Electronic Adhesive Market

Electronic Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709066 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

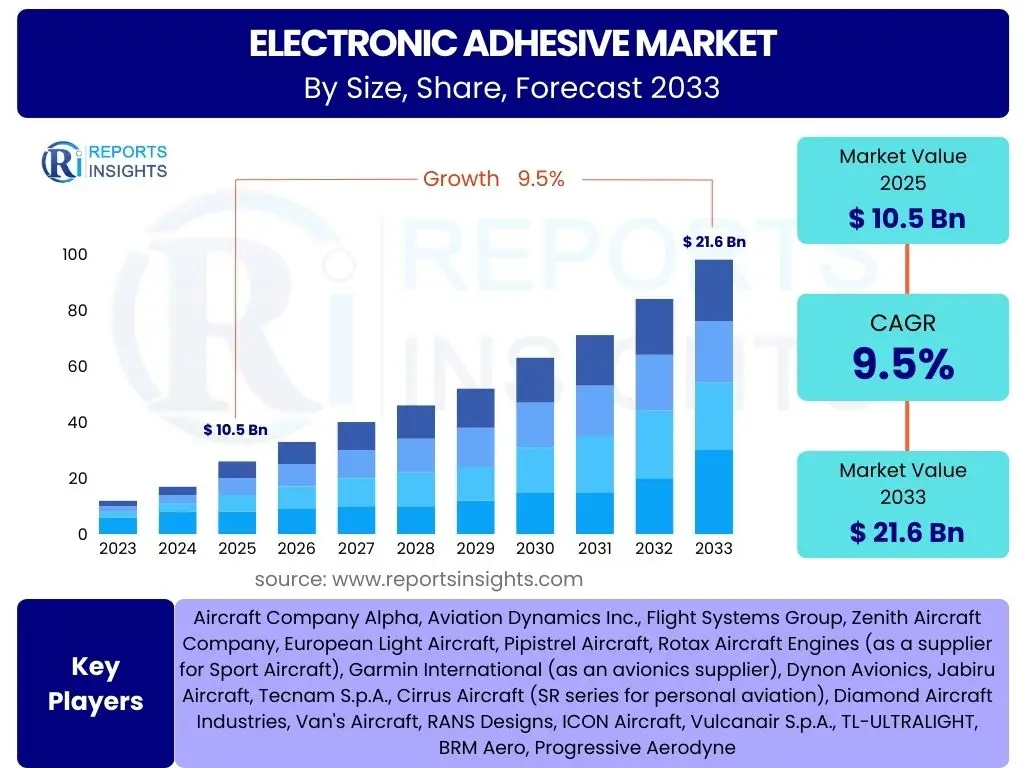

Electronic Adhesive Market Size

According to Reports Insights Consulting Pvt Ltd, The Electronic Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 10.5 Billion in 2025 and is projected to reach USD 21.6 Billion by the end of the forecast period in 2033.

Key Electronic Adhesive Market Trends & Insights

User inquiries frequently highlight the shift towards miniaturization and higher performance in electronic devices as a primary driver for advanced electronic adhesives. There is significant interest in understanding how these materials are evolving to meet stringent requirements for thermal management, electrical conductivity, and structural integrity in increasingly compact and sophisticated electronics. Furthermore, the market is keen on innovations driven by new application areas such as electric vehicles, 5G infrastructure, and advanced medical devices, which demand specialized adhesive properties not previously required in traditional electronics.

Another area of focus for market participants and end-users revolves around the sustainability and environmental impact of electronic adhesives. Questions often emerge regarding the development of eco-friendly formulations, solvent-free options, and adhesives that comply with evolving regulatory standards such as RoHS and REACH. The trend toward automation in manufacturing processes also necessitates adhesives that offer faster cure times, improved dispensing accuracy, and enhanced compatibility with automated assembly lines, reflecting a broader industry push for efficiency and reduced production costs. The increasing demand for robust and reliable connections in harsh operating environments, particularly in automotive and industrial electronics, further shapes the development of highly durable and resilient adhesive solutions.

- Miniaturization and high-density packaging demanding advanced thermal and electrical performance.

- Growth of flexible and printed electronics requiring deformable and low-temperature curable adhesives.

- Increased adoption of electric vehicles (EVs) driving demand for adhesives in battery packs and power electronics.

- Development of sustainable and eco-friendly adhesive formulations.

- Integration of smart manufacturing processes requiring faster-curing and automated dispensing adhesives.

AI Impact Analysis on Electronic Adhesive

Common user questions regarding AI's impact on the electronic adhesive market often center on its role in optimizing material development and manufacturing processes. Stakeholders are keen to understand how artificial intelligence can accelerate the discovery of novel adhesive formulations with specific performance characteristics, predict material behaviors under various conditions, and streamline the R&D cycle. This includes inquiries into AI-driven simulations for material design and the potential for machine learning algorithms to analyze vast datasets of material properties to identify optimal compositions, thereby reducing the need for extensive physical prototyping and testing.

Furthermore, there is significant interest in how AI can enhance efficiency and quality control within electronic adhesive manufacturing and application. Users frequently ask about AI's application in predictive maintenance for dispensing equipment, optimizing curing parameters, and identifying defects in real-time during assembly. AI's capabilities in demand forecasting and supply chain optimization are also frequently discussed, as these can help manufacturers manage inventory, reduce waste, and respond more effectively to market fluctuations. The overall expectation is that AI will lead to more intelligent, adaptive, and precise adhesive solutions, driving both product innovation and operational excellence across the value chain.

- Accelerated material discovery and optimization through AI-driven computational chemistry and simulations.

- Enhanced quality control and defect detection in adhesive application using machine vision and AI algorithms.

- Optimization of manufacturing processes, including curing profiles and dispensing parameters, via machine learning.

- Predictive maintenance for adhesive dispensing equipment, reducing downtime and operational costs.

- Supply chain optimization and demand forecasting for raw materials and finished adhesive products.

Key Takeaways Electronic Adhesive Market Size & Forecast

Analysis of common user questions regarding the electronic adhesive market size and forecast reveals a consistent focus on understanding the primary growth catalysts and the longevity of current expansion trends. Stakeholders are particularly interested in identifying which end-use sectors are poised for the most significant adhesive consumption growth, such as the automotive electrification segment and the expanding consumer electronics market driven by 5G and IoT adoption. There is also considerable attention paid to how technological advancements in device miniaturization and performance requirements are translating into sustained demand for specialized adhesive solutions, underscoring the market's resilience and innovative capacity.

Another key theme emerging from user inquiries is the regional dynamics influencing market expansion. Questions frequently explore which geographical areas, particularly in Asia Pacific, are leading in manufacturing and adoption, and how these regional trends impact global market projections. The forecast indicates that while traditional applications remain stable, nascent technologies and regulatory shifts will be critical in shaping the market's trajectory, emphasizing the importance of adaptability and continuous innovation for market participants. The overall sentiment points to a robust growth outlook, underpinned by ongoing technological evolution and diversified application opportunities across various high-growth industries.

- Robust growth driven by rapid advancements in consumer electronics, automotive, and telecommunications.

- Significant market expansion anticipated in Asia Pacific due to high manufacturing output and increased demand.

- Continuous innovation in adhesive properties is critical to meet evolving demands for performance and reliability.

- The transition towards electric vehicles (EVs) represents a major long-term growth catalyst for specialized adhesives.

- Sustainability and compliance with environmental regulations will increasingly influence product development and market acceptance.

Electronic Adhesive Market Drivers Analysis

The electronic adhesive market is predominantly driven by the escalating demand for advanced electronic devices across various industries. The continuous miniaturization of components and the increasing complexity of electronic assemblies necessitate high-performance adhesives that can provide reliable bonding, thermal management, and electrical conductivity within confined spaces. This trend is particularly evident in consumer electronics, where smartphones, wearables, and other portable devices require sophisticated adhesive solutions to ensure durability and functionality. Furthermore, the proliferation of Internet of Things (IoT) devices and smart home technology significantly contributes to this demand, as these devices integrate numerous sensors and micro-components that rely on specialized adhesives for their assembly and operation.

Another significant driver is the rapid growth of the automotive industry, particularly with the widespread adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS). Electronic adhesives are crucial in EV battery packs for thermal management and structural integrity, in ADAS sensors for environmental protection, and in infotainment systems for robust component integration. This shift towards automotive electrification and enhanced vehicle intelligence demands adhesives that can withstand harsh operating conditions, provide effective thermal dissipation, and ensure long-term reliability. Moreover, the telecommunications sector, driven by the rollout of 5G infrastructure, requires high-frequency and thermally conductive adhesives for base stations and network equipment, further boosting market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of Electronic Devices | +2.3% | Global, particularly Asia Pacific, North America, Europe | 2025-2033 |

| Growth in Consumer Electronics Sector | +2.0% | Asia Pacific, North America, Europe | 2025-2033 |

| Rise of Electric Vehicles (EVs) and Automotive Electronics | +2.5% | Europe, North America, China, Japan | 2025-2033 |

| Expansion of 5G Infrastructure and IoT Devices | +1.8% | Global, especially China, North America, Europe | 2025-2033 |

| Increasing Demand for High-Performance Adhesives | +0.9% | Global | 2025-2033 |

Electronic Adhesive Market Restraints Analysis

The electronic adhesive market faces several notable restraints that can impede its growth trajectory. One primary challenge is the volatility of raw material prices, particularly for key chemical components like epoxy resins, silicones, and various additives. These fluctuations are often influenced by geopolitical events, supply chain disruptions, and the global demand-supply balance for petrochemicals, leading to unpredictable production costs for adhesive manufacturers. This variability can impact profit margins, especially for smaller market players, and may lead to price instability for end-users, potentially affecting adoption rates or encouraging the search for alternative bonding technologies.

Another significant restraint involves stringent environmental regulations and the increasing emphasis on sustainability. Regulatory bodies worldwide are imposing tighter restrictions on the use of certain chemicals, such as solvents and volatile organic compounds (VOCs), due to health and environmental concerns. While this drives innovation towards greener formulations, it also necessitates substantial investment in research and development to reformulate existing products and develop new compliant adhesives. This can lead to increased R&D costs, longer product development cycles, and potential market access barriers for non-compliant products, thereby acting as a brake on market expansion. Furthermore, the high performance requirements for advanced electronic applications often require complex formulations that are difficult to make environmentally friendly, creating a constant trade-off.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.8% | Global | 2025-2033 |

| Stringent Environmental Regulations (e.g., RoHS, REACH) | -0.7% | Europe, North America, Asia Pacific | 2025-2033 |

| High Research and Development Costs | -0.5% | Global | 2025-2033 |

| Competition from Alternative Bonding Technologies | -0.4% | Global | 2025-2033 |

| Technical Challenges in Developing Advanced Formulations | -0.3% | Global | 2025-2033 |

Electronic Adhesive Market Opportunities Analysis

The electronic adhesive market is characterized by several promising opportunities that are set to fuel future growth. The continuous evolution of consumer electronics, particularly in areas like foldable displays, augmented reality (AR)/virtual reality (VR) devices, and advanced wearables, creates a persistent demand for highly flexible, optically clear, and exceptionally durable adhesives. These emerging applications require novel adhesive properties that can withstand bending, stretching, and repeated stress cycles while maintaining structural integrity and performance, presenting a significant avenue for product innovation and market penetration for manufacturers capable of developing such specialized solutions.

Another substantial opportunity lies in the expanding medical devices sector, where precision and reliability are paramount. Electronic adhesives are crucial for assembling miniature sensors, implantable devices, diagnostic equipment, and surgical instruments. The growing trend of home healthcare and portable medical devices further amplifies the need for biocompatible, sterilizable, and high-performance adhesives that can ensure patient safety and device longevity. Moreover, the increasing adoption of renewable energy systems, such as solar panels and wind turbines, presents a unique opportunity for durable, weather-resistant, and thermally stable electronic adhesives required for robust electrical connections and component protection in harsh outdoor environments. The development of advanced packaging technologies for semiconductors, including 3D packaging and chip-on-flex solutions, also creates a niche for ultra-thin, high-strength, and low-stress adhesives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Flexible and Wearable Electronics | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Growth in Medical Devices and Healthcare Electronics | +1.2% | North America, Europe, Japan | 2025-2033 |

| Advancements in Semiconductor Packaging Technologies | +1.0% | Asia Pacific, North America | 2025-2033 |

| Increasing Demand from Renewable Energy Systems | +0.8% | Europe, China, North America | 2025-2033 |

| Development of Biocompatible and Sustainable Adhesives | +0.7% | Global | 2025-2033 |

Electronic Adhesive Market Challenges Impact Analysis

The electronic adhesive market is not without its significant challenges, which require constant innovation and strategic adaptation from manufacturers. One of the primary hurdles is meeting the increasingly stringent performance requirements for advanced electronic devices. As components become smaller and more powerful, adhesives must exhibit exceptional thermal management capabilities, precise electrical conductivity or insulation, and superior mechanical strength, often under extreme operating conditions. Developing formulations that can consistently deliver these multifaceted properties without compromising other critical factors like cure time, dispense accuracy, and long-term reliability is a complex and capital-intensive endeavor, often pushing the boundaries of material science.

Another critical challenge revolves around the rapid pace of technological change within the electronics industry. New device architectures, materials, and manufacturing processes emerge frequently, requiring adhesive manufacturers to constantly innovate and adapt their product lines. This necessitates substantial investments in research and development to keep pace with evolving industry standards and customer demands. Furthermore, managing the intricate global supply chain for raw materials and finished products poses a significant logistical and economic challenge, exacerbated by geopolitical instabilities, trade disputes, and unexpected events like pandemics. Ensuring a consistent supply of high-quality, specialized raw materials while navigating regulatory complexities across different regions adds to the operational burden for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Meeting High Performance and Reliability Standards | -0.9% | Global | 2025-2033 |

| Rapid Technological Advancements in Electronics Industry | -0.7% | Global | 2025-2033 |

| Complexities in Supply Chain Management | -0.6% | Global | 2025-2033 |

| Intellectual Property Protection and Counterfeiting Risks | -0.4% | Asia Pacific, Global | 2025-2033 |

| Shortage of Skilled Labor and R&D Expertise | -0.3% | North America, Europe | 2025-2033 |

Electronic Adhesive Market - Updated Report Scope

This comprehensive report delves into the dynamics of the global electronic adhesive market, providing an in-depth analysis of market size, growth drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis based on resin type, form, end-use industry, and function, alongside regional insights, to provide a holistic view of the market's current state and future trajectory. The report also highlights the competitive landscape by profiling key market players and their strategic initiatives, ensuring a well-rounded understanding for stakeholders aiming to navigate this evolving market efficiently.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 10.5 Billion |

| Market Forecast in 2033 | USD 21.6 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Adhesives Corp, Advanced Electronic Materials Inc., Precision Polymers Ltd., TechBonds Solutions, ElectroChem Innovations, Innova Adhesives, Specialty Resins Group, OmniCoatings, DuraTech Adhesives, NexGen Materials, ProForma Compounds, BondWell Technologies, Syntronix Adhesives, FlexiBond Solutions, Quantum Adhesives, High-Purity Adhesives, Micro-Bond Systems, Eco-Bond Solutions, FutureForm Materials |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The electronic adhesive market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. This segmentation helps identify specific market niches, technological preferences, and application-specific demands, enabling stakeholders to tailor strategies and product development efforts more effectively. Analyzing the market across different dimensions such as resin type, form, end-use industry, and function reveals the intricate interdependencies and growth opportunities within this dynamic sector.

Each segment is influenced by unique technological advancements, regulatory pressures, and market demands. For instance, the choice of resin type is critical for performance characteristics, while the form of the adhesive impacts manufacturing processes. The end-use industry segment highlights the varying requirements from diverse applications, ranging from high-volume consumer electronics to specialized aerospace and medical devices. Functional segmentation, on the other hand, delineates adhesives based on their primary roles, such as electrical conductivity, thermal management, or insulation, providing insights into their specific utility in electronic assembly.

- By Resin Type: This segment includes Epoxy, Silicone, Acrylic, Polyurethane, Cyanoacrylate, and Other Resin Types, each offering distinct properties suited for various electronic applications.

- By Form: Adhesives are available in Liquid, Paste, Film, and Other Forms, catering to different dispensing methods and application requirements.

- By End-Use Industry: Key industries include Consumer Electronics (Smartphones, Tablets, Laptops, Wearables), Automotive (EV Batteries, ADAS, Infotainment), Aerospace & Defense, Medical Devices, Industrial Electronics (IoT Devices, Sensors, Control Systems), Telecommunications (5G Infrastructure), and Other End-Use Industries.

- By Function: Electronic adhesives are categorized by their functional properties, such as Conductive, Non-Conductive, Electrically Insulating, Thermally Conductive, and UV Curable, essential for specific electronic performance needs.

Regional Highlights

- Asia Pacific: This region is expected to dominate the electronic adhesive market, driven by its robust electronics manufacturing base, particularly in countries like China, Japan, South Korea, and Taiwan. The rapid expansion of consumer electronics, automotive electrification, and telecommunications infrastructure in this region significantly fuels demand.

- North America: Characterized by strong R&D capabilities and high adoption of advanced technologies, North America exhibits substantial growth, especially in aerospace & defense, medical devices, and high-performance computing applications. The region's focus on innovation and electric vehicle production contributes to market expansion.

- Europe: Europe represents a mature market with significant demand from the automotive, industrial electronics, and medical sectors. Stringent environmental regulations drive innovation towards sustainable and high-performance adhesive solutions, with countries like Germany and France being key contributors.

- Latin America: This region shows steady growth, primarily influenced by the expansion of consumer electronics manufacturing and increasing investment in automotive and industrial sectors. Brazil and Mexico are emerging as key markets.

- Middle East and Africa (MEA): The MEA market is projected to grow moderately, driven by increasing infrastructure development, digitalization initiatives, and nascent growth in the electronics assembly sector. Investments in renewable energy and telecommunications also contribute to demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electronic Adhesive Market.- Global Adhesives Corp

- Advanced Electronic Materials Inc.

- Precision Polymers Ltd.

- TechBonds Solutions

- ElectroChem Innovations

- Innova Adhesives

- Specialty Resins Group

- OmniCoatings

- DuraTech Adhesives

- NexGen Materials

- ProForma Compounds

- BondWell Technologies

- Syntronix Adhesives

- FlexiBond Solutions

- Quantum Adhesives

- High-Purity Adhesives

- Micro-Bond Systems

- Eco-Bond Solutions

- FutureForm Materials

Frequently Asked Questions

What are electronic adhesives used for?

Electronic adhesives are specialized materials used for bonding, sealing, encapsulating, and protecting components in electronic devices. They provide structural integrity, thermal management, electrical conductivity or insulation, and protection against environmental factors.

Which factors are driving the growth of the electronic adhesive market?

Key drivers include the miniaturization of electronic devices, the rapid expansion of consumer electronics, the proliferation of electric vehicles, the rollout of 5G infrastructure, and increasing demand for high-performance and reliable electronic assemblies.

What types of electronic adhesives are commonly used?

Common types include epoxy, silicone, acrylic, polyurethane, and cyanoacrylate adhesives, each offering distinct properties for various applications such as conductive bonding, thermal management, or structural integrity.

How does the automotive industry influence the electronic adhesive market?

The automotive industry significantly influences the market through the increasing adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), which require specialized adhesives for battery assembly, sensor protection, and electronic control units.

What are the key challenges faced by electronic adhesive manufacturers?

Manufacturers face challenges such as volatile raw material prices, stringent environmental regulations, high research and development costs for advanced formulations, and the need to keep pace with rapid technological changes in the electronics industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted