Edge Card Optical Connector Market

Edge Card Optical Connector Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708651 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Edge Card Optical Connector Market Size

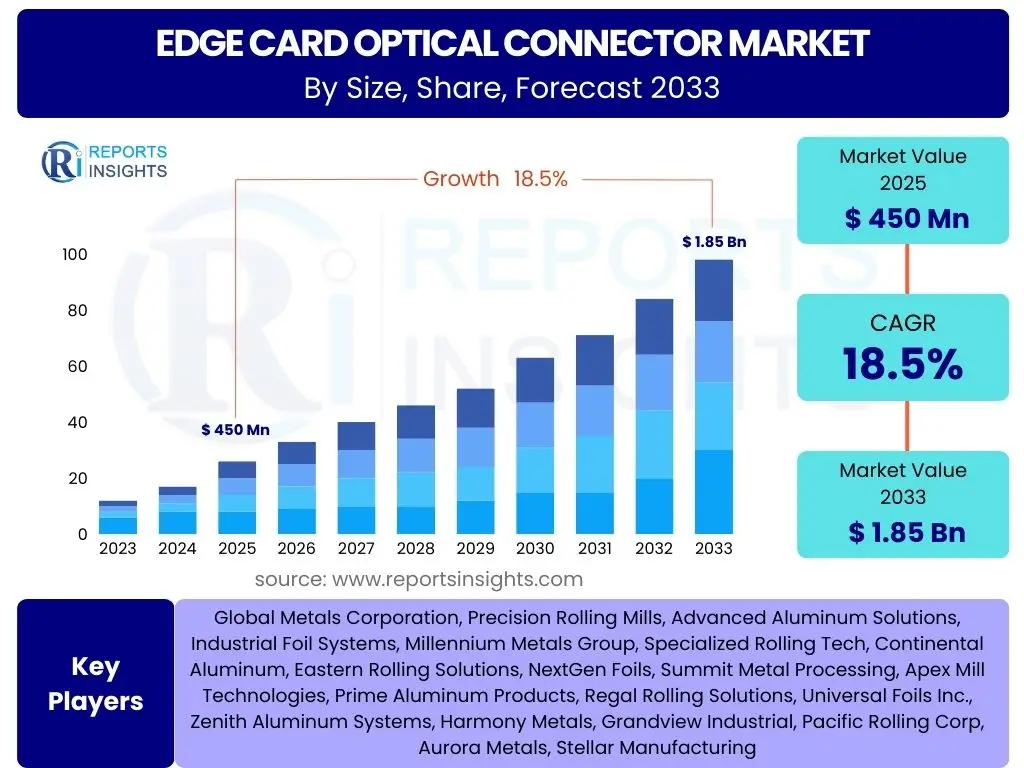

According to Reports Insights Consulting Pvt Ltd, The Edge Card Optical Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 1.85 Billion by the end of the forecast period in 2033. This robust growth is primarily driven by the escalating demand for high-speed, high-density, and low-latency data transmission across various industries, particularly within data centers, telecommunications, and high-performance computing.

The increasing proliferation of cloud computing, artificial intelligence, and machine learning applications necessitates vast improvements in network infrastructure, making edge card optical connectors a critical component. These connectors offer superior bandwidth capabilities and reduced electromagnetic interference compared to traditional electrical connectors, addressing the bottlenecks in data processing and transfer. Furthermore, the miniaturization trend in electronic devices and the need for more efficient power consumption further bolster the adoption of optical interconnect solutions, positioning the market for sustained expansion over the forecast period.

Key Edge Card Optical Connector Market Trends & Insights

Users frequently inquire about the evolving landscape of optical interconnect technology and how it shapes the market for edge card optical connectors. A dominant trend is the relentless pursuit of higher data rates, driven by the exponential growth in data traffic. This translates into a strong demand for connectors capable of supporting 400G, 800G, and even 1.6T Ethernet standards, pushing innovation in connector design, fiber count, and signal integrity. Another critical insight is the increasing integration of optical components directly onto printed circuit boards (PCBs), moving towards board-level optical interconnects to overcome the limitations of traditional electrical traces.

Furthermore, the market is witnessing a significant shift towards greater energy efficiency and thermal management solutions. As data centers become denser and consume more power, the ability of optical connectors to reduce power dissipation and facilitate efficient cooling becomes a key differentiator. There is also a growing emphasis on modularity and hot-swappability, allowing for easier maintenance, upgrades, and increased system flexibility. The integration of silicon photonics technology with edge card connectors is emerging as a transformative trend, promising even higher levels of integration, smaller form factors, and lower costs in the long term, fundamentally reshaping the design and application of these critical components in next-generation network architectures.

- Shift towards 400G, 800G, and 1.6T data rates for next-generation networks.

- Increased demand for miniaturized and high-density connector designs.

- Growing adoption of hybrid optical-electrical connectors for enhanced performance.

- Focus on improved energy efficiency and thermal management in data centers.

- Emergence of silicon photonics integration for board-level optical interconnects.

- Development of modular and hot-swappable optical connector solutions.

AI Impact Analysis on Edge Card Optical Connector

Common user questions regarding AI's impact on edge card optical connectors revolve around how artificial intelligence and machine learning drive the need for faster, denser, and more reliable optical interconnects in data centers and high-performance computing. AI workloads, characterized by massive parallel processing and constant data transfer between GPUs, CPUs, and memory, demand unprecedented bandwidth and ultra-low latency. Traditional electrical interconnects struggle to meet these requirements efficiently over distances, making optical solutions, particularly edge card optical connectors, indispensable for building scalable and high-performing AI infrastructures. The rapid expansion of AI model training and inference capabilities directly fuels the market for advanced optical connectors capable of handling this immense data flow.

The architectural evolution of AI supercomputers and specialized AI accelerators, such as those leveraging chiplets and high-bandwidth memory (HBM), often incorporates optical I/O directly at the board level. This trend pushes the boundaries for edge card optical connectors towards even greater integration, smaller footprints, and higher channel counts per connector. Furthermore, AI itself can play a role in optimizing the design and manufacturing of these connectors, using machine learning algorithms for fault detection, predictive maintenance, and quality control during production. The convergence of AI demand for high-speed data and the technological advancements in optical interconnects creates a symbiotic relationship, propelling significant innovation and market growth for edge card optical connectors as a foundational technology for the AI era.

- AI/ML drive demand for ultra-high-bandwidth and low-latency interconnects.

- Accelerated adoption in AI data centers and high-performance computing (HPC).

- Increased need for high-density optical I/O in AI hardware architectures.

- AI-driven workloads necessitate greater energy efficiency from optical links.

- Potential for AI to optimize design and manufacturing processes of connectors.

- Support for distributed AI computing requiring robust and scalable optical backbones.

Key Takeaways Edge Card Optical Connector Market Size & Forecast

Stakeholders frequently seek concise insights into the most critical aspects of the Edge Card Optical Connector market's future. A primary takeaway is the market's trajectory of significant growth, fueled by the insatiable demand for high-speed data transmission across a multitude of applications, including but not limited to, data centers, telecommunications, and enterprise networking. The forecasted double-digit CAGR underscores a robust and expanding industry, indicative of sustained investment and innovation. This growth is intrinsically linked to macro trends such as digital transformation, cloud adoption, and the proliferation of advanced technologies like AI and 5G, which inherently rely on efficient and high-capacity optical interconnects.

Another crucial insight is the evolving technological landscape, where miniaturization, higher integration, and improved energy efficiency are becoming paramount. The market is not just growing in volume but also in sophistication, with a strong emphasis on developing connectors that can support ever-increasing data rates (e.g., 800G and beyond) and seamless integration with silicon photonics platforms. For market participants, this signifies a need for continuous research and development, strategic partnerships, and a focus on cost-effective manufacturing to capitalize on emerging opportunities. Understanding the regional disparities in infrastructure development and technological adoption will also be key to navigating market entry and expansion strategies effectively.

- The market is poised for substantial growth, driven by increasing data traffic and digital transformation.

- Technological advancements in data rates (400G, 800G, 1.6T) are critical growth enablers.

- Data centers and telecom networks remain primary application areas, with growing influence from AI/HPC.

- Emphasis on miniaturization, higher density, and energy-efficient designs is paramount.

- Strategic investments in R&D and manufacturing are essential for competitive advantage.

- Regional disparities in infrastructure and technological maturity offer varied growth avenues.

Edge Card Optical Connector Market Drivers Analysis

The Edge Card Optical Connector market is primarily propelled by the exponential growth in global data traffic, an outcome of intensified cloud computing adoption, the pervasive internet of things (IoT), and the burgeoning rollout of 5G networks. These factors collectively demand network infrastructures capable of supporting higher bandwidth and lower latency, which traditional electrical interconnects are increasingly unable to provide efficiently. Optical connectors, with their inherent advantages in signal integrity and immunity to electromagnetic interference, become the preferred solution for the crucial backplane and board-to-board connections within servers, switches, and routers, thereby driving significant market expansion.

Furthermore, the rapid advancements in Artificial Intelligence (AI) and Machine Learning (ML) technologies are creating an unprecedented need for high-performance computing (HPC) environments. These environments require massive parallel processing capabilities and ultra-fast communication between processing units, memory, and storage. Edge card optical connectors facilitate these critical high-speed interconnects, enabling the efficient transfer of vast datasets necessary for AI model training and inference. The ongoing miniaturization of electronic devices and the continuous drive for higher port densities in network equipment also serve as strong market drivers, pushing manufacturers to innovate in compact and robust optical connector designs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Data Center Traffic | +5.5% | North America, Asia Pacific, Europe | 2025-2033 |

| Rapid AI/ML Adoption & HPC Expansion | +4.8% | North America, China, Europe | 2025-2033 |

| 5G Network Deployment & Edge Computing | +3.2% | Asia Pacific, North America, Europe | 2025-2030 |

| Miniaturization & Higher Port Density | +2.5% | Global | 2025-2033 |

| Growing Cloud Services Demand | +2.0% | Global | 2025-2033 |

Edge Card Optical Connector Market Restraints Analysis

Despite the robust growth potential, the Edge Card Optical Connector market faces several significant restraints that could temper its expansion. One primary challenge is the relatively high manufacturing cost associated with optical components and precision assembly processes compared to traditional electrical connectors. The intricate nature of aligning optical fibers, integrating delicate transceivers, and maintaining stringent performance standards contributes to elevated production expenses, which can be a barrier for widespread adoption, particularly in cost-sensitive applications or regions with limited budget allocations for infrastructure upgrades. This cost differential often prolongs the decision-making process for enterprises considering a transition to optical interconnects.

Another key restraint involves the complexity of design and integration for optical solutions. Implementing optical interconnects requires specialized expertise in optical engineering, thermal management, and power delivery, which may not be readily available to all system designers. The lack of universal standardization across all aspects of optical interconnects can also create interoperability issues and slow down adoption, as manufacturers and end-users may hesitate to invest in proprietary solutions. Furthermore, the inherent fragility of optical fibers and the need for meticulous handling during installation and maintenance can lead to higher operational costs and potential reliability concerns if not managed appropriately, posing an additional impediment to market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing & Integration Costs | -3.0% | Global, Emerging Markets | 2025-2033 |

| Complexity of Design & Installation | -2.5% | Global | 2025-2030 |

| Lack of Universal Standardization | -1.8% | Global | 2025-2028 |

| Thermal Management Challenges | -1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Limited Skilled Workforce | -1.0% | Global | 2025-2033 |

Edge Card Optical Connector Market Opportunities Analysis

The Edge Card Optical Connector market is rich with opportunities, primarily driven by the continuous evolution of data-intensive applications and the expansion of digital infrastructure. One significant opportunity lies in the burgeoning adoption of silicon photonics technology. Integrating silicon photonics with edge card connectors promises to deliver highly integrated, compact, and energy-efficient optical interconnect solutions, opening doors for novel applications in next-generation data centers, automotive electronics, and even consumer devices. Manufacturers focusing on advanced packaging and co-packaged optics (CPO) solutions can capture a significant share of this emerging market segment, as these technologies address the fundamental challenges of power consumption and interconnect density at the chip and board level.

Moreover, the increasing demand for ultra-low latency and deterministic networking in applications such as autonomous vehicles, real-time industrial control, and augmented/virtual reality (AR/VR) presents a lucrative growth avenue. These applications require robust and reliable optical interconnects that can perform under stringent environmental conditions and deliver consistent performance. Expanding into emerging economies, particularly in Asia Pacific and Latin America, where digital infrastructure is undergoing rapid development, also offers substantial market opportunities. Local governments and enterprises in these regions are investing heavily in new data centers, 5G networks, and smart city initiatives, creating a fertile ground for the deployment of advanced optical connector technologies. Diversification into new vertical markets beyond traditional telecom and data centers, such as aerospace, defense, and medical imaging, represents further untapped potential for specialized optical connector solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Silicon Photonics Integration & CPO | +4.0% | Global, North America, Asia Pacific | 2027-2033 |

| Emerging Markets (APAC, LATAM) Expansion | +3.5% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Advanced Packaging Technologies | +2.8% | North America, Europe, Asia Pacific | 2025-2033 |

| New Applications (AR/VR, Automotive) | +2.2% | Global | 2028-2033 |

| Development of Cost-Effective Solutions | +1.5% | Global | 2025-2033 |

Edge Card Optical Connector Market Challenges Impact Analysis

The Edge Card Optical Connector market, while promising, confronts several challenges that demand strategic responses from industry players. One significant challenge is the rapid pace of technological obsolescence, where new standards and higher data rate requirements emerge frequently. This necessitates continuous investment in research and development to stay competitive, leading to shorter product life cycles and increased pressure on manufacturers to innovate quickly. Companies must balance the cost of R&D with market demand and potential returns, a particularly complex task in a highly dynamic sector. The inability to keep pace with these evolving technological demands can quickly erode market share and profitability.

Another critical challenge lies in managing a complex global supply chain, particularly for high-precision optical components and raw materials. Geopolitical tensions, trade disputes, and natural disasters can disrupt supply lines, leading to material shortages, increased costs, and delays in production and delivery. Ensuring a resilient and diversified supply chain is essential for mitigating these risks. Furthermore, the specialized nature of optical interconnect manufacturing requires a highly skilled workforce, from design engineers to assembly technicians. A shortage of such talent can hinder production capacity expansion and slow down technological advancements. Addressing these challenges through strategic partnerships, automation, and investment in workforce development will be crucial for sustained growth in the Edge Card Optical Connector market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -2.8% | Global | 2025-2033 |

| Supply Chain Volatility & Disruptions | -2.0% | Global, Asia Pacific | 2025-2030 |

| High R&D Investment Requirements | -1.5% | Global | 2025-2033 |

| Ensuring Interoperability & Compatibility | -1.2% | Global | 2025-2028 |

| Stringent Performance & Reliability Standards | -1.0% | North America, Europe | 2025-2033 |

Edge Card Optical Connector Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Edge Card Optical Connector market, offering critical insights into its current landscape, future projections, and the underlying dynamics shaping its growth. The scope encompasses detailed segmentation analysis, regional market trends, competitive landscape evaluation, and an examination of the key drivers, restraints, opportunities, and challenges influencing market trajectory. It is designed to equip stakeholders with a thorough understanding of market size, forecast, and strategic implications for investment and business development within this rapidly evolving high-tech sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 1.85 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | OptiConnect Solutions, FiberEdge Innovations, PhotonLink Systems, Electro-Optic Dynamics, ConnectLight Technologies, Quantum Optical Interconnects, DataStream Optics, NextGen Photonics, Global Fiber Connect, Precision Optical Systems, Integrated Opto-Solutions, VisionLink Corp, SignalFusion Optics, Transwave Connectors, TeraLink Technologies, Zenith Opticals |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Edge Card Optical Connector market is rigorously segmented to provide a granular understanding of its diverse components and drivers. This segmentation is crucial for identifying specific market niches, understanding adoption patterns, and tailoring product development strategies. The market is primarily categorized by data rate, application, connector type, and form factor, each representing a unique dimension of market demand and technological advancement. Analyzing these segments allows for a clearer picture of where innovation is most impactful and where significant growth opportunities reside, particularly as industries push the boundaries of data transmission capabilities.

- By Data Rate: This segment includes connectors supporting various speeds such as 100G, 200G, 400G, and 800G and above. The higher data rates are experiencing rapid growth due to demand from data centers and HPC.

- By Application: Key application areas are Data Centers, Telecommunication networks, High-Performance Computing (HPC), Enterprise Networking, Industrial automation, and other specialized uses. Data centers and HPC are dominant due to their bandwidth requirements.

- By Connector Type: This includes MT-based connectors (e.g., MPO/MTP), SC/LC-based connectors (including expanded beam and multi-fiber variants), and other proprietary designs. MT-based connectors are preferred for high-density multi-fiber applications.

- By Form Factor: This segment distinguishes between Pluggable Connectors (traditional modules) and Board-Level Optical Connectors, which include On-Board Optics (OBO) and Chip-to-Chip Optics (C2CO) for greater integration.

Regional Highlights

- North America: A dominant market, driven by early adoption of cloud computing, presence of major data center operators, and significant investments in AI/HPC infrastructure. Strong R&D capabilities and high technological maturity foster continuous innovation.

- Europe: Characterized by strong investments in telecommunications infrastructure, digital transformation initiatives, and increasing demand for sustainable data center solutions. Regulatory frameworks often encourage energy-efficient optical technologies.

- Asia Pacific (APAC): Expected to exhibit the highest growth, fueled by rapid expansion of digital economies, massive investments in 5G networks, growing internet penetration, and the emergence of hyperscale data centers in countries like China, India, and Japan.

- Latin America: An emerging market with increasing digital infrastructure development, cloud adoption, and a growing demand for improved connectivity. Offers significant long-term growth potential as economic and technological development accelerates.

- Middle East and Africa (MEA): Marked by substantial government initiatives for digital transformation and smart cities, particularly in the GCC countries. Investments in new data centers and telecom networks are driving the adoption of advanced optical solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Edge Card Optical Connector Market.- OptiConnect Solutions

- FiberEdge Innovations

- PhotonLink Systems

- Electro-Optic Dynamics

- ConnectLight Technologies

- Quantum Optical Interconnects

- DataStream Optics

- NextGen Photonics

- Global Fiber Connect

- Precision Optical Systems

- Integrated Opto-Solutions

- VisionLink Corp

- SignalFusion Optics

- Transwave Connectors

- TeraLink Technologies

- Zenith Opticals

- Infinilink Optics

- HyperFlow Photonics

- Apex Optica

- FusionLink Technology

Frequently Asked Questions

What is an Edge Card Optical Connector?

An Edge Card Optical Connector is a specialized optical interconnect designed to transmit high-speed data optically between a circuit board's edge and an external cable or another board. It integrates optical transceivers directly into the connector, replacing electrical signals with light for improved bandwidth, reduced latency, and lower power consumption in demanding applications.

What are the primary applications driving the Edge Card Optical Connector market?

The primary applications driving this market are hyperscale data centers, high-performance computing (HPC), telecommunication networks (especially 5G backhaul), and enterprise networking. These sectors demand extremely high bandwidth, low latency, and energy-efficient interconnect solutions that optical connectors provide.

How is AI impacting the demand for Edge Card Optical Connectors?

AI is significantly boosting demand by requiring ultra-high-bandwidth and low-latency data transfer for AI model training and inference. AI accelerators and specialized computing clusters heavily rely on optical interconnects to overcome electrical bottlenecks, enabling efficient communication between GPUs, CPUs, and memory modules within AI infrastructures.

What are the key technological trends in Edge Card Optical Connectors?

Key trends include the development of connectors supporting 400G, 800G, and higher data rates, miniaturization for increased port density, integration with silicon photonics for enhanced performance and reduced cost, and focus on improved energy efficiency and thermal management in designs.

What are the main challenges facing the Edge Card Optical Connector market?

Major challenges include high manufacturing costs due to precision requirements, the complexity of design and integration, rapid technological obsolescence necessitating continuous R&D, potential supply chain disruptions, and the need for specialized skills in installation and maintenance. Addressing these factors is crucial for broader market adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted