Epoxy Adhesive Market

Epoxy Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705657 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

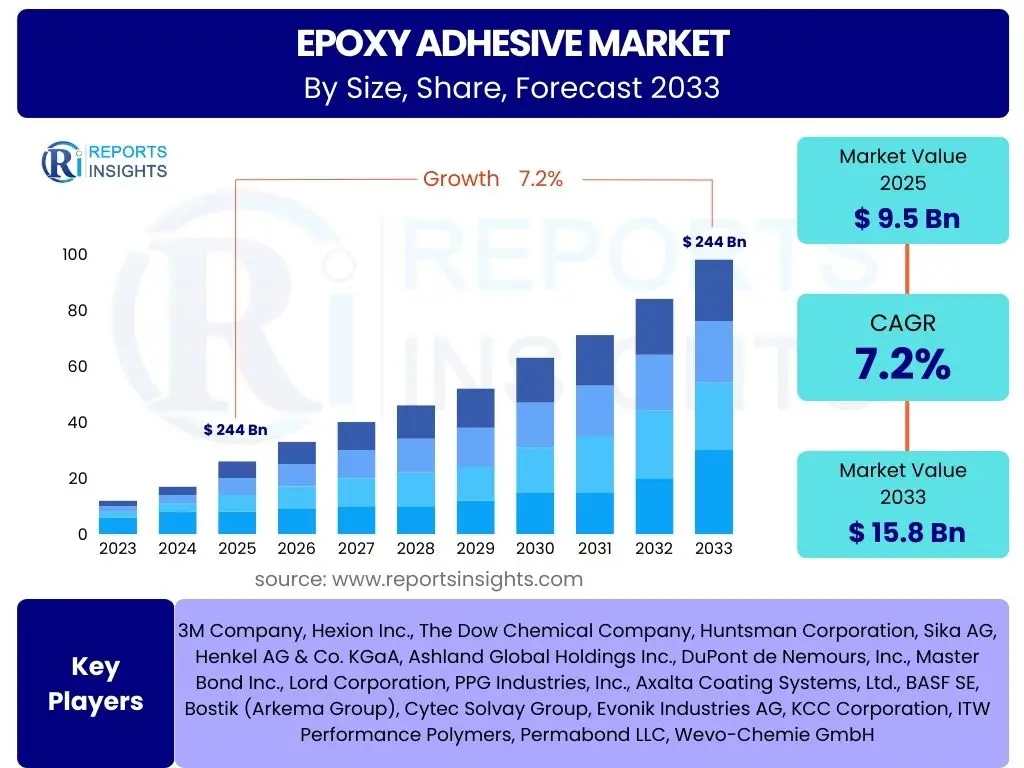

Epoxy Adhesive Market Size

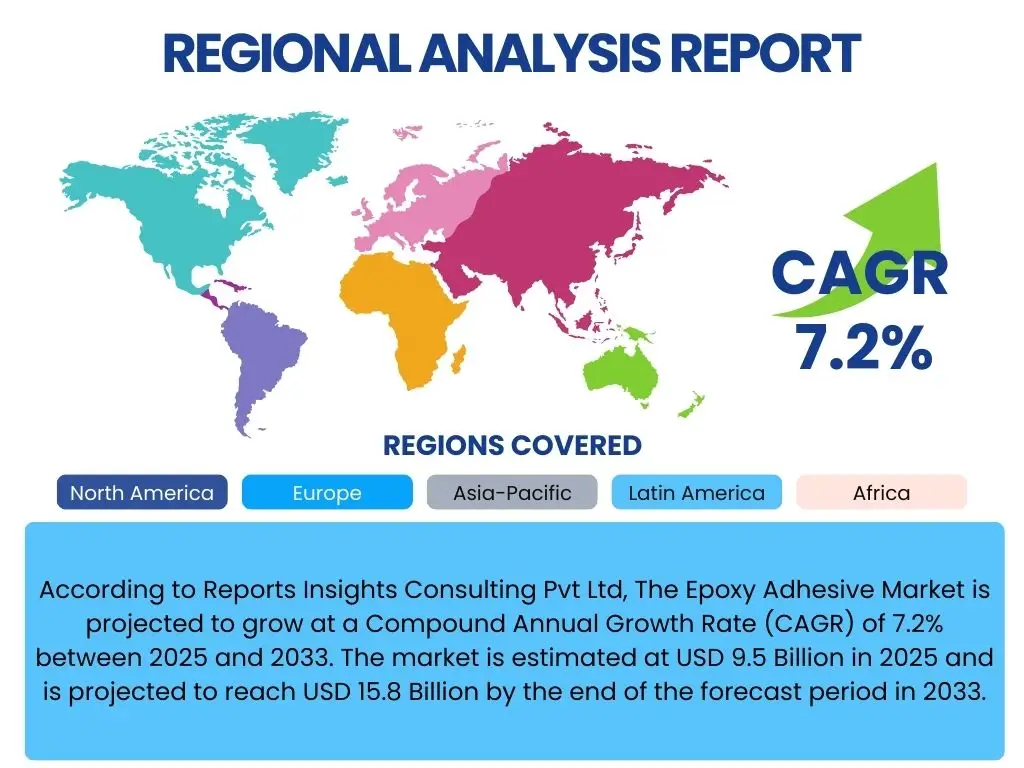

According to Reports Insights Consulting Pvt Ltd, The Epoxy Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 9.5 Billion in 2025 and is projected to reach USD 15.8 Billion by the end of the forecast period in 2033.

Key Epoxy Adhesive Market Trends & Insights

The epoxy adhesive market is experiencing significant transformation driven by evolving industrial demands and technological advancements. Key user inquiries often revolve around the adoption of lightweight materials in transportation, the surge in sustainable product development, and the expansion of high-performance applications in diverse sectors. These trends collectively underscore a market moving towards greater specialization, environmental consciousness, and efficiency in material bonding and protection.

Innovation remains a pivotal driver, with companies focusing on developing products that offer superior bond strength, thermal resistance, and chemical stability, catering to increasingly stringent performance requirements. The market is also witnessing a notable shift towards automation and precision application methods, improving manufacturing efficiency and reducing material waste. Furthermore, the increasing integration of smart materials and IoT-enabled solutions within end-use industries is influencing the design and application of next-generation epoxy adhesives.

- Increasing demand for lightweight materials in automotive and aerospace sectors.

- Growing adoption of bio-based and sustainable epoxy adhesive formulations.

- Expansion of applications in renewable energy, particularly wind turbine manufacturing.

- Development of high-performance and specialty adhesives for niche applications.

- Rising demand from the electronics and electrical industries for encapsulation and bonding.

- Shift towards automation and advanced dispensing systems in manufacturing.

- Focus on rapid-cure and low-VOC (Volatile Organic Compound) formulations.

AI Impact Analysis on Epoxy Adhesive

User questions concerning the impact of Artificial intelligence (AI) on the epoxy adhesive market frequently address how AI can optimize material design, enhance production processes, and improve quality control. AI's capacity for complex data analysis presents a transformative potential for accelerating research and development cycles, enabling predictive insights into material behavior and performance under various conditions. This leads to more efficient formulation and selection of epoxy adhesives tailored for specific industrial requirements.

Beyond R&D, AI significantly influences manufacturing and supply chain operations. Through machine learning algorithms, production lines can achieve higher levels of precision, predictive maintenance, and defect detection, minimizing waste and maximizing output. Furthermore, AI-driven analytics can optimize supply chain logistics, predicting demand fluctuations and ensuring timely raw material procurement, thereby mitigating risks associated with supply chain disruptions. The adoption of AI is poised to enhance the overall operational efficiency and competitiveness within the epoxy adhesive industry.

- Optimized material formulation and design through predictive modeling.

- Enhanced quality control and defect detection in manufacturing processes.

- Predictive maintenance for production equipment, reducing downtime.

- Improved supply chain management and demand forecasting.

- Accelerated research and development cycles for new adhesive solutions.

- Automation of complex application processes, ensuring precision.

Key Takeaways Epoxy Adhesive Market Size & Forecast

Analysis of common user questions reveals a keen interest in understanding the core implications of the epoxy adhesive market's growth trajectory and future outlook. The primary takeaway indicates robust and consistent growth, propelled by sustained demand across a diversified range of industrial applications. This expansion is not merely volume-driven but reflects a deep integration of epoxy adhesives as essential components in modern manufacturing, particularly in sectors prioritizing strength-to-weight ratios and durability.

Furthermore, a critical insight is the increasing emphasis on innovation and sustainability as non-negotiable elements for market success. Companies that invest in developing environmentally friendly formulations and high-performance specialty products are poised for significant competitive advantage. The forecast suggests that adaptability to evolving regulatory landscapes and a proactive approach to technological integration will be paramount for stakeholders aiming to capitalize on the long-term potential of the epoxy adhesive market.

- The epoxy adhesive market is set for sustained growth, driven by industrial expansion.

- Diversification of end-use applications is a key factor supporting market resilience.

- Innovation in product performance and sustainability are critical for future market leadership.

- Asia Pacific remains the fastest-growing region, presenting substantial investment opportunities.

- Strategic partnerships and mergers are likely to increase as companies seek to expand portfolios and market reach.

Epoxy Adhesive Market Drivers Analysis

The epoxy adhesive market is experiencing significant growth propelled by several influential factors. A primary driver is the accelerating demand from key end-use industries such as automotive, aerospace, construction, and electronics, which increasingly rely on advanced bonding solutions for performance and efficiency. The automotive sector, for instance, is progressively adopting epoxy adhesives for lightweighting initiatives, replacing traditional fasteners to improve fuel efficiency and structural integrity. Similarly, the expanding construction industry globally utilizes these adhesives for concrete repair, flooring, and structural bonding, driven by urbanization and infrastructure development projects.

Another crucial driver is the continuous technological advancements in epoxy formulations, leading to products with superior properties such as enhanced thermal resistance, chemical stability, and faster curing times. These innovations meet the stringent requirements of modern manufacturing processes and high-performance applications. The growing focus on renewable energy, particularly the wind energy sector, also significantly boosts demand for epoxy adhesives used in blade manufacturing and turbine assembly due to their excellent adhesion and durability under harsh conditions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Automotive & Aerospace Industries | +1.5% | Global, particularly North America, Europe, APAC | Short to Medium-Term |

| Growth in Building & Construction Sector | +1.2% | APAC, Middle East, Africa | Medium to Long-Term |

| Technological Advancements in Epoxy Formulations | +1.0% | Global | Short to Medium-Term |

| Rising Adoption in Electrical & Electronics Applications | +0.8% | APAC, North America | Medium-Term |

| Expansion of Renewable Energy Sector (e.g., Wind Energy) | +0.7% | Europe, North America, China | Medium to Long-Term |

Epoxy Adhesive Market Restraints Analysis

Despite robust growth, the epoxy adhesive market faces several notable restraints that could temper its expansion. One significant challenge is the volatility of raw material prices, particularly for petrochemical derivatives like bisphenol A and epichlorohydrin, which are essential components in epoxy resin production. Fluctuations in crude oil prices and supply chain disruptions can directly impact production costs, leading to price instability for end products and potentially eroding profit margins for manufacturers. This unpredictability makes long-term planning and consistent pricing strategies challenging.

Another key restraint involves stringent environmental regulations, particularly in developed regions like Europe and North America. These regulations often limit the permissible levels of Volatile Organic Compounds (VOCs) and other hazardous substances in adhesive formulations. Compliance requires significant investment in research and development to formulate eco-friendlier alternatives, such as water-based or solvent-free epoxy adhesives, which can sometimes come at a higher cost or with different performance characteristics that may not universally suit all applications. Furthermore, competition from alternative bonding solutions like polyurethane adhesives, acrylic adhesives, and mechanical fasteners also poses a competitive pressure, as these alternatives might offer specific advantages in terms of cost, curing time, or application ease for certain uses.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.0% | Global | Short to Medium-Term |

| Stringent Environmental Regulations | -0.8% | Europe, North America | Medium to Long-Term |

| Competition from Alternative Adhesives and Bonding Methods | -0.7% | Global | Medium-Term |

| Long Curing Times for Certain Epoxy Formulations | -0.5% | Global | Short to Medium-Term |

Epoxy Adhesive Market Opportunities Analysis

The epoxy adhesive market is poised for numerous growth opportunities driven by evolving industrial needs and a global push towards sustainable and advanced materials. A significant opportunity lies in the burgeoning demand for bio-based and sustainable epoxy adhesive solutions. As environmental consciousness grows and regulations become more stringent, there is an increasing preference for products derived from renewable resources and those with reduced environmental footprints. This trend encourages manufacturers to invest in green chemistry, offering a competitive edge and unlocking new market segments, particularly in eco-sensitive applications.

Another substantial opportunity is the continued expansion into emerging economies, particularly in the Asia Pacific, Latin American, and Middle East & Africa regions. Rapid industrialization, increasing infrastructure development, and growing manufacturing bases in these areas are fueling demand for high-performance adhesives across various sectors, including construction, automotive, and electronics. Furthermore, continuous innovation in high-performance and specialty applications, such as medical devices, flexible electronics, and advanced composites, presents avenues for market players to develop highly specialized products that command premium pricing and cater to niche, high-growth segments. The development of smart adhesives with self-healing or conductive properties also represents a promising frontier.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based & Sustainable Epoxy Adhesives | +1.5% | Global | Long-Term |

| Expansion into Emerging Economies | +1.2% | APAC, Latin America, MEA | Medium to Long-Term |

| Innovation in High-Performance & Specialty Applications | +1.0% | Global | Medium-Term |

| Growth in Medical and Healthcare Sector | +0.8% | North America, Europe | Long-Term |

Epoxy Adhesive Market Challenges Impact Analysis

The epoxy adhesive market faces several challenges that necessitate strategic responses from manufacturers and stakeholders. One significant challenge is the potential for supply chain disruptions, which can stem from geopolitical events, natural disasters, or global health crises. Such disruptions can severely impact the availability of critical raw materials, leading to production delays, increased costs, and ultimately affecting the timely supply of finished products to end-users. The reliance on a few key suppliers for specialized chemicals further exacerbates this vulnerability, making robust supply chain diversification and risk management strategies essential.

Another considerable challenge is the need for skilled labor for the precise application of certain epoxy adhesive systems, especially in highly specialized or automated industrial processes. Improper application can compromise bond strength, product integrity, and overall performance, leading to material waste and potential structural failures. Companies must invest in training and education for their workforce or develop user-friendly application systems to mitigate this issue. Additionally, the increasing complexity of product formulations to meet diverse industrial demands and stringent regulatory requirements adds to the manufacturing complexity, requiring significant R&D investment and adherence to evolving standards, which can be costly and time-consuming for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Potential for Supply Chain Disruptions | -1.0% | Global | Short-Term |

| Need for Skilled Labor in Application | -0.7% | Global | Medium-Term |

| High Initial Investment for Specialized Production Equipment | -0.6% | Global | Medium-Term |

| Disposal and Recycling Challenges for Epoxy Waste | -0.5% | Europe, North America | Long-Term |

Epoxy Adhesive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Epoxy Adhesive Market, encompassing historical data, current market dynamics, and future projections. It delivers detailed insights into market size, growth drivers, restraints, opportunities, and challenges, offering a holistic view of the industry landscape. The report segments the market by various types, forms, applications, and end-use industries, across key geographical regions, to provide granular understanding and actionable intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.5 Billion |

| Market Forecast in 2033 | USD 15.8 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Hexion Inc., The Dow Chemical Company, Huntsman Corporation, Sika AG, Henkel AG & Co. KGaA, Ashland Global Holdings Inc., DuPont de Nemours, Inc., Master Bond Inc., Lord Corporation, PPG Industries, Inc., Axalta Coating Systems, Ltd., BASF SE, Bostik (Arkema Group), Cytec Solvay Group, Evonik Industries AG, KCC Corporation, ITW Performance Polymers, Permabond LLC, Wevo-Chemie GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The epoxy adhesive market is comprehensively segmented to provide granular insights into its diverse components, allowing for a precise understanding of market dynamics across various categories. This segmentation enables detailed analysis of demand patterns, technological preferences, and regional consumption trends, facilitating strategic decision-making for market participants. The market is primarily divided based on type of epoxy resin, physical form, specific application areas, and the end-use industries served, each reflecting distinct market drivers and growth opportunities.

By dissecting the market into these segments, stakeholders can identify high-growth areas, emerging niche markets, and potential shifts in consumer or industrial preferences. For instance, the "By Type" segmentation reveals the prevalence and growth rates of different epoxy resin chemistries, while "By End-Use Industry" highlights the dominant sectors driving demand. This detailed breakdown ensures that the report captures the multifaceted nature of the epoxy adhesive market, offering a robust framework for strategic planning and investment analysis.

- By Type: Diglycidyl Ether of Bisphenol A (DGEBA), Diglycidyl Ether of Bisphenol F (DGEBF), Novolac, Aliphatic, Glycidyl Amine, Others

- By Form: Liquid, Paste, Film, Others

- By Application: Coating, Adhesion, Composites, Encapsulation, Flooring, Others

- By End-Use Industry: Building & Construction, Automotive, Aerospace & Defense, Wind Energy, Electrical & Electronics, Marine, Consumer Goods, Medical, Others

Regional Highlights

- North America: Characterized by significant demand from the automotive, aerospace, and electronics industries, driven by continuous innovation and adoption of high-performance materials. Stringent regulations are fostering a shift towards more sustainable and low-VOC formulations.

- Europe: A mature market with a strong emphasis on environmental regulations and sustainability, leading to increased adoption of bio-based and eco-friendly epoxy adhesives. Key industries include automotive, wind energy, and construction, particularly in Germany and the Nordic countries.

- Asia Pacific (APAC): The largest and fastest-growing market, propelled by rapid industrialization, urbanization, and robust growth in the building and construction, automotive, and electrical and electronics sectors, especially in China, India, and Southeast Asian countries.

- Latin America: Exhibiting emerging growth, primarily driven by infrastructure development projects and expanding manufacturing capabilities, particularly in countries like Brazil and Mexico, leading to increased demand for adhesives in construction and automotive.

- Middle East & Africa (MEA): Growing steadily due to significant investments in construction and infrastructure development, particularly in the UAE, Saudi Arabia, and Qatar, along with increasing industrialization in parts of Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Epoxy Adhesive Market.- 3M Company

- Hexion Inc.

- The Dow Chemical Company

- Huntsman Corporation

- Sika AG

- Henkel AG & Co. KGaA

- Ashland Global Holdings Inc.

- DuPont de Nemours, Inc.

- Master Bond Inc.

- Lord Corporation

- PPG Industries, Inc.

- Axalta Coating Systems, Ltd.

- BASF SE

- Bostik (Arkema Group)

- Cytec Solvay Group

- Evonik Industries AG

- KCC Corporation

- ITW Performance Polymers

- Permabond LLC

- Wevo-Chemie GmbH

Frequently Asked Questions

What is the primary growth driver for the epoxy adhesive market?

The primary growth driver is the surging demand from diverse end-use industries, including automotive, construction, aerospace, and electronics, which increasingly require high-performance, durable, and lightweight bonding solutions.

How do environmental regulations impact the epoxy adhesive market?

Environmental regulations, particularly regarding VOC emissions and hazardous substances, are driving manufacturers to develop more sustainable, bio-based, and low-VOC epoxy formulations, influencing product development and market adoption.

Which end-use industry holds the largest share in the epoxy adhesive market?

The building and construction industry typically accounts for the largest share in the epoxy adhesive market, followed closely by the automotive and electrical and electronics sectors, due to their extensive application requirements.

What are the key emerging opportunities in the epoxy adhesive market?

Key emerging opportunities include the development and adoption of bio-based and sustainable epoxy adhesives, expansion into high-growth emerging economies, and innovation in specialty applications such as medical devices and renewable energy components.

What are the main challenges faced by the epoxy adhesive market?

Major challenges include the volatility of raw material prices, potential supply chain disruptions, the need for skilled labor in precise application processes, and the increasing complexity of regulatory compliance and waste management.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted