Electric Vehicle Charger Market

Electric Vehicle Charger Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705829 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

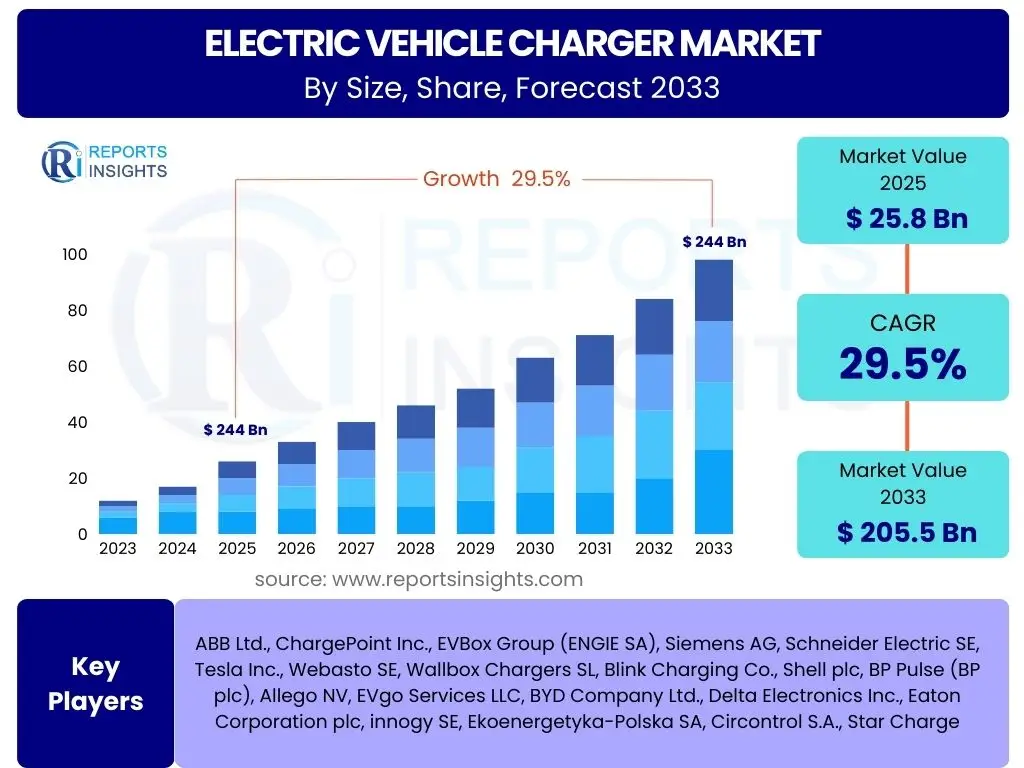

Electric Vehicle Charger Market Size

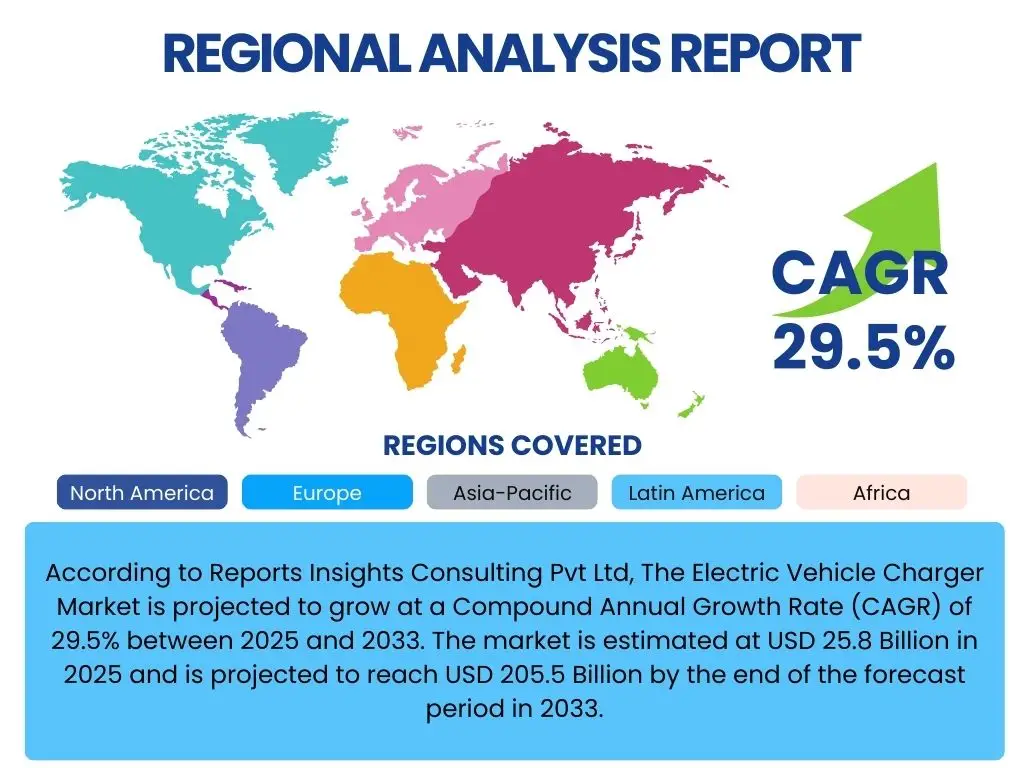

According to Reports Insights Consulting Pvt Ltd, The Electric Vehicle Charger Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 29.5% between 2025 and 2033. The market is estimated at USD 25.8 Billion in 2025 and is projected to reach USD 205.5 Billion by the end of the forecast period in 2033.

Key Electric Vehicle Charger Market Trends & Insights

The Electric Vehicle (EV) Charger Market is undergoing significant transformation, driven by a global surge in EV adoption and advancements in charging technology. Key trends indicate a strong focus on enhancing charging speed, increasing network accessibility, and integrating smart solutions for optimized energy management. Consumers and businesses are increasingly seeking reliable, efficient, and convenient charging options, pushing manufacturers and service providers to innovate rapidly. Furthermore, the market is witnessing a shift towards sustainable charging solutions, incorporating renewable energy sources and enabling vehicle-to-grid (V2G) capabilities.

Technological innovation remains at the forefront, with the development of ultra-fast DC chargers capable of significantly reducing charging times, making EVs more appealing for long-distance travel. There is also a growing emphasis on the interoperability and standardization of charging connectors and protocols to ensure a seamless user experience across different EV models and charging networks. Moreover, the integration of digital platforms for charge point management, payment solutions, and real-time availability updates is becoming standard, improving the overall efficiency and user satisfaction within the EV charging ecosystem.

- Deployment of Ultra-Fast DC Charging Stations: Increasing availability of chargers over 150 kW, significantly reducing charging times.

- Growth of Smart Charging Solutions: Integration with intelligent energy management systems for load balancing, dynamic pricing, and grid stability.

- Rise of Vehicle-to-Grid (V2G) Technology: EVs serving as mobile energy storage units, feeding power back to the grid during peak demand.

- Expansion of Public and Workplace Charging Infrastructure: Accelerated rollout of destination chargers and on-the-go charging options.

- Focus on Wireless Charging Technology: Development of inductive charging solutions for enhanced convenience, particularly for autonomous vehicles.

- Increased Adoption of Charging as a Service (CaaS) Models: Offering flexible subscription-based charging plans for individuals and fleets.

- Integration with Renewable Energy Sources: Pairing charging stations with solar or wind power to reduce carbon footprint.

AI Impact Analysis on Electric Vehicle Charger

Artificial intelligence (AI) is set to revolutionize the Electric Vehicle Charger Market by introducing unprecedented levels of efficiency, intelligence, and user-centricity. User inquiries frequently center on how AI can optimize charging processes, manage grid load, and personalize the charging experience. AI algorithms can analyze vast datasets, including vehicle charging patterns, grid demand, energy prices, and renewable energy availability, to make informed decisions that benefit both the user and the electrical grid. This proactive management capability addresses concerns about grid stability and energy costs associated with mass EV adoption.

Furthermore, AI significantly enhances the operational efficiency and reliability of charging infrastructure. Common user questions explore how AI contributes to predictive maintenance, demand forecasting, and seamless integration with smart city ecosystems. AI-powered diagnostic tools can identify potential issues in charging stations before they lead to failures, minimizing downtime and improving network reliability. For end-users, AI can provide personalized charging recommendations based on driving habits, vehicle state of charge, and preferred tariffs, thereby simplifying the charging process and reducing overall energy costs. The application of AI also extends to cybersecurity, protecting charging networks from malicious attacks and ensuring data privacy for users.

- Smart Load Balancing: AI optimizes power distribution across charging stations to prevent grid overload, especially during peak hours.

- Predictive Maintenance: AI algorithms analyze operational data to predict equipment failures, enabling proactive repairs and minimizing downtime.

- Personalized Charging Experiences: AI recommends optimal charging times and locations based on user preferences, energy prices, and driving patterns.

- Demand Forecasting: AI predicts future charging demand, allowing grid operators and charging network providers to prepare infrastructure and energy supply.

- Autonomous Charging Integration: AI facilitates communication between autonomous vehicles and charging robots for fully automated charging processes.

- Enhanced Cybersecurity: AI-driven systems detect and mitigate cyber threats to charging infrastructure and user data.

- Dynamic Pricing: AI enables real-time adjustment of charging prices based on grid conditions, energy supply, and demand.

Key Takeaways Electric Vehicle Charger Market Size & Forecast

The Electric Vehicle Charger Market is poised for exponential growth, reflecting the global commitment to sustainable transportation and the increasing mainstream adoption of electric vehicles. Key takeaways from the market size and forecast data highlight a robust expansion driven by supportive government policies, significant private sector investment in charging infrastructure, and continuous technological advancements. The projected Compound Annual Growth Rate (CAGR) underscores a dynamic period of development, with substantial opportunities for stakeholders across the value chain, from hardware manufacturers to service providers and energy utilities. This growth is intrinsically linked to efforts in decarbonization and reducing reliance on fossil fuels, making charging infrastructure a critical component of the future energy landscape.

Common user questions regarding market takeaways often revolve around the factors sustaining this rapid growth and the long-term viability of the industry. The forecast indicates that the market's trajectory will be propelled by the expanding sales of both passenger and commercial EVs, coupled with the necessity for a ubiquitous and reliable charging network. Investment in fast-charging technologies, smart grid integration, and diverse charging solutions (home, public, workplace, fleet) will be crucial. Furthermore, the market's growth is not merely about increasing numbers of chargers but also about improving the intelligence, efficiency, and accessibility of the entire charging ecosystem, ensuring a seamless experience for EV owners worldwide.

- Rapid Market Expansion: The market is projected for significant growth, driven by increasing EV sales and supportive policies.

- Infrastructure Investment Boom: Substantial capital infusion is expected in building out comprehensive public and private charging networks.

- Technological Innovation as a Core Driver: Continuous advancements in charging speed, efficiency, and smart capabilities will sustain growth.

- Policy Support Critical: Government incentives, regulations, and subsidies are foundational to accelerating market development.

- Shift Towards Smart and Integrated Solutions: Emphasis on intelligent charging, grid integration, and renewable energy linkages.

Electric Vehicle Charger Market Drivers Analysis

The Electric Vehicle Charger Market is significantly propelled by several synergistic factors that collectively create a robust growth environment. Foremost among these is the escalating global adoption of electric vehicles, fueled by growing environmental consciousness and a desire to mitigate climate change impacts. Governments worldwide are introducing stringent emission standards and offering various incentives, such as tax credits, subsidies, and preferential parking, to encourage EV purchases. This increasing EV fleet naturally necessitates a corresponding expansion of charging infrastructure to support widespread usability and alleviate range anxiety among potential buyers.

Beyond the direct increase in EV sales, technological advancements in battery technology, which provide longer ranges and faster charging capabilities, also indirectly drive the demand for more efficient and powerful chargers. The development of smart grid technologies and the integration of renewable energy sources further support the expansion of the charging ecosystem by offering sustainable and optimized power delivery solutions. Additionally, urbanization trends and the development of smart cities are creating concentrated areas where public and commercial charging solutions are essential, driving infrastructure development in dense populations.

The automotive industry's massive investment in EV models, from entry-level sedans to commercial trucks, ensures a continuous supply of vehicles requiring charging services. This industry-wide pivot, combined with global efforts to reduce reliance on fossil fuels and achieve net-zero emissions targets, positions the EV charger market for sustained, high-growth trajectory. The growing recognition of charging as a critical utility, similar to gasoline stations, is prompting utilities and private entities to invest heavily in building out robust and accessible charging networks.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Electric Vehicle Adoption | +8.5% | North America, Europe, Asia Pacific | Short-to-Mid Term |

| Supportive Government Policies & Incentives | +7.2% | Europe, China, US, Japan | Short-to-Mid Term |

| Growing Demand for Fast Charging Technology | +6.8% | Global | Mid Term |

| Expanding Charging Infrastructure Networks | +6.0% | Emerging Economies, Developed Markets | Mid-to-Long Term |

| Integration with Smart Grid Solutions | +5.5% | Europe, North America, Advanced APAC | Mid-to-Long Term |

Electric Vehicle Charger Market Restraints Analysis

Despite the promising growth trajectory, the Electric Vehicle Charger Market faces several significant restraints that could potentially impede its full potential. One primary challenge is the high upfront cost associated with the installation of charging infrastructure, particularly for fast-charging DC stations, which require substantial capital investment for equipment, grid connection upgrades, and land acquisition. This financial barrier can deter potential investors and slow down the expansion of charging networks, especially in regions with limited government subsidies or private funding.

Another critical restraint is the existing limitations and lack of readiness of current electrical grid infrastructure in many areas to support a massive influx of EV charging demand. Upgrading grid capacity, particularly at local distribution levels, is a complex, time-consuming, and expensive endeavor. Without sufficient grid improvements, widespread EV adoption could lead to grid instability, localized power outages, or increased electricity costs, discouraging EV uptake and charger deployment. Furthermore, the absence of global standardization for charging connectors and communication protocols creates fragmentation, leading to compatibility issues and a less seamless experience for EV owners, which can hinder market growth.

Consumer concerns such as range anxiety, although diminishing, still persist, alongside the perceived long charging times for certain EV models. While fast-charging technologies are addressing this, the existing infrastructure might not always meet immediate charging needs, particularly in underserved rural areas or during peak travel periods. Moreover, the complexities of obtaining permits and navigating regulatory frameworks for new charging installations can be a bureaucratic hurdle, adding to the time and cost involved in deploying new charging points. Addressing these multifaceted restraints will be essential for sustained market acceleration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Installation Costs | -4.5% | Developing Regions, Private Businesses | Short-to-Mid Term |

| Limitations of Existing Grid Infrastructure | -3.8% | Global, Specific Urban/Rural Areas | Mid-to-Long Term |

| Lack of Global Standardization for Connectors & Protocols | -3.0% | Global | Short-to-Mid Term |

| Long Charging Times & Range Anxiety Concerns | -2.5% | Early Adopters, Rural Areas | Short Term |

| Complex Permitting and Regulatory Hurdles | -2.0% | Country-specific, Local Governments | Ongoing |

Electric Vehicle Charger Market Opportunities Analysis

The Electric Vehicle Charger Market presents a multitude of compelling opportunities for growth and innovation, driven by evolving technological landscapes and increasing consumer acceptance. A significant opportunity lies in the burgeoning integration of EV charging infrastructure with renewable energy sources. This synergy not only enhances the environmental credentials of EVs but also contributes to grid stability by utilizing clean, decentralized power generation. Developing solutions that enable smart charging, where vehicles draw power during off-peak hours or when renewable energy is abundant, can unlock substantial value for both consumers and utilities.

Another promising avenue is the expansion into commercial and fleet electrification. Businesses, including logistics companies, public transport operators, and corporate fleets, are rapidly transitioning to EVs to reduce operational costs and meet sustainability targets. This segment offers a substantial market for specialized charging solutions, including depot charging, fast charging for high-utilization vehicles, and integrated energy management systems. The development of Vehicle-to-Grid (V2G) and Vehicle-to-Home (V2H) technologies represents a long-term opportunity, allowing EVs to serve as distributed energy resources, providing power back to the grid or individual homes, thereby enhancing grid resilience and creating new revenue streams for EV owners.

Furthermore, the growth of smart cities and the push for urban sustainability initiatives create fertile ground for the deployment of advanced public charging solutions. This includes integrating chargers into streetlights, parking structures, and public amenities, making charging more accessible and convenient. The potential for innovative business models, such as charging as a service (CaaS), where customers pay a subscription fee for charging, also presents a lucrative opportunity to lower the entry barrier for EV adoption and ensure a consistent revenue stream for service providers. Lastly, underserved markets, particularly in developing economies, represent untapped potential for basic and commercial charging infrastructure as EV adoption gradually accelerates in these regions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of EV Charging with Renewable Energy | +7.0% | Europe, North America, Advanced APAC | Mid-to-Long Term |

| Development of Vehicle-to-Grid (V2G) Technology | +6.5% | Developed Markets (e.g., US, Japan, Europe) | Long Term |

| Electrification of Commercial Fleets and Public Transport | +8.0% | Global | Mid Term |

| Expansion into Underserved Residential & Rural Markets | +5.5% | Emerging Economies, Rural Areas | Mid-to-Long Term |

| New Business Models (e.g., Charging as a Service) | +6.2% | Global | Mid Term |

Electric Vehicle Charger Market Challenges Impact Analysis

The Electric Vehicle Charger Market, while booming, is not without its significant challenges that demand innovative solutions and strategic planning. One prominent challenge is ensuring the cybersecurity of charging networks and user data. As charging stations become increasingly connected and integrated with smart grids, they become potential targets for cyberattacks, risking data breaches, service disruptions, and even grid instability. Protecting this critical infrastructure requires continuous investment in robust cybersecurity measures and compliance with evolving data privacy regulations.

Another major challenge involves navigating the complexities of land acquisition and the availability of suitable sites for new charging stations, especially in densely populated urban areas where space is limited and property costs are high. This challenge is compounded by the often lengthy and intricate processes for obtaining permits and connecting to the grid, which can significantly delay deployment timelines. Furthermore, the global supply chain for critical components, such as semiconductors and raw materials for batteries and power electronics, remains vulnerable to disruptions, which can impact the manufacturing and deployment of charging equipment, leading to increased costs and delivery delays.

Regulatory fragmentation and the absence of harmonized technical standards across different regions and countries pose significant hurdles. This lack of uniformity can complicate cross-border EV travel, increase manufacturing costs for global players, and slow down market penetration due to compatibility issues. Lastly, the dynamic nature of EV technology, with continuous advancements in battery chemistries and charging protocols, means that charging infrastructure must remain adaptable and future-proof, which presents ongoing investment and upgrade challenges for network operators. Overcoming these challenges is crucial for fostering a resilient and rapidly expanding EV charging ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats to Charging Infrastructure | -3.5% | Global | Ongoing |

| Land Availability & Permitting Complexities | -3.0% | Urban Areas, Dense Populations | Mid-to-Long Term |

| Supply Chain Disruptions for Key Components | -2.8% | Global | Short-to-Mid Term |

| Regulatory Fragmentation & Lack of Harmonized Standards | -2.2% | Country-specific, Regional Blocs | Ongoing |

| Technological Obsolescence & Need for Future-Proofing | -1.8% | Global | Mid-to-Long Term |

Electric Vehicle Charger Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Electric Vehicle Charger Market, providing a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges. It encompasses a thorough segmentation analysis across various dimensions, including charger type, application, charging level, connector type, installation type, and end use. The report provides regional insights, highlighting key growth markets and their unique dynamics. Furthermore, it profiles leading market players, offering a competitive landscape assessment and strategic insights for stakeholders. The objective is to equip businesses with actionable intelligence to navigate the evolving market, identify investment opportunities, and formulate effective growth strategies within the global EV charging ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.8 Billion |

| Market Forecast in 2033 | USD 205.5 Billion |

| Growth Rate | 29.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., ChargePoint Inc., EVBox Group (ENGIE SA), Siemens AG, Schneider Electric SE, Tesla Inc., Webasto SE, Wallbox Chargers SL, Blink Charging Co., Shell plc, BP Pulse (BP plc), Allego NV, EVgo Services LLC, BYD Company Ltd., Delta Electronics Inc., Eaton Corporation plc, innogy SE, Ekoenergetyka-Polska SA, Circontrol S.A., Star Charge |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electric Vehicle Charger Market is meticulously segmented to provide a granular understanding of its diverse components and market dynamics. This segmentation is crucial for stakeholders to identify specific growth areas, target audiences, and technological preferences within the expansive EV ecosystem. The market can be dissected based on charger type, distinguishing between slower AC chargers suitable for residential and workplace use, and rapid DC chargers essential for public and commercial applications. Further breakdowns by application reveal the demand patterns from private vehicle owners, commercial fleets, and public charging networks, each with unique requirements and deployment scales.

Additional segmentation by charging level (Level 1, Level 2, and Level 3) allows for an analysis of market preference based on charging speed and infrastructure requirements. Connector type segmentation highlights the regional variations and ongoing efforts towards standardization, while installation type provides insights into deployment flexibility. The end-use segment identifies the diverse sectors utilizing EV chargers, from personal automotive to heavy-duty commercial vehicles, offering a comprehensive view of market penetration and future opportunities across various industries. This detailed approach enables a precise assessment of market size, growth drivers, and competitive landscapes within each niche, facilitating informed strategic decisions.

- By Charger Type:

- AC Chargers: Primarily used for residential and workplace charging, offering slower but more affordable solutions. Includes Level 1 and Level 2 chargers.

- DC Chargers: Known as fast chargers, used for public and commercial applications due to their ability to charge vehicles rapidly. Categorized as Level 3.

- By Application:

- Commercial: Encompasses public charging stations, fleet depots, workplace charging, and charging facilities at retail and hospitality venues.

- Residential: Chargers installed in private homes for personal EV charging.

- By Charging Level:

- Level 1: Standard household outlet charging, typically slow.

- Level 2: Faster AC charging, commonly found in homes, workplaces, and public areas.

- Level 3 (DC Fast Charging): High-power DC charging, providing rapid charging for on-the-go needs.

- By Connector Type:

- Type 1 (J1772): Predominant in North America and Japan for AC charging.

- Type 2 (Mennekes): Standard for AC charging in Europe.

- CCS (Combined Charging System): A combined AC and DC charging standard, common in North America and Europe.

- CHAdeMO: A DC fast-charging standard, prevalent in Japan.

- Tesla Connector: Proprietary connector used by Tesla vehicles.

- GB/T: Standard for EV charging in China.

- By Installation Type:

- Wall-mounted: Fixed installations, common in residential and commercial settings.

- Pedestal: Standalone units, often found in public and commercial parking areas.

- Portable: Mobile charging units for emergency or temporary use.

- By End Use:

- Automotive: Charging solutions for passenger electric vehicles.

- Commercial Vehicles: Chargers for electric buses, trucks, and other fleet vehicles.

- Marine: Charging infrastructure for electric boats and maritime vessels.

- Aerospace: Emerging segment for electric aircraft charging.

Regional Highlights

- North America: Driven by aggressive federal and state government incentives, increasing consumer awareness, and significant investments by automotive manufacturers in EV production. The United States leads the region with substantial public and private sector funding for charging infrastructure expansion, focusing on both residential and public fast-charging networks. Canada is also making strides with strong policy support and growing EV adoption.

- Europe: A frontrunner in EV adoption and charging infrastructure development, propelled by stringent emission regulations and ambitious decarbonization targets set by the European Union. Countries like Norway, Germany, the Netherlands, and the UK are witnessing rapid deployment of smart charging solutions, V2G initiatives, and integrated renewable energy charging. Government subsidies and a high density of public charging points contribute significantly to market growth.

- Asia Pacific (APAC): Represents the largest and fastest-growing market, primarily led by China, which boasts the world's largest EV market and a robust charging infrastructure. Government support, large-scale manufacturing capabilities, and rapid urbanization are key drivers. South Korea and Japan are also investing heavily in advanced charging technologies, while India is emerging as a significant market with increasing EV penetration and charging station rollouts, though it faces challenges in infrastructure readiness.

- Latin America: An emerging market with gradual but increasing EV adoption. Growth is influenced by pilot projects, government initiatives to promote sustainable transport, and foreign investments in charging infrastructure. Brazil and Mexico are leading the region, focusing on public transport electrification and initial charging network build-outs in major cities.

- Middle East and Africa (MEA): This region is in the nascent stages of EV charger market development, with growth largely concentrated in Gulf Cooperation Council (GCC) countries like UAE and Saudi Arabia, driven by diversification efforts away from oil and gas, smart city initiatives, and luxury EV demand. Africa's market is still limited but holds long-term potential with increasing awareness and economic development in key nations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electric Vehicle Charger Market.- ABB Ltd.

- ChargePoint Inc.

- EVBox Group (ENGIE SA)

- Siemens AG

- Schneider Electric SE

- Tesla Inc.

- Webasto SE

- Wallbox Chargers SL

- Blink Charging Co.

- Shell plc

- BP Pulse (BP plc)

- Allego NV

- EVgo Services LLC

- BYD Company Ltd.

- Delta Electronics Inc.

- Eaton Corporation plc

- innogy SE

- Ekoenergetyka-Polska SA

- Circontrol S.A.

- Star Charge

Frequently Asked Questions

Analyze common user questions about the Electric Vehicle Charger market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Electric Vehicle Charger Market?

The Electric Vehicle Charger Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 29.5% between 2025 and 2033, reaching an estimated USD 205.5 Billion by 2033 from USD 25.8 Billion in 2025.

What are the primary drivers for the Electric Vehicle Charger Market?

Key drivers include the increasing global adoption of electric vehicles, supportive government policies and incentives, the growing demand for fast-charging technology, and the continuous expansion of charging infrastructure networks worldwide.

How does AI impact the Electric Vehicle Charger Market?

AI significantly impacts the market by enabling smart load balancing, predictive maintenance of charging stations, personalized charging experiences for users, accurate demand forecasting, and enhanced cybersecurity across the charging network.

What are the key challenges facing the Electric Vehicle Charger Market?

Major challenges include high upfront installation costs, limitations of existing grid infrastructure, lack of global standardization for connectors and protocols, complex permitting processes, and vulnerabilities within the supply chain.

Which regions are expected to dominate the Electric Vehicle Charger Market?

Asia Pacific, particularly China, is expected to remain the largest and fastest-growing market. Europe and North America are also significant regions, driven by strong government support and high EV adoption rates.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted