Electric Motor Market

Electric Motor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704961 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

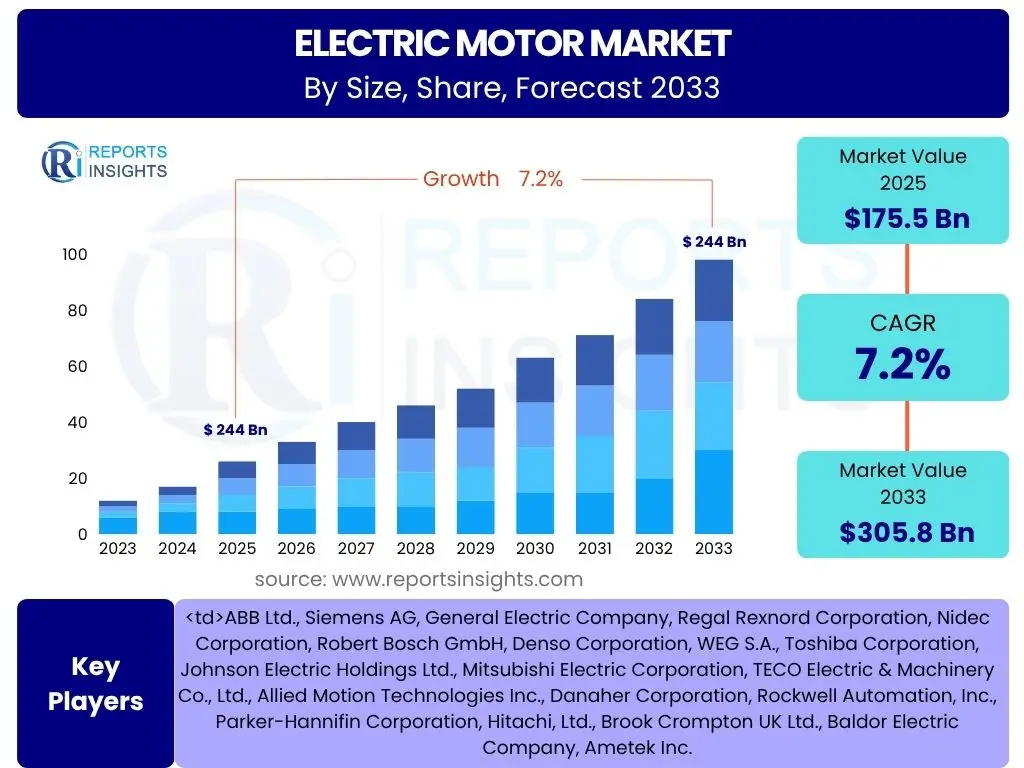

Electric Motor Market Size

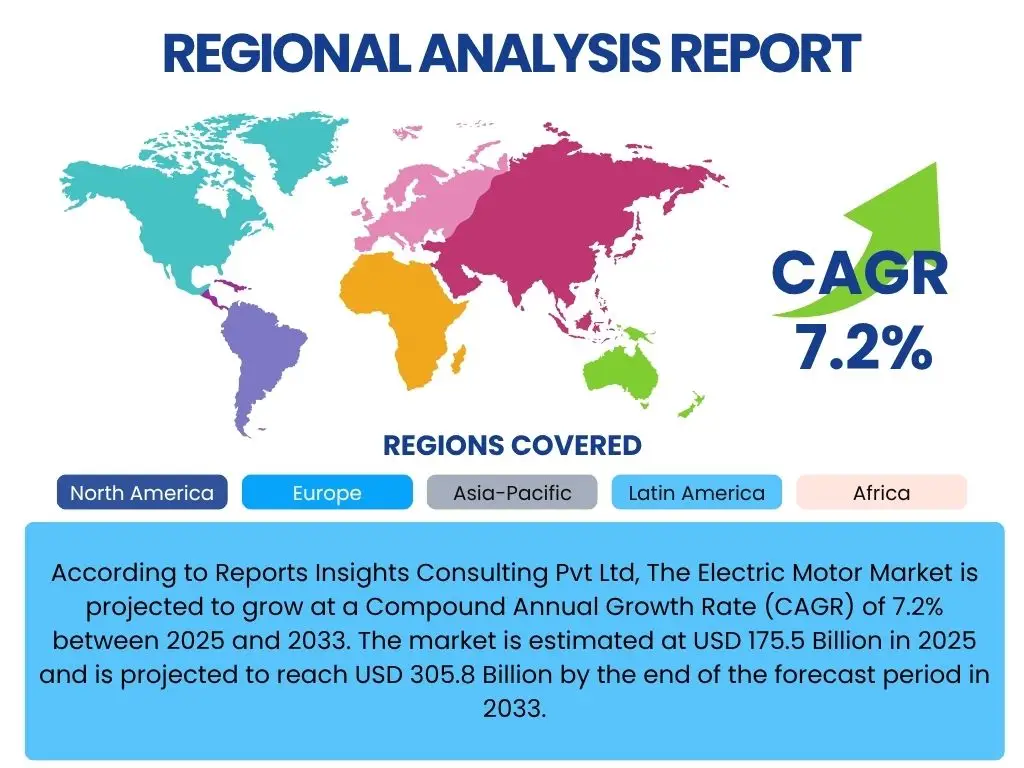

According to Reports Insights Consulting Pvt Ltd, The Electric Motor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 175.5 Billion in 2025 and is projected to reach USD 305.8 Billion by the end of the forecast period in 2033.

Key Electric Motor Market Trends & Insights

The electric motor market is experiencing significant transformation, driven by global shifts towards energy efficiency, automation, and sustainable transportation. User inquiries consistently highlight interest in how technological advancements and evolving regulatory landscapes are shaping product development and market demand. There is a strong focus on the adoption of advanced motor technologies such as Brushless DC (BLDC) motors and servo motors, which offer superior performance, energy efficiency, and compact designs, making them ideal for a wide range of applications from electric vehicles to precision robotics. Furthermore, the integration of smart functionalities and connectivity is emerging as a critical trend, enabling predictive maintenance and enhanced operational control.

Another prominent area of interest pertains to the impact of electrification across various sectors. The burgeoning electric vehicle (EV) industry is a primary catalyst, demanding high-performance, compact, and reliable electric motors. Simultaneously, industrial automation and robotics continue to drive demand for precise and efficient motors, supporting the Industry 4.0 paradigm. Users are also keen to understand the role of new materials and manufacturing techniques, such as additive manufacturing, in creating lighter, more durable, and more efficient motors, reducing the overall environmental footprint and operational costs.

- Increased demand for high-efficiency motors due to stringent energy regulations.

- Proliferation of electric vehicles (EVs) driving innovation in automotive motor designs.

- Growing adoption of automation and robotics in manufacturing sectors globally.

- Miniaturization and compact designs for motors in consumer electronics and medical devices.

- Integration of smart features, IoT, and connectivity for enhanced motor monitoring and control.

- Development of advanced materials (e.g., rare-earth magnets, carbon fiber) for improved performance.

- Focus on sustainable manufacturing practices and recycling of motor components.

AI Impact Analysis on Electric Motor

Artificial Intelligence (AI) is poised to significantly revolutionize the electric motor industry, influencing everything from design and manufacturing to operational maintenance and predictive analytics. Common user questions revolve around how AI can optimize motor performance, enhance diagnostic capabilities, and streamline production processes. AI algorithms are being applied to simulate complex motor behaviors, allowing engineers to refine designs for higher efficiency and reduced material usage before physical prototyping. This reduces development cycles and costs while improving product quality.

Beyond design, AI's impact extends to the operational lifecycle of electric motors. Users frequently inquire about AI-driven predictive maintenance, which can analyze real-time sensor data from motors to anticipate failures, optimize service schedules, and prevent costly downtime. This shift from reactive to proactive maintenance minimizes operational expenditure and extends motor lifespan. Furthermore, AI is crucial in quality control during manufacturing, identifying defects with greater precision and speed than traditional methods, thereby ensuring the reliability and consistency of manufactured motors.

- AI-driven optimization of motor design parameters for enhanced efficiency and power density.

- Predictive maintenance analytics leveraging AI to forecast motor failures and reduce downtime.

- Intelligent control systems for dynamic motor operation, adapting to varying load conditions.

- Automation of manufacturing processes and quality inspection using AI-powered robotics and vision systems.

- Enhanced energy management and load balancing in industrial applications through AI algorithms.

- Development of self-learning motors that adapt and improve performance over time.

Key Takeaways Electric Motor Market Size & Forecast

The Electric Motor Market is poised for substantial and sustained growth throughout the forecast period, reflecting global imperatives for energy efficiency, decarbonization, and industrial advancement. User inquiries consistently underscore a keen interest in the fundamental drivers of this expansion, particularly the accelerating adoption of electric vehicles and the widespread integration of automation in manufacturing processes. The robust CAGR projected signifies a healthy market environment, attracting continued investment in research and development, leading to more sophisticated and efficient motor technologies.

A significant takeaway is the increasing emphasis on advanced motor types, such as BLDC and synchronous reluctance motors, which are gaining traction due to their superior performance characteristics and compliance with evolving energy efficiency standards. Furthermore, the market's trajectory is strongly influenced by policy support and governmental initiatives promoting energy-efficient appliances and industrial equipment. This regulatory push, combined with technological innovation, positions the electric motor sector as a critical enabler of sustainable development and industrial productivity worldwide.

- Robust market growth driven primarily by the global shift towards electrification and industrial automation.

- Significant expansion in the automotive sector, propelled by electric vehicle production.

- Emphasis on energy-efficient motor solutions due to increasing environmental regulations and operational cost reduction.

- Technological advancements, including compact designs and smart features, are key to market evolution.

- Asia Pacific is expected to remain a dominant region, fueled by manufacturing output and EV adoption.

- Long-term market stability underpinned by diverse applications across industrial, commercial, and residential sectors.

Electric Motor Market Drivers Analysis

The electric motor market's expansion is fundamentally propelled by a confluence of macroeconomic trends and technological advancements. A primary driver is the escalating global focus on energy efficiency, mandated by increasingly stringent environmental regulations and the desire to reduce operational costs across industries. This has spurred demand for high-efficiency motors that consume less power and contribute to lower carbon emissions. Simultaneously, the rapid electrification of the transportation sector, particularly the surge in electric vehicle (EV) production and adoption, represents a monumental demand catalyst, requiring specialized, high-performance motors.

Beyond transportation, the pervasive trend of industrial automation and the continued growth of manufacturing sectors worldwide are significant contributors. Modern factories rely heavily on precise and reliable electric motors for robotics, conveyor systems, and various machinery, driving the demand for advanced motor solutions. Furthermore, the integration of renewable energy sources into power grids necessitates efficient motors for applications such as wind turbines and solar tracking systems. These multifaceted drivers create a robust and expanding demand landscape for electric motors across diverse applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Adoption of Electric Vehicles (EVs) | +2.5% | Global, particularly Asia Pacific (China, India), Europe, North America | Short-term to Long-term (2025-2033) |

| Increasing Focus on Energy Efficiency and Green Initiatives | +1.8% | Europe, North America, Japan, and emerging economies adopting green policies | Medium-term to Long-term (2025-2033) |

| Growth in Industrial Automation and Robotics | +1.5% | Asia Pacific (China, South Korea), Germany, USA | Medium-term (2025-2029) |

| Expansion of HVAC Systems and Household Appliances Market | +1.0% | Asia Pacific (India, Southeast Asia), Latin America, Middle East & Africa | Long-term (2027-2033) |

| Development of Smart Cities and Infrastructure | +0.8% | Globally, with strong emphasis in developed and rapidly urbanizing regions | Long-term (2028-2033) |

Electric Motor Market Restraints Analysis

Despite the optimistic growth projections, the electric motor market faces several notable restraints that could temper its expansion. One significant challenge is the volatility and increasing prices of raw materials, particularly rare-earth metals like neodymium and dysprosium, which are crucial components in high-efficiency permanent magnet motors. Supply chain disruptions and geopolitical factors influencing these materials can directly impact manufacturing costs and product availability, potentially leading to price increases for end-users and dampening demand.

Another impediment is the high initial investment cost associated with advanced electric motors, especially for specialized applications or when retrofitting existing infrastructure with more energy-efficient models. While the long-term operational savings often justify this cost, the upfront expenditure can be a barrier for smaller businesses or those with limited capital. Additionally, the complexity involved in integrating new motor technologies into existing systems, coupled with a potential shortage of skilled labor for installation and maintenance, poses practical challenges that could slow adoption rates in certain sectors or regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (e.g., Rare Earth Magnets, Copper) | -0.9% | Global, particularly impacting regions dependent on imports (Europe, North America) | Short-term to Medium-term (2025-2028) |

| High Initial Investment Cost for Advanced Motors | -0.7% | Emerging economies, Small and Medium Enterprises (SMEs) globally | Medium-term (2025-2029) |

| Supply Chain Disruptions and Geopolitical Instability | -0.6% | Global, affecting trade routes and manufacturing hubs (e.g., East Asia) | Short-term (2025-2026) |

| Technological Complexity and Integration Challenges | -0.5% | Sectors with legacy infrastructure (e.g., older industrial plants) | Long-term (2027-2033) |

| Shortage of Skilled Workforce for Installation and Maintenance | -0.4% | Developed countries (North America, Europe, Japan) | Long-term (2028-2033) |

Electric Motor Market Opportunities Analysis

The electric motor market is rich with opportunities, driven by ongoing technological innovation and expanding application landscapes. A significant avenue for growth lies in the burgeoning demand for electric motors in emerging economies, particularly in Asia Pacific and Latin America, where rapid industrialization, urbanization, and increasing consumer purchasing power are fueling demand across various sectors. These regions offer vast untapped potential for both industrial and consumer motor applications, including HVAC systems, household appliances, and new manufacturing facilities.

Furthermore, the development of advanced motor types, such as synchronous reluctance motors (SynRM) and switched reluctance motors (SRM), which offer high efficiency without relying on rare-earth magnets, presents a strategic opportunity to mitigate raw material price volatility and enhance sustainability. The growing emphasis on the Internet of Things (IoT) and Industry 4.0 also creates new opportunities for smart, connected motors that can provide real-time data for predictive maintenance and operational optimization. Lastly, the retrofitting of older industrial equipment with modern, energy-efficient electric motors offers a substantial market for companies focused on efficiency upgrades and sustainability initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Markets in Emerging Economies | +1.2% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Long-term (2027-2033) |

| Development of Rare-Earth Free and Sustainable Motors | +1.0% | Global, particularly Europe and North America driving sustainability | Medium-term to Long-term (2026-2033) |

| Integration with IoT, AI, and Smart Manufacturing (Industry 4.0) | +0.9% | Developed industrial nations (Germany, USA, Japan), China | Short-term to Medium-term (2025-2029) |

| Retrofitting and Upgrading Existing Industrial Infrastructure | +0.7% | Mature industrial regions (Europe, North America) | Medium-term (2025-2030) |

| Expansion into Specialized Applications (e.g., Medical, Aerospace) | +0.6% | Developed countries with high-tech industries | Long-term (2028-2033) |

Electric Motor Market Challenges Impact Analysis

The electric motor market, while promising, is not without its challenges that demand strategic navigation from industry participants. Intense competition from a fragmented landscape of established global players and nimble regional manufacturers creates pricing pressures and necessitates continuous innovation to maintain market share. This competitive environment can lead to thinner profit margins, particularly in commodity motor segments, and requires significant investment in R&D to differentiate products based on performance, efficiency, and features.

Further, adherence to diverse and evolving regulatory standards across different geographies poses a significant compliance challenge. Energy efficiency mandates, safety certifications, and environmental regulations vary by country and region, requiring manufacturers to design and produce motors that meet multiple, often conflicting, sets of requirements. This complexity adds to development costs and time-to-market. Additionally, the protection of intellectual property (IP) in a globally competitive and interconnected market remains a concern, particularly for companies investing heavily in cutting-edge motor technologies, as imitation and unauthorized production can undermine market advantage.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -0.8% | Global, prevalent in all market segments | Short-term to Long-term (2025-2033) |

| Stringent and Evolving Regulatory Compliance | -0.6% | Europe, North America, Japan, China | Medium-term (2025-2030) |

| Maintaining Innovation Pace with Rapid Technological Advancements | -0.5% | Global, particularly for established market leaders | Long-term (2027-2033) |

| Cybersecurity Risks for Connected Motors and Systems | -0.4% | Industries adopting Industry 4.0 (e.g., manufacturing, utilities) | Medium-term to Long-term (2026-2033) |

| Disposal and Recycling of End-of-Life Motors and Components | -0.3% | Developed economies with strict environmental regulations | Long-term (2028-2033) |

Electric Motor Market - Updated Report Scope

This report provides a comprehensive analysis of the global Electric Motor Market, offering in-depth insights into its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges across various segments and major geographical regions. It encompasses a detailed examination of market dynamics from historical data through to a forward-looking forecast, providing stakeholders with strategic intelligence to navigate the evolving industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 175.5 Billion |

| Market Forecast in 2033 | USD 305.8 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, General Electric Company, Regal Rexnord Corporation, Nidec Corporation, Robert Bosch GmbH, Denso Corporation, WEG S.A., Toshiba Corporation, Johnson Electric Holdings Ltd., Mitsubishi Electric Corporation, TECO Electric & Machinery Co., Ltd., Allied Motion Technologies Inc., Danaher Corporation, Rockwell Automation, Inc., Parker-Hannifin Corporation, Hitachi, Ltd., Brook Crompton UK Ltd., Baldor Electric Company, Ametek Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Electric Motor Market is comprehensively segmented by various parameters, providing a granular view of its diverse applications and technological advancements. This segmentation allows for a detailed understanding of market dynamics within specific product categories, power ranges, and end-user industries. The segmentation by type differentiates between AC, DC, and specialized motors, each serving distinct operational requirements and application environments. AC motors, further broken down into synchronous and asynchronous types, are widely used in industrial applications due to their robustness and efficiency, while DC motors, especially BLDC, are gaining prominence in automotive and consumer electronics due to their compact size and precise control capabilities.

Furthermore, the market is segmented by output power, distinguishing between Fractional Horsepower (FHP) motors used in smaller appliances and Integral Horsepower (IHP) motors typically found in heavy industrial machinery. The application-based segmentation provides insights into the primary industries driving demand, ranging from industrial machinery and automotive to HVAC systems and household appliances. Finally, end-user industry segmentation offers a vertical-specific analysis, identifying key sectors such as manufacturing, commercial & residential, and transportation as major contributors to market growth and technological adoption. This multi-faceted segmentation highlights the broad utility and critical role of electric motors across the global economy.

- By Type:

- AC Motor: Significant in industrial and commercial applications; asynchronous motors dominate due to simplicity and cost-effectiveness.

- Synchronous Motor: Utilized in precision applications and power factor correction.

- Asynchronous Motor: Widely used in general industrial machinery and pumping.

- DC Motor: Valued for speed control and compact size, crucial in automotive and portable devices.

- Brushed DC Motor: Cost-effective for basic applications.

- Brushless DC (BLDC) Motor: Superior efficiency, longer lifespan, and lower maintenance, preferred in EVs and high-end appliances.

- Hermetic Motor: Specifically designed for use in hermetically sealed compressors for refrigeration and air conditioning.

- Others: Includes specialized motors like Stepper Motors (for precise positioning in robotics and printers) and Servo Motors (for high-performance control in industrial automation).

- By Output Power:

- Fractional Horsepower (FHP): Motors with output less than 1 HP, common in home appliances, office equipment, and small tools.

- Integral Horsepower (IHP): Motors with output 1 HP or more, extensively used in heavy industrial machinery, pumps, fans, and compressors.

- By Application:

- Industrial Machinery: Drives pumps, compressors, fans, conveyors, and machine tools, backbone of manufacturing.

- Automotive: Crucial for Electric Vehicles (EVs), Hybrid Electric Vehicles (HEVs), and various vehicle auxiliary systems (power windows, seats, wipers).

- HVAC Systems: Integral to air conditioners, furnaces, and ventilation systems in commercial and residential buildings.

- Household Appliances: Found in washing machines, refrigerators, blenders, vacuum cleaners, and other consumer durables.

- Aerospace & Defense: Used in control surface actuation, landing gear, and auxiliary power units of aircraft and defense systems.

- Medical Devices: Powers surgical tools, diagnostic equipment, and patient care devices requiring precision and reliability.

- Agriculture: Used in irrigation systems, farm machinery, and processing equipment.

- Water & Wastewater Management: Essential for pumps in municipal water supply and treatment plants.

- Oil & Gas: Employed in drilling equipment, pumps, and compressors for extraction and processing.

- Power Generation: Used in auxiliary systems, cooling towers, and control mechanisms within power plants.

- By End-User Industry:

- Manufacturing: Automotive, electronics, textiles, food & beverage, and other industrial production sectors.

- Commercial & Residential: HVAC, elevators, escalators, and various consumer durables in buildings.

- Infrastructure & Construction: Pumps for water supply, ventilation systems in tunnels, and construction machinery.

- Transportation: Primarily automotive (EVs, trains, buses) and marine applications.

- Energy & Utilities: Power generation plants, smart grids, and renewable energy installations.

- Healthcare: Hospitals, clinics, and laboratories utilizing medical devices.

Regional Highlights

- North America: This region is a mature market, characterized by significant adoption of industrial automation and a rapidly expanding electric vehicle sector, particularly in the United States and Canada. Stringent energy efficiency regulations and increasing investments in smart infrastructure drive demand for high-efficiency motors. The automotive industry's shift towards electrification is a primary growth engine, alongside robust demand from the manufacturing and HVAC sectors. Technological innovation and substantial R&D investments by key players further solidify the region's market position.

- Europe: Europe is a leader in adopting energy-efficient and sustainable motor technologies, propelled by ambitious climate targets and comprehensive environmental regulations. Countries like Germany, France, and the UK demonstrate strong demand from their advanced manufacturing sectors, including automotive and robotics. The region's focus on Industry 4.0 initiatives and smart factories fuels the adoption of high-precision and IoT-enabled motors. The well-established automotive industry's transition to EVs and continued investment in renewable energy projects also contribute significantly to market expansion.

- Asia Pacific (APAC): APAC stands as the largest and fastest-growing market for electric motors, driven by rapid industrialization, burgeoning manufacturing capabilities, and massive population growth. China and India are at the forefront, with extensive manufacturing bases for electronics, automotive components, and consumer goods. The region's unparalleled growth in electric vehicle production and adoption, coupled with substantial investments in infrastructure development and urbanization, creates immense demand. Lower manufacturing costs and increasing disposable incomes further stimulate market expansion across diverse applications.

- Latin America: This region presents significant growth opportunities, particularly in industrial sectors such as mining, agriculture, and oil & gas, which are undergoing modernization and seeking efficiency improvements. Countries like Brazil and Mexico are experiencing industrial expansion and increasing demand for electric motors in HVAC systems and household appliances due to urbanization and rising consumer spending. Investments in renewable energy and infrastructure projects are also contributing to market development.

- Middle East and Africa (MEA): The MEA region is witnessing steady growth, primarily driven by investments in infrastructure, industrialization, and diversification efforts away from oil-dependent economies. Countries in the Gulf Cooperation Council (GCC) are investing heavily in smart city projects and manufacturing capabilities, increasing demand for electric motors in construction, utilities, and various industrial applications. Growing awareness regarding energy efficiency and the rising adoption of HVAC systems in hot climates further support market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electric Motor Market.- ABB Ltd.

- Siemens AG

- General Electric Company

- Regal Rexnord Corporation

- Nidec Corporation

- Robert Bosch GmbH

- Denso Corporation

- WEG S.A.

- Toshiba Corporation

- Johnson Electric Holdings Ltd.

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Allied Motion Technologies Inc.

- Danaher Corporation

- Rockwell Automation, Inc.

- Parker-Hannifin Corporation

- Hitachi, Ltd.

- Brook Crompton UK Ltd.

- Baldor Electric Company

- Ametek Inc.

Frequently Asked Questions

What is an electric motor and how does it work?

An electric motor is an electromechanical device that converts electrical energy into mechanical energy. It operates on the principle of electromagnetism, where the interaction between a magnetic field and an electric current in a wire coil produces a force that generates rotational motion. This mechanical output can then be used to power a wide array of machines and systems, from small household appliances to large industrial machinery and vehicles.

What are the primary types of electric motors in the market?

The primary types of electric motors are AC (Alternating Current) motors and DC (Direct Current) motors. AC motors include synchronous and asynchronous (induction) motors, commonly used in industrial and large-scale applications. DC motors comprise brushed and brushless (BLDC) motors, with BLDC motors gaining popularity for their efficiency and compact design in applications like electric vehicles and consumer electronics. Hermetic motors and specialized motors like stepper and servo motors also form significant categories.

Which industries are the major end-users of electric motors?

Electric motors are foundational components across numerous industries. Key end-user sectors include automotive, particularly with the rise of Electric Vehicles (EVs); industrial machinery for manufacturing and automation; HVAC systems in commercial and residential buildings; household appliances; and specialized applications in aerospace and defense, medical devices, and the oil & gas sector. Their versatility ensures widespread adoption in almost every aspect of modern industry and daily life.

How are energy efficiency regulations impacting the electric motor market?

Energy efficiency regulations are profoundly impacting the electric motor market by driving demand for higher-efficiency motors. Governments globally are implementing stricter minimum efficiency performance standards (MEPS) to reduce energy consumption and carbon emissions. This regulatory push incentivizes manufacturers to innovate and produce more efficient motor designs, such as IE3 and IE4 class motors, while also encouraging end-users to upgrade to more energy-efficient models to comply with standards and reduce operational costs.

What is the role of smart technology and IoT in the electric motor market's future?

Smart technology and the Internet of Things (IoT) are crucial for the future of the electric motor market, enabling advanced functionalities. Integrating sensors and connectivity allows for real-time monitoring of motor performance, facilitating predictive maintenance, energy optimization, and remote control. This capability enhances operational efficiency, reduces downtime, and extends the lifespan of motors, aligning with Industry 4.0 initiatives and creating opportunities for new data-driven services and more intelligent industrial ecosystems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted