Electric Power Distribution Equipment Market

Electric Power Distribution Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703861 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

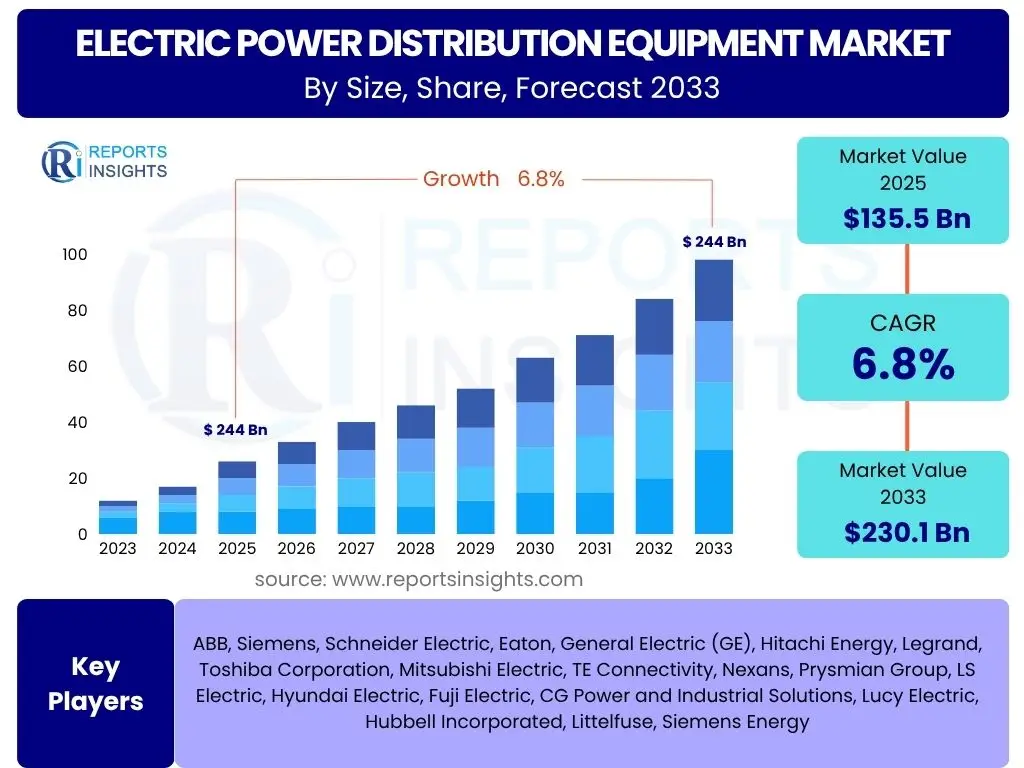

Electric Power Distribution Equipment Market Size

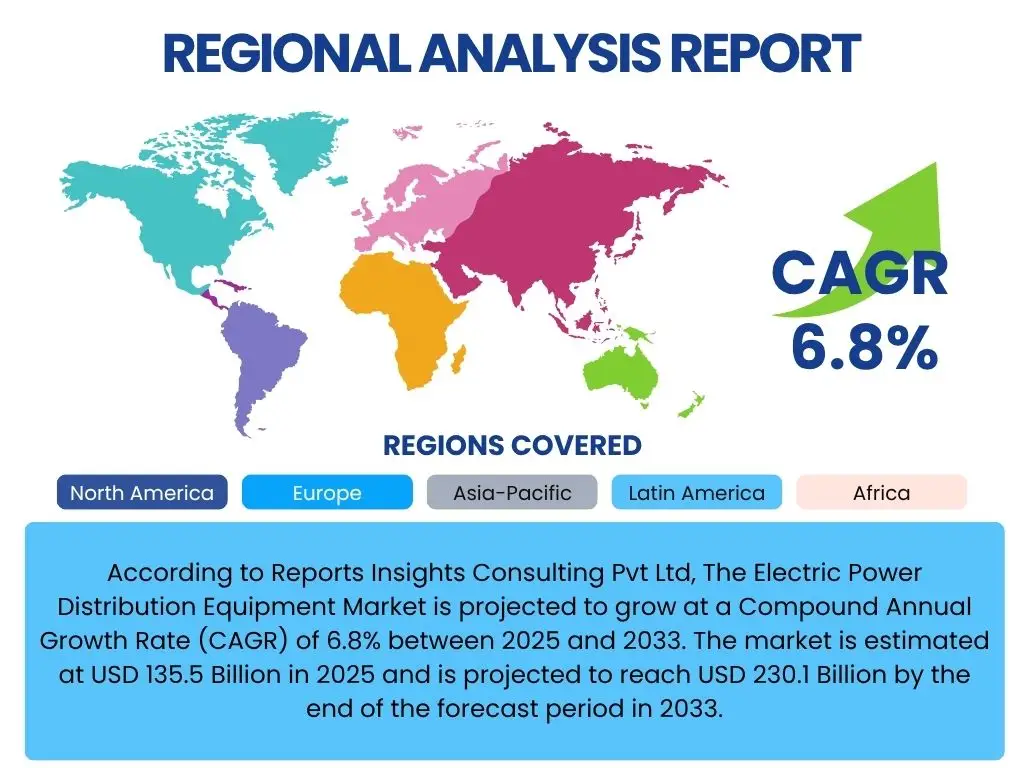

According to Reports Insights Consulting Pvt Ltd, The Electric Power Distribution Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 135.5 Billion in 2025 and is projected to reach USD 230.1 Billion by the end of the forecast period in 2033.

Key Electric Power Distribution Equipment Market Trends & Insights

The Electric Power Distribution Equipment market is undergoing significant transformation driven by global energy transition efforts, rapid technological advancements, and the imperative for grid modernization. Users frequently inquire about the integration of renewable energy sources, the proliferation of smart grid technologies, and the increasing demand for resilient and efficient power infrastructure. Key insights point towards a shift from traditional, centralized grids to more decentralized, intelligent systems capable of handling bidirectional power flow and distributed energy resources. The market is also seeing trends towards digitalization and automation, enhancing operational efficiency and reliability across the distribution network.

Another prominent trend observed is the growing emphasis on sustainable and eco-friendly equipment solutions. This includes the adoption of gas-insulated switchgear (GIS) with alternative insulating gases to sulfur hexafluoride (SF6), as well as the development of compact and modular substation designs. The increasing electrification of transportation, particularly the surge in electric vehicle (EV) adoption, is placing new demands on existing distribution networks, necessitating upgrades and expansion of charging infrastructure and related distribution equipment. Furthermore, the imperative for enhanced grid cybersecurity is influencing equipment design and system integration.

- Smart grid technology integration for enhanced monitoring and control.

- Increased adoption of renewable energy sources leading to grid modernization.

- Decentralization of power generation with microgrid development.

- Demand for resilient and reliable power infrastructure.

- Digitalization and automation of distribution networks.

- Transition towards eco-friendly and sustainable equipment.

- Growth in electric vehicle charging infrastructure deployment.

- Focus on cybersecurity solutions for grid protection.

- Development of compact and modular substation designs.

AI Impact Analysis on Electric Power Distribution Equipment

The impact of Artificial Intelligence (AI) on the Electric Power Distribution Equipment market is a subject of intense interest, with common user questions revolving around its potential to optimize grid operations, enhance predictive maintenance, and improve overall system reliability. Users anticipate that AI will revolutionize how distribution networks are managed, enabling more precise demand forecasting, proactive fault detection, and automated responses to grid disturbances. There is a strong expectation that AI will lead to significant operational efficiencies and cost reductions by minimizing downtime and extending the lifespan of critical equipment through data-driven insights.

Concerns often raised include the complexity of integrating AI systems with legacy infrastructure, the need for robust data security and privacy protocols, and the potential impact on workforce skills and roles. Despite these challenges, the prevailing sentiment is that AI will be a transformative force, enabling smarter, more resilient, and self-healing grids. Its application in real-time load balancing, optimized energy routing, and proactive asset management is expected to drive substantial advancements in the functionality and performance of power distribution equipment, moving towards more autonomous and intelligent distribution systems.

- Enhanced predictive maintenance and fault detection for equipment.

- Optimization of grid operations and energy flow.

- Improved demand forecasting and load balancing.

- Real-time monitoring and anomaly detection in distribution networks.

- Automated decision-making for grid resilience.

- Increased energy efficiency through optimized asset utilization.

- Development of self-healing grid capabilities.

- Cybersecurity enhancements through AI-driven threat analysis.

- Potential for autonomous control of certain distribution assets.

Key Takeaways Electric Power Distribution Equipment Market Size & Forecast

The Electric Power Distribution Equipment market is poised for robust expansion, driven by an accelerating global energy transition and a persistent need for modernizing aging infrastructure. Common inquiries highlight the significance of investments in smart grid technologies, the integration of distributed renewable energy sources, and the electrification of various sectors as primary growth catalysts. The market forecast indicates a sustained growth trajectory, reflecting the essential role of efficient and reliable power distribution in supporting economic development and achieving sustainability goals worldwide. Strategic investments in advanced equipment and digital solutions will be crucial for stakeholders to capitalize on this growth.

A key takeaway from the market analysis is the shift in investment focus towards resilience and sustainability. Governments and utilities are increasingly prioritizing projects that enhance grid robustness against extreme weather events and cyber threats, while also promoting eco-friendly equipment solutions. Furthermore, the rapid expansion of industrial and commercial sectors in emerging economies, coupled with significant urbanization trends, will continue to fuel demand for new distribution infrastructure. This comprehensive growth is expected to create numerous opportunities for technological innovation and market entry across the value chain.

- Strong market growth anticipated driven by energy transition and infrastructure upgrades.

- Smart grid technologies and renewable energy integration are key growth enablers.

- Increased electrification across industries and transportation sectors.

- Significant investment in grid resilience and sustainability.

- Emerging economies present substantial growth opportunities.

- Technological advancements in equipment design and digital solutions.

- Focus on efficiency and reliability of power distribution networks.

- Shift towards decentralized and intelligent grid architectures.

- Opportunities for retrofitting and upgrading existing infrastructure.

Electric Power Distribution Equipment Market Drivers Analysis

The Electric Power Distribution Equipment market is profoundly influenced by several key drivers that are collectively propelling its growth. The escalating global demand for electricity, fueled by rapid urbanization, industrialization, and population growth, necessitates continuous expansion and upgrading of existing distribution networks. This demand is further amplified by the widespread adoption of digital technologies and electric vehicles, which place increased load and complexity on power grids. Consequently, utilities and grid operators are compelled to invest in new and advanced distribution equipment to maintain reliable and efficient power supply.

Another significant driver is the global push towards integrating renewable energy sources such as solar and wind into national grids. This transition requires sophisticated distribution equipment capable of handling intermittent and bidirectional power flows, as well as smart grid technologies for effective management and balancing. Government initiatives and supportive policies promoting grid modernization, energy efficiency, and reduction of carbon emissions also play a crucial role, often providing financial incentives and regulatory frameworks that encourage investment in advanced distribution infrastructure.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Electricity Demand | +1.2% | Asia Pacific, North America, Europe | Short to Long-term (2025-2033) |

| Integration of Renewable Energy Sources | +1.0% | Europe, Asia Pacific, North America | Medium to Long-term (2026-2033) |

| Grid Modernization and Smart Grid Initiatives | +0.9% | North America, Europe, China, India | Medium-term (2025-2030) |

| Government Policies and Infrastructure Spending | +0.8% | Globally, especially Emerging Economies | Short to Medium-term (2025-2029) |

Electric Power Distribution Equipment Market Restraints Analysis

Despite significant growth prospects, the Electric Power Distribution Equipment market faces several restraints that could impede its full potential. One primary challenge is the substantial capital expenditure required for grid infrastructure development and equipment procurement. The high initial investment costs associated with upgrading or building new distribution networks can be a deterrent for utilities, particularly in developing regions where financial resources may be limited. This often leads to deferred projects or reliance on outdated equipment, slowing down modernization efforts.

Another significant restraint involves complex and varying regulatory frameworks across different countries and regions. These regulations can create hurdles for the adoption of new technologies, impose stringent compliance requirements, and prolong project approval processes, thereby increasing lead times and operational costs for manufacturers and service providers. Furthermore, the inherent longevity of distribution equipment often means that replacement cycles are long, leading to a slower adoption rate for newer, more advanced technologies. Supply chain disruptions, often exacerbated by geopolitical tensions and global events, can also pose a significant challenge, affecting the availability and cost of raw materials and components, leading to project delays and increased prices.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure Requirements | -0.7% | Globally, particularly Developing Nations | Long-term (2025-2033) |

| Complex Regulatory Frameworks | -0.5% | Europe, North America, India | Short to Medium-term (2025-2030) |

| Long Replacement Cycles of Existing Infrastructure | -0.4% | Developed Economies | Long-term (2025-2033) |

| Supply Chain Volatility and Raw Material Costs | -0.6% | Globally | Short to Medium-term (2025-2028) |

Electric Power Distribution Equipment Market Opportunities Analysis

Significant opportunities exist within the Electric Power Distribution Equipment market, primarily driven by the ongoing global energy transition and the increasing focus on grid resilience. The rapid development and deployment of smart grid technologies, including advanced metering infrastructure (AMI), intelligent substations, and self-healing networks, present a lucrative avenue for equipment manufacturers. These technologies require sophisticated communication-enabled distribution equipment, opening new product development and market penetration opportunities. Furthermore, the growing adoption of distributed energy resources (DERs) like rooftop solar and battery storage creates demand for new types of bidirectional transformers, advanced inverters, and sophisticated control systems at the edge of the grid.

The expansion of electric vehicle (EV) charging infrastructure represents another substantial growth opportunity. As more EVs hit the roads, the existing distribution networks will need significant upgrades and expansion, including new transformers, switchgear, and cabling capable of handling increased localized loads. Moreover, the aging power infrastructure in developed economies presents a continuous demand for replacement and modernization, fostering opportunities for smart retrofits and upgrades. Emerging economies, undergoing rapid industrialization and urbanization, offer greenfield opportunities for building entirely new and modern power distribution networks, incorporating the latest technologies from the outset.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Smart Grid and Digitalization Initiatives | +1.5% | Globally, especially Developed Regions | Medium to Long-term (2026-2033) |

| Growth of Electric Vehicle Charging Infrastructure | +1.3% | North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Integration of Distributed Energy Resources (DERs) | +1.1% | Europe, North America, Australia | Medium-term (2025-2030) |

| Infrastructure Modernization in Emerging Economies | +1.0% | Asia Pacific, Latin America, MEA | Long-term (2027-2033) |

Electric Power Distribution Equipment Market Challenges Impact Analysis

The Electric Power Distribution Equipment market faces several formidable challenges that require innovative solutions and strategic planning. One significant challenge is the increasing complexity of grid management due to the proliferation of distributed energy resources (DERs) and the bidirectional flow of power. Integrating these diverse sources while maintaining grid stability and power quality presents significant technical hurdles for existing distribution equipment and control systems. This complexity demands more intelligent and adaptable equipment, often requiring substantial research and development investments.

Another critical challenge is the escalating threat of cyberattacks on critical infrastructure. As distribution networks become more digitalized and interconnected, they become more vulnerable to cyber threats that could disrupt operations, compromise data integrity, or even cause widespread power outages. Ensuring robust cybersecurity measures are embedded into new and existing distribution equipment is paramount, requiring continuous vigilance and investment. Furthermore, the global shortage of skilled labor, particularly in power engineering and smart grid technologies, poses a significant operational challenge, impacting equipment installation, maintenance, and the pace of grid modernization efforts. Addressing these challenges will be crucial for the sustained growth and evolution of the power distribution equipment sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration Complexity of Distributed Energy Resources | -0.8% | Globally, particularly Developed Grids | Medium-term (2025-2030) |

| Increasing Cybersecurity Threats | -0.7% | Globally | Short to Long-term (2025-2033) |

| Shortage of Skilled Workforce | -0.6% | North America, Europe | Long-term (2025-2033) |

| Aging Infrastructure and Retrofit Challenges | -0.5% | Developed Economies | Long-term (2025-2033) |

Electric Power Distribution Equipment Market - Updated Report Scope

This report provides a comprehensive analysis of the Electric Power Distribution Equipment market, detailing its current size, historical performance, and future growth projections through 2033. It examines key market trends, identifies critical drivers, restraints, opportunities, and challenges influencing market dynamics. The scope includes an in-depth segmentation analysis by product type, application, voltage level, and end-user, alongside a thorough regional assessment to provide a holistic view of the market landscape. Furthermore, the report offers insights into the competitive landscape, profiling leading players and their strategic initiatives, and includes an analysis of AI's transformative impact on the sector. This comprehensive scope aims to equip stakeholders with actionable insights for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 135.5 Billion |

| Market Forecast in 2033 | USD 230.1 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens, Schneider Electric, Eaton, General Electric (GE), Hitachi Energy, Legrand, Toshiba Corporation, Mitsubishi Electric, TE Connectivity, Nexans, Prysmian Group, LS Electric, Hyundai Electric, Fuji Electric, CG Power and Industrial Solutions, Lucy Electric, Hubbell Incorporated, Littelfuse, Siemens Energy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electric Power Distribution Equipment market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation highlights the various types of equipment deployed across the distribution network, the voltage levels at which they operate, and the specific end-user sectors they serve. Understanding these segments is crucial for identifying niche markets, assessing competitive landscapes, and tailoring product development strategies to meet specific industry needs. The intricate interplay between product categories and their end-use applications defines the market's structure and growth opportunities.

The detailed breakdown by product type, such as transformers, switchgear, and protective relays, allows for an analysis of demand drivers and technological advancements specific to each component. Furthermore, segmenting by voltage level differentiates the equipment designed for local residential networks versus larger industrial or utility-scale distribution. The application and end-user segmentation provides insights into consumption patterns across residential, commercial, industrial, and utility sectors, reflecting varying requirements for reliability, efficiency, and smart functionalities. This multi-dimensional segmentation enables a precise evaluation of market dynamics and future potential across the entire value chain.

- By Product Type: Transformers, Switchgear, Relays, Capacitors, Insulators, Conductors and Cables, Meters, Voltage Regulators, Surge Arresters, Others.

- By Voltage Level: Low Voltage, Medium Voltage, High Voltage.

- By Application: Residential, Commercial, Industrial, Utility.

- By End-User: Utilities, Industrial, Commercial, Residential.

Regional Highlights

- North America: The region is characterized by substantial investments in grid modernization and aging infrastructure replacement. Driven by smart grid initiatives and increasing renewable energy integration, particularly in the United States and Canada, there is high demand for advanced distribution equipment, including smart meters and intelligent transformers.

- Europe: Europe is at the forefront of the energy transition, with ambitious targets for renewable energy deployment and carbon reduction. This drives significant demand for sustainable and highly efficient distribution equipment. Countries like Germany, France, and the UK are heavily investing in smart grid technologies and decentralized energy systems, fostering innovation in the distribution equipment sector.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market due to rapid urbanization, industrialization, and massive infrastructure development projects, especially in China and India. The increasing electricity demand, coupled with government initiatives for rural electrification and smart city development, fuels the expansion of distribution networks and the adoption of new equipment.

- Latin America: Countries such as Brazil and Mexico are experiencing growth in their power sectors, driven by expanding industrial bases and increasing residential electricity consumption. Investments in grid expansion and efforts to reduce transmission and distribution losses are key drivers for the distribution equipment market in this region.

- Middle East and Africa (MEA): The MEA region is witnessing significant investment in power infrastructure to meet the growing energy demands from rapidly expanding populations and industrialization. Renewable energy projects, particularly solar in the Middle East and hydropower in Africa, are also contributing to the demand for modern distribution equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electric Power Distribution Equipment Market.- ABB

- Siemens

- Schneider Electric

- Eaton

- General Electric (GE)

- Hitachi Energy

- Legrand

- Toshiba Corporation

- Mitsubishi Electric

- TE Connectivity

- Nexans

- Prysmian Group

- LS Electric

- Hyundai Electric

- Fuji Electric

- CG Power and Industrial Solutions

- Lucy Electric

- Hubbell Incorporated

- Littelfuse

- Siemens Energy

Frequently Asked Questions

Analyze common user questions about the Electric Power Distribution Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Electric Power Distribution Equipment Market?

The Electric Power Distribution Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 230.1 Billion by 2033.

What are the primary drivers for the Electric Power Distribution Equipment Market?

Key drivers include growing global electricity demand, the integration of renewable energy sources, grid modernization and smart grid initiatives, and supportive government policies for infrastructure development.

How is AI impacting the Electric Power Distribution Equipment sector?

AI is transforming the sector by enabling enhanced predictive maintenance, optimizing grid operations, improving demand forecasting, and facilitating the development of self-healing grids for greater efficiency and reliability.

Which regions are expected to show significant growth in this market?

The Asia Pacific region, particularly China and India, is expected to exhibit the fastest growth due to rapid industrialization, urbanization, and increasing electricity demand, alongside strong growth in North America and Europe driven by grid modernization.

What are the main challenges faced by the Electric Power Distribution Equipment Market?

Major challenges include the complexity of integrating distributed energy resources, increasing cybersecurity threats to interconnected grids, and a global shortage of skilled workforce in power engineering and smart grid technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted