Farm Tractor Market

Farm Tractor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708724 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

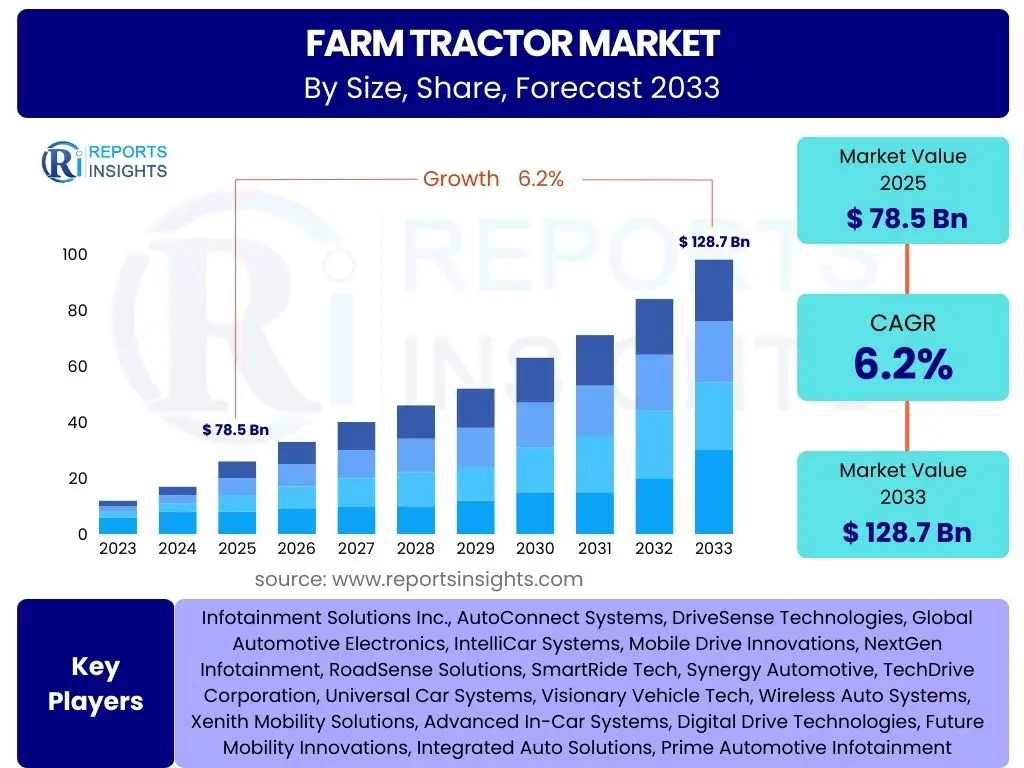

Farm Tractor Market Size

According to Reports Insights Consulting Pvt Ltd, The Farm Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 78.5 Billion in 2025 and is projected to reach USD 128.7 Billion by the end of the forecast period in 2033.

Key Farm Tractor Market Trends & Insights

User queries frequently highlight a strong interest in how technological advancements are reshaping the farm tractor market, specifically focusing on the integration of smart agriculture solutions and sustainable practices. There is a clear demand for information regarding the evolution towards more efficient, autonomous, and environmentally friendly machinery. Additionally, users are keen to understand the shift in demand patterns across different regions, particularly the rising adoption of mechanization in developing economies and the need for high-horsepower tractors in established agricultural markets. The emphasis is on innovations that promise enhanced productivity, reduced operational costs, and improved environmental stewardship.

Another prevalent theme in user questions revolves around the economic factors influencing market dynamics, such as fluctuating commodity prices, government subsidies, and the overall financial health of the agricultural sector. Users seek insights into how these macroeconomic elements impact investment decisions in new farm equipment. Furthermore, there is considerable interest in understanding the evolving design and power output segments of tractors, with specific questions about the growth of electric and hybrid models, and the increasing sophistication of onboard telematics and data analytics capabilities that are becoming standard features in modern farm tractors.

- Integration of precision agriculture technologies, including GPS guidance, telematics, and variable rate technology, is significantly enhancing operational efficiency and yield optimization.

- Rising adoption of autonomous and semi-autonomous tractors, driven by labor shortages and the desire for continuous operation, is a transformative trend.

- Increasing demand for electric and hybrid tractors, propelled by stringent emission regulations and a growing focus on sustainable farming practices, is influencing product development.

- The development of smart implements and connectivity solutions that allow tractors to communicate seamlessly with other farm machinery and cloud-based platforms for data-driven decision-making.

- Growing preference for high-horsepower tractors in large-scale farming operations, particularly in North America and Europe, to cover vast areas efficiently.

- Expansion of rental and leasing services for farm tractors, offering cost-effective solutions for small and medium-sized farms and reducing initial investment burdens.

AI Impact Analysis on Farm Tractor

User inquiries frequently explore the transformative potential of artificial intelligence (AI) in farm tractor technology, focusing on how AI can enhance automation, decision-making, and overall operational efficiency. Common questions revolve around the practical applications of AI in areas such as predictive maintenance, yield optimization, and autonomous navigation. Users are keenly interested in understanding how AI-powered systems can enable tractors to perform tasks with greater precision, reducing waste and improving resource management, thereby addressing critical challenges faced by modern agriculture, including labor shortages and the need for sustainable practices.

Furthermore, concerns and expectations about AI's influence extend to its role in data analysis and farm management. Users want to know how AI algorithms can process vast amounts of sensor data collected by tractors to provide actionable insights for crop health monitoring, soil analysis, and optimal planting and harvesting strategies. There's also an emphasis on the ethical implications, data security, and the necessary infrastructure and skill development required for widespread AI adoption in agricultural machinery, indicating a holistic interest in both the benefits and the practical considerations of AI integration.

- Autonomous Operation: AI enables farm tractors to operate autonomously, performing tasks such as plowing, planting, spraying, and harvesting with minimal human intervention, leveraging advanced sensor fusion, computer vision, and machine learning for navigation and task execution.

- Precision Agriculture: AI-powered systems analyze real-time data from sensors on tractors (e.g., soil conditions, crop health, weather patterns) to optimize inputs like water, fertilizers, and pesticides, leading to higher yields and reduced environmental impact.

- Predictive Maintenance: AI algorithms monitor tractor performance data to predict potential mechanical failures before they occur, scheduling maintenance proactively, reducing downtime, and extending the lifespan of machinery.

- Yield Optimization: AI integrates historical and real-time data to create highly accurate yield maps and recommendations for planting densities, fertilization rates, and irrigation schedules, maximizing crop output per acre.

- Smart Implement Control: AI allows tractors to intelligently control attached implements, adjusting settings in real-time based on varying field conditions and crop requirements for optimal performance and efficiency.

- Data-Driven Decision Making: AI aggregates and analyzes data from the tractor and other farm systems, providing farmers with comprehensive insights and recommendations for improved farm management strategies and operational planning.

Key Takeaways Farm Tractor Market Size & Forecast

Common user questions regarding the farm tractor market size and forecast consistently point to an interest in understanding the primary growth drivers, the impact of technological innovation, and the geographical distribution of market expansion. Users are looking for clear insights into what factors will sustain or accelerate market growth, such as increasing mechanization in emerging economies and the adoption of advanced farming techniques in developed regions. There is also a significant focus on how new product developments, particularly in automation and sustainable power sources, will influence future market valuation and competitive landscapes. The summary reflects a market poised for sustained expansion, underpinned by technological advancements and evolving agricultural practices.

- The farm tractor market is set for robust growth, driven by the imperative to enhance agricultural productivity and efficiency globally.

- Technological innovation, particularly in precision agriculture and autonomous capabilities, will be a primary catalyst for market expansion.

- Emerging economies in Asia Pacific and Latin America are expected to contribute significantly to market growth due to increasing mechanization.

- Demand for higher horsepower and specialized tractors is on the rise, reflecting the trend towards large-scale and intensive farming.

- Sustainable farming practices and environmental regulations are accelerating the adoption of electric and hybrid models, reshaping product portfolios.

- Strategic partnerships and mergers among key players are anticipated to foster innovation and expand market reach.

Farm Tractor Market Drivers Analysis

The global farm tractor market is significantly propelled by several key drivers, primarily stemming from the increasing need for food security for a growing global population and the concurrent pressure to enhance agricultural productivity. The adoption of modern farming techniques, including mechanization, is becoming indispensable for optimizing yield and managing farm operations efficiently. Governments worldwide are also playing a crucial role through supportive policies and subsidies aimed at boosting agricultural output and modernizing farming practices, particularly in developing nations. These initiatives not only incentivize farmers to invest in advanced machinery but also make such investments more financially viable.

Furthermore, the escalating global demand for food, coupled with a shrinking agricultural labor force in many regions, directly drives the need for more efficient and automated farm equipment. This demographic shift necessitates machinery that can perform tasks faster and with less manual input, making farm tractors a critical component of modern agricultural infrastructure. Advancements in tractor technology, such as the integration of GPS, telematics, and smart farming solutions, further contribute to their appeal by offering enhanced precision, fuel efficiency, and operational intelligence, thereby boosting their market demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Food Demand & Population Growth | +1.5% | Global, particularly Asia Pacific, Africa | Short to Long-term (2025-2033) |

| Rising Adoption of Farm Mechanization in Developing Regions | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long-term (2026-2033) |

| Government Support & Subsidies for Agricultural Modernization | +1.0% | India, China, Brazil, EU countries | Short to Medium-term (2025-2030) |

| Technological Advancements in Tractor Features (Precision Farming, Automation) | +1.3% | North America, Europe, Australia | Short to Long-term (2025-2033) |

Farm Tractor Market Restraints Analysis

Despite significant growth potential, the farm tractor market faces several notable restraints that could temper its expansion. One of the primary limiting factors is the high initial capital investment required for purchasing new, technologically advanced tractors. This cost can be prohibitive for small and marginal farmers, especially in developing economies where access to credit and financial resources may be limited. The increasing sophistication of modern tractors, while offering efficiency benefits, also contributes to their higher price tags, making them less accessible to a significant segment of the agricultural community. This economic barrier often forces farmers to rely on older machinery or manual labor, thereby slowing down the rate of mechanization.

Another significant restraint is the volatility in raw material prices, such as steel, rubber, and various electronic components, which directly impacts the manufacturing cost of farm tractors. Fluctuations in these prices can lead to higher production costs for manufacturers, which are often passed on to consumers, further increasing the final price of the equipment. Additionally, stringent environmental regulations in developed regions, while promoting sustainable practices, can lead to increased research and development costs for manufacturers to meet emission standards, potentially stifling innovation or increasing product prices. The shortage of skilled labor capable of operating and maintaining advanced farm machinery also poses a challenge, particularly as tractors become more complex and integrated with smart technologies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Cost for Advanced Tractors | -0.8% | Global, particularly developing economies | Short to Long-term (2025-2033) |

| Fluctuating Raw Material Prices & Supply Chain Disruptions | -0.6% | Global | Short to Medium-term (2025-2028) |

| Stringent Emission Regulations & Environmental Standards | -0.4% | Europe, North America, Japan | Medium to Long-term (2026-2033) |

| Shortage of Skilled Labor for Operation & Maintenance of Advanced Machinery | -0.5% | Global, particularly developed regions | Medium to Long-term (2027-2033) |

Farm Tractor Market Opportunities Analysis

The farm tractor market is characterized by several compelling opportunities that are poised to drive significant growth and innovation. The increasing global focus on precision agriculture and smart farming technologies presents a vast avenue for manufacturers to integrate advanced analytics, IoT, and AI into their products. This shift allows for the development of tractors capable of highly optimized operations, from variable rate application to autonomous field navigation, catering to a growing demand for efficiency and resource conservation. Such technological advancements enable farmers to maximize yields while minimizing environmental impact, thereby creating a strong market pull for next-generation farm machinery.

Furthermore, the emerging markets, particularly in Asia Pacific and Latin America, offer substantial untapped potential due to ongoing agricultural modernization and increasing government support for mechanization. As these regions transition from traditional farming methods to more industrialized approaches, the demand for farm tractors of all horsepower ranges is expected to surge. The growing trend towards electric and hybrid tractors also represents a significant opportunity, driven by rising fuel costs, environmental concerns, and evolving regulatory landscapes. Manufacturers investing in these sustainable power solutions can capture a niche market and establish themselves as leaders in eco-friendly agricultural machinery, appealing to a segment of farmers keen on reducing their carbon footprint and operational expenses.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Adoption of Precision Farming & Smart Agriculture Technologies | +1.8% | North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Growth in Emerging Economies & Mechanization in Developing Countries | +1.5% | India, China, Brazil, Southeast Asia, Africa | Medium to Long-term (2026-2033) |

| Development & Commercialization of Electric & Hybrid Tractors | +1.0% | Europe, North America, Japan | Medium to Long-term (2027-2033) |

| Expansion of Aftermarket Services & Rental Business Models | +0.7% | Global | Short to Medium-term (2025-2030) |

Farm Tractor Market Challenges Impact Analysis

The farm tractor market, while dynamic, faces several significant challenges that could impede its growth trajectory. One prominent challenge is the increasing complexity of advanced farm machinery. Modern tractors, integrated with sophisticated electronics, AI, and IoT, require specialized skills for operation, maintenance, and repair. This presents a substantial hurdle for farmers, particularly in regions where access to skilled labor and technical training is limited, leading to potential operational inefficiencies and increased maintenance costs. The steep learning curve associated with these high-tech tractors can deter adoption, especially among traditional farmers, thus slowing the market penetration of innovative products.

Another critical challenge stems from the intense competition within the market, leading to price wars and reduced profit margins for manufacturers. The presence of numerous global and regional players, coupled with the introduction of new models, puts continuous pressure on pricing strategies. Furthermore, the agricultural sector is inherently susceptible to various external factors such as unpredictable weather patterns, climate change effects, and fluctuating crop prices. These variables can directly impact farmers' purchasing power and their willingness to invest in new equipment, creating demand volatility. Supply chain disruptions, as recently demonstrated by global events, also pose a persistent challenge, affecting the availability of components and raw materials, and leading to production delays and increased costs for manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of Advanced Machinery & Need for Skilled Operators | -0.7% | Global, particularly developing regions | Medium to Long-term (2026-2033) |

| Intense Market Competition & Price Sensitivity | -0.5% | Global | Short to Medium-term (2025-2030) |

| Impact of Climate Change & Volatile Agricultural Yields | -0.4% | Global | Long-term (2028-2033) |

| Supply Chain Disruptions & Raw Material Shortages | -0.6% | Global | Short to Medium-term (2025-2028) |

Farm Tractor Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Farm Tractor Market, offering an in-depth analysis of its current size, historical performance, and future growth projections from 2025 to 2033. It systematically segments the market by power output, drive type, application, and automation level, providing granular insights into each category's market share and growth potential. The report also highlights key market trends, drivers, restraints, opportunities, and challenges that shape the industry landscape, alongside a detailed profiling of top-tier companies operating within this competitive sector. Regional analyses are integrated to offer a holistic understanding of market variations and growth hotspots across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 78.5 Billion |

| Market Forecast in 2033 | USD 128.7 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Mahindra & Mahindra Ltd., Tractors and Farm Equipment Limited (TAFE), CLAAS KGaA mbH, SDF Group, Iseki & Co. Ltd., Escorts Limited, Sonalika International Tractors Ltd., Arbos Group S.p.A., John Deere India Private Limited, Valtra (AGCO Corporation), Kioti Tractor (Daedong Industrial Co., Ltd.), Lovol Heavy Industry Co., Ltd., Zetor Tractors a.s., Same Deutz-Fahr India Pvt. Ltd., Carraro Agritalia S.p.A., Versatile (Buhler Industries Inc.) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The farm tractor market is comprehensively segmented to provide a detailed understanding of its diverse components and growth avenues. This segmentation allows for precise analysis of market dynamics across different product specifications, operational capabilities, and end-use applications. By categorizing tractors based on power output, drive type, application, and automation level, stakeholders can gain targeted insights into consumer preferences, technological adoption rates, and regional demand patterns. This granular view is essential for strategic planning, product development, and market entry strategies, ensuring that investments are aligned with the most promising growth areas within the agricultural machinery sector.

- By Power Output:

- Below 40 HP: Primarily used by small and marginal farmers for tasks like tilling, plowing, and hauling in small landholdings.

- 40-100 HP: Represents the mid-range segment, widely adopted for diverse farming activities in medium-sized farms, offering a balance of power and versatility.

- Above 100 HP: Dominant in large-scale commercial farming, these high-power tractors are essential for heavy-duty tasks, requiring significant traction and pulling power.

- By Drive Type:

- 2-Wheel Drive (2WD): More cost-effective and suitable for flat, dry terrains and lighter tasks, favored in many developing agricultural markets.

- 4-Wheel Drive (4WD): Offers superior traction and power, ideal for challenging terrains, heavy-duty applications, and wet or slippery conditions, prevalent in developed agricultural regions.

- By Application:

- Agriculture: The largest segment, encompassing all farming activities from land preparation to harvesting and post-harvest handling.

- Construction: Tractors are adapted for light construction tasks such as landscaping, excavation, and material handling in smaller projects.

- Other Industrial Applications: Includes utility and municipal applications, such as grounds maintenance, snow removal, and industrial hauling.

- By Automation Level:

- Manual: Traditional tractors requiring full human operation.

- Semi-Autonomous: Tractors with features like auto-steering, GPS guidance, and partial task automation, requiring human oversight.

- Autonomous: Fully self-driving tractors capable of performing tasks without direct human intervention, leveraging AI and advanced sensors.

Regional Highlights

- North America: This region is a mature market characterized by the early adoption of advanced farming technologies, including precision agriculture, GPS-enabled tractors, and increasingly, autonomous solutions. The presence of large-scale farming operations drives demand for high-horsepower and technologically sophisticated tractors, with a strong emphasis on efficiency and data-driven farming. Government support for agricultural innovation and the availability of financing options further bolster market growth.

- Europe: Europe stands as a key market with a strong focus on sustainable agriculture, stringent emission standards, and technological innovation. The demand here is driven by the need for eco-friendly and fuel-efficient tractors, leading to significant investments in electric and hybrid models. Precision farming and digital agriculture solutions are widely adopted, and the market benefits from well-established agricultural policies and a strong emphasis on environmental stewardship.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market for farm tractors, primarily due to rapid agricultural mechanization in countries like India, China, and Southeast Asia. The region is characterized by a large base of small and medium-sized farms, driving demand for compact and mid-horsepower tractors. Government initiatives, subsidies for farm equipment, and a growing population needing food security are key growth enablers. The increasing adoption of modern farming practices is transforming traditional agricultural landscapes.

- Latin America: This region presents significant growth potential, fueled by expanding agricultural lands, the commercialization of farming, and increasing exports of agricultural products. Countries like Brazil and Argentina are witnessing a surge in demand for high-performance tractors to manage vast plantations. Government programs aimed at improving agricultural productivity and enhancing food security are also contributing to market expansion, alongside a growing interest in precision agriculture technologies.

- Middle East and Africa (MEA): The MEA market is gradually expanding, driven by efforts to modernize agriculture, enhance food security, and reduce reliance on food imports. Investments in irrigation projects and the development of large-scale farms in certain areas are stimulating demand for farm tractors. Challenges related to water scarcity and diverse climatic conditions also necessitate efficient and specialized machinery, leading to a steady, albeit slower, adoption of mechanization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Farm Tractor Market.- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- Tractors and Farm Equipment Limited (TAFE)

- CLAAS KGaA mbH

- SDF Group

- Iseki & Co. Ltd.

- Escorts Limited

- Sonalika International Tractors Ltd.

- Arbos Group S.p.A.

- John Deere India Private Limited

- Valtra (AGCO Corporation)

- Kioti Tractor (Daedong Industrial Co., Ltd.)

- Lovol Heavy Industry Co., Ltd.

- Zetor Tractors a.s.

- Same Deutz-Fahr India Pvt. Ltd.

- Carraro Agritalia S.p.A.

- Versatile (Buhler Industries Inc.)

Frequently Asked Questions

What is the current market size of the farm tractor industry?

The farm tractor market is estimated at USD 78.5 Billion in 2025 and is projected to reach USD 128.7 Billion by 2033, growing at a CAGR of 6.2%.

What are the key trends shaping the farm tractor market?

Key trends include the integration of precision agriculture, rising adoption of autonomous and electric tractors, increasing demand for high-horsepower models, and the expansion of digital connectivity and smart implements.

How is AI impacting farm tractor technology?

AI is transforming farm tractors by enabling autonomous operation, optimizing precision agriculture inputs, facilitating predictive maintenance, enhancing yield optimization, and providing data-driven decision-making for farmers.

Which regions are leading in the farm tractor market?

North America and Europe are significant markets for advanced tractors, while Asia Pacific, particularly India and China, is the fastest-growing region due to increasing mechanization and government support.

What are the main challenges for the farm tractor market?

Major challenges include the high initial investment cost, complexity of advanced machinery requiring skilled operators, fluctuating raw material prices, intense market competition, and the impacts of climate change on agricultural yields.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted