Electronic Ceramic Market

Electronic Ceramic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700250 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

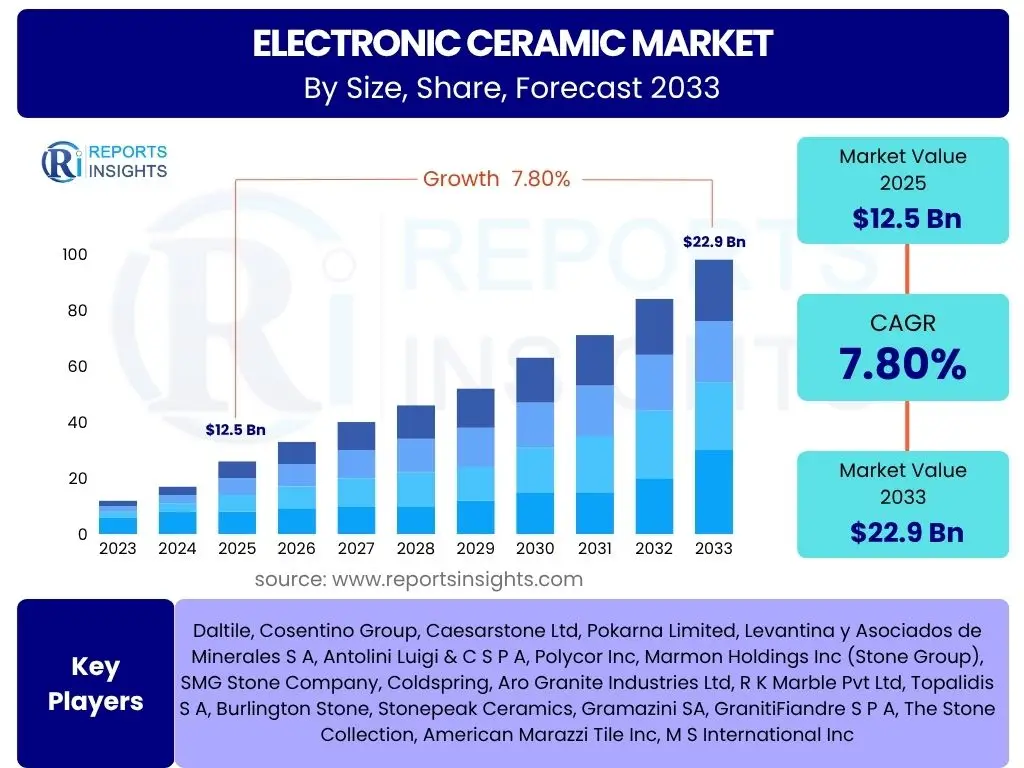

Electronic Ceramic Market is projected to grow at a Compound annual growth rate (CAGR) of 7.8% between 2025 and 2033, current valued at USD 12.5 billion in 2025 and is projected to reach USD 22.9 billion By 2033 the end of the forecast period.

Key Electronic Ceramic Market Trends & Insights

The Electronic Ceramic Market is currently undergoing significant transformation, driven by an escalating demand for advanced materials across various high-tech industries. Emerging trends such as miniaturization, the rollout of 5G technology, and the rapid expansion of electric vehicles are reshaping manufacturing processes and application landscapes. These shifts necessitate materials with superior dielectric properties, thermal management capabilities, and enhanced mechanical strength, pushing innovation in ceramic compositions and fabrication techniques.

- Increasing demand for compact and high-performance electronic components.

- Accelerated adoption of 5G technology requiring advanced dielectric materials.

- Significant growth in electric vehicle production driving demand for power electronics.

- Rising integration of electronic ceramics in medical implants and devices.

- Growing focus on sustainable and eco-friendly manufacturing processes.

- Development of advanced ceramic composites for enhanced functionality.

- Expansion of IoT and AI applications demanding specialized sensor components.

AI Impact Analysis on Electronic Ceramic

Artificial Intelligence (AI) is poised to revolutionize the Electronic Ceramic Market by enhancing efficiency across the entire value chain, from research and development to manufacturing and quality control. AI-driven simulations can significantly reduce the time and cost associated with discovering new material formulations and optimizing their properties, enabling faster innovation cycles. Furthermore, predictive analytics and machine learning algorithms are being deployed to improve manufacturing precision, reduce defects, and optimize supply chain logistics, leading to higher yields and reduced operational expenses.

- Accelerated material discovery and optimization through AI-driven simulations.

- Enhanced predictive maintenance and process optimization in ceramic manufacturing.

- Improved quality control and defect detection using computer vision and machine learning.

- Optimized supply chain management and demand forecasting for raw materials and finished products.

- Development of smart ceramic components with embedded AI capabilities for advanced sensing.

Key Takeaways Electronic Ceramic Market Size & Forecast

- The global Electronic Ceramic Market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 7.8% from 2025 to 2033.

- The market size is estimated at USD 12.5 billion in 2025, reflecting a significant base for future expansion.

- By 2033, the market is forecasted to reach USD 22.9 billion, indicating nearly a doubling in market valuation over the forecast period.

- This growth is primarily fueled by increasing applications in consumer electronics, automotive electrification, and advanced telecommunications.

- Asia Pacific is expected to remain the dominant region due to its extensive electronics manufacturing base.

- Innovations in material science and increasing R&D investments are critical drivers for market expansion.

Electronic Ceramic Market Drivers Analysis

The Electronic Ceramic Market is experiencing substantial growth propelled by several critical factors, primarily stemming from the rapid technological advancements and expanding applications across various industries. The increasing adoption of electronic devices and systems, alongside the ongoing trend towards miniaturization and higher performance, necessitates materials with superior electrical, thermal, and mechanical properties that conventional materials often cannot provide. These drivers collectively contribute to the sustained demand and innovation within the electronic ceramic sector, enabling new functionalities and improved efficiencies in modern electronics.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Consumer Electronics Demand: The proliferation of smartphones, laptops, tablets, wearables, and other smart devices drives significant demand for electronic ceramics due to their use in capacitors, resistors, integrated circuit packages, and display components. | +2.1% | Asia Pacific (China, South Korea, Japan), North America, Europe | Long-term (2025-2033) |

| Expansion of 5G Infrastructure and Telecommunications: The rollout of 5G networks requires high-frequency, high-performance materials for antennas, filters, and base stations, where electronic ceramics offer excellent dielectric properties and low signal loss. | +1.8% | Global, particularly North America, Europe, Asia Pacific (China, South Korea) | Mid-term to Long-term (2025-2030) |

| Rise of Electric Vehicles (EVs) and Automotive Electronics: Electronic ceramics are crucial in power electronics for EVs, including inverters, converters, and battery management systems, offering high temperature resistance and excellent insulation properties critical for vehicle performance and safety. | +1.9% | Europe (Germany, Norway), Asia Pacific (China, Japan), North America (USA) | Long-term (2025-2033) |

| Increasing Demand in Healthcare and Medical Devices: Biocompatible electronic ceramics are increasingly used in medical implants, diagnostic equipment, and sensors due to their inertness, wear resistance, and ability to house complex electronics. | +1.2% | North America, Europe, Japan | Long-term (2025-2033) |

| Advancements in Aerospace and Defense Applications: High-performance electronic ceramics are vital for radar systems, guidance systems, sensors, and communication equipment in aerospace and defense, requiring extreme temperature tolerance and radiation resistance. | +0.8% | North America (USA), Europe (France, UK) | Mid-term to Long-term (2025-2033) |

| Miniaturization and Compact Device Trends: The continuous push for smaller, lighter, and more powerful electronic devices drives the demand for electronic ceramics, which enable high component density and superior performance in reduced footprints. | +1.0% | Global, particularly Asia Pacific, North America | Long-term (2025-2033) |

Electronic Ceramic Market Restraints Analysis

Despite the robust growth potential, the Electronic Ceramic Market faces several significant restraints that could impede its expansion. These challenges primarily revolve around the complex and costly manufacturing processes, volatility in raw material prices, and increasing environmental regulatory pressures. Furthermore, competition from alternative materials that offer comparable performance at potentially lower costs or easier processing methods poses a continuous threat. Addressing these restraints requires strategic investments in R&D for cost-effective production, diversification of raw material sourcing, and adherence to evolving sustainability standards.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Complexity: The production of electronic ceramics often involves complex processes like precision machining, high-temperature sintering, and specialized firing, leading to high capital expenditure and operational costs, which can hinder market entry for new players and impact profitability. | -0.9% | Global, particularly regions with less developed manufacturing infrastructure | Long-term (2025-2033) |

| Volatility in Raw Material Prices: The market relies on specific raw materials such as rare earth elements, zirconia, alumina, and titania, whose supply can be influenced by geopolitical factors, mining regulations, and demand-supply imbalances, leading to price volatility and affecting production costs. | -0.7% | Global, especially for regions reliant on specific raw material imports | Mid-term (2025-2029) |

| Competition from Alternative Materials: Advanced polymers, composites, and specialized metals are continuously improving their properties, posing a competitive threat to electronic ceramics in certain applications where they might offer cost-effectiveness or easier processing. | -0.6% | Global, across various end-use industries | Long-term (2025-2033) |

| Environmental Regulations and Disposal Challenges: Strict environmental regulations regarding hazardous waste disposal and energy consumption in manufacturing processes can increase compliance costs and limit production capacities, particularly for certain ceramic types. | -0.5% | Europe, North America, parts of Asia with stringent environmental policies | Long-term (2025-2033) |

| Supply Chain Disruptions: The global nature of raw material sourcing and manufacturing networks makes the electronic ceramic market vulnerable to geopolitical tensions, trade disputes, and unforeseen events like pandemics, leading to supply chain inefficiencies and delays. | -0.4% | Global, with particular impact on regions heavily reliant on international trade | Short to Mid-term (2025-2027) |

Electronic Ceramic Market Opportunities Analysis

The Electronic Ceramic Market is ripe with promising opportunities driven by continuous technological advancements and the emergence of new high-growth application areas. Innovations in material science are leading to the development of novel ceramic compositions with enhanced properties, expanding their utility beyond traditional electronic components. Furthermore, the increasing global investment in cutting-edge technologies like quantum computing, advanced sensing, and smart infrastructure presents significant avenues for market expansion. Leveraging these opportunities will require strategic investments in research and development, fostering collaborations, and adapting to evolving industry demands for superior performance and sustainable solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Ceramic Materials: Ongoing research in nanotechnology and material science is leading to new ceramic compositions with superior dielectric, piezoelectric, magnetic, and superconducting properties, opening doors for advanced applications in quantum computing, high-frequency communication, and energy storage. | +1.5% | Global, particularly advanced research hubs in North America, Europe, Japan | Long-term (2028-2033) |

| Growing Demand for High-Frequency and High-Power Applications: The increasing power density and operating frequencies in areas like radar systems, electric vehicle chargers, and industrial power supplies create a strong demand for electronic ceramics capable of handling extreme conditions with minimal losses. | +1.3% | Global, with emphasis on automotive, industrial, and defense sectors | Mid-term to Long-term (2026-2033) |

| Integration into Smart Cities and Industrial Automation: Electronic ceramics are critical components in sensors, actuators, and communication modules essential for smart city infrastructure, smart grids, and advanced robotics in industrial automation, presenting a large untapped market. | +1.0% | Asia Pacific (China, Singapore), Europe (Germany, UK), North America | Long-term (2027-2033) |

| Additive Manufacturing (3D Printing) of Ceramics: The advent of 3D printing technologies for ceramics allows for the creation of complex geometries and customized components with reduced material waste and faster prototyping, opening new design possibilities and market niches. | +0.8% | Global, particularly in advanced manufacturing economies | Mid-term (2026-2030) |

| Expansion into Emerging Markets: Developing economies are experiencing rapid industrialization and increasing adoption of electronic devices, creating new demand centers for electronic ceramics as their manufacturing capabilities and consumer bases grow. | +0.6% | Latin America, Southeast Asia, India, parts of Africa | Long-term (2027-2033) |

Electronic Ceramic Market Challenges Impact Analysis

The Electronic Ceramic Market faces several formidable challenges that require strategic responses from manufacturers and innovators. Rapid technological obsolescence, driven by the relentless pace of innovation in the electronics industry, means that ceramic component designs and material specifications can become outdated quickly. Furthermore, a shortage of specialized talent in material science and ceramic engineering poses a hurdle to both research and development and manufacturing efficiency. Maintaining stringent quality control and achieving high yield rates amidst complex production processes are ongoing operational challenges. Overcoming these hurdles will be crucial for sustained growth and competitiveness in this dynamic market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Obsolescence and Rapid Innovation Cycles: The fast pace of technological advancement in the electronics industry means that electronic ceramic components can quickly become obsolete, requiring continuous R&D investment and adaptation, which is costly and risky for manufacturers. | -0.8% | Global, especially in highly competitive electronics manufacturing hubs | Long-term (2025-2033) |

| Talent Shortage in Material Science and Ceramic Engineering: A specialized skill set is required for research, development, and manufacturing of advanced electronic ceramics. A lack of trained professionals can hinder innovation, production efficiency, and overall market growth. | -0.6% | North America, Europe, Japan (aging workforce), specific emerging markets | Long-term (2025-2033) |

| Maintaining Quality Control and Yield Rates: The intricate manufacturing processes of electronic ceramics, which involve precise compositional control, sintering temperatures, and geometric tolerances, make achieving consistent quality and high yield rates challenging, leading to potential waste and increased costs. | -0.5% | Global manufacturing centers | Long-term (2025-2033) |

| Geopolitical Tensions and Trade Barriers: Disruptions arising from international trade disputes, tariffs, and geopolitical instability can significantly impact the sourcing of raw materials, cross-border technology transfer, and market access, affecting global supply chains. | -0.4% | Global, with specific impacts on US-China, EU-Asia trade routes | Short to Mid-term (2025-2028) |

| Recycling and End-of-Life Management: The durable and often chemically stable nature of electronic ceramics makes their recycling and environmentally sound disposal challenging, raising concerns about sustainability and requiring innovative end-of-life solutions. | -0.3% | Europe (due to WEEE directive), North America, Japan | Long-term (2027-2033) |

Electronic Ceramic Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Electronic Ceramic Market, offering crucial insights into its current landscape and future growth trajectory. The scope encompasses detailed segmentation, regional analysis, competitive benchmarking, and strategic insights for stakeholders. The report aims to furnish decision-makers with actionable intelligence to navigate market dynamics, identify growth opportunities, and formulate robust business strategies. It covers historical data, current market size, and future projections across various dimensions of the electronic ceramic industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 billion |

| Market Forecast in 2033 | USD 22.9 billion |

| Growth Rate | 7.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kyocera Corporation, Murata Manufacturing Co., Ltd., TDK Corporation, CeramTec GmbH, CoorsTek Inc., Morgan Advanced Materials plc, Hitachi Metals, Ltd., Shin-Etsu Chemical Co., Ltd., Nippon Chemi-Con Corporation, Noritake Co., Limited, NGK Spark Plug Co., Ltd., AGC Inc., DuPont de Nemours, Inc., Corning Incorporated, Littelfuse, Inc., Taiyo Yuden Co., Ltd., EPCOS AG, Vishay Intertechnology, Inc., KOA Corporation, Sumitomo Electric Industries, Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electronic Ceramic Market is comprehensively segmented to provide a granular view of its diverse landscape, enabling a thorough analysis of market dynamics across various dimensions. Understanding these segments is crucial for identifying specific growth pockets, competitive landscapes, and strategic opportunities. The segmentation covers different types of electronic ceramics based on their material composition, a broad range of applications where these ceramics are utilized, and the various end-use industries that drive their demand, offering a multifaceted perspective on the market's structure and potential.

- By Type: This segment categorizes electronic ceramics based on their chemical composition and material properties, which dictate their specific functionalities and applications.

- Alumina: Widely used for substrates, insulators, and packaging due to its high strength, hardness, and excellent dielectric properties.

- Zirconia: Valued for its toughness, wear resistance, and high strength, often found in oxygen sensors and solid oxide fuel cells.

- Titanates: Includes Barium Titanate and Lead Zirconate Titanate (PZT), crucial for capacitors, piezoelectrics, and sensors due to their high dielectric constant and piezoelectric properties.

- Ferrites: Magnetic ceramics (Soft Ferrites for inductors, transformers; Hard Ferrites for permanent magnets) used in various electronic devices.

- Silicon Carbide: Known for high thermal conductivity, high power handling, and semiconductor applications in power electronics.

- Beryllium Oxide: Offers exceptional thermal conductivity, making it suitable for high-power semiconductor packages and heat sinks.

- Aluminum Nitride: High thermal conductivity and electrical insulation make it ideal for power modules and LED substrates.

- Silicon Nitride: Excellent mechanical properties, high-temperature stability, and wear resistance, used in specific sensor applications.

- Others: Includes a range of specialized ceramics like steatite, forsterite, and various advanced composites for niche applications.

- By Application: This segment details the diverse functions and components where electronic ceramics are essential, reflecting the breadth of their utility in modern electronics.

- Capacitors: Primarily uses titanates (e.g., BaTiO3) for multilayer ceramic capacitors (MLCCs) and other capacitor types.

- Resistors: Used in ceramic-based resistors for stability and thermal performance.

- Inductors: Utilizes ferrite materials for core components in inductive devices.

- Insulators: Alumina and other high-dielectric strength ceramics provide electrical insulation in various components.

- Integrated Circuit Packages: Materials like alumina and aluminum nitride form the protective and functional housing for semiconductor chips (e.g., DIP, QFP, BGA).

- Sensors: Piezoelectric ceramics (PZT) and others used in pressure, temperature, gas, and optical sensors.

- Actuators: Piezoelectric ceramics convert electrical energy into mechanical motion for precision control.

- Transducers: Devices that convert energy from one form to another, often utilizing piezoelectric ceramics.

- Piezoelectric Devices: Direct application of piezoelectric ceramics in buzzers, transducers, and ultrasonic devices.

- Filters: Ceramic filters are used for signal processing in communication devices due to their stable frequency response.

- Thermistors: Ceramics whose resistance varies significantly with temperature, used for temperature sensing and control.

- Varistors: Ceramic components that protect circuits from voltage surges.

- Other Passive Components: Includes a variety of other ceramic-based components essential for circuit functionality.

- By End-Use Industry: This segment highlights the major sectors that drive the demand for electronic ceramics, showcasing the market's reliance on industrial growth and technological advancement in these areas.

- Consumer Electronics: Largest segment, driven by demand for smartphones, laptops, TVs, wearables, and other household electronic devices.

- Automotive: Crucial for electric vehicles (EVs), hybrid vehicles, advanced driver-assistance systems (ADAS), and engine management.

- Healthcare: Used in medical implants, diagnostic equipment, surgical tools, and imaging systems.

- Aerospace and Defense: Essential for radar systems, navigation equipment, communication devices, and high-temperature components in aircraft and spacecraft.

- Industrial: Applications in industrial machinery, robotics, power generation, and automation systems.

- Telecommunications: Critical for 5G infrastructure, base stations, fiber optics, and network equipment.

- Energy and Power: Utilized in power generation, transmission, distribution, and renewable energy systems (e.g., solar inverters, fuel cells).

- Others: Includes applications in research and development, scientific instruments, and niche industrial uses.

Regional Highlights

The Electronic Ceramic Market exhibits diverse growth patterns and market concentrations across different geographical regions, heavily influenced by industrial development, technological adoption rates, and governmental initiatives. Each region presents unique opportunities and challenges based on its established manufacturing base, R&D capabilities, and consumer demand. Understanding these regional dynamics is crucial for businesses to tailor their strategies, optimize supply chains, and identify high-potential markets for investment and expansion. The following highlights focus on the top-performing regions and the factors that underpin their significance in the global market landscape.

- Asia Pacific (APAC): Dominates the global Electronic Ceramic Market, primarily driven by the colossal manufacturing bases for consumer electronics, automotive components, and telecommunication equipment in countries like China, Japan, South Korea, Taiwan, and India. The region benefits from lower labor costs, robust governmental support for electronics industries, and a rapidly expanding middle-class consumer base. Significant investments in 5G infrastructure, electric vehicle manufacturing, and smart city projects further solidify APAC's leading position, making it the most critical region for both production and consumption.

- North America: Represents a significant market, characterized by high adoption of advanced technologies, strong R&D capabilities, and a robust defense and aerospace sector. The region, particularly the United States, drives demand for high-performance electronic ceramics in specialized applications, medical devices, and innovative consumer electronics. The presence of major technology companies and consistent investment in cutting-edge research contribute to its steady market growth and focus on high-value products.

- Europe: A mature market with strong emphasis on automotive electronics, industrial automation, and healthcare. Countries like Germany, France, and the UK are key contributors, driven by stringent environmental regulations promoting EV adoption and significant investments in Industry 4.0. Europe also leads in research and development of advanced materials, though its manufacturing scale for commodity electronic components is less than APAC. The region focuses on quality, high-reliability components, and sustainable manufacturing practices.

- Latin America: An emerging market with growing electronics manufacturing and automotive industries, particularly in countries like Brazil and Mexico. While smaller in market share compared to established regions, it offers future growth potential driven by increasing urbanization, industrialization, and rising consumer spending on electronic devices. Investments in local manufacturing capabilities and infrastructure development will be crucial for its market expansion.

- Middle East and Africa (MEA): Currently a nascent but rapidly developing market for electronic ceramics. Growth is stimulated by increasing investments in telecommunications infrastructure, smart city initiatives (especially in the GCC countries), and diversification efforts away from oil economies. The region presents opportunities for technology transfer and establishment of new manufacturing facilities, though local demand for advanced electronic devices is still evolving.

Top Key Players:

The market research report covers the analysis of key stake holders of the Electronic Ceramic Market. Some of the leading players profiled in the report include -- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- CeramTec GmbH

- CoorsTek Inc.

- Morgan Advanced Materials plc

- Hitachi Metals, Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Nippon Chemi-Con Corporation

- Noritake Co., Limited

- NGK Spark Plug Co., Ltd.

- AGC Inc.

- DuPont de Nemours, Inc.

- Corning Incorporated

- Littelfuse, Inc.

- Taiyo Yuden Co., Ltd.

- EPCOS AG

- Vishay Intertechnology, Inc.

- KOA Corporation

- Sumitomo Electric Industries, Ltd.

Frequently Asked Questions:

What are electronic ceramics?

Electronic ceramics are inorganic, non-metallic materials specifically engineered for their unique electrical, magnetic, and optical properties, making them indispensable components in electronic devices and systems. Unlike traditional ceramics, electronic ceramics possess functionalities such as electrical insulation, semiconduction, superconductivity, piezoelectricity, and magnetism. They are crucial for components like capacitors, sensors, actuators, insulators, and integrated circuit packages, enabling the performance and miniaturization of modern electronics across various industries.

What are the key applications of electronic ceramics?

Electronic ceramics find widespread applications across numerous high-tech industries due to their superior performance characteristics. In consumer electronics, they are vital for components in smartphones, laptops, and wearables. The automotive sector utilizes them extensively in electric vehicle power electronics and advanced driver-assistance systems. They are also critical in telecommunications for 5G infrastructure, in healthcare for medical implants and diagnostic tools, and in aerospace and defense for high-performance sensors and radar systems. Their versatility extends to industrial automation, energy management, and various specialized devices requiring high reliability and specific electrical properties.

What is the projected market size and growth forecast for the Electronic Ceramic Market?

The Electronic Ceramic Market is projected for substantial growth. It was valued at USD 12.5 billion in 2025 and is forecasted to reach USD 22.9 billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 7.8% over the forecast period. This growth is driven by the increasing global demand for high-performance electronic devices, advancements in telecommunications infrastructure, the rapid expansion of electric vehicles, and continuous innovation in material science and engineering across various end-use industries.

What are the main drivers influencing the Electronic Ceramic Market growth?

The primary drivers propelling the Electronic Ceramic Market include the surging demand from the consumer electronics industry due to device proliferation and miniaturization trends. The global rollout of 5G networks, requiring advanced dielectric materials, and the rapid expansion of electric vehicle production, necessitating high-performance power electronics, are also significant catalysts. Furthermore, increasing applications in the healthcare sector for biocompatible devices and specialized components in aerospace and defense contribute significantly to the market's sustained growth. These factors collectively underscore the critical role of electronic ceramics in modern technological advancements.

What key challenges does the Electronic Ceramic Market face?

The Electronic Ceramic Market faces several notable challenges that can impact its growth and operational efficiency. These include the inherently high manufacturing costs and complexity associated with producing advanced ceramic components, which can limit market entry and affect profitability. Volatility in the prices and supply of critical raw materials due to geopolitical factors poses a continuous risk. Additionally, competition from alternative materials that offer comparable performance, stringent environmental regulations, and the rapid pace of technological obsolescence necessitating constant R&D investments are significant hurdles that market players must strategically address to maintain competitiveness and growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted