Education Software Market

Education Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710228 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

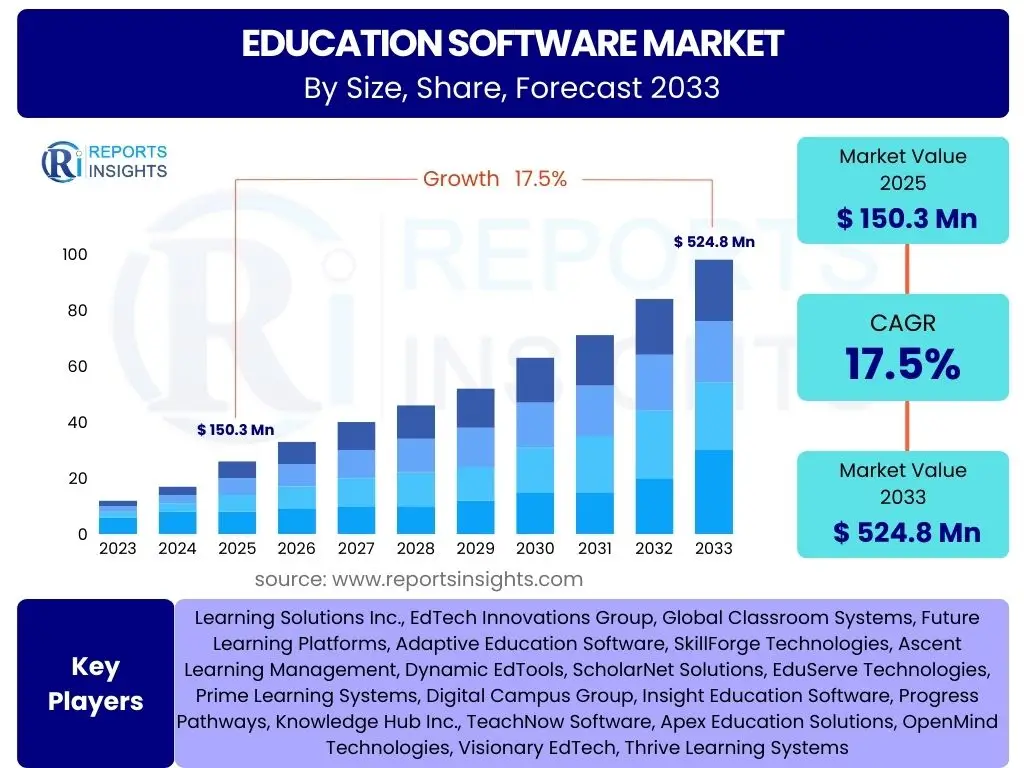

Education Software Market Size

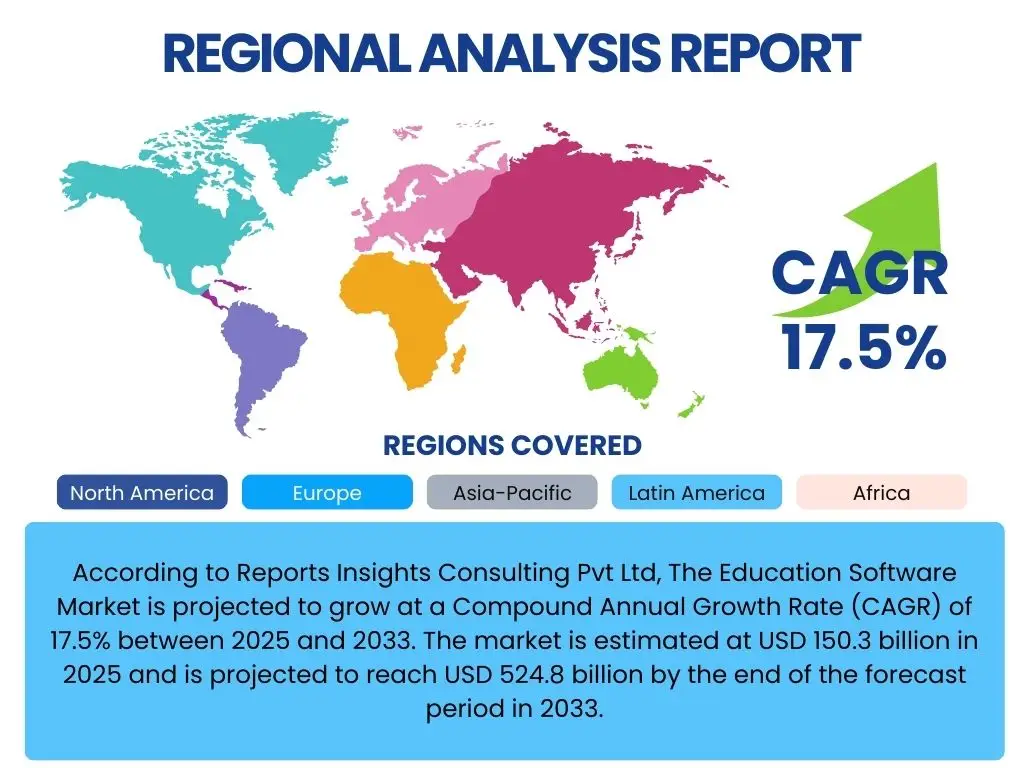

According to Reports Insights Consulting Pvt Ltd, The Education Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 17.5% between 2025 and 2033. The market is estimated at USD 150.3 billion in 2025 and is projected to reach USD 524.8 billion by the end of the forecast period in 2033.

Key Education Software Market Trends & Insights

Users frequently inquire about the transformative shifts and emerging patterns shaping the education software landscape. Analysis reveals a strong emphasis on personalized learning experiences, the integration of advanced analytics, and the increasing ubiquity of cloud-based solutions. Stakeholders are keen to understand how these trends are redefining traditional pedagogy, improving learner outcomes, and driving innovation within educational technology, particularly regarding accessibility and engagement across diverse learning environments. The focus is on scalable, adaptable, and user-centric platforms that cater to evolving educational needs from K-12 to corporate training.

- Personalized Learning Pathways: Software adapting content and pace to individual student needs and learning styles.

- Gamification and Experiential Learning: Incorporation of game-design elements and immersive simulations to enhance engagement and retention.

- Data Analytics and Learning Management Systems (LMS) Integration: Leveraging data to track student progress, identify learning gaps, and inform instructional strategies.

- Cloud-Based Solutions and SaaS Models: Growing preference for accessible, scalable, and cost-effective cloud-hosted education platforms.

- Microlearning and Skill-Based Credentials: Focus on bite-sized content delivery and verifiable skills for lifelong learning and professional development.

- Hybrid Learning Models: Development of software supporting seamless transitions between in-person and remote learning environments.

- Enhanced Cybersecurity and Data Privacy: Increasing demand for robust security features to protect sensitive student and institutional data.

AI Impact Analysis on Education Software

Common user questions regarding AI's impact on education software revolve around its potential to revolutionize learning, automate administrative tasks, and personalize educational content. Users seek clarity on how AI can enhance student engagement, provide intelligent tutoring, and adapt curricula dynamically. Concerns often include ethical implications, data bias, the need for human-AI collaboration, and ensuring equitable access to advanced AI-powered tools. The overarching expectation is that AI will make education more efficient, effective, and tailored, while also presenting new challenges in implementation and oversight. Furthermore, the generative capabilities of AI are particularly scrutinized for their potential in content creation and assessment, prompting questions about authenticity and originality.

- Personalized Adaptive Learning: AI algorithms analyze student performance to offer customized learning paths and resources.

- Intelligent Tutoring Systems (ITS): AI-powered virtual tutors provide real-time feedback, answer questions, and guide students through complex topics.

- Automated Assessment and Grading: AI assists in grading assignments, quizzes, and essays, providing faster feedback and reducing educator workload.

- Content Generation and Curation: AI tools help create educational materials, summarize texts, and recommend relevant learning resources.

- Administrative Efficiency: AI automates routine tasks like scheduling, student support, and data management for educational institutions.

- Predictive Analytics for Student Success: AI identifies at-risk students and predicts academic performance, enabling early intervention.

- Enhanced Accessibility: AI-driven features like speech-to-text, translation, and alt-text generation improve access for diverse learners.

- Adaptive Content Creation: Generative AI assists educators in developing dynamic and engaging lesson plans, quizzes, and interactive exercises tailored to specific learning objectives and student demographics.

- Personalized Feedback Loops: AI provides nuanced, individualized feedback on student assignments, going beyond simple right/wrong answers to suggest improvements and highlight areas for growth.

Key Takeaways Education Software Market Size & Forecast

Stakeholders frequently ask for concise summaries of the market's trajectory and the most critical factors influencing its growth. The primary takeaway is the robust and sustained expansion of the education software market, driven by a confluence of technological advancements, evolving pedagogical approaches, and increasing digital literacy. The significant projected CAGR underscores a long-term shift towards digital-first learning ecosystems, necessitating continuous investment in innovative software solutions. Understanding the specific drivers, such as remote learning permanence and AI integration, alongside potential restraints like budget limitations, is crucial for strategic planning within this dynamic sector.

- Substantial Market Growth: The education software market is poised for significant expansion, exceeding 17% CAGR over the forecast period.

- Digital Transformation Imperative: Educational institutions globally are increasingly adopting digital tools to enhance learning and administrative efficiency.

- AI as a Core Enabler: Artificial intelligence is a critical factor driving personalization, automation, and intelligent learning experiences within software.

- Diverse Application Across Segments: Growth is widespread, affecting K-12, higher education, and corporate/vocational training sectors.

- Shift to Cloud and Subscription Models: Cloud-based SaaS solutions are becoming the standard, offering scalability and accessibility.

- Focus on Learner-Centric Solutions: Software development prioritizes engaging, interactive, and adaptive learning experiences.

- Investment in Cybersecurity is Paramount: Protecting sensitive data within education software is a growing concern and area of investment.

Education Software Market Drivers Analysis

The education software market is primarily propelled by the ongoing global digital transformation within the education sector. This shift, significantly accelerated by recent global events, has necessitated the widespread adoption of digital learning platforms, tools, and content to ensure continuity and enhance pedagogical effectiveness. Institutions across all levels, from K-12 to higher education and corporate training, are investing heavily in robust software solutions for content delivery, student management, assessment, and collaborative learning.

Furthermore, the increasing demand for personalized and adaptive learning experiences is a key driver. Modern education software leverages advanced analytics and artificial intelligence to tailor content, pace, and feedback to individual student needs, leading to improved engagement and learning outcomes. This trend is complemented by the growing emphasis on lifelong learning and skill development, expanding the market beyond traditional academic settings into professional development and vocational training, where specialized software facilitates continuous upskilling and reskilling.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Adoption of Online Learning Platforms | +4.2% | Global, particularly North America, Europe, APAC | Short-term to Long-term |

| Growing Demand for Personalized Learning | +3.8% | Global, especially developed economies | Medium-term to Long-term |

| Integration of Artificial Intelligence (AI) and Machine Learning (ML) | +3.5% | Global, all regions | Medium-term to Long-term |

| Rise of Corporate E-learning and Upskilling Programs | +2.9% | North America, Europe, Asia Pacific | Short-term to Medium-term |

| Government Initiatives and Funding for Digital Education | +2.5% | Emerging economies, Europe, parts of APAC | Medium-term |

| Technological Advancements in Mobile Learning and Cloud Computing | +2.1% | Global | Short-term to Long-term |

Education Software Market Restraints Analysis

Despite robust growth, the education software market faces several significant restraints that could impede its full potential. A primary challenge is the substantial initial investment required for institutions to procure and implement sophisticated education software solutions. This financial barrier can be particularly daunting for smaller institutions or those in developing regions with limited budgetary allocations for technology upgrades, impacting the rate of adoption and market penetration.

Another critical restraint involves the persistent issues surrounding data privacy and security. Education software often handles sensitive personal and academic data of students, making it a prime target for cyber threats. Concerns about data breaches, unauthorized access, and compliance with stringent regulations like GDPR or FERPA can deter institutions and parents from fully embracing digital solutions, leading to cautious adoption and slowed growth in certain segments. Additionally, the lack of adequate digital infrastructure, particularly reliable internet access and sufficient hardware, in many rural or underserved areas continues to limit the reach and effectiveness of online education software.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Budget Constraints for Institutions | -3.0% | Global, particularly developing regions | Short-term to Medium-term |

| Data Privacy and Security Concerns | -2.8% | Global, highly regulated markets (EU, North America) | Short-term to Long-term |

| Lack of Adequate Digital Infrastructure in Emerging Markets | -2.5% | Africa, parts of Asia Pacific, Latin America | Medium-term |

| Resistance to Change and Traditional Pedagogical Approaches | -2.0% | Global, particularly older educators | Short-term |

| Interoperability Issues Between Different Software Systems | -1.8% | Global, institutions with legacy systems | Medium-term |

| Digital Divide and Accessibility Gaps | -1.5% | Global, socioeconomic disparities | Short-term to Long-term |

Education Software Market Opportunities Analysis

The education software market presents numerous opportunities driven by evolving educational paradigms and technological advancements. One significant opportunity lies in the expansion of lifelong learning and reskilling initiatives. As industries undergo rapid transformation, there is an increasing demand for continuous education and professional development. Education software providers can capitalize on this by offering specialized platforms and content for vocational training, corporate upskilling, and credentialing, catering to a vast adult learner demographic beyond traditional academic students.

Moreover, the advent of advanced technologies such as virtual reality (VR), augmented reality (AR), and the metaverse creates new avenues for immersive and interactive learning experiences. These technologies can transform abstract concepts into tangible, experiential lessons, particularly in fields like medicine, engineering, and vocational training. Software developers who can effectively integrate these immersive elements into their platforms stand to gain a competitive edge. The growing focus on inclusive education also presents an opportunity for developing software solutions that cater to diverse learning needs, including those with disabilities, by incorporating accessibility features and adaptive technologies.

The burgeoning edtech market in emerging economies, particularly in Asia Pacific and Latin America, represents another substantial opportunity. Governments and private institutions in these regions are increasingly investing in digital education infrastructure and solutions to bridge educational gaps and improve access to quality learning. Providers offering scalable, affordable, and culturally relevant software can tap into these rapidly expanding markets, fostering long-term growth and impact.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Lifelong Learning and Professional Development | +3.5% | Global, particularly developed economies | Medium-term to Long-term |

| Integration of AR/VR and Immersive Learning Technologies | +3.2% | Global, early adopters in tech-forward regions | Medium-term to Long-term |

| Growth in Emerging Economies and Underserved Markets | +2.9% | Asia Pacific, Latin America, Middle East & Africa | Short-term to Long-term |

| Development of Niche Software for Specialized Skills and Trades | +2.7% | Global, industry-specific markets | Medium-term |

| Increased Demand for Data-Driven Instructional Design | +2.4% | Global, particularly higher education and corporate training | Short-term to Medium-term |

| Partnerships with Educational Institutions and Content Providers | +2.0% | Global | Short-term to Long-term |

Education Software Market Challenges Impact Analysis

The education software market, while expanding rapidly, contends with several notable challenges that require strategic navigation. One primary challenge is the high degree of fragmentation within the market, where numerous providers offer specialized solutions that may not seamlessly integrate with existing institutional infrastructure. This lack of interoperability can lead to complexities in data management, increased administrative burden, and a fragmented user experience, making it difficult for institutions to adopt comprehensive, unified digital ecosystems.

Another significant hurdle is the rapid pace of technological obsolescence. The education software sector is characterized by continuous innovation, with new tools and platforms emerging frequently. This constant evolution requires providers to invest heavily in research and development to remain competitive, while institutions face the challenge of keeping their systems updated and ensuring educators and students are trained on the latest functionalities. The cost associated with frequent upgrades and continuous professional development for educators can be a substantial barrier, particularly for budget-constrained schools.

Furthermore, ensuring equitable access and effective utilization of education software across diverse socioeconomic backgrounds remains a critical challenge. The "digital divide," characterized by disparities in internet access, device ownership, and digital literacy, can exacerbate existing educational inequalities. Software providers must develop solutions that are accessible, affordable, and adaptable to low-bandwidth environments, while institutions need to implement robust support systems to empower all learners to benefit from digital tools, moving beyond mere provision to genuine engagement and efficacy.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Market Fragmentation and Lack of Interoperability | -2.8% | Global | Medium-term |

| Rapid Technological Obsolescence and Need for Continuous Updates | -2.6% | Global | Short-term to Long-term |

| Ensuring Digital Equity and Accessibility Across Diverse Populations | -2.3% | Global, especially emerging markets and disadvantaged areas | Long-term |

| Teacher Training and Professional Development for New Technologies | -2.0% | Global | Short-term to Medium-term |

| Balancing Innovation with Cost-Effectiveness for Institutions | -1.7% | Global | Medium-term |

| Maintaining Student Engagement in Digital Learning Environments | -1.5% | Global | Short-term to Medium-term |

Education Software Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the education software market, covering its current size, historical performance, and future growth projections from 2025 to 2033. It examines key market trends, drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. The scope includes a detailed segmentation analysis by component, deployment, application, and end-user, alongside a thorough regional and competitive landscape assessment to deliver a holistic understanding of the market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 150.3 Billion |

| Market Forecast in 2033 | USD 524.8 Billion |

| Growth Rate | 17.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Learning Solutions Inc., EdTech Innovations Group, Global Classroom Systems, Future Learning Platforms, Adaptive Education Software, SkillForge Technologies, Ascent Learning Management, Dynamic EdTools, ScholarNet Solutions, EduServe Technologies, Prime Learning Systems, Digital Campus Group, Insight Education Software, Progress Pathways, Knowledge Hub Inc., TeachNow Software, Apex Education Solutions, OpenMind Technologies, Visionary EdTech, Thrive Learning Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The education software market is segmented to provide a granular understanding of its diverse components and applications, reflecting the varied needs of learners and institutions. These segments highlight key areas of development and adoption, enabling a targeted analysis of market dynamics. By breaking down the market based on component, deployment, application, and end-user, stakeholders can identify specific growth drivers and investment opportunities within each niche.

The "By Component" segment differentiates between standalone software offerings and the crucial services that support their implementation and maintenance, recognizing that comprehensive solutions often require both. The "By Deployment" segment distinguishes between cloud-based and on-premise solutions, illustrating the industry's shift towards more flexible and accessible cloud infrastructures. This distinction is critical for understanding scalability, cost structures, and security considerations influencing market preferences.

Furthermore, the "By Application" segment delineates the myriad uses of education software, from core learning management to specialized tools for content creation, assessment, and language acquisition, demonstrating the breadth of functionality available. Finally, the "By End-User" segment categorizes the primary beneficiaries of these technologies, ranging from K-12 students to corporate professionals, underscoring the universal applicability and growing demand for digital learning solutions across all educational stages and professional development pathways.

- By Component:

- Software (On-premise, Cloud-based)

- Services (Consulting, Implementation, Support & Maintenance)

- By Deployment:

- Cloud

- On-Premise

- By Application:

- Learning Management Systems (LMS)

- Content Management Systems (CMS)

- Student Information Systems (SIS)

- Authoring Tools

- Assessment & Analytics

- Language Learning

- Coding & Programming

- Virtual Classrooms

- Others (e.g., library management, timetabling)

- By End-User:

- K-12

- Higher Education

- Corporate & Vocational Training

- Individual Learners

Regional Highlights

North America maintains a dominant position in the education software market, characterized by early adoption of advanced technologies, substantial investment in R&D, and a robust ecosystem of technology providers and educational institutions. The region benefits from high internet penetration, a strong emphasis on personalized learning, and significant corporate training expenditures. Government initiatives promoting STEM education and digital literacy further bolster market growth, particularly in the United States and Canada, where competitive pressures drive continuous innovation in learning solutions.

Europe demonstrates significant growth, driven by digitalization initiatives, supportive regulatory frameworks, and increasing investments in educational technology across the European Union. Countries like the UK, Germany, and France are leading in the adoption of cloud-based solutions and AI-powered learning platforms. The region's focus on lifelong learning and vocational training, coupled with a push for standardized digital education tools, contributes substantially to market expansion. However, language diversity and varying educational systems can present unique challenges and opportunities for localized software solutions.

The Asia Pacific (APAC) region is projected to experience the fastest growth, fueled by its massive student population, rising disposable incomes, and increasing government spending on education infrastructure and digital transformation. Countries such as China, India, Japan, and South Korea are at the forefront of this expansion, with a strong demand for online learning platforms, language learning software, and skill-based training. The proliferation of affordable smartphones and internet access in emerging economies within APAC is democratizing access to education software, creating a vast untapped market.

Latin America is an emerging market for education software, characterized by increasing internet penetration, government initiatives to integrate technology into public education, and a growing middle class. Brazil and Mexico are key markets, witnessing rising adoption of blended learning models and digital content. Challenges such as economic disparities and infrastructure limitations are being addressed through public-private partnerships, fostering a gradual but steady market expansion. The demand for accessible and affordable solutions is particularly strong here.

The Middle East and Africa (MEA) region presents significant growth potential, driven by ambitious government visions focused on economic diversification, human capital development, and digital transformation, particularly in the GCC countries. Investments in smart schools and higher education modernization projects are propelling the adoption of advanced education software. While challenges like varying internet infrastructure and digital literacy exist, the concerted efforts to digitalize education systems across key nations like UAE, Saudi Arabia, and South Africa are opening new avenues for education software providers.

- North America: Leading market share due to technological advancements, high investment in EdTech, and strong demand for personalized learning. Emphasis on corporate training and higher education.

- Europe: Significant growth driven by digital education initiatives, government funding, and focus on skill development. Adoption of cloud and AI solutions is high.

- Asia Pacific (APAC): Fastest-growing market due to large student population, increasing internet penetration, and government support for digital learning. Emerging economies are key growth drivers.

- Latin America: Growing adoption of online learning, propelled by increasing smartphone penetration and government investments in digital education infrastructure. Demand for accessible solutions.

- Middle East & Africa (MEA): Emerging market with strong government focus on digital transformation in education and vocational training, particularly in the GCC countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Education Software Market.- Learning Solutions Inc.

- EdTech Innovations Group

- Global Classroom Systems

- Future Learning Platforms

- Adaptive Education Software

- SkillForge Technologies

- Ascent Learning Management

- Dynamic EdTools

- ScholarNet Solutions

- EduServe Technologies

- Prime Learning Systems

- Digital Campus Group

- Insight Education Software

- Progress Pathways

- Knowledge Hub Inc.

- TeachNow Software

- Apex Education Solutions

- OpenMind Technologies

- Visionary EdTech

- Thrive Learning Systems

Frequently Asked Questions

Analyze common user questions about the Education Software market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Education Software market?

The Education Software market is projected to grow at a Compound Annual Growth Rate (CAGR) of 17.5% between 2025 and 2033, indicating robust expansion driven by digital transformation in education.

How is AI impacting education software?

AI is significantly impacting education software by enabling personalized adaptive learning, powering intelligent tutoring systems, automating assessment, assisting in content generation, and enhancing administrative efficiency for institutions.

What are the primary drivers of the Education Software market?

Key drivers include the increased adoption of online learning platforms, growing demand for personalized learning experiences, integration of AI/ML, rise of corporate e-learning, and supportive government initiatives for digital education.

Which regions are leading in education software adoption?

North America currently holds the largest market share due to high tech adoption, while the Asia Pacific (APAC) region is projected to experience the fastest growth due to its large student population and increasing digital investments.

What are the main challenges facing the education software market?

Major challenges include high initial investment costs for institutions, data privacy and security concerns, lack of digital infrastructure in certain regions, market fragmentation, and the need for continuous teacher training to adopt new technologies effectively.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted