Embolic Protection Device Material Market

Embolic Protection Device Material Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707313 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

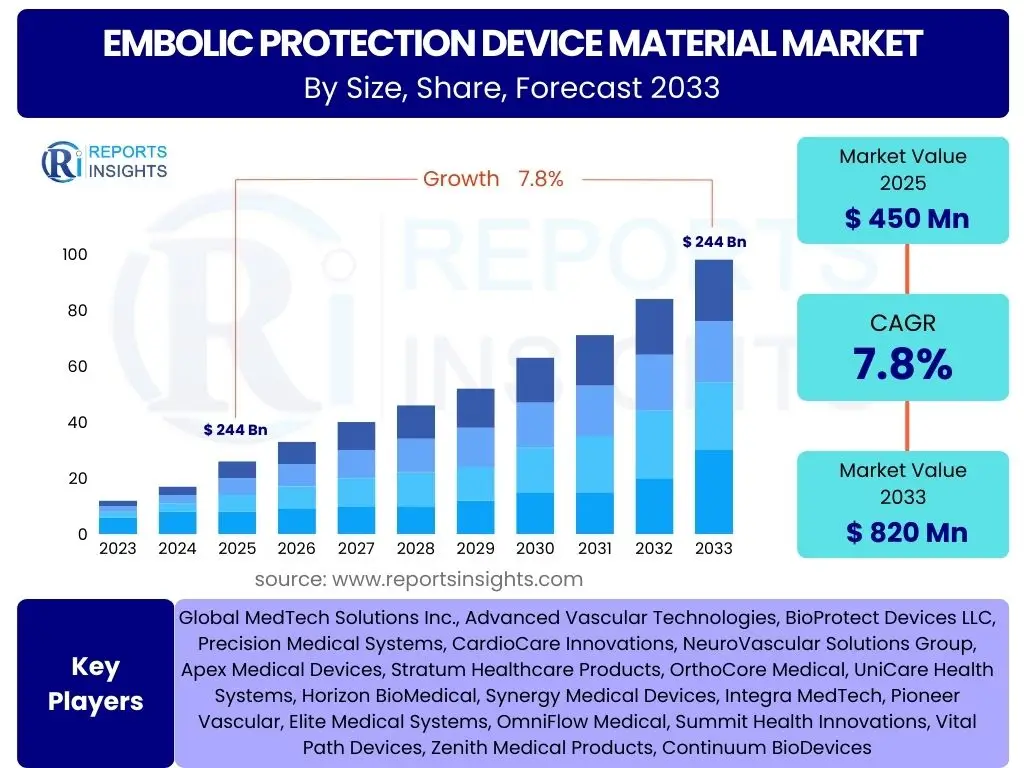

Embolic Protection Device Material Market Size

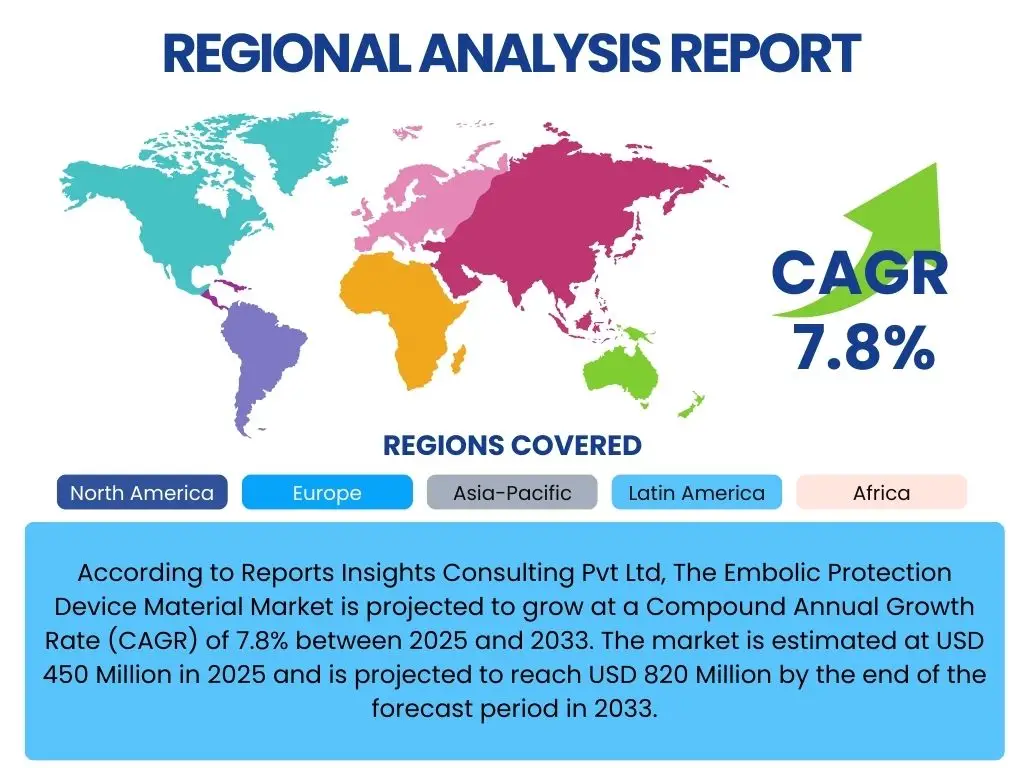

According to Reports Insights Consulting Pvt Ltd, The Embolic Protection Device Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 820 Million by the end of the forecast period in 2033.

Key Embolic Protection Device Material Market Trends & Insights

The Embolic Protection Device Material Market is undergoing significant transformation, driven by advancements in material science and increasing demand for enhanced patient safety during vascular interventions. Current trends reflect a strong emphasis on developing materials that offer superior biocompatibility, flexibility, and anti-thrombogenic properties. Users frequently inquire about the latest innovations in material composition, the integration of smart functionalities, and the shift towards personalized device design, indicating a keen interest in the future landscape of embolic protection.

Furthermore, the market is witnessing a notable move towards sustainable and bioresorbable materials, addressing concerns regarding long-term device presence and potential complications. This aligns with broader healthcare trends favoring less invasive and more natural physiological integration. The drive for improved device deliverability and expanded application areas for embolic protection devices also heavily influences material research and development, aiming to facilitate safer and more efficient procedures across a wider range of vascular anatomies.

- Shift towards advanced polymer materials, including bioresorbable and biodegradable polymers, for enhanced biocompatibility and reduced long-term complications.

- Development of custom-designed embolic protection devices tailored to specific patient anatomies and procedural requirements, leveraging advanced imaging and manufacturing techniques.

- Integration of smart features and sensor technologies into EPD materials for real-time monitoring of blood flow, pressure, or clot formation during interventions.

- Focus on enhancing device deliverability, flexibility, and kink resistance through novel material compositions and innovative device architectures.

- Growing research and development into drug-eluting embolic protection devices that can deliver therapeutic agents locally to prevent restenosis or thrombosis.

- Increasing adoption of nanotechnology in material formulations to improve surface properties, reduce friction, and enhance anti-thrombogenic characteristics.

AI Impact Analysis on Embolic Protection Device Material

Artificial intelligence is poised to revolutionize the Embolic Protection Device Material Market by enhancing various stages of product development, manufacturing, and application. Common user questions revolve around how AI can accelerate material discovery, optimize design processes, and improve the overall efficiency and safety of EPDs. The integration of AI promises to streamline complex research and development cycles, reducing the time and cost associated with bringing new materials to market.

Specifically, AI algorithms can analyze vast datasets of material properties, performance characteristics, and clinical outcomes to identify optimal compositions and designs for embolic protection. This predictive capability allows manufacturers to simulate and test new materials virtually, minimizing the need for extensive physical prototyping. Furthermore, AI-driven analytics can contribute to more precise patient selection and personalized device recommendations, ultimately improving procedural success rates and patient safety.

Beyond design and development, AI is expected to significantly impact manufacturing processes, enabling greater precision and consistency in material production. Quality control can be dramatically enhanced through AI-powered visual inspection systems, capable of detecting minute defects that human eyes might miss. This leads to higher product reliability and reduced waste, optimizing the entire supply chain for embolic protection device materials.

- Accelerated material discovery and optimization through AI-driven computational modeling and simulation, predicting novel material properties and performance.

- Enhanced design processes for embolic protection devices, utilizing AI to optimize device geometry and material distribution for improved flow dynamics and clot capture.

- Optimized manufacturing processes for EPD materials, employing AI for predictive maintenance of machinery, quality control, and consistency in production.

- Personalized EPD design and selection based on AI analysis of patient-specific anatomical data and procedural requirements, leading to improved outcomes.

- AI-powered predictive analytics for anticipating material degradation or device failure, enabling proactive measures and enhancing device longevity and safety.

- Advanced quality control and defect detection in EPD materials and finished devices using AI-driven image analysis and machine vision systems.

Key Takeaways Embolic Protection Device Material Market Size & Forecast

The Embolic Protection Device Material Market is on a robust growth trajectory, driven primarily by the escalating global incidence of cardiovascular and neurovascular diseases requiring interventional procedures. Stakeholders are keen to understand the primary growth catalysts, the regions poised for the most significant expansion, and the overarching factors influencing market valuation. The market's expansion is heavily reliant on continuous technological advancements that enhance device efficacy and patient safety, making them indispensable in complex interventions.

A significant takeaway is the increasing strategic importance of Asia Pacific, which is projected to exhibit the fastest growth due to improving healthcare infrastructure, rising awareness, and a burgeoning patient population. The market outlook is overwhelmingly positive, with sustained investment in research and development to address evolving clinical needs and overcome existing challenges. The forecast indicates a steady increase in market size, reflecting the growing adoption of minimally invasive procedures globally and the critical role of embolic protection in ensuring their success.

- The market is experiencing substantial growth, primarily fueled by the rising prevalence of cardiovascular, peripheral, and neurovascular diseases requiring catheter-based interventions.

- Technological advancements in material science, leading to the development of more effective, flexible, and biocompatible embolic protection devices, are crucial for market expansion.

- The Asia Pacific region is anticipated to be the fastest-growing market segment, driven by improving healthcare access, increasing healthcare expenditure, and a large patient pool.

- Growing preference for minimally invasive surgical procedures globally directly contributes to the increased demand for embolic protection devices.

- Regulatory landscape and reimbursement policies will continue to play a significant role in shaping market dynamics and the adoption of novel embolic protection materials.

Embolic Protection Device Material Market Drivers Analysis

The Embolic Protection Device Material Market is propelled by several critical factors that collectively enhance its growth prospects and drive innovation. A primary driver is the escalating global prevalence of cardiovascular diseases (CVDs), including atherosclerosis, myocardial infarction, and stroke, which necessitate an increasing number of interventional procedures where embolic protection is vital. As these conditions become more widespread due to lifestyle changes and an aging population, the demand for effective protection solutions naturally rises, particularly in regions experiencing rapid demographic shifts.

Furthermore, the ongoing advancements in medical device technology, specifically in the field of minimally invasive procedures, significantly contribute to market expansion. These procedures, favored for their reduced patient trauma, shorter recovery times, and lower complication rates, inherently require sophisticated embolic protection to prevent procedural debris from causing downstream embolisms. This technological synergy ensures that as interventional techniques evolve, so too does the need for advanced protective materials, fostering continuous innovation in device design and material composition.

The increasing elderly demographic worldwide also plays a pivotal role. Older populations are inherently more susceptible to vascular diseases, leading to a higher volume of diagnostic and interventional cardiac and neurovascular procedures. This demographic shift directly translates into a larger patient pool requiring embolic protection, solidifying the market's growth foundation across established and emerging healthcare economies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Cardiovascular & Neurovascular Diseases | +2.5% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Rising Geriatric Population Susceptible to Vascular Conditions | +1.8% | Developed Economies (e.g., Japan, Western Europe, North America) | Medium to Long-term (2026-2033) |

| Technological Advancements in Minimally Invasive Procedures | +1.5% | Global, especially high-tech healthcare markets | Short to Medium-term (2025-2030) |

| Growing Awareness and Adoption of Embolic Protection Devices | +1.0% | Emerging Markets (e.g., China, India, Brazil) | Medium-term (2027-2033) |

Embolic Protection Device Material Market Restraints Analysis

Despite robust growth drivers, the Embolic Protection Device Material Market faces several significant restraints that could impede its expansion. One of the primary limiting factors is the high cost associated with embolic protection devices and the sophisticated materials used in their manufacturing. These expenses can be prohibitive for healthcare systems in developing economies or for patients without adequate insurance coverage, thereby limiting market penetration and widespread adoption. The intricate design and specialized production processes contribute significantly to the overall device cost, impacting affordability and accessibility.

Another substantial restraint is the stringent regulatory approval process governing medical devices, particularly those that are implantable or used in critical vascular interventions. Obtaining market authorization for new materials or device designs requires extensive pre-clinical and clinical trials, which are both time-consuming and capital-intensive. This rigorous oversight, while ensuring patient safety, can significantly delay market entry for innovative products and deter smaller companies from investing in research and development, thus stifling innovation.

Furthermore, the potential for device-related complications, including device malfunction or adverse patient reactions, also acts as a restraint. Instances of product recalls or reported safety concerns can erode clinician confidence and negatively impact market perception, leading to reduced adoption rates. The specialized skills required for proper device deployment and the potential for procedural complications also represent a hurdle, emphasizing the need for continuous professional training and education to mitigate risks.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Embolic Protection Devices | -1.2% | Global, especially emerging and cost-sensitive markets | Short to Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -0.8% | North America, Europe | Medium-term (2026-2030) |

| Risk of Device-Related Complications & Product Recalls | -0.7% | Global | Short-term (2025-2028) |

| Lack of Skilled Professionals for Complex Procedures | -0.5% | Developing Regions | Medium to Long-term (2027-2033) |

Embolic Protection Device Material Market Opportunities Analysis

The Embolic Protection Device Material Market is replete with opportunities for growth and innovation, driven by evolving healthcare needs and technological advancements. One significant opportunity lies in the expanding healthcare infrastructure and increasing healthcare expenditure in emerging economies, particularly in the Asia Pacific and Latin American regions. These markets present a vast untapped patient pool and a growing demand for advanced medical technologies, offering manufacturers substantial avenues for market penetration and expansion beyond saturated developed markets.

Moreover, the continuous advancements in material science present a fertile ground for developing novel embolic protection materials. The focus on creating biodegradable, bioresorbable, and biocompatible materials that integrate seamlessly with the body's physiological processes can revolutionize the market. Such innovations promise to mitigate long-term complications associated with permanent implants, potentially expanding the indications for EPD use and attracting a wider patient demographic seeking safer, more natural solutions. This aligns with a broader industry shift towards patient-centric outcomes.

Furthermore, the exploration and expansion of embolic protection devices into new therapeutic indications beyond traditional coronary and neurovascular interventions offer considerable growth potential. As clinical research validates the benefits of embolic protection in peripheral vascular interventions, structural heart procedures, or even non-vascular applications, the market size and scope will naturally broaden. Strategic collaborations between device manufacturers, research institutions, and clinical centers can accelerate these developments, fostering a synergistic environment for innovation and market leadership.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets (Asia Pacific, Latin America) | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long-term (2027-2033) |

| Development of Biodegradable and Bioresorbable Materials | +1.2% | Global, particularly advanced research hubs | Long-term (2029-2033) |

| Expansion of EPD Application into New Indications | +1.0% | Global, driven by clinical evidence | Medium to Long-term (2028-2033) |

| Strategic Collaborations and Partnerships for R&D | +0.8% | Global | Short to Medium-term (2025-2030) |

Embolic Protection Device Material Market Challenges Impact Analysis

The Embolic Protection Device Material Market, while growing, faces several inherent challenges that demand strategic attention from market participants. Intense competition is a persistent hurdle, with numerous established and emerging players vying for market share. This competitive landscape often leads to price erosion and increased pressure on manufacturers to innovate continuously, potentially squeezing profit margins and making it difficult for new entrants to gain a foothold without significant investment in R&D and marketing. The need to differentiate products through superior performance or cost-effectiveness is paramount.

Supply chain disruptions represent another significant challenge, particularly in the wake of global events such as pandemics, geopolitical tensions, or natural disasters. The sourcing of specialized raw materials, components, and the logistics of manufacturing and distribution can be severely affected, leading to production delays, increased costs, and ultimately, product shortages in the market. Ensuring supply chain resilience and diversification is critical for maintaining consistent product availability and meeting market demand. This necessitates robust risk management strategies and alternative sourcing options.

Furthermore, navigating the complex and often varying reimbursement policies across different healthcare systems globally poses a considerable challenge. Inadequate or inconsistent reimbursement for embolic protection devices can significantly limit their adoption, especially for newer, more advanced, and often more expensive technologies. Manufacturers must demonstrate clear clinical and economic value to secure favorable reimbursement, which is a lengthy and complex process impacting market access and commercial viability. This financial barrier can impede broader market penetration despite clinical benefits.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Pricing Pressures | -0.9% | Global | Short to Medium-term (2025-2030) |

| Supply Chain Disruptions and Raw Material Volatility | -0.7% | Global | Short to Medium-term (2025-2028) |

| Complex Reimbursement Policies and Funding Constraints | -0.6% | North America, Europe | Medium to Long-term (2026-2033) |

| Intellectual Property Protection and Litigation Risks | -0.4% | Global, particularly competitive markets | Long-term (2029-2033) |

Embolic Protection Device Material Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Embolic Protection Device Material Market, offering critical insights into its current landscape and future growth trajectory. The report meticulously details market size estimations, growth forecasts, key market trends, and an exhaustive examination of market drivers, restraints, opportunities, and challenges. It is designed to equip stakeholders with actionable intelligence for strategic decision-making within this evolving medical device segment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 820 Million |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global MedTech Solutions Inc., Advanced Vascular Technologies, BioProtect Devices LLC, Precision Medical Systems, CardioCare Innovations, NeuroVascular Solutions Group, Apex Medical Devices, Stratum Healthcare Products, OrthoCore Medical, UniCare Health Systems, Horizon BioMedical, Synergy Medical Devices, Integra MedTech, Pioneer Vascular, Elite Medical Systems, OmniFlow Medical, Summit Health Innovations, Vital Path Devices, Zenith Medical Products, Continuum BioDevices |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Embolic Protection Device Material Market is meticulously segmented to provide a granular understanding of its diverse components and their individual contributions to the overall market dynamics. This segmentation allows for a detailed analysis of material preferences, device types, prevalent applications, and primary end-use settings, offering stakeholders a clear view of where growth is concentrated and where opportunities for differentiation lie. Understanding these segments is crucial for strategic planning, product development, and targeted market penetration.

The market is primarily segmented by Material Type, which categorizes the core components used in EPD manufacturing, reflecting the ongoing innovation in material science aimed at improving biocompatibility and performance. Device Type further differentiates products based on their mechanism of action and placement during procedures, highlighting specific functional requirements. Application segments illustrate the clinical areas where EPDs are predominantly utilized, showcasing the critical demand driven by various cardiovascular and neurovascular conditions. Finally, the End-Use segment identifies the key healthcare facilities where these devices are adopted, providing insights into the primary distribution channels and consumption patterns.

- By Material Type: This segment includes the various materials predominantly used in the construction of embolic protection devices, each offering unique properties regarding flexibility, strength, biocompatibility, and filterability.

- Nitinol: Valued for its superelasticity and shape memory properties, making it ideal for self-expanding filters.

- Polyurethane: Chosen for its flexibility and biocompatibility, often used in balloon-based EPDs.

- ePTFE (expanded Polytetrafluoroethylene): Known for its porosity and smooth surface, suitable for filter membranes.

- Other Advanced Polymers: Includes newer synthetic and bioresorbable polymers designed for enhanced performance and reduced long-term presence.

- By Device Type: This classification refers to the design and operational mechanism of the embolic protection devices.

- Distal Embolic Protection Devices: Positioned beyond the lesion to capture emboli before they reach downstream vasculature.

- Proximal Embolic Protection Devices: Placed before the lesion to occlude blood flow or divert emboli away from the target vessel.

- By Application: This segment highlights the primary medical interventions and conditions where embolic protection devices are critically employed to prevent complications.

- Coronary Interventions: Procedures such as Percutaneous Coronary Interventions (PCIs) for coronary artery disease.

- Peripheral Interventions: Procedures in peripheral arteries to treat conditions like Peripheral Artery Disease (PAD).

- Neurovascular Interventions: Procedures in the brain and neck vasculature, for conditions such as stroke or carotid artery disease.

- Other Vascular Interventions: Includes applications in renal arteries, venous interventions, and other less common vascular procedures.

- By End-Use: This segment identifies the key healthcare settings where embolic protection devices are primarily utilized and purchased.

- Hospitals: Major consumers due to the volume of complex interventional cardiology and neurology procedures performed.

- Ambulatory Surgical Centers (ASCs): Growing adoption for less complex, outpatient vascular procedures.

- Specialty Clinics: Focused clinics offering specific cardiac or vascular treatments.

- Research Institutes: Involved in the development and testing of new embolic protection technologies and materials.

Regional Highlights

- North America: This region holds a dominant share in the Embolic Protection Device Material Market, primarily due to its advanced healthcare infrastructure, high prevalence of cardiovascular and neurovascular diseases, and significant adoption of minimally invasive procedures. The presence of key market players, robust R&D activities, and favorable reimbursement policies further contribute to its leading position. The United States and Canada are major contributors, characterized by high disposable incomes and strong awareness regarding advanced medical treatments.

- Europe: The European market for embolic protection device materials is mature, characterized by a well-established healthcare system and a strong emphasis on medical innovation. Countries like Germany, the UK, France, and Italy are significant contributors, driven by an aging population, rising incidence of vascular disorders, and increasing investment in healthcare technology. Strict regulatory standards ensure high product quality and safety, fostering clinician confidence and widespread adoption.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the Embolic Protection Device Material Market during the forecast period. This growth is attributed to improving healthcare infrastructure, rising healthcare expenditure, a large and aging population, and increasing awareness of advanced medical devices. Countries such as China, India, and Japan are at the forefront of this expansion, driven by economic development, growing medical tourism, and a rising prevalence of lifestyle-related diseases. The increasing demand for minimally invasive procedures and local manufacturing initiatives also fuel market growth.

- Latin America: The market in Latin America is witnessing steady growth, influenced by improving healthcare access, increasing government investments in healthcare facilities, and a rising middle-class population. Brazil, Mexico, and Argentina are key markets in this region, adopting advanced medical technologies to address the burden of cardiovascular diseases. However, economic instability and varying regulatory landscapes can pose challenges.

- Middle East and Africa (MEA): The MEA market for embolic protection device materials is in its nascent stage but shows promising growth potential. This is driven by increasing healthcare investments, a growing patient pool with cardiovascular conditions, and a rising demand for specialized medical procedures, particularly in countries like Saudi Arabia, UAE, and South Africa. However, limited healthcare infrastructure and lower per capita healthcare spending in some parts of the region can be restraining factors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Embolic Protection Device Material Market.- Global MedTech Solutions Inc.

- Advanced Vascular Technologies

- BioProtect Devices LLC

- Precision Medical Systems

- CardioCare Innovations

- NeuroVascular Solutions Group

- Apex Medical Devices

- Stratum Healthcare Products

- OrthoCore Medical

- UniCare Health Systems

- Horizon BioMedical

- Synergy Medical Devices

- Integra MedTech

- Pioneer Vascular

- Elite Medical Systems

- OmniFlow Medical

- Summit Health Innovations

- Vital Path Devices

- Zenith Medical Products

- Continuum BioDevices

Frequently Asked Questions

Analyze common user questions about the Embolic Protection Device Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What materials are commonly used in embolic protection devices?

The most common materials utilized in embolic protection devices include Nitinol for its superelasticity and shape memory, Polyurethane for flexibility, and ePTFE (expanded Polytetrafluoroethylene) for filter membranes. Research is also expanding into other advanced polymers, including biodegradable and bioresorbable options.

How large is the Embolic Protection Device Material Market expected to grow?

The Embolic Protection Device Material Market is projected to grow from an estimated USD 450 Million in 2025 to USD 820 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period.

What are the primary applications of embolic protection devices?

Embolic protection devices are primarily used in critical interventional procedures to prevent emboli (clots or debris) from traveling downstream. Key applications include coronary interventions (e.g., during angioplasty and stenting), peripheral interventions, and neurovascular interventions, such as carotid artery stenting.

What are the key factors driving the growth of the Embolic Protection Device Material Market?

Key drivers include the increasing global prevalence of cardiovascular and neurovascular diseases, a rising aging population, ongoing technological advancements in minimally invasive procedures, and growing awareness and adoption of embolic protection for enhanced patient safety during interventions.

How is AI impacting the development and manufacturing of EPD materials?

AI is significantly impacting EPD materials by accelerating material discovery, optimizing device design through simulation, enhancing manufacturing processes for consistency, and improving quality control with advanced defect detection. AI can also aid in personalized EPD selection based on patient data.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted