Ferrou Scrap Recycling Market

Ferrou Scrap Recycling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707879 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Ferrous Scrap Recycling Market Size

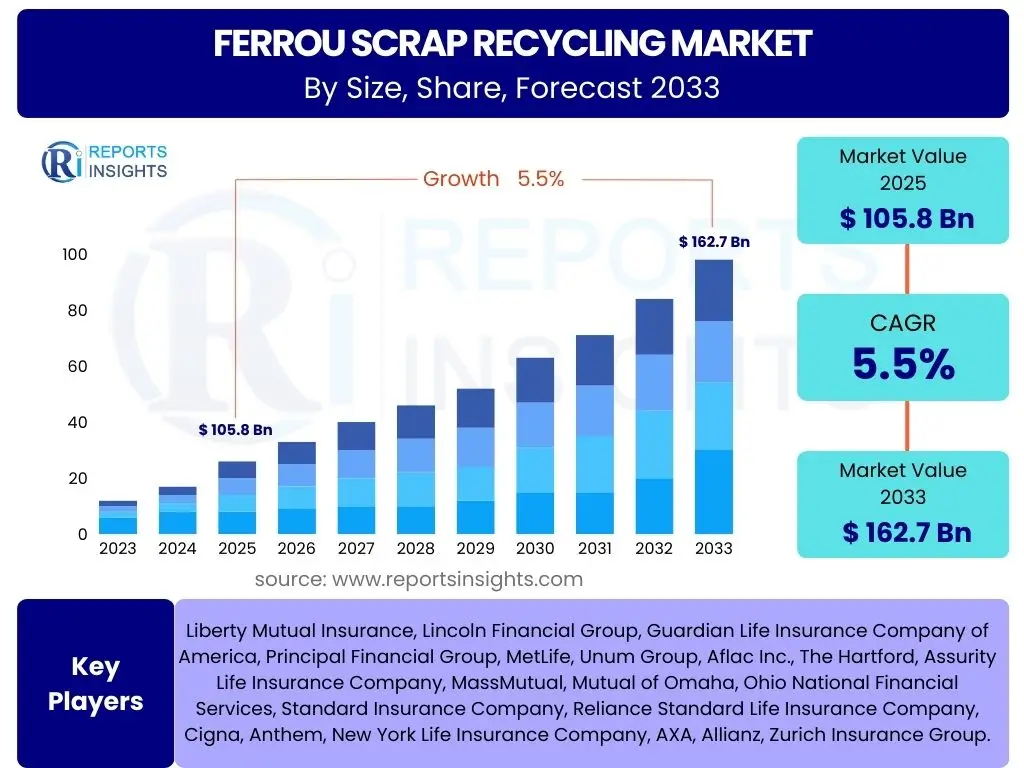

According to Reports Insights Consulting Pvt Ltd, The Ferrous Scrap Recycling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 105.8 billion in 2025 and is projected to reach USD 162.7 billion by the end of the forecast period in 2033.

Key Ferrous Scrap Recycling Market Trends & Insights

Analysis of common user questions reveals a strong interest in understanding the core dynamics shaping the ferrous scrap recycling sector. Users frequently inquire about the shift towards circular economy models, the influence of stricter environmental regulations, and the technological advancements making recycling more efficient. These questions often underscore a desire to grasp how global sustainability goals are translating into tangible market shifts, particularly concerning resource optimization and emission reduction targets within heavy industries like steel production. The emphasis is on identifying trends that promise both environmental benefits and economic viability, signaling a market maturing beyond mere waste management into a strategic component of industrial supply chains.

Further examination of user queries highlights concerns regarding the stability of raw material supply chains, especially in light of increasing geopolitical tensions and trade restrictions. There is a discernible focus on how the market is adapting to fluctuating scrap prices, the impact of varying regional collection rates, and the role of innovation in improving scrap quality and processing. Stakeholders are keen to understand the emergent trends in digitalization, such as the use of advanced analytics for inventory management and predictive maintenance of recycling machinery, which are poised to optimize operations and enhance overall market transparency. This indicates a forward-looking perspective, where efficiency and resilience are paramount considerations for market participants.

Moreover, user interest extends to the long-term implications of these trends, including the potential for new market entrants and the evolution of business models. There is a clear need for insights into how recycling infrastructure is developing across different regions, particularly in emerging economies where industrialization is accelerating. The discussions also touch upon the evolving landscape of end-use applications for recycled ferrous metals, beyond traditional steelmaking, such as in additive manufacturing and specialized alloys. This collective inquiry points to a market undergoing significant transformation, driven by both regulatory push and technological pull, with a strong emphasis on sustainable practices and economic competitiveness.

- Growing emphasis on circular economy principles and sustainable industrial practices globally.

- Increasing adoption of advanced sorting and processing technologies to enhance scrap quality and recovery rates.

- Rising demand for electric arc furnace (EAF) steel production, which primarily utilizes ferrous scrap.

- Stricter environmental regulations and government initiatives promoting recycling and resource efficiency.

- Fluctuations in global commodity prices and their direct impact on scrap market dynamics.

- Integration of digital solutions for optimized supply chain management and inventory tracking.

- Development of innovative applications for recycled ferrous metals beyond traditional steel production.

AI Impact Analysis on Ferrous Scrap Recycling

Common user questions regarding AI's impact on ferrous scrap recycling frequently center on its potential to revolutionize sorting and quality control processes. Stakeholders are keenly interested in how artificial intelligence, particularly machine learning and computer vision, can enhance the identification and segregation of different types of ferrous metals, thereby improving the purity of recycled materials. Queries often explore the accuracy and speed of AI-driven systems compared to traditional methods, as well as the cost implications of integrating such advanced technologies. There is a clear expectation that AI will lead to higher-value scrap products, reduced contamination, and more efficient operational workflows within recycling facilities, addressing long-standing challenges in material differentiation.

Furthermore, users consistently ask about AI's role in optimizing logistics and supply chain management within the ferrous scrap market. Questions revolve around predictive analytics for scrap availability, demand forecasting, and efficient transportation routes, aiming to minimize operational costs and environmental footprint. The potential for AI to streamline complex supply networks, from collection points to processing plants and steel mills, is a significant area of inquiry. This includes understanding how AI algorithms can anticipate market fluctuations, manage inventory levels more effectively, and inform strategic purchasing decisions, indicating a desire for increased market resilience and profitability through data-driven insights.

Additionally, inquiries often extend to the broader implications of AI for workforce development and safety within the recycling industry. Users are curious about the skills required to operate and maintain AI-powered systems, the potential for job displacement, and how AI can contribute to safer working environments by automating hazardous tasks. There is also an interest in the ethical considerations and data privacy aspects associated with deploying AI technologies. These questions reflect a comprehensive perspective on AI's transformative potential, encompassing not only technological advancements but also their societal and operational impacts on the ferrous scrap recycling ecosystem.

- Enhanced material identification and sorting accuracy through AI-powered computer vision and machine learning.

- Optimization of supply chain logistics, including collection, transportation, and inventory management, using predictive analytics.

- Improved quality control and impurity detection, leading to higher-grade recycled ferrous materials.

- Predictive maintenance for recycling machinery, reducing downtime and operational costs.

- Automation of hazardous tasks, increasing safety and efficiency in recycling facilities.

- Data-driven insights for market forecasting, pricing strategies, and strategic decision-making.

- Potential for energy efficiency improvements through optimized processes and resource allocation.

Key Takeaways Ferrous Scrap Recycling Market Size & Forecast

Analysis of common user questions regarding the ferrous scrap recycling market size and forecast consistently highlights an eagerness to understand the underlying drivers of growth and the long-term sustainability of this sector. Users frequently inquire about the primary factors contributing to the projected CAGR, such as the increasing global steel demand, the shift towards more environmentally friendly steel production methods, and the expanding regulatory framework promoting circular economy principles. These questions often seek to validate the market's robust growth trajectory, emphasizing its critical role in reducing reliance on virgin resources and mitigating environmental impact. The focus is on confirming that the observed growth is sustained by fundamental economic and environmental shifts rather than transient factors.

Furthermore, stakeholders are keen to grasp the specific segments and regions that are expected to drive the majority of this growth. Queries often probe into which types of ferrous scrap (e.g., obsolete, prompt industrial, or shredded scrap) will see the most significant demand, and which geographical areas (e.g., Asia Pacific, Europe, or North America) are poised for the most substantial expansion. There is a strong interest in understanding the contributing market share of key regions and the factors that differentiate their growth profiles, such as industrialization rates, regulatory stringency, and existing recycling infrastructure. This granular perspective helps in identifying strategic investment opportunities and understanding competitive landscapes.

Moreover, user inquiries frequently address potential challenges or risks that could impact the forecast, such as volatile commodity prices, geopolitical instability, or technological disruptions. There is a clear desire to obtain a balanced view of the market's prospects, considering both opportunities and potential headwinds. Questions often touch upon the impact of innovative technologies on processing costs and efficiency, and how these might alter the market's long-term structure. The overarching theme of these questions is to secure a comprehensive understanding of the market's future, enabling informed decision-making for investors, policymakers, and industry participants alike, ensuring resilience in the face of evolving market dynamics.

- The market is poised for significant growth, driven by increasing global steel production and demand for sustainable materials.

- Strong regulatory support and environmental mandates worldwide are accelerating the adoption of ferrous scrap recycling.

- Technological advancements in sorting, processing, and quality control are improving the economic viability of recycling operations.

- The shift towards Electric Arc Furnace (EAF) steelmaking significantly boosts demand for ferrous scrap as a primary input.

- Asia Pacific is anticipated to remain a dominant region, with robust industrial growth and increasing infrastructure development.

- Volatile raw material prices and geopolitical factors continue to influence market stability and investment decisions.

Ferrous Scrap Recycling Market Drivers Analysis

The ferrous scrap recycling market is significantly propelled by a confluence of economic, environmental, and technological factors that underscore its increasing importance in the global industrial landscape. A primary driver is the accelerating shift towards sustainable manufacturing practices across industries, particularly in steel production. As environmental concerns gain prominence and regulatory bodies impose stricter emission standards, steelmakers are increasingly turning to ferrous scrap as a key input for Electric Arc Furnaces (EAFs), which offer a lower carbon footprint compared to traditional blast furnaces. This growing preference for EAF-based production, driven by its energy efficiency and reduced greenhouse gas emissions, directly amplifies the demand for high-quality ferrous scrap, making it an indispensable component of modern steelmaking.

Furthermore, the escalating global demand for steel, fueled by rapid urbanization, infrastructure development, and industrial expansion in emerging economies, acts as a significant market driver. While virgin iron ore remains crucial, the finite nature of natural resources and the energy-intensive process of extracting and processing them make recycled steel an economically attractive and environmentally responsible alternative. Governments worldwide are also implementing policies and incentives that promote recycling and circular economy models, thereby creating a supportive regulatory environment for the ferrous scrap market. These legislative measures often include mandates for recycled content in products, waste diversion targets, and financial incentives for recycling operations, which collectively stimulate market growth and investment in recycling infrastructure.

Technological advancements in scrap processing, such as enhanced sorting capabilities, metal recovery techniques, and quality control systems, further contribute to market expansion. Innovations in shredding, baling, and magnetic separation technologies enable recyclers to produce higher-grade ferrous scrap, which is more appealing to steel manufacturers. These advancements not only improve efficiency and reduce operational costs but also expand the range of materials that can be effectively recycled, thereby increasing the overall supply of usable scrap. The synergy between robust demand from steel industries, supportive environmental policies, and continuous technological innovation collectively positions the ferrous scrap recycling market for sustained growth, reinforcing its vital role in achieving global sustainability objectives.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Steel & EAF Production | +1.5% | Global, particularly Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Growing Environmental Regulations & Sustainability Goals | +1.2% | Europe, North America, China, India | Medium to Long-term (2025-2033) |

| Resource Scarcity & Cost-Effectiveness of Recycling | +0.8% | Global | Long-term (2025-2033) |

| Technological Advancements in Scrap Processing | +0.7% | Developed Economies (EU, US, Japan) | Medium-term (2025-2030) |

| Urbanization & Infrastructure Development | +0.5% | Emerging Economies (China, India, Southeast Asia) | Long-term (2025-2033) |

Ferrous Scrap Recycling Market Restraints Analysis

Despite its significant growth potential, the ferrous scrap recycling market faces several notable restraints that can impede its expansion and efficiency. One primary restraint is the volatility of scrap metal prices, which are intrinsically linked to global commodity markets, industrial production rates, and economic cycles. Fluctuations in these prices can create uncertainty for recyclers and steelmakers alike, impacting profitability, investment decisions, and long-term planning. When scrap prices are low, collection and processing become less economically viable, potentially leading to reduced supply, while high prices can strain the budgets of steel producers. This inherent price instability makes it challenging for market participants to maintain consistent operational margins and can deter new investments in recycling infrastructure, thereby limiting overall market growth.

Another significant restraint is the presence of varying quality and contamination levels in collected ferrous scrap. The effectiveness of recycling heavily depends on the purity of the incoming material. Contaminants such as non-ferrous metals, plastics, rubber, or hazardous substances necessitate extensive and costly sorting and processing efforts. Inadequate sorting can lead to lower-grade recycled products, which may fetch lower prices or require further refinement, thereby increasing operational expenses. The lack of standardized collection and sorting practices across different regions and sources contributes to this challenge, making it difficult to achieve consistent high-quality output and fully capitalize on the value of recycled materials. This issue is particularly pronounced in regions with less developed recycling infrastructure.

Furthermore, regulatory complexities and inconsistencies across different jurisdictions pose a considerable restraint. While many governments advocate for recycling, the specific regulations regarding waste collection, transportation of hazardous materials, environmental compliance, and trade barriers can vary significantly. These discrepancies can create logistical hurdles, increase administrative burdens, and raise compliance costs for businesses operating across borders or in multiple regions. Additionally, stringent environmental permits and licensing requirements can delay the establishment or expansion of recycling facilities. The presence of illegal scrap trading and a lack of robust enforcement in some areas can also undermine legitimate recycling efforts, contributing to market inefficiencies and making it harder for compliant businesses to compete effectively, thereby slowing the market's organic growth potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Scrap Metal Prices | -1.0% | Global | Short to Medium-term (2025-2030) |

| Varying Quality & Contamination Levels | -0.8% | Emerging Economies, Developing Regions | Long-term (2025-2033) |

| Logistical Challenges & Inadequate Infrastructure | -0.6% | Developing Regions, Remote Areas | Medium to Long-term (2025-2033) |

| High Capital Investment for Advanced Processing | -0.5% | Global | Long-term (2025-2033) |

| Trade Barriers & Geopolitical Influences | -0.4% | Specific Trade Blocs, Geopolitically Sensitive Regions | Short-term (2025-2027) |

Ferrous Scrap Recycling Market Opportunities Analysis

The ferrous scrap recycling market is replete with significant opportunities driven by global sustainability mandates and the ongoing transformation of industrial processes. A key opportunity lies in the expanding adoption of Electric Arc Furnace (EAF) technology in steelmaking, which relies almost exclusively on scrap metal as its primary raw material. As countries worldwide commit to decarbonization and reducing their carbon footprint, steel producers are increasingly investing in EAFs over traditional blast furnaces, creating a robust and growing demand for high-quality ferrous scrap. This fundamental shift presents a sustained opportunity for recyclers to supply a critical, environmentally preferred input to a major global industry, fostering long-term market stability and growth.

Furthermore, the development and implementation of advanced recycling technologies offer substantial opportunities for enhanced efficiency and value creation. Innovations in automated sorting systems, such as those utilizing artificial intelligence (AI), machine learning, and sensor-based technologies, enable more precise segregation of different ferrous grades and removal of contaminants. This leads to higher purity scrap, which commands premium prices and expands the range of end-use applications. Investment in these cutting-edge technologies not only improves operational efficiency and reduces processing costs but also allows recyclers to tap into higher-value market segments by providing customized scrap blends tailored to specific steelmaking requirements. The continuous evolution of these technologies ensures a competitive edge and opens new avenues for profitability.

Another compelling opportunity arises from the expanding regulatory frameworks and public pressure for a circular economy. Governments are increasingly implementing policies that mandate higher recycling rates, promote the use of recycled content in manufacturing, and offer incentives for sustainable waste management. These policies create a favorable environment for the growth of the ferrous scrap recycling industry by ensuring a consistent supply of scrap material and a reliable market for recycled products. Additionally, growing consumer awareness and corporate social responsibility initiatives are driving demand for products made from recycled materials, further incentivizing businesses to integrate recycled ferrous metals into their supply chains. This strong regulatory and societal push reinforces the long-term viability and growth prospects of the market, opening doors for strategic partnerships and innovative business models focused on resource recovery.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Shift to EAF Steel Production | +1.8% | Global, especially North America, Europe, China | Long-term (2025-2033) |

| Technological Advancements in Sorting & Processing | +1.5% | Developed Economies, Technologically Advanced Regions | Medium to Long-term (2025-2033) |

| Emergence of Circular Economy Mandates & ESG Focus | +1.3% | Europe, North America, Japan, Australia | Long-term (2025-2033) |

| Expansion in Emerging Markets' Industrial & Urban Development | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Development of New Applications for Recycled Steel | +0.7% | Global | Long-term (2028-2033) |

Ferrous Scrap Recycling Market Challenges Impact Analysis

The ferrous scrap recycling market, while robust, faces several significant challenges that can impede its growth and operational efficiency. One of the primary challenges is the inconsistent global supply and demand dynamics for ferrous scrap. This inconsistency is often a direct result of fluctuating industrial activity, varying economic conditions across regions, and unpredictable geopolitical events that can disrupt trade flows. When industrial output slows down, the generation of prompt industrial scrap decreases, impacting supply. Conversely, high demand coupled with restricted supply can lead to price spikes, making recycled steel less competitive against virgin materials. These unpredictable supply-demand imbalances create operational hurdles for recyclers and steelmakers, making long-term planning difficult and potentially affecting profitability margins across the value chain, thereby hindering steady market growth.

Another substantial challenge lies in the complex logistics and high transportation costs associated with moving bulky and heavy ferrous scrap. Scrap materials are often generated in diverse locations and need to be collected, transported to processing facilities, and then shipped to steel mills. The sheer volume and weight of ferrous scrap make transportation particularly energy-intensive and expensive, especially over long distances. Infrastructure limitations in certain regions, such as inadequate rail networks or port capacities, further exacerbate these logistical complexities. These challenges can significantly add to the overall cost of recycled steel, potentially eroding its cost advantage over virgin materials and limiting market reach, particularly in landlocked regions or areas with underdeveloped transportation systems.

Furthermore, the ongoing need for significant capital investment in advanced processing technologies and infrastructure represents a considerable hurdle for many market participants, especially smaller and medium-sized enterprises. To meet the rising demand for higher-quality scrap and to comply with stricter environmental standards, recyclers must invest in sophisticated sorting equipment, shredders, balers, and environmental control systems. These investments often require substantial upfront capital, which can be a barrier to entry for new players and a challenge for existing ones seeking to upgrade their facilities. Without continuous investment in modernization, the industry risks falling behind in efficiency and quality, thereby impacting its ability to capitalize on market opportunities and compete effectively. This financial constraint can slow down technological adoption and limit the overall expansion capacity of the recycling sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply-Demand Imbalances & Trade Policies | -0.9% | Global | Short to Medium-term (2025-2030) |

| High Transportation & Logistics Costs | -0.7% | Global, particularly regions with poor infrastructure | Long-term (2025-2033) |

| Technological Obsolescence & Investment Requirements | -0.6% | Developing Regions | Medium to Long-term (2025-2033) |

| Environmental Compliance & Permitting Hurdles | -0.5% | Developed Economies (EU, US) | Long-term (2025-2033) |

| Competition from Virgin Material Production | -0.4% | Global | Long-term (2025-2033) |

Ferrous Scrap Recycling Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global ferrous scrap recycling market, offering critical insights into its current landscape, future projections, and the dynamic forces shaping its trajectory. The scope covers a thorough examination of market size, growth drivers, restraints, opportunities, and challenges across key segments and major geographical regions. It delves into technological advancements, regulatory frameworks, and sustainability trends influencing market evolution, providing a robust foundation for strategic decision-making and investment planning within the circular economy. The analysis is meticulously structured to address the complex interplay of economic, environmental, and technological factors that define this vital industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 105.8 billion |

| Market Forecast in 2033 | USD 162.7 billion |

| Growth Rate | 5.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nucor Corporation, Schnitzer Steel Industries, Sims Metal Management, European Metal Recycling (EMR), CMC Recycling, Commercial Metals Company, Gerdau S.A., Steel Dynamics, Inc., Metalico Inc., OmniSource Corporation, Triple M Metal, SA Recycling, Ferrous Processing & Trading Company, Hugo Neu Corporation, Upstate Shredding, Industrial Services of America, Inc., Alter Trading Corporation, TSR Recycling GmbH & Co. KG, Chiho Environmental Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ferrous scrap recycling market is comprehensively segmented to provide a detailed understanding of its diverse components and the distinct dynamics that characterize each. This segmentation allows for a granular analysis of how various types of scrap are processed and utilized across different end-use industries, offering crucial insights into market demand and supply patterns. Understanding these segments is vital for stakeholders to identify specific growth opportunities, optimize operational strategies, and tailor product offerings to meet the unique requirements of various consumers. The differentiation by scrap type, end-use, source, and processing technology reflects the intricate ecosystem of the ferrous recycling value chain, highlighting specialized niches and broad market trends.

The segmentation by scrap type, for instance, distinguishes between new (prompt industrial) scrap, which is generated during manufacturing processes, and old (obsolete) scrap, derived from end-of-life products like automobiles and demolished structures. Further distinctions are made for categories like shredded scrap, heavy melting steel (HMS), and cast iron, each possessing unique characteristics and commanding different market values based on purity and composition. These distinctions are critical for both recyclers, who must efficiently sort and process these materials, and steelmakers, who specify particular scrap grades for their production processes. The varying availability and quality of these scrap types significantly influence regional market dynamics and global trade flows, making this segmentation essential for comprehensive market analysis.

Moreover, segmenting the market by end-use industry, such as Electric Arc Furnace (EAF) and Basic Oxygen Furnace (BOF) steel mills, as well as foundries, reveals the specific demand drivers and quality requirements for recycled ferrous metals. Each end-use sector has distinct technical specifications for scrap inputs, influencing processing techniques and market pricing. Similarly, segmentation by source (e.g., manufacturing waste, demolition & construction, automotive) provides insights into where scrap is generated and how efficiently it can be collected. Lastly, analyzing the market by processing technology, including shredding, baling, shearing, and advanced sensor-based sorting, helps to understand the technological landscape, investment trends, and the efficiency gains achieved in the recycling process. This multi-faceted segmentation framework offers a holistic view of the market, essential for strategic planning and informed decision-making.

- By Scrap Type:

- New (Prompt Industrial) Scrap

- Old (Obsolete) Scrap

- Shredded Scrap

- Heavy Melting Steel (HMS)

- Plate and Structural (P&S)

- Turnings

- Cast Iron

- By End-Use Industry:

- Steel Mills (EAF, BOF)

- Foundries

- Others (e.g., Fabrication, Automotive)

- By Source:

- Manufacturing Waste

- Demolition & Construction

- Automotive

- Consumer Durables

- Machinery

- Others

- By Processing Technology:

- Shredding

- Baling

- Shearing

- Magnetic Separation

- Sensor-based Sorting

- Other Advanced Technologies

Regional Highlights

The global ferrous scrap recycling market exhibits significant regional variations, influenced by differing levels of industrialization, regulatory landscapes, and existing recycling infrastructure. Asia Pacific, for instance, stands as the largest and fastest-growing market, primarily driven by rapid economic expansion, massive urbanization, and extensive infrastructure development in countries like China, India, and Southeast Asian nations. These countries are experiencing booming steel demand, coupled with increasing governmental pressure to adopt sustainable practices, thus creating a robust market for ferrous scrap. The region's sheer volume of industrial and post-consumer waste, combined with growing investments in recycling technologies, underpins its dominant position and future growth potential.

Europe and North America represent mature markets characterized by well-established recycling infrastructures, stringent environmental regulations, and a strong emphasis on circular economy principles. In Europe, policies such as the EU's Circular Economy Action Plan actively promote resource recovery and high recycling targets, stimulating consistent demand for ferrous scrap. Similarly, North America benefits from a highly developed collection network and a significant installed base of Electric Arc Furnaces (EAFs), which are major consumers of scrap. These regions are also at the forefront of adopting advanced sorting and processing technologies, driving efficiency and quality improvements in the recycled material output. Their stable regulatory environments and technological leadership ensure their continued relevance in the global market.

Latin America, the Middle East, and Africa (MEA) are emerging markets with considerable untapped potential. These regions are seeing increasing industrialization and infrastructure projects, which are beginning to generate a growing stream of ferrous scrap. While recycling infrastructure may be less developed compared to mature markets, there is a rising awareness of environmental benefits and economic opportunities associated with ferrous scrap recycling. Investments in new steel mills, often EAF-based, are gradually increasing demand, and governments are exploring policies to improve waste management and resource efficiency. These regions are expected to experience accelerated growth as their industrial bases mature and recycling practices become more formalized and economically viable, contributing increasingly to the global ferrous scrap supply chain.

- Asia Pacific: Dominant market due to rapid industrialization, urbanization, infrastructure development (China, India, Southeast Asia), and increasing steel demand, coupled with emerging environmental regulations.

- Europe: Mature market with strong regulatory support for circular economy, high recycling rates, advanced processing technologies, and significant EAF capacity.

- North America: Well-established recycling infrastructure, high scrap generation from automotive and construction sectors, substantial EAF steel production, and emphasis on sustainable manufacturing.

- Latin America: Emerging market with increasing industrial output and infrastructure growth (Brazil, Mexico), leading to rising scrap generation and demand, though infrastructure development is still evolving.

- Middle East & Africa (MEA): Nascent market with growing industrialization and construction activities (GCC countries, South Africa), increasing focus on diversifying economies, and developing recycling capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ferrous Scrap Recycling Market.- ArcelorMittal

- Nucor Corporation

- Schnitzer Steel Industries

- Sims Metal Management

- European Metal Recycling (EMR)

- CMC Recycling

- Commercial Metals Company

- Gerdau S.A.

- Steel Dynamics, Inc.

- Metalico Inc.

- OmniSource Corporation

- Triple M Metal

- SA Recycling

- Ferrous Processing & Trading Company

- Hugo Neu Corporation

- Upstate Shredding

- Industrial Services of America, Inc.

- Alter Trading Corporation

- TSR Recycling GmbH & Co. KG

- Chiho Environmental Group

Frequently Asked Questions

What is ferrous scrap recycling?

Ferrous scrap recycling is the process of recovering and reprocessing discarded iron and steel materials to produce new steel and iron products. This process significantly reduces the need for virgin raw materials, conserves energy, and lowers greenhouse gas emissions compared to producing steel from iron ore.

Why is ferrous scrap recycling important?

Ferrous scrap recycling is crucial for environmental sustainability and resource conservation. It reduces landfill waste, saves energy (up to 75% less energy than making steel from scratch), decreases air and water pollution, and lowers the demand for mining new iron ore, thereby preserving natural resources.

What drives the demand for ferrous scrap?

The demand for ferrous scrap is primarily driven by the global steel industry, especially the increasing adoption of Electric Arc Furnace (EAF) technology, which uses scrap as its main input. Additionally, stricter environmental regulations, the push for a circular economy, and the cost-effectiveness of recycled steel compared to virgin materials also fuel demand.

What are the main types of ferrous scrap?

The main types of ferrous scrap include new (prompt industrial) scrap generated during manufacturing, old (obsolete) scrap from end-of-life products like cars and appliances, shredded scrap, heavy melting steel (HMS), plate and structural (P&S), turnings, and cast iron. Each type has specific applications and market values.

What are the challenges in the ferrous scrap recycling market?

Key challenges include volatile scrap metal prices, varying quality and contamination levels in collected scrap, high transportation and logistics costs, the need for significant capital investment in advanced processing technologies, and the impact of global supply-demand imbalances and trade policies. Overcoming these challenges is crucial for sustained market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted