Factory Automation and Industrial Control Market

Factory Automation and Industrial Control Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703952 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Factory Automation and Industrial Control Market Size

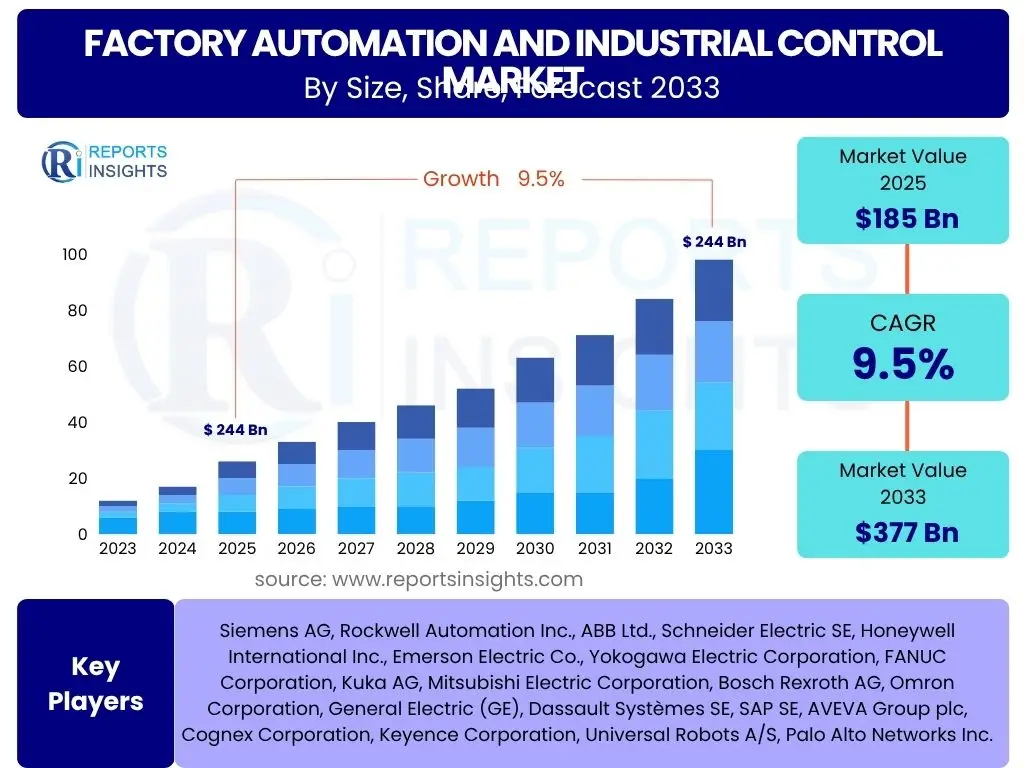

According to Reports Insights Consulting Pvt Ltd, The Factory Automation and Industrial Control Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 185 billion in 2025 and is projected to reach USD 377 billion by the end of the forecast period in 2033.

Key Factory Automation and Industrial Control Market Trends & Insights

User queries frequently highlight the accelerating pace of digital transformation and the imperative for operational efficiency as central themes in the Factory Automation and Industrial Control market. Businesses are keenly interested in understanding how emerging technologies are being integrated to enhance productivity, reduce costs, and improve overall quality. A significant focus of user inquiry is on the practical applications of Industry 4.0 paradigms, encompassing the convergence of information technology (IT) and operational technology (OT), and the development of intelligent, interconnected systems within manufacturing and process industries.

Furthermore, there is a consistent demand for insights into the evolution of automation beyond traditional programmable logic controllers (PLCs) and distributed control systems (DCS). Users are exploring advancements in collaborative robotics, autonomous mobile robots (AMRs), and advanced analytics platforms that enable predictive maintenance and real-time decision-making. The increasing complexity of global supply chains and the need for greater agility and resilience are also driving interest in modular and flexible automation solutions that can adapt to fluctuating market demands and geopolitical shifts. Cybersecurity in industrial environments is another critical area of concern, as the proliferation of connected devices introduces new vulnerabilities that require robust protective measures.

- Accelerated adoption of Industry 4.0 principles and digital transformation initiatives across industrial sectors.

- Rising integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive maintenance, quality control, and process optimization.

- Proliferation of Industrial Internet of Things (IIoT) devices and cloud/edge computing for enhanced connectivity and data analytics.

- Development and deployment of collaborative robots (cobots) and autonomous mobile robots (AMRs) to work alongside human operators.

- Emphasis on modular, flexible, and scalable automation solutions to adapt to dynamic production requirements.

- Increased focus on cybersecurity measures for protecting critical industrial infrastructure and data from cyber threats.

- Growth in demand for sustainable and energy-efficient automation technologies to meet environmental regulations and reduce operational costs.

AI Impact Analysis on Factory Automation and Industrial Control

Common user questions regarding AI's impact on Factory Automation and Industrial Control revolve primarily around its transformative potential for efficiency, predictive capabilities, and autonomous operations. Users are keen to understand how AI algorithms can analyze vast datasets generated by industrial equipment to preempt failures, optimize production parameters, and reduce downtime. There is significant interest in AI's role in enhancing quality control through vision systems and defect detection, moving beyond traditional statistical process control to more intelligent, real-time adjustments. Concerns often include the complexity of AI implementation, the need for specialized data infrastructure, and the ethical implications surrounding job displacement and human-AI collaboration.

The discussion frequently extends to the practicalities of integrating AI into existing legacy systems and the necessity for robust cybersecurity frameworks to protect AI-driven processes. Users are also exploring how AI can facilitate more sophisticated adaptive control, enabling systems to learn and adjust autonomously to varying conditions, leading to greater flexibility and resilience in manufacturing. Expectations are high for AI to unlock new levels of operational intelligence, fostering a proactive rather than reactive approach to factory management. This includes the development of digital twins augmented by AI to simulate and optimize complex industrial processes before physical implementation, thereby reducing risks and accelerating innovation cycles.

- Enhances predictive maintenance capabilities by analyzing sensor data to forecast equipment failures, minimizing unplanned downtime.

- Optimizes production processes through real-time data analysis, leading to improved throughput, energy efficiency, and resource utilization.

- Boosts quality control with advanced vision systems and machine learning algorithms for precise defect detection and product inspection.

- Enables more autonomous operations and adaptive control systems, allowing machines to learn and adjust to dynamic environmental conditions.

- Facilitates human-robot collaboration by allowing AI-powered robots to understand and respond to human gestures and intentions.

- Improves supply chain efficiency and logistics through AI-driven demand forecasting and inventory management.

- Strengthens industrial cybersecurity by identifying anomalous behavior and potential threats within operational technology (OT) networks.

Key Takeaways Factory Automation and Industrial Control Market Size & Forecast

Analysis of common user questions regarding the Factory Automation and Industrial Control market size and forecast consistently reveals a focus on sustained growth driven by pervasive digital transformation initiatives. Users are primarily interested in understanding the primary catalysts behind this expansion, with particular emphasis on how increased investment in smart manufacturing and Industry 4.0 technologies is shaping the market trajectory. The transition from traditional, isolated automation systems to integrated, data-driven frameworks is a significant area of inquiry, reflecting a broader industry shift towards intelligent and adaptive production environments. This includes the adoption of advanced robotics, sophisticated sensor technologies, and robust data analytics platforms.

Furthermore, user queries often seek to identify the most promising sectors and geographical regions for automation adoption, indicating a strategic interest in market hotbeds and emerging opportunities. The growing imperative for efficiency, labor cost optimization, and enhanced product quality is frequently cited as a core motivation for investment. There is also a notable interest in the resilience benefits offered by automation, particularly in mitigating supply chain disruptions and enabling agile responses to market fluctuations. The long-term forecast points to an expanding scope of automation applications, moving beyond traditional manufacturing into diverse sectors like logistics, utilities, and even healthcare, underscoring the broad impact of these technologies on global industrial landscapes.

- The market is poised for robust growth, driven by the global push towards digital transformation and smart manufacturing.

- Significant expansion is expected in sectors prioritizing operational efficiency, cost reduction, and enhanced product quality through automation.

- Technological advancements in AI, IIoT, and robotics are key enablers, fostering more intelligent and interconnected industrial systems.

- Investments in factory automation are critical for building resilient supply chains and maintaining competitiveness in a dynamic global economy.

- The Asia Pacific region is anticipated to be a major growth engine, fueled by rapid industrialization and government support for smart factories.

- Increased adoption by Small and Medium-sized Enterprises (SMEs) presents a substantial untapped growth opportunity for vendors.

- The market will see continued integration of IT and OT, leading to more holistic and predictive industrial control environments.

Factory Automation and Industrial Control Market Drivers Analysis

The Factory Automation and Industrial Control market is fundamentally driven by a confluence of factors centered on the pursuit of operational excellence and industrial evolution. A primary driver is the pervasive adoption of Industry 4.0 principles, which advocate for smart factories characterized by interconnected systems, real-time data exchange, and autonomous operations. This paradigm shift encourages manufacturers to integrate advanced automation technologies to achieve higher levels of productivity, precision, and flexibility. The global competitive landscape further intensifies this drive, as companies seek to reduce production costs, minimize human error, and accelerate time-to-market through automated processes, thereby maintaining a competitive edge.

Another significant driver is the increasing cost of labor and a growing shortage of skilled workers in many industrialized nations. Automation provides a compelling solution to these challenges, enabling businesses to optimize their workforce, reallocate human capital to higher-value tasks, and ensure consistent production quality despite labor constraints. Furthermore, stringent regulatory requirements for product quality, safety, and environmental compliance are compelling industries to adopt automated systems that offer precise control, comprehensive data logging, and reduced waste. The rising demand for mass customization and personalized products also necessitates agile and reconfigurable automation solutions, moving away from rigid, mass-production lines towards flexible manufacturing systems capable of handling diverse product portfolios.

The expanding capabilities of technologies such as Artificial Intelligence, Machine Learning, and the Industrial Internet of Things (IIoT) serve as powerful enablers for market growth. These advancements allow for predictive maintenance, real-time analytics, and optimized resource utilization, significantly enhancing the efficiency and reliability of industrial operations. Governments worldwide are also playing a crucial role by initiating programs and offering incentives that promote the adoption of advanced manufacturing technologies, recognizing their importance for economic growth and national competitiveness. This supportive policy environment, combined with continuous innovation in automation hardware and software, creates a robust ecosystem for sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industry 4.0 and Digital Transformation Initiatives | +2.5% | Global, particularly Europe, Asia Pacific, North America | Short to Long-term |

| Rising Labor Costs and Skilled Workforce Shortage | +2.0% | North America, Europe, Developed Asia Pacific | Medium to Long-term |

| Increasing Demand for Operational Efficiency and Productivity | +1.8% | Global | Short to Medium-term |

| Growing Emphasis on Quality Control and Product Consistency | +1.5% | Global | Short to Medium-term |

| Government Support and Initiatives for Smart Manufacturing | +1.2% | China, Germany, Japan, South Korea, US | Medium to Long-term |

Factory Automation and Industrial Control Market Restraints Analysis

Despite the strong growth trajectory, the Factory Automation and Industrial Control market faces several significant restraints that could impede its full potential. A primary constraint is the substantial initial capital investment required for implementing advanced automation systems. Many small and medium-sized enterprises (SMEs) find these upfront costs prohibitive, especially when considering not only the hardware and software but also the expenses associated with system integration, training, and infrastructure upgrades. This high entry barrier can slow down the adoption rate, particularly in developing regions or for companies with limited financial resources, thereby limiting overall market penetration.

Another critical restraint is the inherent cybersecurity risk associated with increasingly connected industrial environments. As operational technology (OT) networks become more integrated with information technology (IT) systems and external networks, they become vulnerable to sophisticated cyberattacks. Concerns about data breaches, intellectual property theft, and disruptions to critical infrastructure deter some organizations from fully embracing digitalized automation. The lack of standardized communication protocols and interoperability issues among different vendors' systems also poses a challenge, leading to complex and costly integration efforts that can deter potential adopters seeking seamless, plug-and-play solutions.

Furthermore, the scarcity of a skilled workforce capable of deploying, maintaining, and troubleshooting advanced automation and control systems presents a significant bottleneck. While automation aims to address labor shortages, it simultaneously creates a demand for new skill sets related to programming, data analytics, AI, and cybersecurity. The slow pace of workforce upskilling and reskilling can limit the effective utilization of sophisticated automation technologies, leading to suboptimal performance and hindering wider adoption. Economic uncertainties, such as global recessions or trade disputes, can also lead to reduced industrial investment, consequently impacting the growth of the factory automation and industrial control market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment and Implementation Costs | -1.5% | Global, particularly SMEs in developing regions | Short to Medium-term |

| Growing Cybersecurity Risks and Data Vulnerabilities | -1.2% | Global, critical infrastructure sectors | Short to Long-term |

| Lack of Skilled Workforce for Advanced Automation Systems | -1.0% | Global, particularly North America, Europe | Medium to Long-term |

| Interoperability and Standardization Challenges | -0.8% | Global | Short to Medium-term |

| Economic Uncertainties and Geopolitical Instability | -0.7% | Global, varying by region | Short-term |

Factory Automation and Industrial Control Market Opportunities Analysis

The Factory Automation and Industrial Control market is rich with opportunities stemming from technological innovation, expanding application areas, and evolving business models. A significant opportunity lies in the continued advancements and wider adoption of the Industrial Internet of Things (IIoT) and 5G technology. The proliferation of connected devices, combined with the high bandwidth and low latency of 5G networks, enables real-time data collection, remote monitoring, and highly distributed control, opening doors for more sophisticated and efficient automation solutions across various industrial verticals. This connectivity facilitates new services, such as condition monitoring as a service and performance optimization, creating recurring revenue streams for vendors.

The growing interest in sustainable manufacturing and circular economy principles also presents a substantial opportunity. Companies are increasingly seeking automation solutions that can reduce energy consumption, minimize waste, and optimize resource utilization, aligning with global environmental objectives. This drives demand for energy-efficient industrial control systems, advanced process optimization software, and robotics that can handle recycling and remanufacturing processes. Furthermore, the untapped potential in small and medium-sized enterprises (SMEs) represents a vast market segment. As automation solutions become more affordable, modular, and easier to deploy, SMEs are increasingly able to leverage these technologies to enhance their competitiveness, improve product quality, and scale their operations.

The emergence of Artificial Intelligence (AI) and Machine Learning (ML) as integral components of industrial control systems creates opportunities for predictive analytics, self-optimizing processes, and highly personalized production. AI-powered vision systems for quality control, machine learning for predictive maintenance, and robotic process automation (RPA) for administrative tasks are transforming operations across industries. Moreover, the shift towards cloud-based and edge computing solutions for industrial applications is enabling greater flexibility, scalability, and data processing closer to the source, reducing latency and improving decision-making speed. The development of digital twins and simulation technologies also offers immense potential for optimizing plant design, process validation, and operator training, leading to faster deployment and reduced operational risks.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of IIoT and 5G Connectivity in Industrial Environments | +2.0% | Global | Short to Medium-term |

| Growing Adoption of Automation by Small and Medium Enterprises (SMEs) | +1.8% | Emerging Economies, Europe, North America | Medium to Long-term |

| Integration of AI and Machine Learning for Enhanced Automation | +1.7% | Global | Short to Long-term |

| Increasing Demand for Sustainable and Energy-Efficient Solutions | +1.5% | Europe, North America, Developed Asia Pacific | Medium to Long-term |

| Rise of Cloud-based and Edge Computing for Industrial Applications | +1.3% | Global | Short to Medium-term |

Factory Automation and Industrial Control Market Challenges Impact Analysis

The Factory Automation and Industrial Control market is not without its significant challenges, which require careful navigation for sustained growth. One prominent challenge is the complexity of integrating diverse automation technologies and systems, particularly in brownfield environments with legacy infrastructure. Achieving seamless interoperability between new intelligent devices, existing control systems, and enterprise-level software often involves extensive customization, significant engineering effort, and can lead to cost overruns and project delays. The lack of universal communication standards further exacerbates these integration complexities, making holistic automation difficult to achieve for many organizations.

Another critical challenge lies in managing and analyzing the vast amounts of data generated by connected industrial assets. While data is a key enabler for advanced automation, its effective collection, storage, processing, and interpretation require robust infrastructure, sophisticated analytics capabilities, and specialized expertise. Ensuring data quality, security, and privacy across a complex industrial ecosystem presents considerable hurdles. Additionally, the rapid pace of technological evolution means that companies must constantly invest in upgrading their systems and training their personnel, creating a continuous cycle of expenditure and the risk of technology obsolescence if not managed strategically.

Compliance with evolving regulatory frameworks and industry standards also poses a significant hurdle, especially for operations across multiple geographies with varying requirements for safety, environmental impact, and data governance. Maintaining compliance while implementing innovative automation solutions adds layers of complexity to project planning and execution. Furthermore, supply chain disruptions, as experienced recently, can impact the availability of critical components and lead times for automation equipment, directly affecting project timelines and costs. Navigating these multifaceted challenges requires a strategic approach that prioritizes robust integration strategies, data governance, continuous upskilling, and a proactive stance on regulatory compliance and supply chain resilience.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration Complexities with Legacy Systems (Brownfield Sites) | -1.3% | Global | Short to Medium-term |

| Managing and Analyzing Big Data from Industrial Operations | -1.1% | Global | Medium to Long-term |

| Rapid Technological Obsolescence and Continuous Upgrade Requirements | -0.9% | Global | Short to Medium-term |

| Adherence to Evolving Regulatory and Compliance Standards | -0.8% | Global, varying by region/industry | Short to Long-term |

| Supply Chain Disruptions Affecting Component Availability | -0.7% | Global | Short-term |

Factory Automation and Industrial Control Market - Updated Report Scope

This report provides a comprehensive analysis of the Factory Automation and Industrial Control Market, offering in-depth insights into market size estimations, growth forecasts, and detailed segmentation. It examines the key drivers, restraints, opportunities, and challenges shaping the industry landscape, alongside a thorough impact analysis of emerging technologies like Artificial Intelligence and the Industrial Internet of Things. The scope encompasses a global perspective, covering major regions and identifying dominant as well as rapidly growing segments, ultimately equipping stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185 billion |

| Market Forecast in 2033 | USD 377 billion |

| Growth Rate | 9.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, Rockwell Automation Inc., ABB Ltd., Schneider Electric SE, Honeywell International Inc., Emerson Electric Co., Yokogawa Electric Corporation, FANUC Corporation, Kuka AG, Mitsubishi Electric Corporation, Bosch Rexroth AG, Omron Corporation, General Electric (GE), Dassault Systèmes SE, SAP SE, AVEVA Group plc, Cognex Corporation, Keyence Corporation, Universal Robots A/S, Palo Alto Networks Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Factory Automation and Industrial Control market is comprehensively segmented to provide granular insights into its diverse components, technologies, and end-use industries. This detailed segmentation allows for a precise understanding of market dynamics, growth drivers, and emerging opportunities within each specific sub-segment, enabling businesses to tailor their strategies effectively. The analysis delves into how each segment contributes to the overall market growth, highlighting areas of high potential and those facing specific challenges.

- By Component: This segment differentiates between the physical hardware infrastructure, the controlling and analytical software, and the essential support services required for complete automation systems.

- Hardware includes all tangible components such as sensors, actuators, robotics, controllers (PLCs, DCS), human-machine interfaces, vision systems, and industrial PCs, forming the backbone of automated operations.

- Software encompasses the intelligent applications like Manufacturing Execution Systems (MES), SCADA, Product Lifecycle Management (PLM), Enterprise Resource Planning (ERP), IIoT platforms, cloud solutions, and cybersecurity tools that manage and optimize processes.

- Services cover the crucial support functions from initial consulting and system integration to ongoing maintenance, technical support, training, and managed services, ensuring efficient system operation and longevity.

- By Technology: This segment categorizes the market by the core automation and control technologies employed.

- Key technologies include Distributed Control Systems (DCS) for continuous processes, Programmable Logic Controllers (PLC) for discrete control, Supervisory Control and Data Acquisition (SCADA) for monitoring and control, and Manufacturing Execution Systems (MES) for production management.

- Advanced technologies such as Robotics & Automation, Industrial Internet of Things (IIoT), Artificial Intelligence (AI) & Machine Learning (ML), Additive Manufacturing, Digital Twin, Cloud Computing, and Edge Computing are driving innovation and new capabilities.

- By Industry Vertical: This segmentation examines the adoption and application of factory automation across various end-user industries.

- Major verticals include Automotive, Discrete Manufacturing (e.g., Electronics, Machinery), and Process Manufacturing (e.g., Oil & Gas, Chemicals, Food & Beverage, Pharmaceuticals), each with unique automation requirements.

- Other significant industries include Energy & Utilities, Metals & Mining, Pulp & Paper, Water & Wastewater Management, Aerospace & Defense, Healthcare, and Logistics & Warehousing, all increasingly leveraging automation for efficiency and competitiveness.

Regional Highlights

- North America: This region is characterized by early adoption of advanced manufacturing technologies, significant investments in R&D, and a strong presence of key market players. The push for reshoring manufacturing and modernizing existing facilities, coupled with a focus on smart factory initiatives and cybersecurity, drives robust demand. The automotive, aerospace, and electronics sectors are key contributors to market growth here.

- Europe: Europe is at the forefront of Industry 4.0 adoption, particularly in Germany's "Industrie 4.0" initiative. High labor costs, stringent environmental regulations, and a strong emphasis on sustainability and energy efficiency are propelling the demand for sophisticated automation solutions. The automotive, machinery, and process industries represent significant end-user segments.

- Asia Pacific (APAC): APAC is expected to exhibit the highest growth rate, primarily driven by rapid industrialization, large-scale manufacturing bases, and significant government investments in smart manufacturing infrastructure, particularly in China, Japan, South Korea, and India. The expanding automotive, electronics, and food and beverage sectors are major consumers of factory automation and industrial control systems in this region.

- Latin America: This region is experiencing steady growth in automation adoption, driven by increasing foreign direct investment in manufacturing, particularly in automotive and consumer goods sectors. Modernization efforts and the need to improve production efficiency and competitiveness in global markets are key factors influencing market expansion.

- Middle East and Africa (MEA): The MEA region is witnessing increasing adoption of industrial automation, especially in the oil and gas, petrochemicals, and utilities sectors, driven by infrastructure development and diversification efforts away from traditional energy sources. Investment in smart cities and advanced industrial zones further supports market growth in this evolving landscape.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Factory Automation and Industrial Control Market.- Siemens AG

- Rockwell Automation Inc.

- ABB Ltd.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- FANUC Corporation

- Kuka AG

- Mitsubishi Electric Corporation

- Bosch Rexroth AG

- Omron Corporation

- General Electric (GE)

- Dassault Systèmes SE

- SAP SE

- AVEVA Group plc

- Cognex Corporation

- Keyence Corporation

- Universal Robots A/S

- Palo Alto Networks Inc.

Frequently Asked Questions

What is factory automation and industrial control?

Factory automation and industrial control refers to the use of technology and systems to automate processes, machinery, and equipment in manufacturing and industrial settings. This includes hardware, software, and services designed to enhance efficiency, reduce manual intervention, and improve consistency and quality in production, encompassing technologies from basic control systems to advanced robotics and AI.

What are the key drivers of growth in this market?

Key drivers include the global push for Industry 4.0 adoption, the increasing demand for operational efficiency and productivity, rising labor costs and a shortage of skilled workers, and stricter quality and regulatory compliance requirements. Technological advancements in AI, IIoT, and robotics also significantly contribute to market expansion.

How is AI transforming factory automation?

AI is transforming factory automation by enabling predictive maintenance, optimizing production processes through real-time data analysis, enhancing quality control with advanced vision systems, and facilitating more autonomous and adaptive control systems. It also improves human-robot collaboration and strengthens industrial cybersecurity by identifying anomalies.

What are the main challenges faced by industries adopting these technologies?

Main challenges include the high initial capital investment required, complex integration with existing legacy systems, growing cybersecurity risks to interconnected industrial networks, the scarcity of a skilled workforce to manage advanced systems, and navigating evolving regulatory frameworks and supply chain disruptions.

Which regions are leading the adoption of factory automation?

The Asia Pacific region, particularly countries like China, Japan, and South Korea, is leading in factory automation adoption due to rapid industrialization and strong government support for smart manufacturing. North America and Europe also show significant adoption, driven by advanced manufacturing initiatives and a focus on modernization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted