Extremity Product Market

Extremity Product Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702025 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

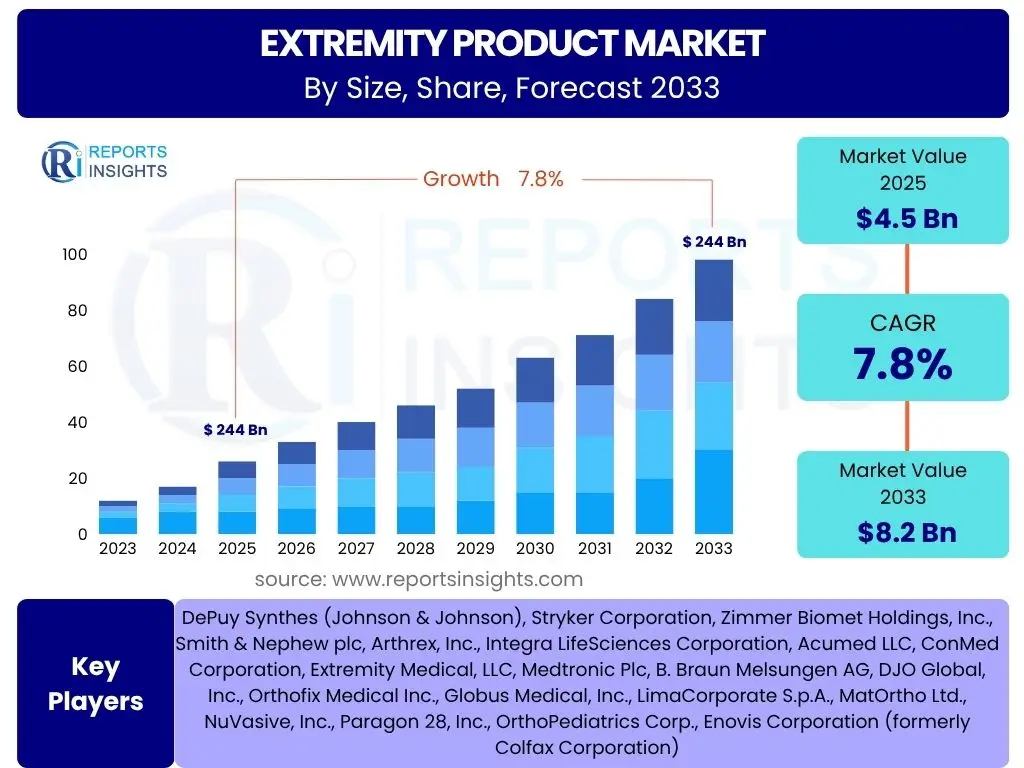

Extremity Product Market Size

According to Reports Insights Consulting Pvt Ltd, The Extremity Product Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 8.2 Billion by the end of the forecast period in 2033.

Key Extremity Product Market Trends & Insights

User inquiries concerning the Extremity Product market frequently center on evolving technological landscapes, shifts in patient demographics, and the adoption of novel surgical techniques. Stakeholders are particularly interested in understanding how advancements in materials science, digital health integration, and non-invasive procedures are reshaping clinical practice and market opportunities. The demand for products that offer improved patient outcomes, faster recovery times, and reduced surgical complexities is a recurring theme, highlighting a strong market pull towards innovation and efficiency.

Another significant area of interest revolves around the increasing prevalence of lifestyle-related injuries and age-related degenerative conditions, which are directly impacting the demand for extremity products. The rising participation in sports, coupled with an aging global population, underscores a growing need for sophisticated solutions in trauma care, joint reconstruction, and rehabilitation. Furthermore, questions arise regarding the customization of implants and the trend towards personalized medicine, indicating a market moving beyond one-size-fits-all approaches to more tailored and patient-specific interventions.

- Growing adoption of minimally invasive surgical techniques for extremity procedures.

- Increasing integration of 3D printing and additive manufacturing for custom implants.

- Shift towards biologics and regenerative medicine solutions for tissue repair.

- Rising prevalence of sports injuries and orthopedic conditions among the aging population.

- Enhanced focus on outpatient settings and ambulatory surgical centers for cost-efficiency.

- Development of smart implants and connected devices for real-time monitoring.

AI Impact Analysis on Extremity Product

Common user questions regarding AI's impact on the Extremity Product domain highlight interest in its application across diagnosis, surgical planning, and post-operative care. Users are keen to understand how artificial intelligence can enhance precision in orthopedic procedures, personalize treatment pathways, and improve predictive analytics for patient outcomes. There is a general expectation that AI will streamline workflows, reduce human error, and potentially lead to more cost-effective healthcare solutions, while also raising questions about data security and regulatory frameworks.

The role of AI in assisting with complex surgical simulations and robotic-assisted surgeries is a significant area of discussion, reflecting a desire for more predictable and repeatable surgical results. Furthermore, inquiries touch upon AI's potential in designing highly customized implants based on individual patient anatomy and pathology, driven by advanced imaging and computational models. This indicates a forward-looking perspective on how AI can contribute to greater personalization and improved functional recovery for patients receiving extremity products.

- Enhanced pre-operative planning and simulation for complex extremity surgeries.

- Improved diagnostic accuracy through AI-powered image analysis (X-ray, MRI, CT).

- Personalized implant design and sizing using AI algorithms and patient-specific data.

- Development of AI-driven robotic assistance for precise surgical execution.

- Predictive analytics for post-operative recovery, rehabilitation, and complication prevention.

- Optimization of supply chain and inventory management for extremity devices.

Key Takeaways Extremity Product Market Size & Forecast

Analysis of user inquiries concerning key takeaways from the Extremity Product market size and forecast reveals a strong interest in understanding the primary growth drivers and potential areas for investment. Users frequently seek concise insights into the market's long-term viability, the influence of technological innovation, and the impact of demographic shifts. The discussions underscore the importance of identifying sustainable growth segments and emerging geographical opportunities that will shape the market's trajectory over the next decade.

Furthermore, there is a consistent demand for information on the competitive landscape and the strategies employed by leading market players to maintain their position or gain market share. Users are keen to grasp the most significant factors that will either accelerate or impede market expansion, enabling them to make informed strategic decisions. The focus remains on understanding the fundamental forces that dictate market expansion, technological adoption, and the overall value proposition of extremity products.

- The market is poised for robust growth, driven by an aging global population and rising incidence of musculoskeletal injuries.

- Technological advancements, including minimally invasive techniques and personalized implants, are key accelerators.

- Emerging economies, particularly in Asia Pacific, represent significant untapped growth opportunities.

- Regulatory challenges and high product costs remain critical factors influencing market accessibility.

- Collaboration between medical device manufacturers and healthcare providers is crucial for product innovation and adoption.

Extremity Product Market Drivers Analysis

The extremity product market is significantly driven by an increasing global geriatric population, which is more susceptible to age-related orthopedic conditions such as osteoarthritis, osteoporosis, and degenerative joint diseases. This demographic shift naturally escalates the demand for reconstructive surgeries and trauma care involving extremity joints. Concurrently, the rising participation in sports and outdoor activities across all age groups contributes to a higher incidence of sports-related injuries, including fractures, ligament tears, and joint dislocations, further boosting the need for advanced extremity products and surgical interventions.

Technological advancements in biomaterials, implant design, and surgical techniques also play a pivotal role in driving market expansion. Innovations such as 3D printing for patient-specific implants, the development of less invasive surgical instruments, and improved biocompatible materials are enhancing product efficacy and reducing recovery times. These advancements not only improve patient outcomes but also encourage broader adoption by healthcare professionals. Additionally, increasing healthcare expenditure in developed and emerging economies, coupled with favorable reimbursement policies for orthopedic procedures, makes advanced extremity treatments more accessible, thereby stimulating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Musculoskeletal Disorders | +1.5% | Global | Long-term (2025-2033) |

| Aging Global Population | +1.3% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Technological Advancements in Extremity Devices | +1.2% | Global, Developed Regions | Mid to Long-term (2025-2033) |

| Rising Incidence of Sports Injuries | +1.0% | North America, Europe, Asia Pacific | Mid-term (2025-2029) |

| Growing Awareness & Healthcare Expenditure | +0.8% | Emerging Economies, Global | Mid to Long-term (2025-2033) |

Extremity Product Market Restraints Analysis

The high cost associated with advanced extremity products and related surgical procedures presents a significant restraint on market growth, particularly in developing economies or healthcare systems with limited public funding. These costs can include the price of implants, surgical equipment, hospital stays, and post-operative rehabilitation, making them unaffordable for a considerable portion of the population. This financial barrier can limit patient access to necessary treatments, thereby impacting overall market penetration and adoption rates for innovative products.

Furthermore, stringent regulatory approval processes imposed by health authorities like the FDA in the US and the EMA in Europe can significantly delay the market entry of new products. The rigorous testing, clinical trials, and documentation required to demonstrate product safety and efficacy are time-consuming and expensive. This regulatory burden not only increases R&D costs for manufacturers but also slows down innovation diffusion, potentially limiting the availability of cutting-edge solutions to patients. The risk of product recalls and post-surgical complications also acts as a restraint, eroding patient and physician confidence and potentially leading to significant financial and reputational damage for manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Extremity Products & Procedures | -1.0% | Global, Developing Economies | Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -0.9% | North America, Europe | Mid to Long-term (2025-2033) |

| Risk of Post-Surgical Complications & Product Recalls | -0.8% | Global | Short to Mid-term (2025-2029) |

| Lack of Skilled Orthopedic Surgeons in Certain Regions | -0.7% | Emerging Economies | Long-term (2025-2033) |

| Reimbursement Challenges and Healthcare Reforms | -0.6% | North America, Europe | Mid-term (2025-2029) |

Extremity Product Market Opportunities Analysis

The extremity product market presents significant opportunities through the expansion into emerging economies, particularly in Asia Pacific and Latin America. These regions are experiencing rapid economic growth, improving healthcare infrastructure, and an increasing middle-class population with greater access to healthcare services. The rising prevalence of lifestyle-related disorders and trauma cases, combined with a growing medical tourism sector, positions these markets as crucial avenues for future growth. Manufacturers can capitalize on these opportunities by tailoring their product offerings to meet local needs and developing effective distribution networks.

Another major opportunity lies in the continuous innovation and development of personalized implants and custom solutions. Advancements in imaging technologies, computational modeling, and 3D printing allow for the creation of patient-specific devices that offer superior fit, function, and potentially better long-term outcomes. This trend caters to the increasing demand for tailored medical treatments and opens new revenue streams for companies investing in advanced manufacturing capabilities. Furthermore, the integration of digital health technologies, such as AI-powered surgical planning, augmented reality (AR) for intra-operative guidance, and remote patient monitoring, offers avenues for enhancing surgical precision, optimizing patient recovery, and creating value-added services around extremity products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +1.2% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Development of Personalized & Custom Implants | +1.1% | Global, Developed Regions | Mid to Long-term (2025-2033) |

| Integration of Digital Technologies (AI, AR/VR) | +1.0% | Global | Mid to Long-term (2025-2033) |

| Focus on Outpatient & ASC Settings | +0.9% | North America, Europe | Mid-term (2025-2029) |

| Strategic Collaborations and Partnerships | +0.8% | Global | Short to Mid-term (2025-2029) |

Extremity Product Market Challenges Impact Analysis

The extremity product market faces significant challenges from intense competition and pervasive pricing pressures. A crowded market with numerous established and emerging players often leads to aggressive pricing strategies, particularly for generic or less differentiated products. This competitive environment puts downward pressure on profit margins for manufacturers and can force them to innovate constantly to justify premium pricing. Furthermore, the increasing demand from healthcare providers for cost-effective solutions and value-based care models compels manufacturers to balance innovation with affordability, which can be a difficult equilibrium to maintain.

Another considerable challenge is the potential for supply chain disruptions and the scarcity of raw materials. The global nature of manufacturing and distribution for medical devices makes the supply chain vulnerable to geopolitical events, natural disasters, and pandemics, as witnessed in recent years. Shortages of critical components or delays in logistics can severely impact production schedules and product availability, leading to lost sales and increased operational costs. Moreover, evolving healthcare reforms and complex reimbursement models in various countries pose a continuous challenge, requiring manufacturers to adapt their business strategies and engage proactively with policymakers to ensure favorable market access and sustainable revenue streams.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Pricing Pressures | -1.1% | Global | Long-term (2025-2033) |

| Supply Chain Disruptions & Raw Material Scarcity | -1.0% | Global | Short to Mid-term (2025-2029) |

| Evolving Healthcare Reforms & Reimbursement Models | -0.9% | North America, Europe | Mid to Long-term (2025-2033) |

| Counterfeit Products & Intellectual Property Theft | -0.8% | Emerging Economies | Long-term (2025-2033) |

| Physician Reluctance to Adopt New Technologies | -0.7% | Global | Mid-term (2025-2029) |

Extremity Product Market - Updated Report Scope

This report provides a comprehensive analysis of the global Extremity Product Market, offering in-depth insights into market size, growth trends, drivers, restraints, opportunities, and challenges. It covers a detailed forecast period from 2025 to 2033, building upon historical data from 2019 to 2023. The scope includes an exhaustive segmentation analysis by product type, application, material, and end-user, alongside a thorough regional assessment to identify key market dynamics and growth prospects across major geographical areas. The report also profiles leading market players, offering a competitive landscape analysis and strategic recommendations for stakeholders navigating this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.2 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | DePuy Synthes (Johnson & Johnson), Stryker Corporation, Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Arthrex, Inc., Integra LifeSciences Corporation, Acumed LLC, ConMed Corporation, Extremity Medical, LLC, Medtronic Plc, B. Braun Melsungen AG, DJO Global, Inc., Orthofix Medical Inc., Globus Medical, Inc., LimaCorporate S.p.A., MatOrtho Ltd., NuVasive, Inc., Paragon 28, Inc., OrthoPediatrics Corp., Enovis Corporation (formerly Colfax Corporation) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Extremity Product Market is comprehensively segmented to provide a granular view of its diverse components and dynamics. This segmentation facilitates a deeper understanding of specific product applications, material preferences, and end-user demands, enabling stakeholders to pinpoint high-growth areas and tailor their strategies accordingly. The market is primarily categorized by the anatomical region of application, further differentiated by the type of surgical intervention, the materials used in manufacturing, and the primary healthcare settings where these products are utilized. This multi-dimensional approach ensures a robust analysis of the market's structure and potential.

- By Product Type: Includes Upper Extremity Products (e.g., shoulder, elbow, wrist, hand implants) and Lower Extremity Products (e.g., foot and ankle, knee, hip components designed for extremity-specific conditions).

- By Application: Covers broad categories such as trauma (fracture fixation), reconstruction (joint replacement), sports injuries (ligament repair, arthroscopy), deformity correction, and other specialized applications.

- By Material: Encompasses various materials used in implant manufacturing, including metals (titanium, stainless steel), polymers (PEEK, UHMWPE), composites, and biologics (allografts, autografts, synthetic bone grafts).

- By End-User: Differentiates between primary healthcare facilities like hospitals, increasingly popular Ambulatory Surgical Centers (ASCs), specialized orthopedic clinics, and other outpatient settings.

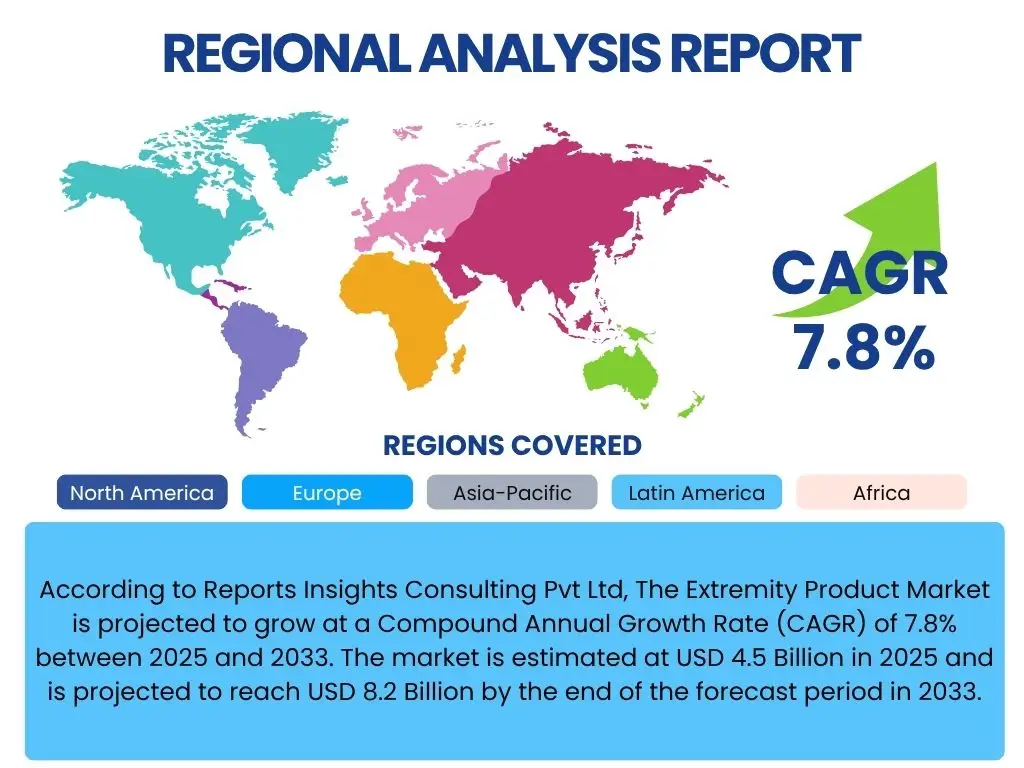

Regional Highlights

- North America: This region holds the largest market share in the extremity product market, driven by its advanced healthcare infrastructure, high adoption rate of technologically sophisticated products, increasing prevalence of orthopedic conditions, and favorable reimbursement policies. The presence of major market players and significant R&D investments also contributes to its dominance. The United States is a primary contributor to regional market growth due to its robust healthcare spending and high awareness of advanced treatment options.

- Europe: Europe represents the second-largest market for extremity products, characterized by an aging population, rising incidences of sports injuries, and well-established public and private healthcare systems. Countries like Germany, the United Kingdom, and France are key contributors, emphasizing a focus on innovative surgical techniques and high-quality medical devices. Strict regulatory standards ensure product safety and efficacy, fostering patient and physician confidence.

- Asia Pacific (APAC): The Asia Pacific region is projected to exhibit the fastest growth rate in the extremity product market during the forecast period. This growth is attributable to improving healthcare infrastructure, increasing healthcare expenditure, rising medical tourism, and a large patient pool with a growing awareness of modern orthopedic treatments. Countries such as China, India, Japan, and South Korea are key growth engines, offering significant opportunities for market expansion due to their large populations and economic development.

- Latin America: This region is an emerging market for extremity products, driven by improving economic conditions, expanding healthcare access, and a rising prevalence of orthopedic injuries. Brazil, Mexico, and Argentina are leading the growth, though challenges related to healthcare spending and infrastructure development persist. There is a growing demand for affordable and effective orthopedic solutions.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth in the extremity product market, fueled by increasing investment in healthcare infrastructure, growing medical tourism in certain countries (e.g., UAE, Saudi Arabia), and a rising awareness of orthopedic care. However, political instability and varying economic conditions across the region can impact market development and product adoption rates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Extremity Product Market.- DePuy Synthes (Johnson & Johnson)

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Smith & Nephew plc

- Arthrex, Inc.

- Integra LifeSciences Corporation

- Acumed LLC

- ConMed Corporation

- Extremity Medical, LLC

- Medtronic Plc

- B. Braun Melsungen AG

- DJO Global, Inc.

- Orthofix Medical Inc.

- Globus Medical, Inc.

- LimaCorporate S.p.A.

- MatOrtho Ltd.

- NuVasive, Inc.

- Paragon 28, Inc.

- OrthoPediatrics Corp.

- Enovis Corporation (formerly Colfax Corporation)

Frequently Asked Questions

Analyze common user questions about the Extremity Product market and generate a concise list of summarized FAQs reflecting key topics and concerns.What factors primarily drive the growth of the Extremity Product market?

The market's growth is largely driven by an aging global population, increasing incidence of sports injuries and musculoskeletal disorders, and continuous technological advancements in implant design and surgical techniques. Growing healthcare expenditure and awareness also contribute significantly.

How is artificial intelligence (AI) influencing the Extremity Product sector?

AI is transforming the sector by enabling more precise surgical planning, facilitating personalized implant design based on patient-specific anatomy, enhancing diagnostic accuracy through advanced image analysis, and assisting in robotic-aided surgeries for improved outcomes.

What are the main categories of extremity products available in the market?

Extremity products are broadly categorized by anatomical region (e.g., upper extremity including shoulder, elbow, wrist, hand; and lower extremity including foot, ankle, knee, hip for specific applications). They are used across applications like trauma, reconstruction, sports injury treatment, and deformity correction.

Which geographical regions offer the most significant growth opportunities for extremity product manufacturers?

The Asia Pacific region, particularly countries like China and India, presents the most substantial growth opportunities due to its large and growing patient population, improving healthcare infrastructure, increasing disposable incomes, and expanding medical tourism.

What are the key challenges faced by the Extremity Product market?

Major challenges include the high cost of advanced products and procedures, stringent regulatory approval processes, intense market competition leading to pricing pressures, potential supply chain disruptions, and the evolving landscape of healthcare reforms and reimbursement policies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted