Empty Capsule Market

Empty Capsule Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710377 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

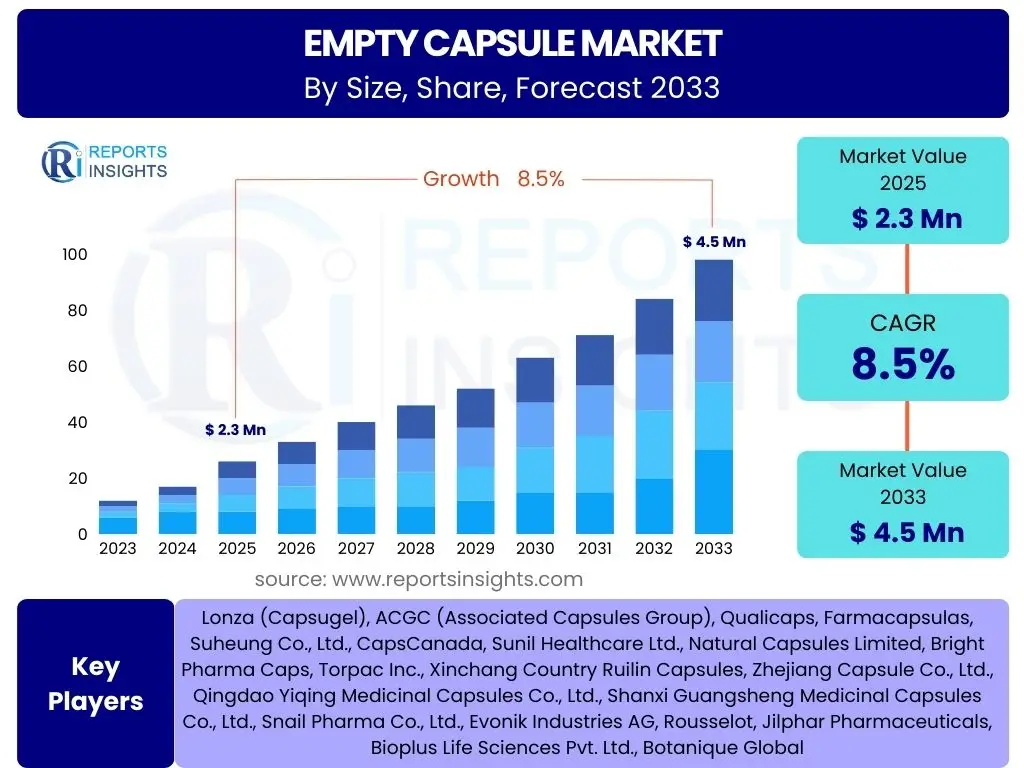

Empty Capsule Market Size

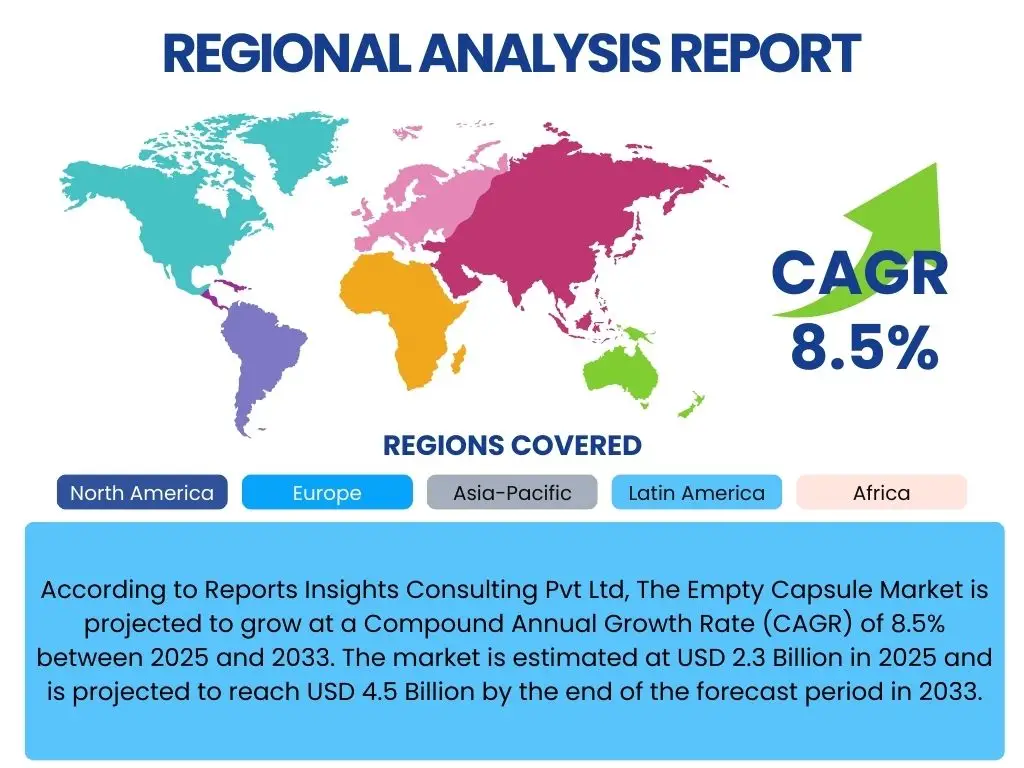

According to Reports Insights Consulting Pvt Ltd, The Empty Capsule Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 2.3 Billion in 2025 and is projected to reach USD 4.5 Billion by the end of the forecast period in 2033.

Key Empty Capsule Market Trends & Insights

The empty capsule market is undergoing significant transformation driven by evolving consumer preferences, technological advancements, and a heightened focus on health and wellness. A primary trend observed is the surging demand for non-gelatin, plant-based capsules, fueled by increasing vegetarian and vegan populations, religious dietary restrictions, and a growing consumer preference for natural and clean-label products. This shift extends beyond dietary choices, as formulators also seek alternatives that offer superior stability for moisture-sensitive active pharmaceutical ingredients (APIs).

Furthermore, the market is witnessing a rise in specialized capsule technologies designed for targeted drug delivery and improved bioavailability. Innovations such as enteric-coated capsules, liquid-filled hard capsules, and capsules with modified release characteristics are gaining traction. These advancements are crucial for addressing complex therapeutic requirements and enhancing patient compliance. The expansion of the nutraceutical and dietary supplements industry is also a significant driver, as manufacturers increasingly opt for capsules due to their ease of consumption, aesthetic appeal, and ability to mask unpleasant tastes.

Sustainability and environmental concerns are increasingly influencing product development and manufacturing processes within the empty capsule sector. Companies are investing in eco-friendly raw materials, sustainable production methods, and biodegradable packaging solutions to align with global environmental mandates and consumer expectations. Additionally, the adoption of advanced manufacturing techniques, including automation and real-time quality control, is enhancing production efficiency and product consistency, further shaping the competitive landscape of the empty capsule market.

- Shift towards plant-based and non-gelatin capsules driven by dietary and ethical considerations.

- Increasing adoption of specialized and functional capsules for targeted drug delivery and enhanced stability.

- Rapid expansion of the nutraceutical and dietary supplements sector boosting capsule demand.

- Focus on sustainable and eco-friendly capsule manufacturing and materials.

- Integration of advanced manufacturing technologies for improved efficiency and quality control.

AI Impact Analysis on Empty Capsule

Artificial Intelligence (AI) is poised to significantly impact the empty capsule market by revolutionizing various stages from raw material sourcing to quality assurance and supply chain management. Users frequently inquire about AI's potential to optimize manufacturing processes, improve product consistency, and accelerate the development of novel capsule materials. AI-driven predictive analytics can forecast demand fluctuations more accurately, enabling manufacturers to optimize production schedules and minimize waste, thereby enhancing operational efficiency and reducing costs.

In terms of research and development, AI algorithms can analyze vast datasets to identify suitable new polymers or excipients for capsule formulation, predict their compatibility with active ingredients, and even simulate their performance under various conditions. This capability drastically reduces the time and cost associated with traditional R&D cycles, fostering innovation in areas like extended-release capsules or those tailored for highly sensitive biologics. AI can also facilitate the design of capsules with specific dissolution profiles, crucial for advanced drug delivery systems.

Furthermore, AI's role in quality control is paramount. Machine vision systems powered by AI can detect microscopic defects or inconsistencies in capsule shells at high speeds and with greater accuracy than human inspection, ensuring stringent quality standards are met consistently. This not only enhances product safety and efficacy but also reduces batch rejection rates. Supply chain optimization through AI can lead to more resilient and transparent networks, mitigating risks associated with raw material procurement and distribution, which is a critical concern for global empty capsule manufacturers.

- AI-driven optimization of manufacturing processes to enhance efficiency and reduce waste.

- Accelerated research and development of novel capsule materials and formulations using predictive analytics.

- Enhanced quality control through AI-powered machine vision for defect detection.

- Improved supply chain resilience and transparency via AI-driven demand forecasting and logistics.

- Facilitation of personalized capsule design and targeted drug delivery systems.

Key Takeaways Empty Capsule Market Size & Forecast

The empty capsule market is positioned for robust and sustained growth through 2033, driven primarily by the global expansion of the pharmaceutical and nutraceutical industries. Users frequently seek to understand the primary growth catalysts and the long-term viability of specific capsule types. The forecast indicates a significant shift towards non-gelatin capsules, which are expected to capture a larger market share due to their versatility and alignment with evolving consumer preferences for vegetarian and vegan products. This segment's growth trajectory is steeper than traditional gelatin capsules, though gelatin will remain a foundational component of the market.

Regional dynamics play a crucial role in the market's trajectory, with emerging economies in Asia Pacific and Latin America demonstrating accelerated growth due to increasing healthcare expenditure, rising chronic disease prevalence, and expanding manufacturing capabilities. These regions are not only significant consumption hubs but also emerging production centers, influencing global supply chains and competitive strategies. Manufacturers are increasingly focusing on strategic partnerships and capacity expansion to capitalize on these burgeoning markets, which are expected to be key contributors to the overall market valuation.

Innovation in capsule materials and delivery technologies will be a pivotal factor in shaping market leadership. The development of advanced polymer-based capsules, enteric coatings, and modified-release formulations caters to complex therapeutic needs and offers opportunities for product differentiation. Investment in research and development for sustainable and functional capsules will be critical for companies aiming to maintain a competitive edge and address the evolving demands of both pharmaceutical companies and end-consumers. This continuous innovation will fuel new applications and further solidify the market's growth path.

- The empty capsule market is projected for significant growth, reaching USD 4.5 billion by 2033, driven by pharmaceutical and nutraceutical expansion.

- Non-gelatin capsules are a key growth segment, propelled by dietary preferences and superior formulation compatibility.

- Asia Pacific and Latin America are emerging as critical growth regions due to increasing healthcare investments and manufacturing expansion.

- Innovation in capsule materials and drug delivery technologies will be crucial for competitive advantage and market diversification.

- Sustainability and functional properties are central to future product development and market strategy.

Empty Capsule Market Drivers Analysis

The empty capsule market is significantly propelled by the consistent growth and evolving demands of the global pharmaceutical and nutraceutical industries. As these sectors expand, so does the need for efficient and effective drug delivery systems, with capsules being a preferred choice due to their ease of administration, dose accuracy, and ability to mask taste and odor. The increasing prevalence of chronic diseases globally necessitates a steady supply of oral medications, directly translating to higher demand for empty capsules. This fundamental driver is further amplified by the ongoing research and development in drug formulation, which often leverages capsule technology for novel drug delivery solutions.

Another major driver is the burgeoning consumer trend towards preventive healthcare and the widespread adoption of dietary supplements. Consumers are increasingly proactive about managing their health through vitamins, minerals, herbal extracts, and other nutraceuticals, many of which are delivered in capsule form. This trend is particularly strong in developed economies and is rapidly gaining traction in emerging markets, creating a sustained demand for empty capsules suitable for a wide range of supplement formulations. The convenience and perceived efficacy of encapsulated supplements contribute to their popularity, directly benefiting capsule manufacturers.

Furthermore, advancements in capsule technology, including the development of specialized materials and functional attributes, act as a key market driver. Innovations such as enteric-coated capsules for targeted release, liquid-filled hard capsules for improved bioavailability, and plant-derived capsules catering to specific dietary needs broaden the applicability of capsules across diverse therapeutic and wellness segments. These technological enhancements enable formulators to address complex drug delivery challenges and cater to specific patient populations, thereby expanding the overall market opportunities for empty capsules.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in pharmaceutical industry | +1.2% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Rise of nutraceuticals and dietary supplements | +1.0% | Global, strong in North America, Europe, APAC | Mid-to-long term (2025-2033) |

| Increasing demand for various drug delivery systems | +0.8% | Global | Mid-to-long term (2025-2033) |

| Growing preference for oral dosage forms | +0.7% | Global | Long-term (2025-2033) |

| Technological advancements in capsule materials | +0.6% | Global | Mid-to-long term (2025-2033) |

| Increasing geriatric population | +0.5% | Developed countries (North America, Europe, Japan) | Long-term (2025-2033) |

| Shift towards preventive healthcare | +0.4% | North America, Europe, emerging APAC | Mid-term (2025-2029) |

Empty Capsule Market Restraints Analysis

Despite robust growth, the empty capsule market faces several restraints that could potentially impede its expansion. One significant challenge is the volatility and fluctuating prices of raw materials, particularly for gelatin and its plant-based alternatives like HPMC. Gelatin prices are often subject to livestock market dynamics, while plant-based polymers can be affected by agricultural yields and processing costs. These unpredictable cost fluctuations directly impact manufacturing costs and profit margins, making it difficult for capsule manufacturers to maintain stable pricing and long-term planning.

Another key restraint is the stringent regulatory landscape governing pharmaceutical and nutraceutical products. Empty capsules, as components of these products, must comply with rigorous quality standards, pharmacopoeial requirements, and good manufacturing practices (GMP) across different regions. Achieving and maintaining these certifications requires significant investment in quality control, documentation, and facility upgrades, which can be particularly challenging for smaller manufacturers. Any deviation can lead to product recalls, reputational damage, and legal penalties, acting as a barrier to market entry and expansion.

Furthermore, the availability of alternative drug delivery systems poses a competitive restraint to the empty capsule market. While capsules are highly popular, tablets, softgels, liquid formulations, and parenteral routes offer viable alternatives depending on the active ingredient, therapeutic indication, and patient preference. The continuous innovation in these alternative delivery methods, such as orally disintegrating tablets or transdermal patches, can divert a portion of the market demand that might otherwise be served by capsules. This ongoing competition necessitates constant innovation from capsule manufacturers to maintain their market share.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw material price fluctuations | -0.5% | Global | Mid-to-long term (2025-2033) |

| Stringent regulatory landscape | -0.4% | North America, Europe (highly regulated regions) | Long-term (2025-2033) |

| Competition from alternative delivery systems | -0.3% | Global | Long-term (2025-2033) |

| High capital investment for manufacturing and R&D | -0.2% | Global | Long-term (2025-2033) |

| Stability issues for certain moisture-sensitive formulations | -0.1% | Global | Mid-term (2025-2029) |

Empty Capsule Market Opportunities Analysis

The empty capsule market is ripe with opportunities, primarily driven by the increasing demand for specialized and customized drug delivery solutions. One significant avenue lies in the continued innovation and expansion of plant-based and other non-gelatin capsule materials. As consumer preferences for vegetarian, vegan, and clean-label products grow globally, there is an escalating market for HPMC, pullulan, and other novel plant-derived capsules. This presents an opportunity for manufacturers to diversify their product portfolios, catering to specific dietary restrictions and religious requirements, while also addressing concerns regarding animal-derived products.

Another compelling opportunity emerges from the rapid growth of the personalized medicine and custom compounding sectors. These areas require flexible, high-quality empty capsules that can be filled with precise dosages for individual patient needs. Manufacturers capable of providing small batch sizes, a variety of colors, and customizable printing options will find a significant niche in this evolving market. Furthermore, the development of functional capsules with advanced features like enteric protection, extended release, or targeted delivery mechanisms offers substantial growth potential, allowing for the encapsulation of complex and sensitive active ingredients more effectively.

Geographic expansion into emerging economies, particularly in Asia Pacific, Latin America, and the Middle East and Africa, represents a substantial market opportunity. These regions are experiencing significant growth in healthcare infrastructure, pharmaceutical manufacturing capabilities, and a rising middle class with increased access to medicines and supplements. Localizing manufacturing capabilities, forming strategic partnerships, and understanding regional regulatory nuances can enable capsule manufacturers to tap into these underserved yet rapidly expanding markets. The growing demand for over-the-counter (OTC) medications and nutraceuticals in these regions further strengthens this opportunity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of plant-based and non-gelatin capsules | +1.0% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Expansion in emerging economies | +0.9% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Customization for personalized medicine and compounding | +0.8% | North America, Europe | Mid-to-long term (2025-2033) |

| Innovation in functional and specialized capsules | +0.7% | Global | Mid-to-long term (2025-2033) |

| Growing demand for clean-label and sustainable products | +0.6% | North America, Europe | Mid-term (2025-2029) |

| Increased focus on contract manufacturing services | +0.5% | Global | Mid-term (2025-2029) |

Empty Capsule Market Challenges Impact Analysis

The empty capsule market faces several significant challenges that require strategic navigation from manufacturers. One primary concern is maintaining consistent product quality and ensuring compliance with a complex web of international and regional regulatory standards. Any inconsistency in capsule dimensions, dissolution rates, or material composition can lead to rejection of entire batches by pharmaceutical clients, resulting in substantial financial losses and reputational damage. The challenge is amplified by the diverse requirements for different types of capsules and the stringent testing protocols mandated by regulatory bodies like the FDA or EMA.

Another critical challenge is managing supply chain disruptions and ensuring a stable, cost-effective supply of raw materials. The global nature of the empty capsule industry means that geopolitical events, trade disputes, natural disasters, or pandemics can severely impact the availability and pricing of key ingredients such as gelatin, HPMC, or colorants. Manufacturers must invest in robust supply chain resilience strategies, including diversification of suppliers, establishing regional hubs, and leveraging advanced inventory management systems to mitigate these risks and ensure uninterrupted production.

Furthermore, the empty capsule market is characterized by intense competition among a few large, established players and numerous smaller regional manufacturers. This competitive pressure often leads to pricing pressures, making it difficult for companies to maintain healthy profit margins while simultaneously investing in research and development for innovation. Differentiation becomes challenging, requiring companies to focus on niche markets, specialized capsule technologies, or superior customer service to stand out. Continuous investment in advanced manufacturing technologies and automation is also a capital-intensive challenge for many players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining quality control and consistency | -0.4% | Global | Long-term (2025-2033) |

| Supply chain vulnerabilities and disruptions | -0.3% | Global | Mid-term (2025-2029) |

| Intense market competition and pricing pressures | -0.2% | Global | Long-term (2025-2033) |

| High capital investment for advanced manufacturing | -0.2% | Global | Long-term (2025-2033) |

| Environmental and sustainability concerns in production | -0.1% | Europe, North America | Mid-term (2025-2029) |

Empty Capsule Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Empty Capsule Market, offering a detailed overview of its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges influencing the industry landscape. It also delves into key market trends, the impact of emerging technologies like AI, and a meticulous segmentation analysis to provide a holistic understanding for stakeholders and strategic decision-makers.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.3 Billion |

| Market Forecast in 2033 | USD 4.5 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Lonza (Capsugel), ACGC (Associated Capsules Group), Qualicaps, Farmacapsulas, Suheung Co., Ltd., CapsCanada, Sunil Healthcare Ltd., Natural Capsules Limited, Bright Pharma Caps, Torpac Inc., Xinchang Country Ruilin Capsules, Zhejiang Capsule Co., Ltd., Qingdao Yiqing Medicinal Capsules Co., Ltd., Shanxi Guangsheng Medicinal Capsules Co., Ltd., Snail Pharma Co., Ltd., Evonik Industries AG, Rousselot, Jilphar Pharmaceuticals, Bioplus Life Sciences Pvt. Ltd., Botanique Global |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The empty capsule market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of demand dynamics across various product types, applications, and end-use industries. This segmentation helps identify specific growth pockets and market opportunities, highlighting the evolving preferences of consumers and the strategic focus areas for manufacturers. The analysis considers both established and emerging segments, reflecting the market's continuous innovation and adaptation to new trends and regulatory landscapes.

- By Type: This segment is crucial, differentiating between traditional gelatin capsules (hard and soft) and the rapidly expanding non-gelatin alternatives. Non-gelatin capsules include HPMC (hydroxypropyl methylcellulose), pullulan, starch, and PVA capsules, which cater to specific dietary, religious, and stability requirements.

- By Application: The market is segmented based on the primary use cases for empty capsules. Pharmaceuticals represent the largest application, encompassing a wide range of therapeutic areas such as antibiotics, cardiac therapy, anti-inflammatory drugs, and an increasing portion of vitamins and dietary supplements. Nutraceuticals form another significant and growing application, including herbal supplements, probiotics, and sports nutrition. Cosmetics and other industrial applications also contribute to this segment.

- By End-use: This segmentation focuses on the key consumers of empty capsules. Contract Manufacturing Organizations (CMOs) are major end-users, providing services to pharmaceutical and nutraceutical companies. Pharmaceutical companies and nutraceutical companies directly procure capsules for their in-house production. Cosmetic companies and research & academic institutes also constitute a smaller but vital part of the end-use landscape.

Regional Highlights

- North America: This region holds a significant share of the empty capsule market, driven by a well-established pharmaceutical industry, high consumer awareness regarding dietary supplements, and robust research and development activities. The presence of major pharmaceutical companies and a strong trend towards personalized medicine and clean-label products further propels market growth.

- Europe: Europe is another key market, characterized by stringent regulatory standards, a mature pharmaceutical sector, and increasing demand for vegetarian and vegan capsules. Countries like Germany, France, and the UK are prominent contributors due to high healthcare expenditure and a focus on advanced drug delivery systems.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by increasing healthcare spending, a burgeoning population, and the expansion of domestic pharmaceutical and nutraceutical manufacturing capabilities in countries such as China, India, and Japan. The rising prevalence of chronic diseases and improving economic conditions are key growth drivers.

- Latin America: This region is experiencing steady growth, attributed to improving healthcare infrastructure, increasing access to generic drugs, and a growing consumer interest in dietary supplements. Brazil and Mexico are leading the market in this region.

- Middle East and Africa (MEA): The MEA market is gradually expanding, driven by increasing government investments in healthcare, a rising incidence of lifestyle diseases, and growing pharmaceutical production capabilities in countries like Saudi Arabia and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Empty Capsule Market.- Lonza (Capsugel)

- ACGC (Associated Capsules Group)

- Qualicaps

- Farmacapsulas

- Suheung Co., Ltd.

- CapsCanada

- Sunil Healthcare Ltd.

- Natural Capsules Limited

- Bright Pharma Caps

- Torpac Inc.

- Xinchang Country Ruilin Capsules

- Zhejiang Capsule Co., Ltd.

- Qingdao Yiqing Medicinal Capsules Co., Ltd.

- Shanxi Guangsheng Medicinal Capsules Co., Ltd.

- Snail Pharma Co., Ltd.

- Evonik Industries AG

- Rousselot

- Jilphar Pharmaceuticals

- Bioplus Life Sciences Pvt. Ltd.

- Botanique Global

Frequently Asked Questions

Analyze common user questions about the Empty Capsule market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary types of empty capsules available in the market?

The primary types of empty capsules include gelatin capsules, derived from animal collagen, and non-gelatin capsules, which are typically plant-based, such as HPMC (hydroxypropyl methylcellulose) and pullulan capsules. Each type offers distinct advantages for specific applications and dietary preferences.

How is the empty capsule market segmented by application?

The empty capsule market is segmented by application primarily into pharmaceuticals and nutraceuticals. Pharmaceuticals encompass a wide range of drug formulations for various therapeutic areas, while nutraceuticals include dietary supplements, vitamins, minerals, and herbal extracts for health and wellness.

What factors are driving the growth of non-gelatin capsules?

The growth of non-gelatin capsules is driven by increasing vegetarian and vegan populations, religious dietary restrictions, a rising consumer preference for natural and clean-label products, and their suitability for moisture-sensitive active pharmaceutical ingredients (APIs) due to lower moisture content.

Which geographical region is expected to witness the fastest growth in the empty capsule market?

The Asia Pacific (APAC) region is projected to experience the fastest growth in the empty capsule market. This growth is attributed to expanding pharmaceutical and nutraceutical industries, increasing healthcare expenditure, and a rising population with greater access to medicines and supplements in countries like China and India.

What impact does AI have on the empty capsule manufacturing process?

AI significantly impacts empty capsule manufacturing by optimizing production efficiency, enhancing quality control through machine vision systems for defect detection, and accelerating the development of novel capsule materials and formulations. It also aids in more accurate demand forecasting and supply chain management.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted