Ferronickel Market

Ferronickel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702996 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

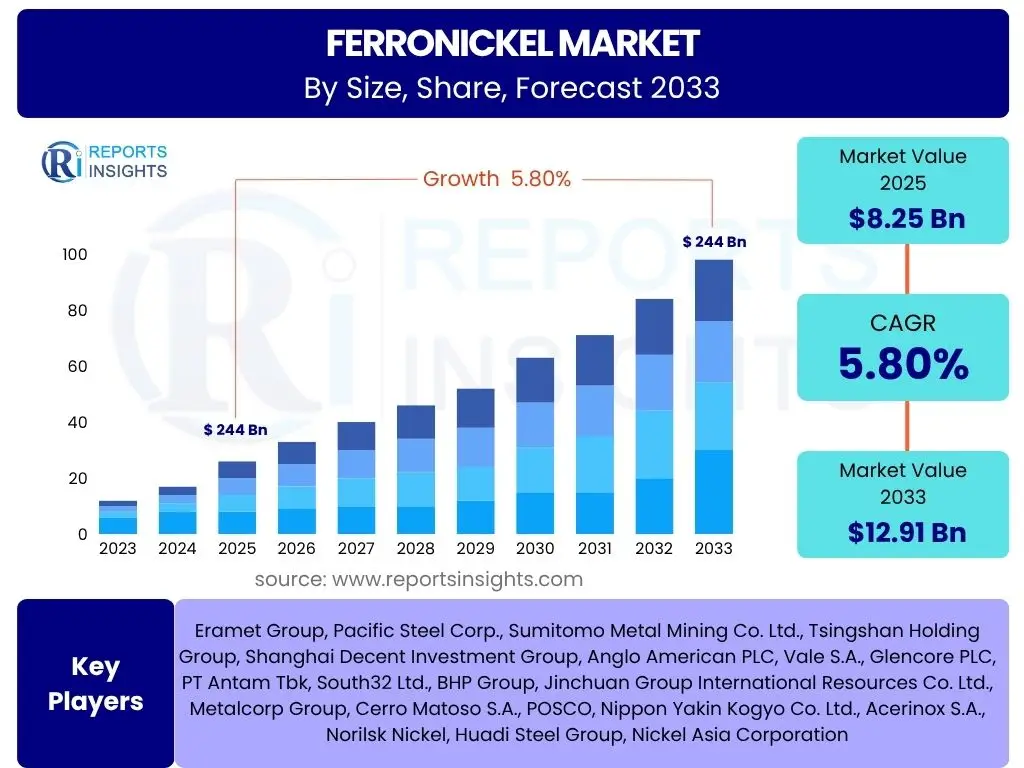

Ferronickel Market Size

According to Reports Insights Consulting Pvt Ltd, The Ferronickel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 8.25 Billion in 2025 and is projected to reach USD 12.91 Billion by the end of the forecast period in 2033.

Key Ferronickel Market Trends & Insights

The Ferronickel market is currently shaped by a confluence of factors, primarily the robust and expanding demand for stainless steel, which consumes the vast majority of ferronickel production. Emerging trends indicate a growing emphasis on more sustainable and energy-efficient production processes, driven by stricter environmental regulations and rising energy costs. Furthermore, technological advancements in smelting and refining processes are enabling producers to optimize output and reduce waste, contributing to both operational efficiency and environmental compliance. The market is also seeing shifts in geographical production and consumption patterns, with Asia Pacific, particularly China and Indonesia, playing an increasingly dominant role in both supply and demand.

Another significant trend is the increasing vertical integration within the industry, where mining companies are investing in smelting and refining capabilities to control the entire value chain, thereby enhancing supply security and profitability. The focus on high-purity ferronickel is also intensifying as advanced stainless steel grades and specialized alloys demand superior material properties. This trend is pushing producers to innovate and adopt advanced purification techniques. Moreover, the long-term outlook for ferronickel is bolstered by global urbanization and infrastructure development, which consistently drive demand for construction materials and consumer goods incorporating stainless steel.

- Persistent high demand from the stainless steel industry, particularly in Asia Pacific.

- Increased focus on sustainable and energy-efficient production methods.

- Technological advancements in smelting and refining for enhanced purity and yield.

- Growing vertical integration among key market players to secure supply chains.

- Shifting geographical dominance in production, with Southeast Asian nations gaining prominence.

AI Impact Analysis on Ferronickel

The integration of Artificial Intelligence (AI) into the Ferronickel industry is poised to revolutionize various aspects of its operations, from raw material sourcing to final product distribution. Users frequently inquire about AI's potential to optimize operational efficiency, enhance predictive maintenance, and improve decision-making processes within the capital-intensive and energy-demanding ferronickel production cycle. Concerns often revolve around the initial investment required for AI infrastructure, data security, and the need for a skilled workforce capable of managing these advanced systems. However, the overarching expectation is that AI will unlock new levels of productivity and sustainability.

AI's influence is expected to extend into areas such as geological exploration for nickel ore, where machine learning algorithms can analyze vast datasets to identify promising deposits more efficiently. In the smelting and refining phases, AI can optimize furnace operations, predict equipment failures, and fine-tune chemical processes to improve yield and reduce energy consumption. Furthermore, AI-powered supply chain management can enhance logistics, predict demand fluctuations, and optimize inventory levels, leading to reduced operational costs and increased responsiveness to market changes. The technology's ability to process and interpret complex data sets will be crucial for navigating the volatile commodity market and making informed strategic decisions.

- Optimized resource utilization and energy consumption in smelting operations through AI algorithms.

- Enhanced predictive maintenance of heavy machinery, reducing downtime and operational costs.

- Improved quality control and consistency of ferronickel through real-time data analysis.

- AI-driven supply chain management for better logistics, inventory, and demand forecasting.

- Advanced data analytics for market trend prediction and strategic decision-making.

Key Takeaways Ferronickel Market Size & Forecast

Key insights from the Ferronickel market size and forecast indicate a stable, albeit moderately growing, market primarily propelled by global stainless steel production. The consistent expansion of urban infrastructure, automotive industries, and consumer goods sectors, which are significant consumers of stainless steel, underpins this growth. The forecast highlights the resilience of the market even amidst geopolitical and economic uncertainties, largely due to the indispensable nature of ferronickel in its primary application.

Furthermore, the long-term outlook suggests a strategic shift towards more responsible sourcing and environmentally compliant production. Future growth will likely be influenced by innovations in recycling technologies for nickel-containing materials, reducing reliance on primary ore extraction. The market's trajectory will also be shaped by the ability of producers to adapt to evolving environmental regulations and fluctuating energy prices, which directly impact production costs and profitability. Overall, the market remains robust, with continued demand for its foundational role in modern industrial applications.

- Robust demand from the stainless steel industry remains the primary growth driver.

- Market stability is supported by consistent global infrastructure and manufacturing growth.

- Increasing emphasis on sustainable production and recycling initiatives will influence future supply dynamics.

- Technological advancements in extraction and processing are key to cost efficiency and market competitiveness.

- Asia Pacific continues to dominate both production and consumption, driving regional market expansion.

Ferronickel Market Drivers Analysis

The Ferronickel market is significantly driven by the expanding global demand for stainless steel, which represents the largest end-use application for ferronickel. Stainless steel, known for its corrosion resistance, durability, and aesthetic appeal, finds widespread use in various industries including construction, automotive, consumer goods, and industrial machinery. As global urbanization rates increase and infrastructure projects proliferate, the demand for stainless steel products continues to escalate, directly translating into higher demand for ferronickel.

Beyond stainless steel, the increasing adoption of nickel-containing alloys in specialized applications such as aerospace, chemical processing, and power generation also contributes to market growth. These industries require materials with superior properties like high-temperature resistance and enhanced strength, for which ferronickel serves as a crucial component. Additionally, technological advancements in steel manufacturing processes that favor the use of ferronickel over pure nickel in certain applications, due to cost-effectiveness and ease of alloying, further bolster its market position. The overall economic development and industrialization in emerging economies also play a pivotal role in driving consumption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Stainless Steel Demand | +1.5% | Global, particularly APAC | Long-term |

| Urbanization & Infrastructure Development | +1.2% | Asia Pacific, Latin America, Africa | Mid-to-Long-term |

| Increasing Use in Specialized Alloys | +0.8% | North America, Europe, APAC | Mid-term |

| Cost-Effectiveness over Pure Nickel in Certain Applications | +0.7% | Global | Short-to-Mid-term |

| Industrialization in Emerging Economies | +0.9% | China, India, Southeast Asia | Long-term |

Ferronickel Market Restraints Analysis

The Ferronickel market faces several significant restraints that could impede its growth trajectory. One of the primary concerns is the volatility in nickel prices, which are influenced by global supply-demand dynamics, geopolitical events, and speculative trading. Erratic price fluctuations can create uncertainty for producers and consumers, affecting investment decisions and profitability. High energy costs, particularly for power-intensive smelting operations, pose another substantial challenge. The energy component accounts for a significant portion of ferronickel production costs, and rising energy prices directly impact the competitiveness and margins of producers.

Environmental regulations, especially concerning emissions and waste management, are becoming increasingly stringent globally. Ferronickel production, particularly from lateritic ores, can be energy-intensive and generate considerable environmental by-products. Compliance with these regulations often requires substantial capital investment in new technologies and processes, which can increase production costs and potentially constrain output for some producers. Furthermore, the availability and quality of nickel ore resources can also act as a restraint. Depleting high-grade ore reserves necessitate the processing of lower-grade ores, which is generally more expensive and energy-intensive, adding to operational complexities.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Nickel Price Volatility | -1.0% | Global | Short-to-Mid-term |

| High Energy Costs & Fluctuations | -0.8% | Europe, Asia Pacific | Mid-term |

| Stringent Environmental Regulations | -0.7% | Europe, North America, China | Long-term |

| Availability of High-Grade Nickel Ore | -0.5% | Global (Specific Mining Regions) | Long-term |

| Trade Barriers and Tariffs | -0.4% | Specific Bilateral/Regional | Short-term |

Ferronickel Market Opportunities Analysis

Despite the challenges, the Ferronickel market is ripe with opportunities for growth and innovation. One significant area is the increasing focus on the circular economy and recycling of nickel-containing materials, particularly stainless steel scrap. As primary nickel extraction becomes more costly and environmentally scrutinized, the development of efficient and economical recycling technologies for ferronickel and stainless steel can provide a sustainable and cost-effective source of raw materials. This also aligns with global sustainability goals and reduces the environmental footprint of the industry.

Another key opportunity lies in technological advancements within the smelting and refining processes. Innovations such as enhanced rotary kiln-electric furnace (RKEF) technology, new pyrometallurgical techniques, and hydrometallurgical approaches can improve energy efficiency, reduce emissions, and increase the recovery rate of nickel from lower-grade ores. Investment in these advanced technologies can lead to significant cost savings and improved operational performance. Furthermore, the expansion of stainless steel production capacity in emerging markets, driven by rapid industrialization and infrastructure development, presents a continuous demand base for ferronickel, offering long-term growth prospects for producers willing to invest in these regions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Recycling of Nickel-containing Scrap | +0.9% | Global, particularly Europe | Long-term |

| Technological Advancements in Production Processes | +1.1% | Global (for producers) | Mid-to-Long-term |

| Expansion of Stainless Steel Production in Emerging Markets | +1.3% | Asia Pacific, Southeast Asia | Long-term |

| Development of Niche Applications for Ferronickel | +0.6% | Global | Mid-term |

| Strategic Partnerships & Mergers | +0.5% | Global | Short-to-Mid-term |

Ferronickel Market Challenges Impact Analysis

The Ferronickel market faces several critical challenges that require strategic responses from industry players. One significant challenge is the increasing scrutiny over the environmental impact of mining and smelting operations, particularly concerning carbon emissions and waste disposal. Stringent emission norms and growing public environmental awareness necessitate substantial investments in cleaner technologies and sustainable practices, adding to operational complexities and costs. Non-compliance can lead to hefty fines, operational shutdowns, and reputational damage.

Another major challenge is the volatility of global commodity prices, including not just nickel itself but also key inputs like coke, coal, and electricity. These fluctuations can severely impact the profitability and financial stability of ferronickel producers, making long-term planning difficult. Geopolitical tensions and trade disputes also pose a significant risk, potentially disrupting supply chains, imposing tariffs, or restricting access to key markets and raw materials. Furthermore, the growing competition from alternative nickel sources, such as nickel pig iron (NPI) and battery-grade nickel, especially with the surge in electric vehicle demand, could divert investment and resources away from traditional ferronickel production for stainless steel, although the direct substitutability varies by application.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Environmental & Emission Regulations | -1.2% | Global, especially Europe & China | Long-term |

| Volatility of Input Costs (Energy, Coke) | -0.9% | Global | Short-to-Mid-term |

| Geopolitical Risks & Trade Disputes | -0.8% | Global (specific regions affected) | Short-to-Mid-term |

| Competition from Alternative Nickel Sources (e.g., NPI, Class 1 Nickel) | -0.7% | Global | Mid-to-Long-term |

| Supply Chain Disruptions | -0.6% | Global | Short-term |

Ferronickel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Ferronickel market, segmenting it by various types, applications, and regional landscapes. The report offers a detailed historical analysis from 2019 to 2023, coupled with robust market estimations for 2025 and projections up to 2033, enabling stakeholders to understand past trends and anticipate future growth. It covers critical market dynamics including drivers, restraints, opportunities, and challenges, providing a holistic view of the market's evolving landscape and strategic insights for informed decision-making across the value chain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.25 Billion |

| Market Forecast in 2033 | USD 12.91 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Eramet Group, Pacific Steel Corp., Sumitomo Metal Mining Co. Ltd., Tsingshan Holding Group, Shanghai Decent Investment Group, Anglo American PLC, Vale S.A., Glencore PLC, PT Antam Tbk, South32 Ltd., BHP Group, Jinchuan Group International Resources Co. Ltd., Metalcorp Group, Cerro Matoso S.A., POSCO, Nippon Yakin Kogyo Co. Ltd., Acerinox S.A., Norilsk Nickel, Huadi Steel Group, Nickel Asia Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ferronickel market is extensively segmented to provide granular insights into its diverse components and their respective contributions to the overall market dynamics. This segmentation facilitates a deeper understanding of specific market niches, demand patterns, and regional variances, enabling stakeholders to identify precise growth opportunities and formulate targeted strategies. The primary segmentation categories include product type, application, and end-use industry, each revealing distinct market behaviors and growth drivers.

Analyzing these segments allows for a comprehensive assessment of which ferronickel grades are most in demand, where it is predominantly utilized, and which industrial sectors are driving its consumption. This detailed breakdown highlights the critical role of high-carbon ferronickel in the majority of stainless steel production, while low-carbon variants cater to more specialized alloy and foundry applications requiring higher purity. The end-use industry segmentation further clarifies the diverse economic sectors that rely on ferronickel-containing materials, ranging from heavy industrial machinery to everyday consumer goods, underscoring its foundational importance in the modern economy.

- By Type:

- High-Carbon Ferronickel (HCFN)

- Low-Carbon Ferronickel (LCFN)

- By Application:

- Stainless Steel Production

- Alloy Manufacturing

- Foundries

- Other Industrial Applications

- By End-Use Industry:

- Construction

- Automotive

- Industrial Machinery

- Consumer Goods

- Others

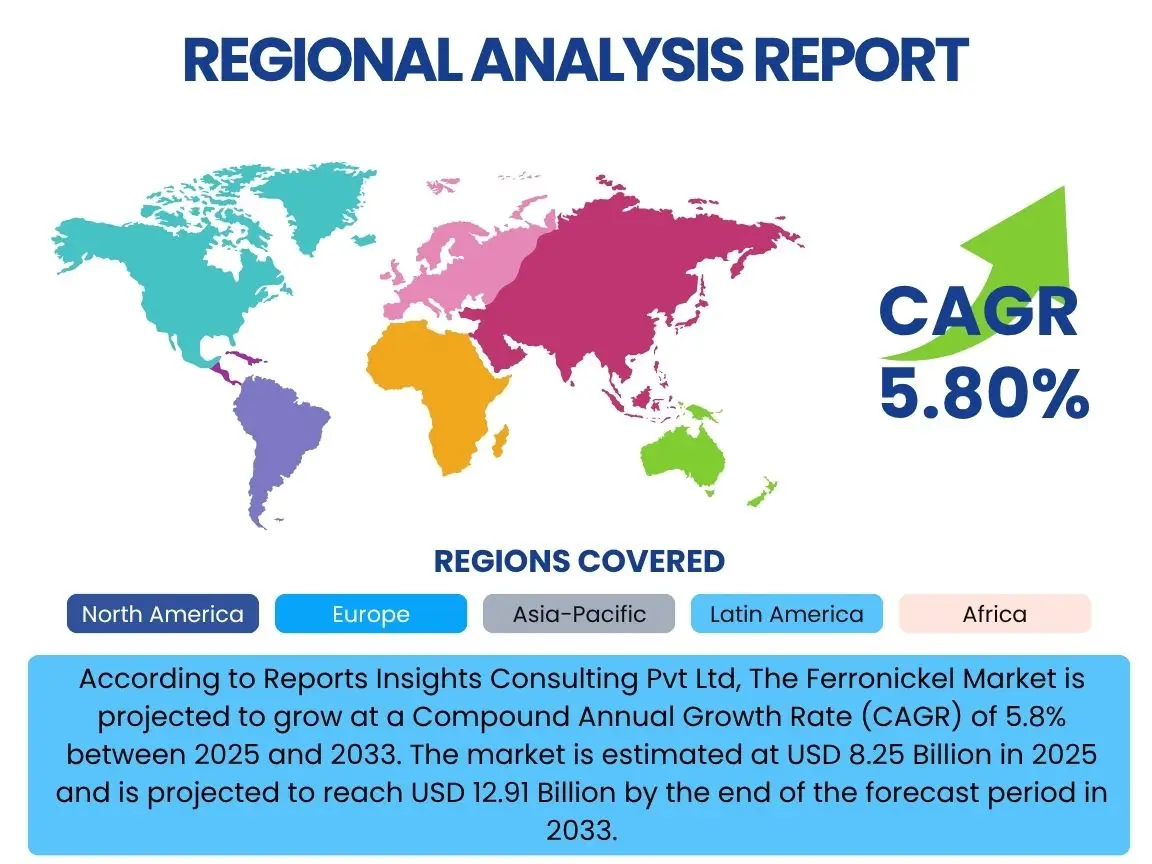

Regional Highlights

- Asia Pacific (APAC): Dominates the global Ferronickel market, driven by massive stainless steel production capabilities, particularly in China, India, and Indonesia. These countries benefit from abundant nickel ore reserves, lower production costs, and rapidly expanding industrial and construction sectors. Indonesia, in particular, has emerged as a key global producer due to its extensive lateritic nickel deposits and strong government support for domestic processing.

- Europe: A significant consumer of ferronickel, primarily for its advanced stainless steel and specialized alloy industries. The region focuses on high-value-added products and increasingly stringent environmental regulations are driving investments in cleaner production technologies and recycling initiatives. Germany, Italy, and Spain are key markets within Europe.

- North America: Characterized by mature industrial sectors and a demand for high-quality stainless steel for various applications, including automotive, aerospace, and infrastructure. The region emphasizes technological innovation and sustainable sourcing, with a growing interest in domestic production and recycling to enhance supply chain resilience.

- Latin America: Holds importance due to its nickel mining activities, particularly in countries like Brazil and Colombia. While also a producer, its consumption of ferronickel is growing with developing industrial bases and infrastructure projects, although less dominant than Asia Pacific.

- Middle East and Africa (MEA): Emerging as a region with potential, driven by developing infrastructure and industrial projects. While currently smaller in consumption compared to other regions, increasing industrialization and diversification efforts are expected to fuel future demand for stainless steel and, consequently, ferronickel.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ferronickel Market.- Eramet Group

- Pacific Steel Corp.

- Sumitomo Metal Mining Co. Ltd.

- Tsingshan Holding Group

- Shanghai Decent Investment Group

- Anglo American PLC

- Vale S.A.

- Glencore PLC

- PT Antam Tbk

- South32 Ltd.

- BHP Group

- Jinchuan Group International Resources Co. Ltd.

- Metalcorp Group

- Cerro Matoso S.A.

- POSCO

- Nippon Yakin Kogyo Co. Ltd.

- Acerinox S.A.

- Norilsk Nickel

- Huadi Steel Group

- Nickel Asia Corporation

Frequently Asked Questions

What is ferronickel primarily used for?

Ferronickel is predominantly used in the production of stainless steel, where it provides essential properties such as corrosion resistance and enhanced strength. Approximately 80-90% of global ferronickel output is consumed by the stainless steel industry.

Which region dominates the ferronickel market?

The Asia Pacific region, particularly countries like China and Indonesia, dominates the global ferronickel market due to extensive nickel ore reserves, significant stainless steel production capacities, and ongoing industrialization.

What are the key factors driving the growth of the ferronickel market?

The primary drivers include the consistent global demand for stainless steel, rapid urbanization and infrastructure development, and the increasing use of nickel-containing alloys in various specialized industrial applications.

How do environmental regulations impact ferronickel production?

Strict environmental regulations, especially concerning emissions and waste management, significantly impact ferronickel production by increasing operational costs due to required investments in cleaner technologies and sustainable practices.

What are the main types of ferronickel available in the market?

The main types of ferronickel are High-Carbon Ferronickel (HCFN), which is widely used in standard stainless steel production, and Low-Carbon Ferronickel (LCFN), utilized for more specialized alloys requiring lower carbon content.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted