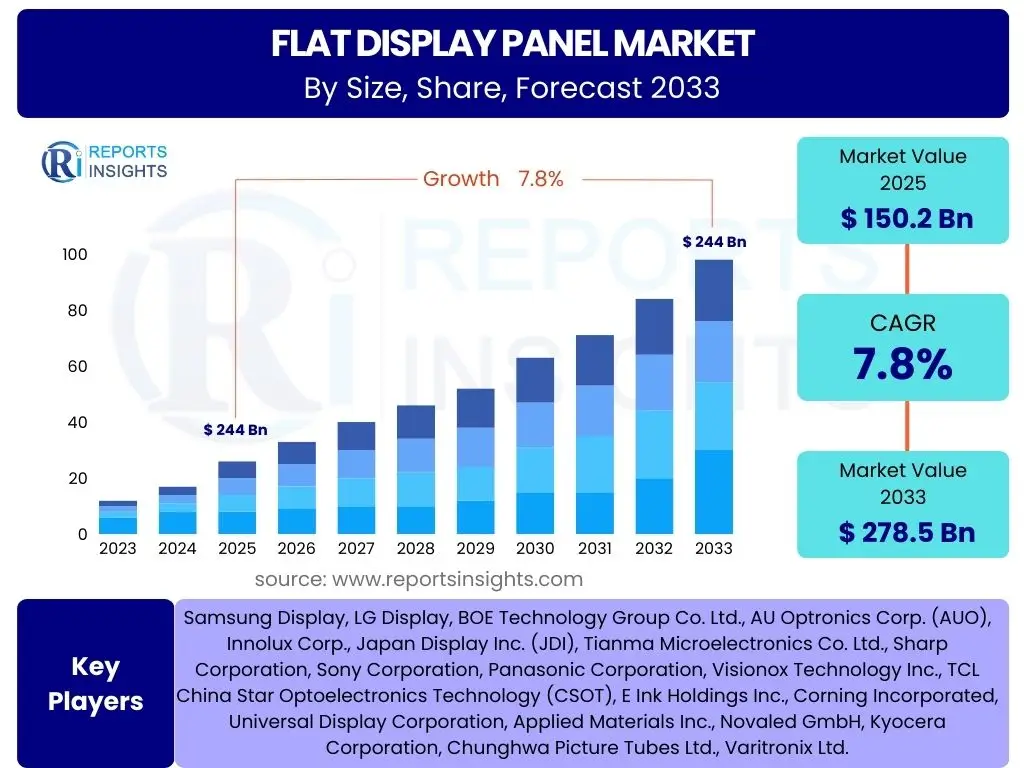

Flat Display Panel Market Size

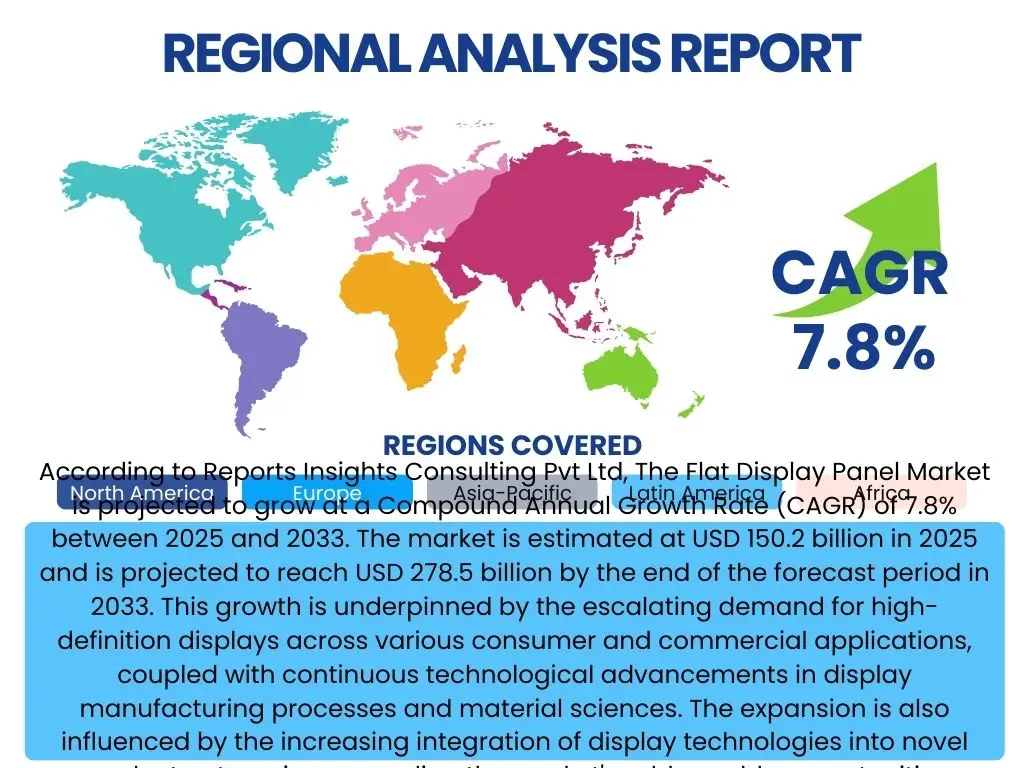

According to Reports Insights Consulting Pvt Ltd, The Flat Display Panel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 150.2 billion in 2025 and is projected to reach USD 278.5 billion by the end of the forecast period in 2033. This growth is underpinned by the escalating demand for high-definition displays across various consumer and commercial applications, coupled with continuous technological advancements in display manufacturing processes and material sciences. The expansion is also influenced by the increasing integration of display technologies into novel product categories, expanding the market's addressable opportunities significantly.

Key Flat Display Panel Market Trends & Insights

Inquiries into the flat display panel market frequently center on identifying the significant technological shifts and market dynamics that are reshaping the industry. The current landscape is defined by an accelerating push towards superior visual fidelity, energy efficiency, and novel form factors. Consumers and industries alike are seeking more immersive, interactive, and flexible display solutions, driving innovation in material science and panel architecture.

Furthermore, the market is experiencing a notable trend towards customization and specialized display applications, moving beyond traditional consumer electronics. This includes robust displays for industrial use, sophisticated medical imaging panels, and interactive screens for retail and education. The emphasis is also on sustainability, with a growing demand for eco-friendly manufacturing processes and recyclable display components, reflecting a broader industry commitment to environmental responsibility.

- Proliferation of advanced display technologies such as OLED, Mini-LED, and Micro-LED for enhanced picture quality and energy efficiency.

- Increasing adoption of flexible, foldable, and transparent display form factors across consumer electronics and niche applications.

- Growing demand for large-screen displays in televisions, public signage, and automotive infotainment systems.

- Integration of interactive and touch functionalities for intuitive user experiences in diverse sectors like education, retail, and healthcare.

- Shift towards higher resolutions (4K, 8K) and faster refresh rates for gaming, professional content creation, and cinematic viewing.

- Emphasis on eco-friendly manufacturing processes and sustainable display materials to reduce environmental impact.

AI Impact Analysis on Flat Display Panel

Common questions concerning the impact of Artificial Intelligence (AI) on the flat display panel market revolve around its role in enhancing display performance, optimizing manufacturing, and creating new user interaction paradigms. AI is increasingly being leveraged to improve image processing capabilities, enabling displays to offer more vivid colors, deeper contrasts, and adaptive brightness based on content and ambient lighting conditions. This translates into a more personalized and immersive viewing experience for the end-user, directly impacting perceived display quality.

Beyond visual enhancement, AI also plays a critical role in the production and quality control of flat display panels. Machine learning algorithms are employed to detect microscopic defects during manufacturing, optimize production yields, and predict maintenance needs for equipment, thereby reducing costs and improving efficiency. Furthermore, AI facilitates intelligent content delivery and user interface adaptation, allowing displays to learn user preferences and present information in a more intuitive and responsive manner. This pervasive integration of AI is not merely incremental but transformative, promising a new generation of smart and responsive display systems.

- AI-powered image processing for enhanced contrast, color accuracy, and dynamic range in display content.

- Optimization of display manufacturing processes through AI for defect detection, yield improvement, and predictive maintenance.

- Development of adaptive display technologies that adjust screen settings based on user behavior, content, and environmental factors.

- Integration of AI for advanced gesture recognition and natural language processing in smart displays, enabling more intuitive user interactions.

- Facilitation of personalized content delivery and advertising on public displays through AI-driven analytics.

- Enabling of real-time calibration and self-correction mechanisms for long-term display performance and consistency.

Key Takeaways Flat Display Panel Market Size & Forecast

Analysis of user queries regarding the flat display panel market size and forecast consistently highlights interest in growth drivers, technological shifts, and regional market dominance. A primary takeaway is the significant projected expansion, fueled by innovation in display technologies and their ubiquitous integration across various sectors. The market's resilience is notable, driven by both replacement demand in mature markets and new adoption in emerging economies, alongside the continuous evolution of application areas.

Furthermore, the forecast underscores the pivotal role of advanced display technologies such as OLED and Micro-LED in shaping future growth trajectories. These technologies are not only enhancing existing product categories but also enabling entirely new use cases, from flexible wearable devices to sophisticated automotive displays. The market is also poised for dynamic shifts in regional influence, with Asia Pacific maintaining its manufacturing stronghold while North America and Europe lead in advanced technology adoption and high-value applications, collectively driving the substantial forecasted market value.

- Robust Compound Annual Growth Rate (CAGR) indicating sustained market expansion through 2033.

- Substantial increase in market valuation, reaching nearly double its 2025 size by the end of the forecast period.

- Technological advancements, particularly in OLED, Mini-LED, and Micro-LED, are central to future growth.

- Diversification of display applications beyond traditional consumer electronics is a key growth accelerator.

- Strong demand from emerging economies and increasing disposable incomes contribute significantly to market volume.

- Continuous innovation in display resolution, energy efficiency, and form factors remains a critical market driver.

Flat Display Panel Market Drivers Analysis

The flat display panel market is significantly propelled by several key factors that stimulate both demand and technological innovation. A primary driver is the pervasive integration of displays into everyday life, from smartphones and televisions to smart home devices and public information systems. Consumers increasingly demand higher resolution, better color reproduction, and more immersive viewing experiences, which continuously pushes manufacturers to innovate and introduce advanced display technologies. This inherent desire for visual fidelity and interactive capability across all device categories forms a foundational element of market expansion.

Another crucial driver stems from the rapid growth of diverse end-use industries that rely heavily on display technologies. The automotive sector, for instance, is increasingly incorporating multiple displays for infotainment, navigation, and driver assistance systems, demanding robust and high-performance panels. Similarly, healthcare, retail, and industrial automation sectors are adopting specialized displays for diagnostic imaging, interactive digital signage, and human-machine interfaces, respectively. This widespread application diversification not only broadens the market but also encourages the development of display solutions tailored to specific industrial requirements, thereby sustaining strong market momentum.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Consumer Electronics | +2.5% | Global, particularly Asia Pacific & North America | 2025-2033 |

| Technological Advancements in Display Panels | +2.0% | Global, led by Asia Pacific & Europe | 2025-2033 |

| Rising Adoption in Automotive Sector | +1.5% | Europe, North America, Asia Pacific | 2026-2033 |

| Growth of Digital Signage and Commercial Displays | +1.0% | North America, Europe, Asia Pacific (Tier 1 cities) | 2025-2031 |

| Expanding Applications in Healthcare & Industrial Segments | +0.8% | North America, Europe, select APAC countries | 2027-2033 |

Flat Display Panel Market Restraints Analysis

Despite robust growth, the flat display panel market faces several significant restraints that could impede its overall expansion. One major challenge is the high manufacturing cost associated with advanced display technologies, particularly OLED and Micro-LED panels. The complex production processes, expensive raw materials, and the need for high-precision equipment contribute to higher unit costs, which can limit widespread adoption, especially in price-sensitive markets or for entry-level products. This cost factor creates a barrier to entry for smaller manufacturers and can slow down the transition to newer technologies for consumers.

Another notable restraint is the market saturation in certain traditional consumer electronics segments, such as smartphones and televisions, in developed regions. While there is still demand for upgrades and replacements, the rapid growth seen in previous decades has tempered, leading to more modest sales volumes. Furthermore, intense competition among existing players often leads to price wars, impacting profit margins for manufacturers. The supply chain vulnerabilities, particularly those related to the availability of critical components and geopolitical tensions affecting global trade, also pose ongoing challenges, potentially disrupting production and increasing operational complexities within the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Displays | -1.2% | Global | 2025-2030 |

| Market Saturation in Mature Consumer Electronics Segments | -0.8% | North America, Europe, developed APAC | 2025-2033 |

| Intense Price Competition Among Manufacturers | -0.7% | Global | 2025-2028 |

| Supply Chain Disruptions and Geopolitical Instability | -0.5% | Global, particularly Asia Pacific (manufacturing hubs) | 2025-2027 |

| Environmental Regulations and Disposal Challenges | -0.3% | Europe, North America, select APAC countries | 2028-2033 |

Flat Display Panel Market Opportunities Analysis

Significant opportunities in the flat display panel market arise from emerging technological innovations and the expansion into new application areas. The development of next-generation display technologies, such as advanced Micro-LED and Quantum Dot displays, presents considerable avenues for growth by offering superior performance characteristics like higher brightness, improved color volume, and extended lifespan. These advancements are not only enhancing existing product lines but also enabling the creation of entirely new product categories, promising a fresh wave of consumer and industrial adoption. The continued miniaturization and increased efficiency of these displays further open doors for integration into compact and power-sensitive devices.

Beyond technological frontiers, the increasing demand for displays in specialized and industrial applications represents a burgeoning opportunity. Sectors such as augmented reality/virtual reality (AR/VR) devices, smart wearables, advanced automotive cockpits, and specialized medical imaging equipment are poised for substantial growth, requiring highly customized and robust display solutions. These niche markets often command higher profit margins and less price sensitivity compared to mass-market consumer electronics. Furthermore, the push towards smart cities and intelligent infrastructure creates demand for large-format, durable, and energy-efficient displays for public information, advertising, and monitoring, collectively presenting diverse and lucrative pathways for market expansion and innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Advanced Technologies (Micro-LED, QD-OLED) | +1.8% | Global, especially North America & Asia Pacific | 2027-2033 |

| Growth in Automotive Display Market | +1.5% | Europe, North America, China | 2025-2033 |

| Expansion into Augmented/Virtual Reality (AR/VR) Devices | +1.2% | North America, Asia Pacific, Europe | 2026-2033 |

| Increasing Demand for Flexible and Transparent Displays | +1.0% | Asia Pacific, North America | 2028-2033 |

| Development of Smart City & Public Information Displays | +0.9% | Global, with focus on urban centers | 2025-2032 |

Flat Display Panel Market Challenges Impact Analysis

The flat display panel market encounters several critical challenges that demand strategic responses from industry players. One significant hurdle is the intense global competition and the resulting pressure on pricing. As more manufacturers enter the market and established players expand capacity, oversupply can lead to declining average selling prices, eroding profit margins and making it difficult for companies to sustain investments in research and development for future innovations. This competitive intensity necessitates continuous cost optimization and differentiation strategies to maintain market viability.

Furthermore, the rapid pace of technological obsolescence poses a constant challenge. Displays developed with significant investment can quickly become outdated as newer, more efficient, or higher-performing technologies emerge. This necessitates a delicate balance between investing in cutting-edge R&D and ensuring a reasonable return on investment before a technology becomes obsolete. Additionally, complex supply chains, often spanning multiple countries, are vulnerable to geopolitical events, trade disputes, and natural disasters, leading to component shortages, logistics disruptions, and increased operational risks, all of which can severely impact production schedules and market supply.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition and Margin Erosion | -1.0% | Global | 2025-2030 |

| Rapid Technological Obsolescence and R&D Investment | -0.7% | Global | 2025-2033 |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.6% | Asia Pacific (manufacturing hubs), Global (trade) | 2025-2027 |

| Environmental Concerns and Regulatory Compliance | -0.4% | Europe, North America, specific Asian markets | 2028-2033 |

| High Capital Expenditure for New Production Facilities | -0.3% | Global | 2025-2031 |

Flat Display Panel Market - Updated Report Scope

This report provides a comprehensive analysis of the global Flat Display Panel Market, encompassing a detailed review of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key regions. It offers an in-depth understanding of the market dynamics, technological landscape, and competitive environment to assist stakeholders in making informed strategic decisions and identifying growth prospects. The report delineates the market’s trajectory from historical performance to future projections, highlighting the critical factors influencing its evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 150.2 Billion |

| Market Forecast in 2033 | USD 278.5 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Display, LG Display, BOE Technology Group Co. Ltd., AU Optronics Corp. (AUO), Innolux Corp., Japan Display Inc. (JDI), Tianma Microelectronics Co. Ltd., Sharp Corporation, Sony Corporation, Panasonic Corporation, Visionox Technology Inc., TCL China Star Optoelectronics Technology (CSOT), E Ink Holdings Inc., Corning Incorporated, Universal Display Corporation, Applied Materials Inc., Novaled GmbH, Kyocera Corporation, Chunghwa Picture Tubes Ltd., Varitronix Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Flat Display Panel Market is meticulously segmented to provide granular insights into its diverse components and their respective market dynamics. This segmentation facilitates a comprehensive understanding of technological adoption rates, application-specific demands, and the varying preferences across different display sizes and form factors. Each segment contributes uniquely to the overall market landscape, influenced by specific technological advancements, production capabilities, and consumer or industrial requirements.

- By Technology: This segment differentiates displays based on their underlying panel technology, including Liquid Crystal Display (LCD), Organic Light Emitting Diode (OLED), Light Emitting Diode (LED), Quantum Dot Display (QLED), Micro-LED, Electronic Paper Display (EPD), and Plasma Display Panel (PDP). OLED and Micro-LED are anticipated to witness the fastest growth due to superior visual performance and increasing application scope.

- By Application: This segmentation highlights the primary uses of flat display panels. Key applications include Consumer Electronics (smartphones, tablets, laptops, wearables, televisions), Automotive Displays (infotainment, instrument clusters), Digital Signage (public information, advertising), Medical Displays (diagnostic, surgical), Industrial Displays (control panels, machinery interfaces), and specialized uses in Avionics & Marine, smart home appliances, education, and sports & entertainment.

- By Display Size: Categorization by size provides insights into market demand for different form factors, encompassing Small Displays (typically under 6 inches for wearables and smartphones), Medium Displays (6-20 inches for tablets and small monitors), and Large Displays (over 20 inches for televisions, monitors, and public displays). The large display segment is witnessing significant growth due to trends in home entertainment and digital signage.

- By Form Factor: This segment distinguishes displays by their physical shape and flexibility, including Rigid Displays (traditional flat panels), Flexible Displays (bendable or rollable), Foldable Displays (devices that fold upon themselves), and Transparent Displays. Flexible and foldable displays are emerging as significant trends, particularly in mobile devices and innovative architectural designs.

- By End-Use Industry: This segment analyzes the market based on the broad sectors utilizing flat display panels. These industries include Residential (home entertainment), Commercial (offices, retail, hospitality), Industrial (manufacturing, logistics), Automotive (vehicle integration), Healthcare (hospitals, clinics), and Government & Public Sector (defense, public infrastructure). Each industry presents unique requirements concerning display durability, performance, and specific functionalities.

Regional Highlights

The Flat Display Panel Market exhibits significant regional disparities, driven by varying levels of technological adoption, manufacturing capabilities, and consumer purchasing power. Asia Pacific (APAC) stands as the dominant region, primarily due to the presence of major display manufacturing hubs in countries like South Korea, China, Japan, and Taiwan. These nations lead in the production of advanced display technologies, including OLED and LCD panels, supplying a vast global market. The region also benefits from a large consumer base with increasing disposable incomes, driving demand for consumer electronics. Furthermore, the rapid growth of automotive and digital signage industries in emerging economies like China and India fuels regional market expansion.

North America holds a substantial market share, characterized by high adoption rates of advanced display technologies and a strong presence of key technology innovators. The region's demand is driven by high-end consumer electronics, significant investment in automotive display integration, and the widespread use of digital signage in retail and corporate environments. The sophisticated healthcare infrastructure also contributes to the demand for high-resolution medical displays. Continuous research and development activities, coupled with early adoption of cutting-edge display solutions, position North America as a leading market for innovation and premium product consumption.

Europe represents a mature but growing market, propelled by stringent energy efficiency regulations, a strong automotive sector, and increasing demand for smart home and industrial automation displays. Countries like Germany and the UK are at the forefront of adopting high-quality displays for premium televisions and professional applications. The region's focus on sustainable manufacturing practices also influences the types of display technologies being adopted. Latin America, the Middle East, and Africa (MEA) are emerging markets, characterized by increasing urbanization, rising internet penetration, and a growing consumer electronics market. While smaller in market size compared to APAC, North America, and Europe, these regions offer significant future growth potential as economic development and technological access expand, driving demand for affordable and increasingly sophisticated display solutions across various applications.

- Asia Pacific (APAC): Dominant market share attributed to major manufacturing bases (South Korea, China, Japan, Taiwan) and a large consumer electronics market; rapid adoption of advanced technologies like OLED and Micro-LED.

- North America: Strong demand for high-end consumer electronics, significant investments in automotive displays, and widespread adoption of digital signage; high technological readiness and early adoption of innovations.

- Europe: Mature market with a focus on premium displays and energy-efficient solutions; robust demand from the automotive, industrial, and healthcare sectors; stringent environmental regulations influencing product development.

- Latin America: Emerging market driven by increasing disposable incomes and growing demand for smartphones and televisions; gradual adoption of advanced display technologies.

- Middle East and Africa (MEA): Growth fueled by urbanization, infrastructure development, and increasing penetration of consumer electronics; significant potential in digital signage and public displays.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Flat Display Panel Market.- Samsung Display

- LG Display

- BOE Technology Group Co. Ltd.

- AU Optronics Corp. (AUO)

- Innolux Corp.

- Japan Display Inc. (JDI)

- Tianma Microelectronics Co. Ltd.

- Sharp Corporation

- Sony Corporation

- Panasonic Corporation

- Visionox Technology Inc.

- TCL China Star Optoelectronics Technology (CSOT)

- E Ink Holdings Inc.

- Corning Incorporated

- Universal Display Corporation

- Applied Materials Inc.

- Novaled GmbH

- Kyocera Corporation

- Chunghwa Picture Tubes Ltd.

- Varitronix Ltd.

Frequently Asked Questions

What is the current market size and projected growth of the Flat Display Panel Market?

The Flat Display Panel Market is estimated at USD 150.2 billion in 2025 and is projected to reach USD 278.5 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period.

Which technologies are driving growth in the Flat Display Panel Market?

Growth is significantly driven by advanced technologies such as OLED (Organic Light Emitting Diode), Mini-LED, and Micro-LED, offering superior visual performance, energy efficiency, and enabling new form factors like flexible and transparent displays.

How is Artificial Intelligence impacting the Flat Display Panel Market?

AI impacts the market by enhancing image processing for improved display quality, optimizing manufacturing processes for higher yields, and enabling adaptive user interfaces for more intuitive interactions across various applications.

What are the primary applications of Flat Display Panels?

Flat display panels are predominantly used in consumer electronics (smartphones, TVs, laptops), automotive infotainment systems, digital signage, medical equipment, industrial control systems, and emerging applications like AR/VR devices and smart home appliances.

Which region holds the largest market share in the Flat Display Panel Market?

Asia Pacific (APAC) holds the largest market share due to the concentration of major display manufacturing facilities and a vast consumer base, particularly in countries like South Korea, China, and Japan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted