EMI Shielding Market

EMI Shielding Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708841 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

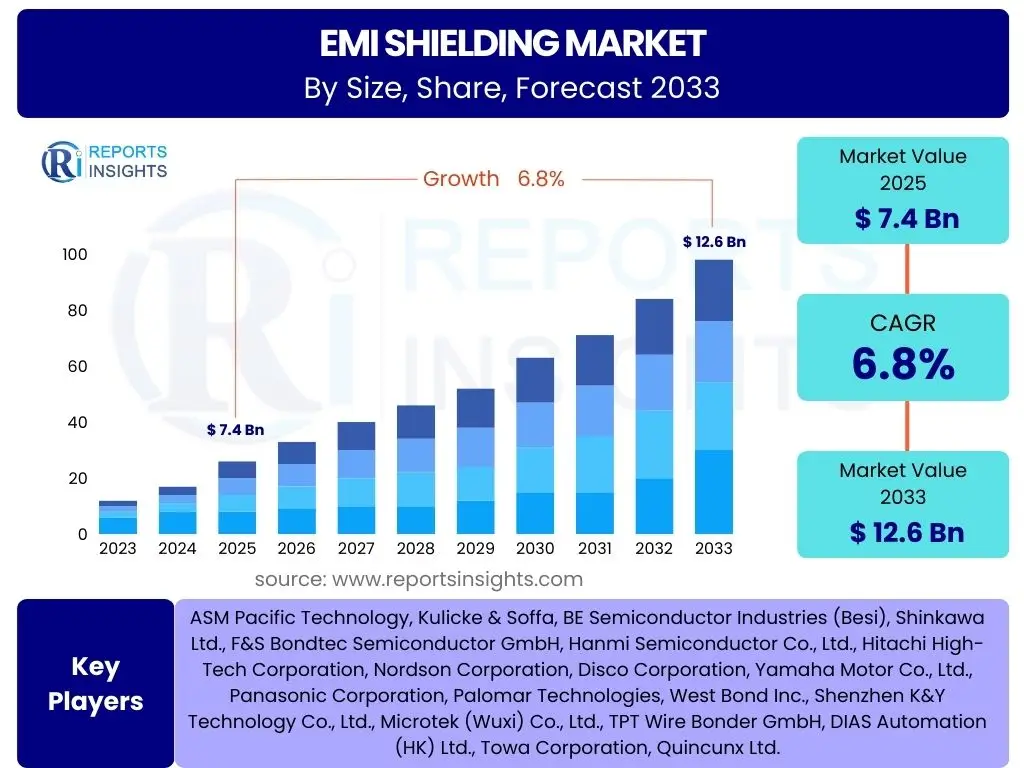

EMI Shielding Market Size

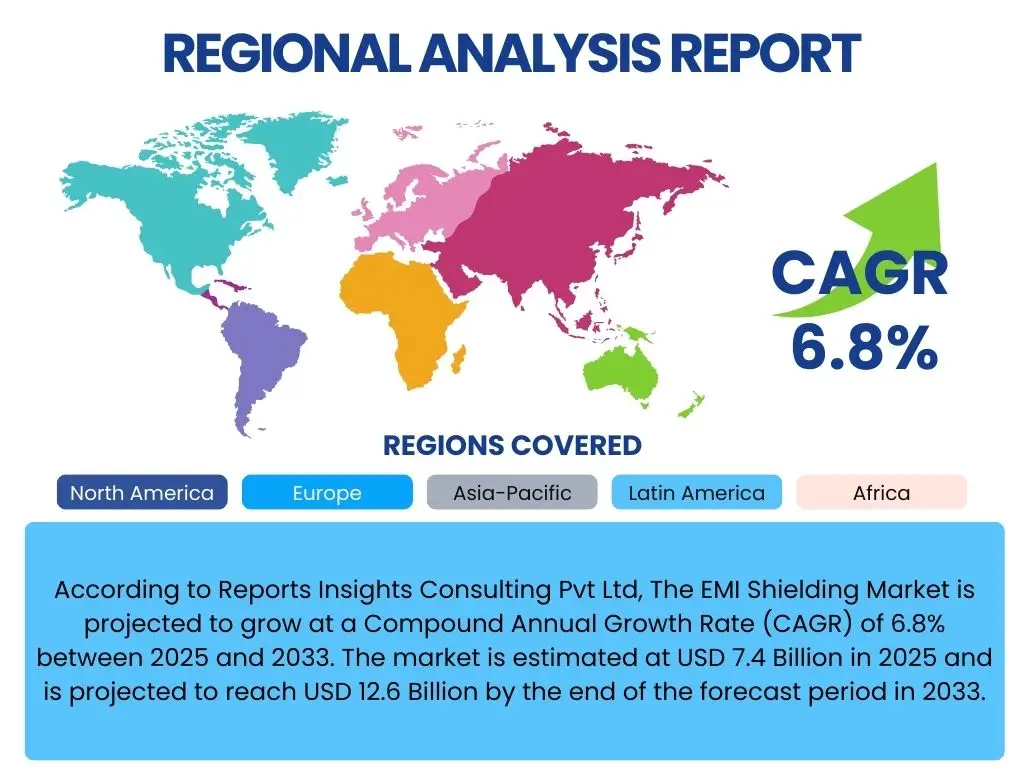

According to Reports Insights Consulting Pvt Ltd, The EMI Shielding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 7.4 Billion in 2025 and is projected to reach USD 12.6 Billion by the end of the forecast period in 2033.

Key EMI Shielding Market Trends & Insights

The market for EMI shielding is currently experiencing a transformative period, driven by the pervasive integration of electronic components across virtually all sectors. A primary trend involves the relentless push towards miniaturization of electronic devices, which intensifies the challenge of managing electromagnetic interference within confined spaces. This trend necessitates the development of advanced shielding solutions that are thin, lightweight, and highly effective, driving innovation in material science and application techniques to accommodate increasingly compact designs.

Furthermore, the global rollout of 5G infrastructure and the rapid expansion of the Internet of Things (IoT) ecosystem are significantly contributing to the market's dynamism. These technologies rely on high-frequency signals and dense networks of interconnected devices, increasing the potential for electromagnetic compatibility (EMC) issues. Consequently, demand for robust EMI shielding to ensure signal integrity, device reliability, and compliance with increasingly stringent regulatory standards is escalating. The electrification of the automotive industry, particularly the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), also represents a powerful trend, as these applications require sophisticated shielding to protect sensitive onboard electronics from intense electromagnetic fields.

Another critical insight is the shift towards customized and integrated shielding solutions. As design complexity grows, off-the-shelf shielding components are often insufficient. Manufacturers are increasingly seeking tailored solutions that can be seamlessly integrated into specific product designs, offering optimal performance without compromising space or aesthetics. This trend fosters collaboration between shielding material providers and original equipment manufacturers (OEMs), leading to the co-development of application-specific materials and designs. Environmental considerations are also shaping trends, with a growing emphasis on sustainable and recyclable shielding materials, influencing research and development efforts across the industry.

- Accelerated miniaturization of electronic devices and components.

- Rapid global deployment of 5G technology and widespread IoT adoption.

- Electrification of the automotive industry and expansion of ADAS.

- Increasing demand for high-performance, lightweight, and thin shielding materials.

- Growing focus on customized, integrated, and application-specific shielding solutions.

- Stricter electromagnetic compatibility (EMC) regulations and standards.

- Emphasis on environmentally friendly and sustainable shielding solutions.

AI Impact Analysis on EMI Shielding

Artificial intelligence (AI) is poised to significantly transform the EMI shielding market by enhancing design, material development, and manufacturing processes. AI algorithms can analyze vast datasets from electromagnetic simulations and test results, enabling engineers to predict EMI patterns with greater accuracy and optimize shielding designs for maximum effectiveness in minimal space. This capability is particularly crucial as devices become more complex and densely packed, where traditional trial-and-error methods are time-consuming and costly. AI-driven predictive modeling can simulate various material combinations and geometries, accelerating the development of novel shielding solutions.

Beyond design, AI offers substantial improvements in material innovation and manufacturing efficiency. Machine learning techniques can be applied to discover new conductive polymers, composite materials, or nanofiller-enhanced solutions with superior shielding properties. By rapidly iterating through material compositions and predicting their performance characteristics, AI can significantly shorten the material development lifecycle. In manufacturing, AI-powered systems can monitor production lines for defects in shielding application, ensure consistent quality, and optimize processes for material waste reduction and enhanced throughput, leading to more cost-effective and reliable shielding products while minimizing human error.

While AI provides powerful tools for EMI shielding, it also presents challenges. The proliferation of AI-powered devices, especially those with high-speed processors and communication modules, inherently generates more electromagnetic noise. This creates a paradox where AI, while helping to design better shielding, concurrently increases the overall EMI landscape, thereby amplifying the need for even more sophisticated and adaptive shielding solutions. Furthermore, securing AI systems from external EMI is critical to their reliable operation, highlighting a dual role for EMI shielding in protecting AI and managing the interference it generates, ensuring both functional integrity and data security.

- Optimization of EMI shielding design through advanced simulation and predictive analytics.

- Acceleration of novel material discovery and development using machine learning.

- Enhancement of manufacturing processes for improved efficiency and quality control.

- Prediction of electromagnetic compatibility issues in complex electronic systems.

- Increased complexity of EMI landscape due to proliferation of AI-powered devices.

- Requirement for robust shielding to protect sensitive AI hardware from external interference.

Key Takeaways EMI Shielding Market Size & Forecast

The EMI Shielding market is on a robust growth trajectory, primarily driven by the relentless advancement and proliferation of electronic devices across nearly every industry sector. This growth is intrinsically linked to the increasing demand for seamless connectivity, higher processing speeds, and the miniaturization of components. The forecast highlights a sustained expansion, indicating that EMI shielding is no longer merely an ancillary component but a critical enabler for the reliable and efficient operation of modern electronics, underscoring its foundational importance in the digital age.

Strategic implications derived from this forecast suggest a growing imperative for innovation in material science and application techniques. As electromagnetic environments become more complex and regulations more stringent, companies that invest in developing advanced, lightweight, and customizable shielding solutions are poised to capture significant market share. The market's resilience, even amidst global economic fluctuations, demonstrates its essential nature for diverse applications ranging from consumer electronics to highly sensitive aerospace and medical equipment, highlighting a diversified demand base.

Furthermore, the significant compound annual growth rate projected indicates lucrative opportunities for new entrants and established players alike. The market demands continuous adaptation to evolving technological landscapes, such as the rollout of 5G and the surge in electric vehicle adoption, which necessitate specialized shielding solutions. This forecast serves as a critical guide for investment decisions, product development strategies, and market positioning, emphasizing the long-term value and strategic importance of electromagnetic interference mitigation in technological advancement.

- Robust market growth driven by pervasive electronic device proliferation.

- Criticality of EMI shielding for ensuring reliable and efficient electronic operations.

- Significant opportunities for innovation in advanced materials and customized solutions.

- Diversified demand across key industries including consumer electronics, automotive, and healthcare.

- Strategic importance of EMI shielding in enabling next-generation technologies like 5G and EVs.

EMI Shielding Market Drivers Analysis

The EMI Shielding market is propelled by several potent forces, primarily stemming from the increasing sophistication and ubiquity of electronic devices. The global digital transformation has led to an unprecedented demand for connected devices, high-speed data transmission, and compact electronic assemblies. These advancements, while beneficial, inherently increase the generation of electromagnetic interference, thereby escalating the need for effective shielding solutions to maintain device integrity and performance. Stringent regulatory mandates for electromagnetic compatibility (EMC) further reinforce this demand, making EMI shielding a compliance necessity rather than just a performance enhancement.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Consumer Electronics & IoT Devices | +1.5% | Global | Short to Mid-term |

| Growth in Automotive Electronics & EVs | +1.2% | North America, Europe, Asia Pacific | Mid-term |

| Expansion of 5G Technology & Telecommunications | +1.0% | Global | Short to Mid-term |

| Increasing Demand from Healthcare & Medical Devices | +0.8% | North America, Europe | Mid-term |

| Stringent EMI/EMC Regulations | +0.7% | Global | Long-term |

EMI Shielding Market Restraints Analysis

Despite robust growth drivers, the EMI Shielding market faces several significant restraints that could temper its expansion. One primary challenge is the high cost associated with advanced shielding materials and complex application processes, particularly for high-performance or customized solutions. This cost factor can deter adoption in price-sensitive applications or smaller-scale productions. Additionally, the intricate design and integration of shielding solutions into increasingly miniaturized and densely packed electronic devices present considerable engineering hurdles, requiring specialized expertise and adding to development timelines and expenses. The volatility of raw material prices further introduces uncertainty, impacting manufacturing costs and profitability across the value chain.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Shielding Materials | -0.6% | Global | Short to Mid-term |

| Design Complexity & Integration Challenges | -0.5% | North America, Europe, Asia Pacific | Mid-term |

| Volatility in Raw Material Prices | -0.4% | Global | Short-term |

| Limited Awareness and Adoption in Smaller Enterprises | -0.3% | Asia Pacific, Latin America, MEA | Mid-term |

EMI Shielding Market Opportunities Analysis

The EMI Shielding market is ripe with opportunities for innovation and expansion, particularly driven by advancements in material science and the emergence of new high-growth applications. The continuous demand for lighter, thinner, and more effective shielding solutions opens avenues for the development of novel conductive polymers, composites, and nanostructured materials. Furthermore, the burgeoning aerospace and defense sectors, with their stringent performance and reliability requirements, offer significant untapped potential for high-performance, custom-engineered shielding solutions. The relentless trend towards miniaturization in consumer electronics necessitates highly customized, integrated shielding components, presenting a constant stream of bespoke market opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced & Lightweight Materials | +1.0% | Global | Mid to Long-term |

| Growing Demand in Aerospace & Defense Sectors | +0.9% | North America, Europe | Mid-term |

| Miniaturization of Electronics Driving Custom Solutions | +0.8% | Global | Short to Mid-term |

| Untapped Potential in Developing Economies | +0.7% | Asia Pacific, Latin America | Long-term |

EMI Shielding Market Challenges Impact Analysis

The EMI Shielding market faces several critical challenges that require continuous innovation and strategic adaptation from industry participants. A significant hurdle is the escalating difficulty in achieving high shielding effectiveness within increasingly compact and complex electronic designs, where space constraints limit material thickness and application area. Additionally, the growing focus on environmental sustainability and stricter regulations regarding material composition (e.g., REACH, RoHS) compel manufacturers to develop eco-friendly shielding solutions, often requiring substantial R&D investments and presenting compliance complexities. The rapid pace of technological obsolescence in the electronics industry also pressures shielding providers to constantly innovate and adapt their product offerings to new device generations and evolving interference profiles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving High Shielding Effectiveness in Compact Designs | -0.7% | Global | Mid-term |

| Environmental Regulations on Shielding Materials | -0.6% | Europe, North America | Long-term |

| Rapid Technological Obsolescence | -0.5% | Global | Short-term |

| Supply Chain Disruptions and Material Shortages | -0.4% | Global | Short-term |

EMI Shielding Market - Updated Report Scope

This comprehensive market report offers an in-depth analysis of the EMI Shielding market, providing a detailed overview of its current landscape, historical performance, and future growth projections. The scope encompasses a thorough examination of market size and forecast, key trends, drivers, restraints, opportunities, and challenges influencing industry dynamics. Furthermore, the report delves into a granular segmentation analysis across various parameters, offering critical insights into regional market variations and the competitive strategies of leading market participants to provide a holistic understanding for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.4 Billion |

| Market Forecast in 2033 | USD 12.6 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Laird Performance Materials (a DuPont Business), Chomerics (a Parker Hannifin Company), 3M Company, Henkel AG & Co. KGaA, PPG Industries Inc., Schlegel Electronic Materials (a division of Bekaert), TDK Corporation, KGS Electronics, Kitagawa Industries Co., Ltd., W. L. Gore & Associates, Inc., Tecknit (A company of Parker Hannifin), Kemtron Ltd., ETS-Lindgren, Tech-Etch, Inc., Leader Tech, Inc., Marian Inc., Spira Manufacturing Corporation, Guangzhou Techwin Electronic Co., Ltd., Shenzhen Jinke Shielding Material Co., Ltd., Hitachi Metals, Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The EMI Shielding market is meticulously segmented across various critical parameters to provide a granular view of its diverse landscape and growth opportunities. This detailed breakdown by material, end-use industry, product type, and application allows for a precise understanding of demand patterns, technological preferences, and market saturation levels across different niches. Such segmentation is instrumental in identifying key revenue streams, emerging application areas, and strategic investment opportunities for market participants seeking to optimize their product portfolios and market penetration strategies.

Understanding these segments reveals that each category presents unique challenges and opportunities. For instance, material segmentation highlights the shift towards advanced composites and conductive polymers for lightweight solutions, while end-use industry analysis underscores the burgeoning demand from automotive and telecommunications sectors. Product type segmentation distinguishes between various shielding forms, such as gaskets for sealing and coatings for surface protection, reflecting diverse functional requirements. The application-specific analysis provides a direct link between shielding solutions and the specific electronic devices or systems they protect, illustrating the market's breadth and depth.

This comprehensive segmentation not only aids in competitive analysis but also supports strategic planning by offering insights into regional market nuances. For example, high growth in consumer electronics in Asia Pacific would emphasize demand for specific material types and application methods tailored to mass production and cost-efficiency. Conversely, the stringent requirements of the aerospace and defense sectors in North America and Europe would highlight a demand for high-performance, certified shielding solutions. Thus, market segmentation is a foundational element for informed decision-making within the EMI shielding industry.

- By Material: Conductive Coatings & Paints, Conductive Polymers, EMI Shielding Tapes & Laminates, Metal Shielding (e.g., Copper, Aluminum, Steel), Fabric over Foam, Ferrite.

- By End-Use Industry: Consumer Electronics, Telecommunications & IT, Automotive, Aerospace & Defense, Healthcare & Medical, Industrial, Others (e.g., Marine, Scientific Research).

- By Product Type: EMI Shielding Gaskets, EMI Shielding Cans & Enclosures, EMI Filters, Shielding Laminates & Foils, Conductive Coatings, Grounding & Contact Products, Absorbers.

- By Application: Smartphones, Tablets, Laptops, Wearable Devices, Electric Vehicles (EVs), Advanced Driver-Assistance Systems (ADAS), Network Infrastructure, Medical Imaging Equipment, Diagnostic Devices, Industrial Control Systems, Data Centers, Communication Systems, Military Radar Systems.

Regional Highlights

The global EMI Shielding market exhibits diverse growth dynamics and regional specificities, influenced by technological adoption, industrial development, and regulatory frameworks. North America and Europe, as established markets, are characterized by high demand from the aerospace and defense, medical, and advanced automotive sectors, coupled with stringent EMC regulations. These regions are also at the forefront of R&D for advanced shielding materials and custom solutions, driven by a strong innovation ecosystem and significant investments in high-tech industries.

The Asia Pacific (APAC) region stands out as the fastest-growing market, propelled by its dominance in consumer electronics manufacturing, rapid expansion of telecommunications infrastructure, including 5G deployment, and a burgeoning automotive industry, particularly in countries like China, South Korea, Japan, and India. The region's vast manufacturing capabilities and increasing domestic demand for electronic devices contribute significantly to the volume growth of EMI shielding solutions, with a strong focus on cost-effective yet efficient shielding technologies.

Latin America and the Middle East & Africa (MEA) represent emerging markets with considerable untapped potential. These regions are experiencing increasing digitalization, infrastructure development, and a gradual rise in electronic device consumption and local manufacturing. While currently smaller in market share, these regions are expected to witness accelerated growth over the forecast period, driven by foreign investments, technological transfers, and a growing emphasis on modernizing their industrial and consumer sectors, leading to increased adoption of EMI shielding technologies.

- North America: A mature market with significant demand from aerospace, defense, medical, and automotive sectors. Characterized by stringent regulatory standards and a strong focus on high-performance, custom shielding solutions due to advanced R&D capabilities.

- Europe: Driven by the robust automotive industry (especially EV production), industrial automation, and telecommunications. Strong emphasis on environmental compliance (e.g., RoHS, REACH) in material selection and manufacturing processes.

- Asia Pacific (APAC): The leading and fastest-growing region, fueled by massive consumer electronics manufacturing bases, rapid 5G infrastructure rollout, and expanding automotive and industrial sectors in countries like China, Japan, South Korea, and India. Focus on volume, cost-efficiency, and integration into compact devices.

- Latin America: An emerging market showing increasing adoption due to digitalization initiatives, growing consumer electronics demand, and developing automotive and industrial sectors. Growth is supported by increasing local manufacturing capabilities and rising disposable incomes.

- Middle East & Africa (MEA): Demonstrating growth from ongoing infrastructure development projects, increasing investment in IT and telecommunications, and a nascent but growing industrial sector. Adoption is driven by smart city initiatives and the gradual expansion of electronic device usage.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the EMI Shielding Market.- Laird Performance Materials (a DuPont Business)

- Chomerics (a Parker Hannifin Company)

- 3M Company

- Henkel AG & Co. KGaA

- PPG Industries Inc.

- Schlegel Electronic Materials (a division of Bekaert)

- TDK Corporation

- KGS Electronics

- Kitagawa Industries Co., Ltd.

- W. L. Gore & Associates, Inc.

- Tecknit (A company of Parker Hannifin)

- Kemtron Ltd.

- ETS-Lindgren

- Tech-Etch, Inc.

- Leader Tech, Inc.

- Marian Inc.

- Spira Manufacturing Corporation

- Guangzhou Techwin Electronic Co., Ltd.

- Shenzhen Jinke Shielding Material Co., Ltd.

- Hitachi Metals, Ltd.

Frequently Asked Questions

What is EMI Shielding?

EMI Shielding, or Electromagnetic Interference Shielding, is the practice of reducing the electromagnetic field in one area by blocking the field with barriers made of conductive or magnetic materials. Its primary purpose is to prevent the unwanted coupling of electromagnetic energy, ensuring electronic devices function reliably without being disrupted by external interference or causing interference to other devices. It's crucial for maintaining signal integrity and complying with electromagnetic compatibility (EMC) standards in various applications.

Why is EMI Shielding important?

EMI Shielding is critically important because electromagnetic interference can degrade the performance, reliability, and even safety of electronic devices. In sensitive applications like medical equipment, aerospace systems, or high-speed data communications, unchecked EMI can lead to malfunctions, data loss, or system failures. With the proliferation of electronic devices and wireless technologies, effective EMI shielding ensures that these systems operate as intended, meet regulatory compliance, and deliver consistent performance, protecting both the devices and the users.

What are the main types of EMI Shielding materials?

The main types of EMI Shielding materials include conductive coatings and paints, conductive polymers, EMI shielding tapes and laminates, and various metals such as copper, aluminum, and steel. Specialized materials like fabric over foam gaskets and ferrite materials are also widely used. The choice of material depends on factors such as the frequency of interference, required shielding effectiveness, environmental conditions, cost, and the specific application's mechanical and aesthetic demands.

Which industries primarily use EMI Shielding?

EMI Shielding is extensively used across a wide array of industries. Key sectors include consumer electronics (smartphones, laptops, wearables), telecommunications (5G infrastructure, network equipment), automotive (electric vehicles, ADAS), aerospace and defense (avionics, radar systems), and healthcare (medical imaging, diagnostic devices). Industrial applications, data centers, and various other high-tech sectors also rely heavily on EMI shielding to ensure the optimal performance and longevity of their electronic systems.

How is 5G technology impacting the EMI Shielding market?

5G technology is significantly impacting the EMI Shielding market by increasing demand for more advanced and effective solutions. The higher frequencies and greater density of components in 5G devices and infrastructure lead to more complex electromagnetic environments, escalating the risk of interference. This necessitates enhanced shielding to maintain signal integrity, ensure reliable performance, and prevent cross-talk. The miniaturization requiredfor 5G components further drives the need for thin, lightweight, and highly efficient shielding materials that can be integrated into compact designs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted