Fiber Enclosure Market

Fiber Enclosure Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710115 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

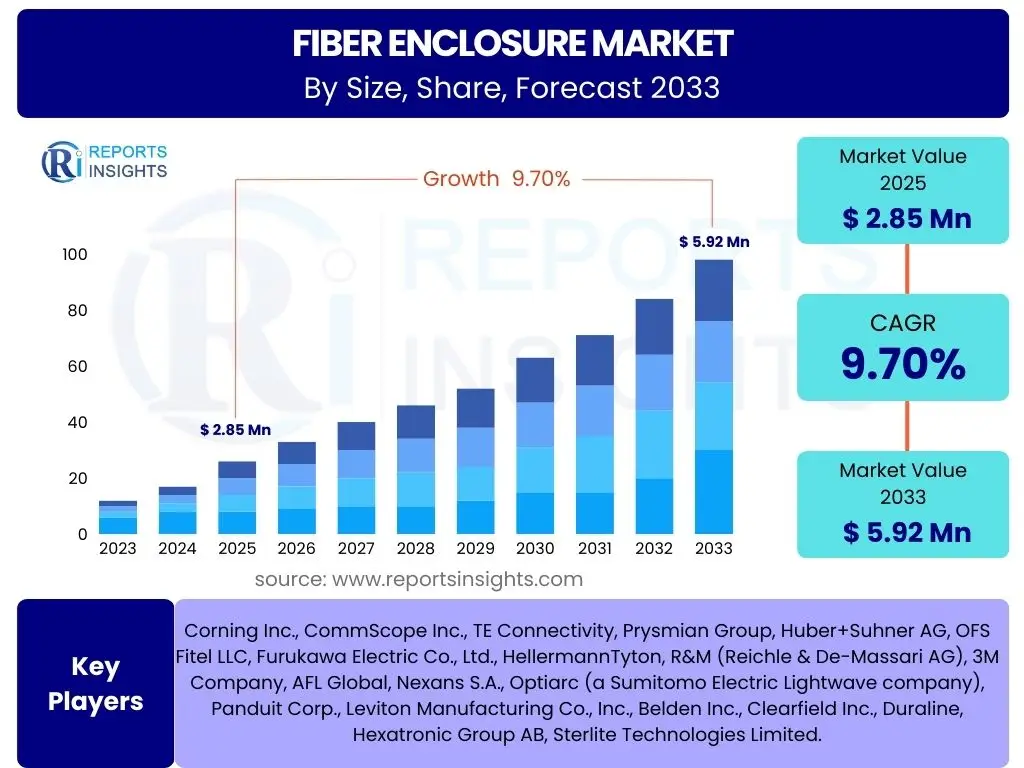

Fiber Enclosure Market Size

According to Reports Insights Consulting Pvt Ltd, The Fiber Enclosure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 2.85 Billion in 2025 and is projected to reach USD 5.92 Billion by the end of the forecast period in 2033.

Key Fiber Enclosure Market Trends & Insights

User queries regarding Fiber Enclosure market trends frequently highlight the impact of evolving network infrastructures and the growing demand for high-speed data. The market is experiencing significant transformation driven by the aggressive rollout of 5G technology, which necessitates a denser fiber optic network and robust, weather-resistant enclosures to protect connections in diverse environments. Furthermore, the expansion of data centers globally, coupled with the increasing adoption of cloud computing and IoT devices, fuels the demand for high-density, modular fiber enclosures that support efficient cable management and future scalability.

Another prominent area of interest among users concerns the advancements in enclosure materials and designs. There is a discernible shift towards more compact, durable, and environmentally resilient enclosures capable of withstanding harsh conditions, particularly in outdoor deployments. The emphasis on plug-and-play solutions and pre-terminated fiber systems is also a key trend, aimed at reducing installation time and costs, thereby improving overall operational efficiency. These trends collectively underscore the industry's focus on enhancing network reliability, simplifying deployment, and adapting to the escalating data traffic demands.

- Aggressive Global 5G Network Rollouts Driving Demand for Outdoor and FTTH Enclosures

- Surge in Data Center Expansion and Cloud Computing Requiring High-Density Fiber Management Solutions

- Increasing Adoption of Pre-terminated Fiber Solutions for Faster and More Efficient Deployments

- Technological Advancements in Material Science for Enhanced Durability and Environmental Protection

- Growing Demand for Modular and Scalable Enclosure Designs to Accommodate Future Network Upgrades

AI Impact Analysis on Fiber Enclosure

Common user questions regarding AI's impact on Fiber Enclosures often revolve around how artificial intelligence can optimize network management, enhance predictive maintenance, and inform future infrastructure development. AI is poised to significantly influence the operational aspects of fiber networks, including the performance and longevity of their physical components like enclosures. Through AI-driven analytics, network operators can gain deeper insights into traffic patterns, identify potential vulnerabilities, and predict maintenance needs for fiber optic infrastructure, including the enclosures that protect critical splice and termination points. This predictive capability can minimize downtime, extend the lifespan of enclosures, and optimize resource allocation for repairs and upgrades.

Furthermore, AI can contribute to the intelligent design and deployment of fiber enclosures. By analyzing vast datasets related to environmental conditions, network performance, and installation challenges, AI algorithms can provide recommendations for optimal enclosure placement, material selection, and design features that enhance resilience and efficiency. While AI does not directly interact with the physical enclosure, its influence on network planning, monitoring, and maintenance indirectly impacts the demand for specific types of enclosures, promoting solutions that are compatible with smart network management systems and facilitate easy access for automated diagnostics. The integration of AI also drives the need for more structured and easily identifiable fiber routing within enclosures to support automated inventory and fault location systems.

- AI-driven predictive maintenance for fiber optic networks, reducing enclosure-related failures.

- Optimization of network design and deployment through AI, influencing enclosure specifications.

- Enhanced monitoring of environmental conditions impacting enclosures via AI-powered sensors.

- Development of smart enclosures with integrated sensors for real-time data collection for AI analytics.

- Increased demand for modular and easily accessible enclosures to facilitate AI-assisted diagnostics and repairs.

Key Takeaways Fiber Enclosure Market Size & Forecast

The primary insights derived from the analysis of the Fiber Enclosure market size and forecast consistently highlight robust growth driven by foundational shifts in global digital infrastructure. Users frequently inquire about the underlying factors contributing to this expansion and the long-term sustainability of the market. The consistent deployment of advanced telecommunication technologies, such as 5G, and the relentless expansion of broadband networks, including Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB), are identified as the most significant growth catalysts. These initiatives require a substantial increase in the physical fiber infrastructure, thereby escalating the demand for reliable and durable enclosures to protect these critical connections.

Moreover, the forecast indicates a sustained upward trajectory, supported by the continuous growth of data centers and the pervasive adoption of cloud services, which necessitate complex and high-density fiber optic cabling. The market is not only growing in volume but also evolving in terms of technological sophistication, with a trend towards more compact, modular, and environmentally resilient enclosures. This evolution is crucial for accommodating the increasing density of fiber connections while simplifying installation and maintenance. The market’s future is intrinsically linked to global digitalization efforts, ensuring its continued expansion throughout the forecast period.

- Significant growth projected, driven by global 5G rollout and extensive FTTH/B deployments.

- Data center expansion and cloud computing adoption are critical demand generators.

- Technological advancements in enclosure design and materials are crucial for market evolution.

- Market resilience is strong due to the indispensable nature of fiber optic infrastructure.

- Sustainable growth expected as digital transformation accelerates worldwide.

Fiber Enclosure Market Drivers Analysis

The Fiber Enclosure market is primarily propelled by the insatiable global demand for high-speed internet and reliable network connectivity. The aggressive deployment of 5G wireless technology stands as a paramount driver, necessitating an extensive and dense fiber optic backhaul infrastructure to support its high bandwidth and low latency requirements. This proliferation of 5G base stations, often requiring fiber to be brought closer to the end-user, directly translates into increased demand for robust outdoor fiber enclosures designed for environmental protection and efficient cable management. Similarly, government initiatives and private investments in Fiber-to-the-Home (FTTH) and Fiber-to-the-Curb (FTTC) projects across both developed and developing regions are significantly expanding the reach of fiber networks, thereby fueling the need for various types of fiber enclosures, including distribution, splice, and termination boxes, to connect homes and businesses.

Beyond telecommunications, the exponential growth of data centers globally represents another critical driver. As enterprises increasingly migrate their operations to cloud platforms and as the volume of digital data continues to surge, the expansion of hyper-scale and co-location data centers becomes imperative. These facilities require vast amounts of fiber optic cabling and, consequently, high-density, modular fiber enclosures to manage and protect these connections within a controlled environment. The need for efficient space utilization, ease of maintenance, and scalability within data centers drives innovation and demand for advanced enclosure solutions. Additionally, the proliferation of smart cities initiatives, which rely heavily on interconnected fiber infrastructure for various applications like intelligent transportation systems, surveillance, and smart utilities, further contributes to the market's upward trajectory, demanding specialized enclosures that integrate seamlessly into urban environments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Rollouts | +3.2% | North America, Asia Pacific, Europe | 2025-2033 |

| Expansion of Data Centers & Cloud Computing | +2.8% | North America, Europe, Asia Pacific (China, India) | 2025-2033 |

| Increasing Fiber-to-the-Home (FTTH) Deployments | +2.5% | Asia Pacific, Europe, Latin America | 2025-2033 |

| Growth in Smart City Initiatives | +1.2% | Europe, Asia Pacific, Middle East | 2025-2033 |

Fiber Enclosure Market Restraints Analysis

Despite the robust growth drivers, the Fiber Enclosure market faces several restraints that could potentially temper its expansion. One significant challenge is the high initial capital expenditure required for fiber optic network deployment. The cost associated with laying fiber optic cables, acquiring active and passive components, and installing enclosures, especially in new or underdeveloped areas, can be substantial. This high investment barrier can slow down projects, particularly in regions with limited funding or where return on investment periods are extended. Consequently, this financial hurdle can delay or reduce the scale of fiber infrastructure projects, directly impacting the demand for fiber enclosures.

Another prominent restraint is the shortage of skilled labor for fiber optic installation and maintenance. The specialized nature of fiber optic technology requires trained technicians for proper splicing, termination, and enclosure installation to ensure optimal network performance. A scarcity of such skilled professionals can lead to increased labor costs, project delays, and potentially compromise the quality of installations. This issue is particularly prevalent in rapidly expanding markets where the pace of infrastructure development outstrips the availability of qualified personnel. Furthermore, stringent regulatory hurdles and environmental impact assessments, especially for large-scale outdoor deployments, can introduce complexities and prolong project timelines, adding to overall costs and acting as a bottleneck for market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs for Fiber Infrastructure | -1.8% | Global, particularly emerging markets | 2025-2030 |

| Shortage of Skilled Technicians for Installation & Maintenance | -1.5% | North America, Europe, parts of Asia Pacific | 2025-2033 |

| Environmental and Regulatory Challenges for Deployment | -1.0% | Europe, North America | 2025-2033 |

| Logistical Challenges in Remote or Difficult Terrains | -0.7% | Africa, Latin America, Remote Asia Pacific | 2025-2033 |

Fiber Enclosure Market Opportunities Analysis

The Fiber Enclosure market presents significant opportunities for growth, particularly driven by untapped potential in emerging economies and the continuous advancement of fiber optic technologies. Developing countries across Asia Pacific, Latin America, and Africa are increasingly investing in digital infrastructure to bridge the digital divide and foster economic growth. This push for broadband expansion, often supported by government initiatives and international funding, creates a substantial market for fiber enclosures as these regions build out their foundational networks. Companies that can offer cost-effective, scalable, and robust enclosure solutions tailored to the unique environmental and logistical challenges of these markets are poised for considerable growth. The rapid urbanization in these regions also fuels the demand for FTTx deployments, further expanding the market for various enclosure types.

Another key opportunity lies in the development of advanced materials and smart enclosure technologies. Innovations in lightweight, durable, and corrosion-resistant materials, such as advanced polymers and composites, can enhance the lifespan and performance of enclosures, especially in harsh outdoor environments. Furthermore, the integration of smart features, such as embedded sensors for monitoring temperature, humidity, and intrusion detection, offers value-added solutions that cater to the evolving needs of network operators for enhanced security and predictive maintenance. The growing trend towards miniaturization and higher fiber density within enclosures to optimize space utilization in increasingly congested network environments also represents a fertile ground for product innovation and market penetration. These technological advancements not only improve product offerings but also address specific pain points of network deployment and management.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Markets in Emerging Economies | +2.0% | Asia Pacific (Southeast Asia, India), Africa, Latin America | 2025-2033 |

| Development of Advanced Materials and Smart Enclosures | +1.7% | Global | 2025-2033 |

| Rising Demand for Miniaturized and High-Density Solutions | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Increased Focus on Sustainable and Eco-Friendly Enclosure Solutions | +1.0% | Europe, North America | 2025-2033 |

Fiber Enclosure Market Challenges Impact Analysis

The Fiber Enclosure market faces several notable challenges that can impede its growth trajectory and operational efficiency. One significant challenge pertains to standardization and interoperability across different vendor solutions. The absence of universally adopted standards for fiber enclosure designs, connectors, and cable management systems can lead to compatibility issues, increased complexity during network expansion, and higher integration costs for operators. This fragmentation can limit market adoption, especially for large-scale, multi-vendor deployments, and complicate maintenance procedures. Ensuring seamless integration of diverse enclosure types from various manufacturers remains a critical hurdle for the industry.

Furthermore, environmental resilience and protection against extreme weather conditions pose an ongoing challenge, particularly for outdoor deployments. Fiber enclosures must be designed to withstand a wide range of temperatures, humidity, UV radiation, and physical impacts, which requires advanced material science and rigorous testing. Failures due to environmental degradation can lead to costly network outages and repairs, impacting service reliability. Additionally, supply chain disruptions, as experienced recently with global events, present a considerable challenge. Dependencies on specific raw material suppliers or manufacturing regions can lead to delays, increased costs, and shortages of critical components, affecting the timely delivery of fiber enclosures and impacting project timelines for network rollouts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardization and Interoperability | -1.2% | Global | 2025-2033 |

| Ensuring Environmental Resilience in Harsh Conditions | -0.9% | Global, particularly outdoor deployments | 2025-2033 |

| Supply Chain Volatility and Raw Material Scarcity | -0.8% | Global | 2025-2030 |

| Competition from Wireless Alternatives in Last-Mile Connectivity | -0.5% | Rural areas, specific urban deployments | 2025-2033 |

Fiber Enclosure Market - Updated Report Scope

This market research report provides an in-depth analysis of the Fiber Enclosure market, covering historical trends, current market dynamics, and future growth projections from 2025 to 2033. The scope includes a comprehensive examination of market size, segmentation by various attributes, key growth drivers, formidable restraints, emerging opportunities, and significant challenges impacting the industry. It also features a detailed competitive landscape analysis, profiling leading players and their strategic initiatives to provide a holistic view of the market's structure and potential trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 5.92 Billion |

| Growth Rate | 9.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Corning Inc., CommScope Inc., TE Connectivity, Prysmian Group, Huber+Suhner AG, OFS Fitel LLC, Furukawa Electric Co., Ltd., HellermannTyton, R&M (Reichle & De-Massari AG), 3M Company, AFL Global, Nexans S.A., Optiarc (a Sumitomo Electric Lightwave company), Panduit Corp., Leviton Manufacturing Co., Inc., Belden Inc., Clearfield Inc., Duraline, Hexatronic Group AB, Sterlite Technologies Limited. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Fiber Enclosure market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective contributions to the overall market. This segmentation allows for a nuanced analysis of market dynamics, identifying growth pockets and areas of strategic importance. The market is primarily broken down by type, application, material, and capacity, reflecting the varied requirements of different deployment scenarios and end-user industries.

Analyzing these segments reveals that each category plays a critical role in the broader fiber optic ecosystem. For instance, rack-mount enclosures are crucial for data center environments due to their high-density and structured cabling advantages, while wall-mount and splice enclosures are vital for FTTx and outdoor telecom deployments, offering protection against environmental factors. Material segmentation highlights the shift towards durable and weather-resistant options, essential for long-term network reliability. Capacity segmentation directly correlates with the scale of fiber deployment, from small enterprise networks to large-scale data centers or metropolitan fiber rings.

- By Type: Wall-Mount Enclosures, Rack-Mount Enclosures, Splice Enclosures, Distribution Enclosures, Termination Enclosures, Others.

- By Application: Fiber-to-the-Home (FTTH), Data Centers, Telecommunication Networks, Enterprise Networks, Industrial Applications, Others.

- By Material: Metal, Plastic, Composite.

- By Capacity: Low Density, Medium Density, High Density.

Regional Highlights

- North America: A mature market characterized by significant investments in 5G infrastructure, data center expansion, and enterprise networking. High adoption of advanced fiber technologies and demand for high-density, scalable enclosure solutions. The U.S. and Canada are leading in network upgrades and FTTx deployments.

- Europe: Driven by ambitious digital agenda initiatives and widespread FTTH deployments across various countries. Focus on regulatory compliance, sustainability, and innovative enclosure designs that meet stringent environmental standards. Germany, France, and the UK are key contributors to market growth.

- Asia Pacific (APAC): The fastest-growing region, fueled by massive investments in telecom infrastructure, rapid urbanization, and extensive FTTH/B rollouts in countries like China, India, Japan, and South Korea. Emerging economies are also rapidly expanding their broadband networks, creating substantial demand for all types of fiber enclosures.

- Latin America: Experiencing robust growth in fiber optic infrastructure due to increasing internet penetration and government initiatives aimed at expanding digital connectivity. Brazil and Mexico are leading the adoption of fiber technologies and requiring significant fiber enclosure deployments.

- Middle East and Africa (MEA): Emerging as a significant market with substantial investments in smart city projects, 5G networks, and data center developments, particularly in the UAE, Saudi Arabia, and South Africa. The demand is growing for resilient outdoor enclosures capable of withstanding harsh environmental conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Fiber Enclosure Market.- Corning Inc.

- CommScope Inc.

- TE Connectivity

- Prysmian Group

- Huber+Suhner AG

- OFS Fitel LLC

- Furukawa Electric Co., Ltd.

- HellermannTyton

- R&M (Reichle & De-Massari AG)

- 3M Company

- AFL Global

- Nexans S.A.

- Optiarc (a Sumitomo Electric Lightwave company)

- Panduit Corp.

- Leviton Manufacturing Co., Inc.

- Belden Inc.

- Clearfield Inc.

- Duraline

- Hexatronic Group AB

- Sterlite Technologies Limited

Frequently Asked Questions

What is a fiber enclosure?

A fiber enclosure is a protective housing designed to securely store, organize, and protect fiber optic cable splices, connectors, and passive components from environmental elements and physical damage. They are essential for managing fiber optic networks in various applications.

What are the primary types of fiber enclosures?

Primary types include wall-mount enclosures for indoor or outdoor building connections, rack-mount enclosures for data centers and central offices, splice enclosures for protecting cable splices, distribution enclosures for fiber distribution, and termination enclosures for connecting to active equipment.

Why are fiber enclosures crucial for network infrastructure?

Fiber enclosures are crucial because they ensure the reliability and longevity of fiber optic networks by protecting sensitive connections from dust, moisture, temperature fluctuations, and physical impact. They also facilitate organized cable management, making maintenance, upgrades, and troubleshooting more efficient.

How do 5G and data center growth impact the fiber enclosure market?

5G expansion requires denser fiber backhaul networks and robust outdoor enclosures, while data center growth demands high-density, modular enclosures for efficient cable management within controlled environments. Both trends significantly increase the demand for diverse fiber enclosure solutions.

What technological advancements are shaping fiber enclosure designs?

Technological advancements include the use of advanced durable and lightweight materials, the integration of smart sensors for environmental monitoring, and the development of modular, high-density, and pre-terminated designs to simplify installation and enhance scalability and maintainability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted