E Health Market

E Health Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703446 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

E Health Market Size

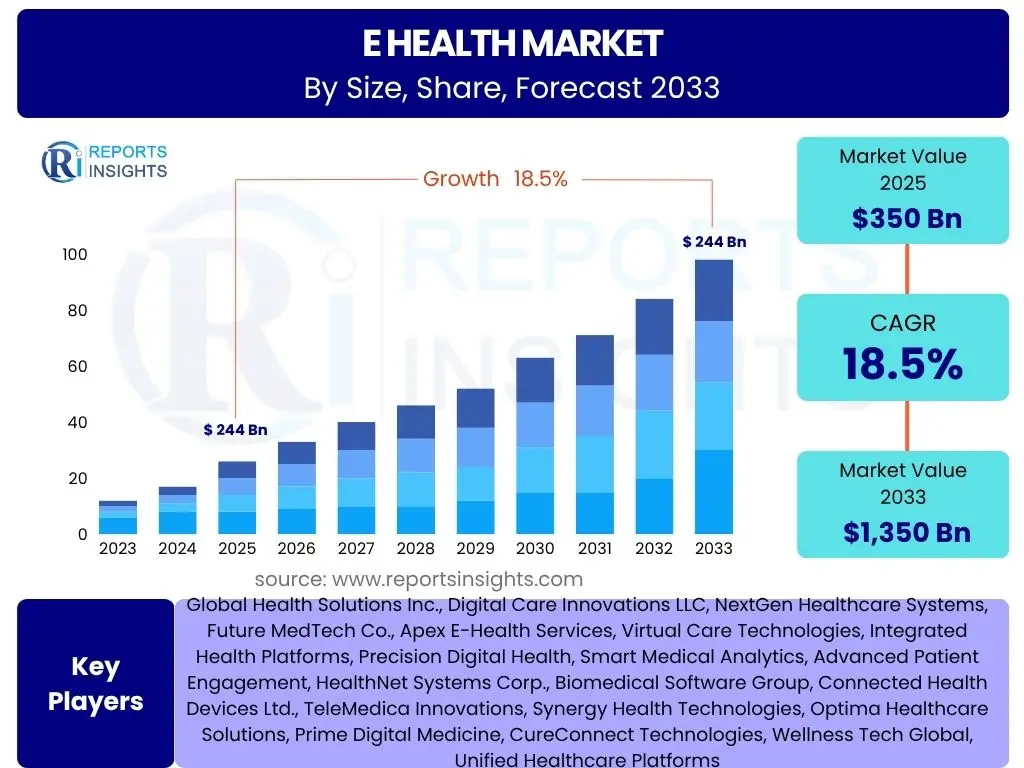

According to Reports Insights Consulting Pvt Ltd, The E Health Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 350 Billion in 2025 and is projected to reach USD 1,350 Billion by the end of the forecast period in 2033. This substantial growth trajectory is indicative of a profound transformation within the healthcare sector, driven by technological advancements and an increasing demand for more efficient, accessible, and personalized healthcare services. The market's expansion is fueled by a confluence of factors including the rising prevalence of chronic diseases, a global aging population, and the growing adoption of digital solutions to manage patient care and health information.

The shift towards preventive and proactive healthcare models further underpins the E Health market's robust expansion. Governments and private entities globally are investing heavily in digital health infrastructure to enhance healthcare delivery, reduce costs, and improve patient outcomes. This includes the widespread implementation of electronic health records, telehealth services, and remote patient monitoring systems. The COVID-19 pandemic significantly accelerated the adoption of E Health solutions, demonstrating their critical role in ensuring continuity of care and maintaining public health during crises, thereby setting a new baseline for market growth and innovation.

Key E Health Market Trends & Insights

Users frequently inquire about the evolving landscape of the E Health market, seeking to understand the significant shifts and innovations shaping its future. Common questions revolve around the adoption rates of new technologies, the integration of digital tools into clinical practice, and the implications for patient engagement and healthcare accessibility. The market is witnessing a profound transformation driven by consumer demand for convenience, the imperative for cost reduction, and advancements in data analytics, all converging to create a more interconnected and responsive healthcare ecosystem. These trends highlight a movement towards decentralized care and patient empowerment, fundamentally altering traditional healthcare delivery models.

Another area of strong user interest is the impact of regulatory frameworks and technological interoperability on market growth. Stakeholders are keen to understand how policies are adapting to accommodate rapid technological change and how seamless data exchange between disparate systems can be achieved. The emphasis is increasingly on creating holistic digital health platforms that can integrate various services, from telemedicine to remote monitoring, ensuring a cohesive and continuous patient care journey. This holistic approach is crucial for realizing the full potential of E Health and addressing complex healthcare challenges effectively.

- Increased adoption of telehealth and virtual care platforms due to enhanced convenience and accessibility.

- Proliferation of wearable devices and remote patient monitoring (RPM) solutions for continuous health tracking.

- Growing emphasis on personalized medicine through data analytics and AI-driven insights.

- Integration of blockchain technology for secure health data management and interoperability.

- Expansion of digital mental health services, addressing a critical and underserved area.

- Focus on preventive healthcare and wellness management through mobile health (mHealth) applications.

AI Impact Analysis on E Health

Users frequently express curiosity regarding the transformative potential of Artificial Intelligence (AI) within the E Health sector. Key inquiries often center on how AI can enhance diagnostic accuracy, personalize treatment plans, and streamline administrative processes, ultimately leading to improved patient outcomes and operational efficiencies. There is significant interest in AI's role in predictive analytics, enabling early detection of diseases and proactive interventions. The expectations are high for AI to revolutionize drug discovery, optimize clinical trials, and provide intelligent insights from vast quantities of healthcare data, thereby reducing costs and accelerating medical advancements.

Conversely, common concerns users raise about AI in E Health include issues of data privacy, algorithmic bias, and the ethical implications of autonomous decision-making in critical medical contexts. Questions arise about the reliability of AI models, the need for robust regulatory oversight, and the importance of maintaining human oversight in clinical settings. Addressing these concerns is paramount for building trust and ensuring the responsible deployment of AI technologies. The future integration of AI in E Health will require a careful balance between leveraging its immense potential and mitigating associated risks to ensure equitable and safe healthcare delivery.

- Enhanced diagnostic accuracy and early disease detection through AI-powered image analysis.

- Personalized treatment plans and drug discovery acceleration via AI-driven genomic analysis.

- Optimization of clinical workflows and administrative tasks, leading to operational cost reduction.

- Predictive analytics for patient deterioration, allowing proactive interventions and better resource allocation.

- Development of intelligent virtual assistants and chatbots for patient support and information.

- Improved data security and fraud detection through AI-driven anomaly recognition.

Key Takeaways E Health Market Size & Forecast

Users are keen to understand the pivotal insights derived from the E Health market size and forecast, particularly what the projected growth signifies for various stakeholders. Common inquiries focus on the segments expected to experience the most significant expansion, the geographic regions poised for rapid adoption, and the underlying technological shifts driving these trends. The overall takeaway indicates a resilient and rapidly expanding market, characterized by increasing investment in digital infrastructure and a widespread commitment to leveraging technology for better health outcomes. This growth is not merely incremental but represents a fundamental shift in how healthcare services are conceptualized and delivered globally.

Another crucial aspect users seek to comprehend is the long-term strategic implications for healthcare providers, technology developers, and policymakers. The forecast suggests a future where E Health solutions are not merely supplementary but become integral to the core fabric of healthcare, influencing everything from patient interaction to operational management. Key insights include the imperative for interoperability, the growing importance of cybersecurity, and the continuous need for innovation to meet evolving patient demands and clinical requirements. Understanding these dynamics is essential for any entity looking to capitalize on or adapt to the E Health revolution.

- The E Health market is experiencing robust, double-digit growth, driven by digital transformation in healthcare.

- Significant investment is flowing into telehealth, remote monitoring, and AI-driven diagnostic tools.

- North America and Europe currently lead the market, with Asia Pacific exhibiting the highest growth potential.

- Focus on preventative care, chronic disease management, and mental health services is propelling adoption.

- Interoperability and data security remain critical factors influencing market development and trust.

E Health Market Drivers Analysis

The E Health market is propelled by a multitude of factors that collectively foster its expansion and integration into mainstream healthcare. A primary driver is the escalating prevalence of chronic diseases globally, necessitating continuous monitoring and long-term care management that digital solutions can effectively support. This demographic shift, coupled with an aging population, places immense pressure on traditional healthcare systems, making E Health an indispensable tool for managing patient loads and improving efficiency. Additionally, the increasing demand for accessible and convenient healthcare services, especially in remote or underserved areas, strongly favors the adoption of telehealth and remote patient monitoring technologies.

Technological advancements also play a crucial role, with innovations in artificial intelligence, machine learning, and big data analytics enabling more personalized and predictive healthcare. Government initiatives and supportive regulatory frameworks across various regions are further accelerating market growth by promoting digital health adoption and encouraging investment in e-infrastructure. Furthermore, the rising penetration of smartphones and high-speed internet, alongside growing digital literacy among both patients and healthcare providers, provides a fertile ground for the widespread implementation and utilization of E Health solutions, thereby creating a robust demand ecosystem.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Chronic Diseases | +5.2% | Global, particularly North America, Europe | Long-term (2025-2033) |

| Aging Population and Burden on Healthcare Systems | +4.8% | Developed Economies (e.g., Japan, Germany, Italy, US) | Long-term (2025-2033) |

| Technological Advancements in AI, ML, IoT | +4.5% | Global, with strong adoption in US, China, Europe | Medium to Long-term (2025-2030) |

| Government Initiatives and Supportive Regulations | +3.9% | Specific Countries (e.g., US, UK, Canada, Australia) | Short to Medium-term (2025-2028) |

| Growing Demand for Convenient and Accessible Healthcare | +3.6% | Global, especially urban and remote areas | Medium to Long-term (2025-2033) |

E Health Market Restraints Analysis

Despite the promising growth trajectory, the E Health market faces several significant restraints that could impede its full potential. A primary concern is the inherent complexity and sensitivity of patient data, leading to substantial cybersecurity risks and privacy concerns. Breaches of health records can have severe consequences, undermining patient trust and exposing healthcare organizations to legal liabilities. This necessitates robust security infrastructure and strict compliance with evolving data protection regulations, which can be costly and challenging for providers to implement, especially smaller clinics or those in developing regions.

Another major restraint is the lack of interoperability between different E Health systems and platforms. Disparate systems, often developed by various vendors, struggle to communicate seamlessly, creating data silos and hindering comprehensive patient care coordination. This fragmentation can lead to inefficiencies, duplicate testing, and incomplete patient histories. Additionally, the high initial investment required for implementing advanced E Health solutions, coupled with ongoing maintenance costs, can be prohibitive for healthcare facilities with limited budgets. Furthermore, resistance from traditional healthcare professionals to adopt new technologies, often due to a lack of training or skepticism regarding efficacy, also acts as a significant barrier to widespread adoption and utilization of E Health services, requiring substantial efforts in change management and education.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -4.5% | Global, particularly regions with strict GDPR-like regulations | Long-term (2025-2033) |

| Lack of Interoperability and Data Silos | -3.8% | Global, prominent in fragmented healthcare systems | Long-term (2025-2033) |

| High Initial Investment and Infrastructure Costs | -3.2% | Developing and Emerging Economies | Medium-term (2025-2029) |

| Resistance to Change from Healthcare Professionals | -2.9% | Global, varying by organizational culture | Medium-term (2025-2029) |

E Health Market Opportunities Analysis

The E Health market presents numerous opportunities for growth and innovation, poised to capitalize on evolving healthcare needs and technological advancements. One significant opportunity lies in the untapped potential of emerging markets, particularly in Asia Pacific, Latin America, and Africa, where healthcare infrastructure is often underdeveloped and digital solutions can bridge critical access gaps. These regions offer vast populations with increasing digital literacy and a readiness to adopt cost-effective, scalable E Health services, driving demand for telehealth, mHealth, and remote monitoring solutions. Furthermore, the expansion into underserved rural areas globally presents a chance for providers to extend their reach and improve health equity through digital means.

The convergence of E Health with other cutting-edge technologies like the Internet of Medical Things (IoMT), advanced analytics, and personalized medicine offers fertile ground for product and service innovation. Developing integrated platforms that combine data from wearables, EHRs, and genetic information can lead to highly customized and predictive healthcare models. Additionally, the growing focus on mental health and wellness presents a burgeoning niche for specialized digital solutions, ranging from telepsychiatry platforms to AI-powered mental health applications. Strategic partnerships between technology companies, healthcare providers, and payers can further unlock these opportunities, fostering collaborative ecosystems that drive market expansion and enhance patient care delivery.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets and Rural Areas | +4.8% | Asia Pacific, Latin America, Africa | Long-term (2026-2033) |

| Integration with Internet of Medical Things (IoMT) and Wearables | +4.2% | Global, particularly North America, Europe, APAC | Medium to Long-term (2025-2032) |

| Growth in Personalized Medicine and Predictive Analytics | +3.9% | Developed Economies (e.g., US, UK, Germany) | Long-term (2027-2033) |

| Untapped Potential in Digital Mental Health Solutions | +3.5% | Global, driven by increasing awareness | Medium-term (2025-2030) |

E Health Market Challenges Impact Analysis

The E Health market, while dynamic and full of potential, faces several significant challenges that require strategic navigation. Cybersecurity threats, including data breaches and ransomware attacks, pose a constant and evolving risk to the highly sensitive patient information managed by E Health systems. The increasing sophistication of cyber adversaries necessitates continuous investment in advanced security measures, which can be a substantial burden for healthcare organizations. Moreover, maintaining compliance with diverse and frequently updating regulatory frameworks across different geographies adds another layer of complexity, demanding significant legal and technical expertise to avoid penalties and maintain operational integrity.

Beyond security and regulatory hurdles, ensuring equitable access and digital literacy across all demographics remains a critical challenge. A significant portion of the population, particularly the elderly or those in low-income areas, may lack the necessary digital skills or access to reliable internet connectivity and devices to fully utilize E Health services. This digital divide can exacerbate health disparities, counteracting the primary objective of improving access to care. Furthermore, managing the sheer volume and complexity of data generated by E Health systems, while ensuring its quality and interpretability for clinical decision-making, presents ongoing technical and analytical challenges. Addressing these multifaceted issues requires collaborative efforts from technology providers, healthcare institutions, policymakers, and communities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats and Data Breaches | -4.2% | Global, particularly developed regions with high digital adoption | Long-term (2025-2033) |

| Regulatory Compliance and Policy Fragmentation | -3.5% | Regions with complex regulatory landscapes (e.g., EU, US states) | Long-term (2025-2033) |

| Digital Divide and Lack of Patient Digital Literacy | -3.0% | Developing Countries, Rural Areas, Elderly Populations | Long-term (2025-2033) |

| High Cost of Implementation and Maintenance | -2.7% | Small Clinics, Public Hospitals, Low-Resource Settings | Medium-term (2025-2029) |

E Health Market - Updated Report Scope

This comprehensive market research report on the E Health market provides an in-depth analysis of its current landscape, historical performance, and future growth projections. It delves into the critical drivers, restraints, opportunities, and challenges shaping the industry, offering a holistic view for strategic decision-making. The scope encompasses detailed segmentation analysis by various components, applications, end-use sectors, and delivery models, providing granular insights into market dynamics. Furthermore, the report offers a thorough regional analysis, highlighting key country-level trends and growth prospects, alongside profiles of leading market participants to provide a competitive overview.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 350 Billion |

| Market Forecast in 2033 | USD 1,350 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Health Solutions Inc., Digital Care Innovations LLC, NextGen Healthcare Systems, Future MedTech Co., Apex E-Health Services, Virtual Care Technologies, Integrated Health Platforms, Precision Digital Health, Smart Medical Analytics, Advanced Patient Engagement, HealthNet Systems Corp., Biomedical Software Group, Connected Health Devices Ltd., TeleMedica Innovations, Synergy Health Technologies, Optima Healthcare Solutions, Prime Digital Medicine, CureConnect Technologies, Wellness Tech Global, Unified Healthcare Platforms |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The E Health market is extensively segmented to provide granular insights into its diverse components and applications, reflecting the varied needs and technological solutions within the healthcare ecosystem. These segmentations allow for a detailed examination of market performance across different product types, service offerings, deployment models, and end-user adoption patterns. Such a comprehensive breakdown helps stakeholders identify high-growth areas, understand specific market demands, and tailor strategies to capitalize on emerging opportunities. The structure of the market is complex, spanning software, hardware, and essential services that enable digital healthcare delivery across various settings.

Understanding these segments is crucial for accurate market forecasting and strategic planning. For instance, the growth in telemedicine is driven by the demand for accessible virtual consultations, while the rise of remote patient monitoring is linked to managing chronic conditions effectively at home. Similarly, the increasing adoption of cloud-based solutions over on-premise deployments reflects a broader trend towards scalable, flexible, and cost-efficient IT infrastructure. Each segment and subsegment contributes uniquely to the overall market trajectory, underscoring the multifaceted nature of the E Health industry and its continuous evolution.

- By Component:

- Software: EMR/EHR Systems, Telehealth Platforms, mHealth Apps, Remote Patient Monitoring Software, Clinical Decision Support Systems, Pharmacy Management Systems.

- Hardware: Wearable Devices, Medical Devices (connected), Kiosks, Servers, Communication Devices.

- Services: Consulting, Integration & Implementation, Maintenance & Support, Training & Education.

- By Application:

- Telemedicine (Teleconsultation, Teleradiology, Telemonitoring, Telepharmacy).

- Remote Patient Monitoring (RPM).

- Electronic Health Records (EHRs)/Electronic Medical Records (EMRs).

- Electronic Prescribing (e-Prescribing).

- Health Information Exchange (HIE).

- Wellness Management (Fitness, Nutrition, Stress Management).

- Clinical Workflow Management.

- Population Health Management.

- By End-Use:

- Hospitals.

- Clinics.

- Ambulatory Surgical Centers.

- Homecare Settings.

- Payers.

- Employers.

- Pharmacies.

- Diagnostic Centers.

- By Delivery Model:

- On-Premise.

- Cloud-Based.

Regional Highlights

- North America: Dominates the E Health market due to advanced healthcare infrastructure, high adoption of digital technologies, significant government funding for digital health initiatives, and the presence of numerous key market players. The United States accounts for the largest share, driven by a strong focus on value-based care and chronic disease management.

- Europe: Exhibits substantial growth, propelled by favorable government policies supporting digital health, increasing awareness regarding preventive healthcare, and a strong emphasis on data privacy and security. Countries like the UK, Germany, and France are leading in the implementation of national digital health strategies and cross-border data exchange initiatives.

- Asia Pacific (APAC): Expected to register the highest CAGR during the forecast period. This growth is attributed to the rapidly expanding healthcare expenditure, increasing internet penetration, rising population, and growing awareness of digital health benefits in emerging economies like China, India, and Japan. Government efforts to digitalize healthcare systems and address unmet medical needs in remote areas are key drivers.

- Latin America: Shows promising growth potential, driven by improving healthcare infrastructure, rising demand for affordable healthcare solutions, and increasing smartphone adoption. Brazil and Mexico are emerging as key markets within the region, with growing investments in telehealth and electronic health records.

- Middle East and Africa (MEA): Gradually adopting E Health solutions, primarily driven by government initiatives to diversify economies and improve healthcare access. Investments in smart city projects and digital infrastructure are creating opportunities for telehealth and mHealth, particularly in countries like UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the E Health Market.- Global Health Solutions Inc.

- Digital Care Innovations LLC

- NextGen Healthcare Systems

- Future MedTech Co.

- Apex E-Health Services

- Virtual Care Technologies

- Integrated Health Platforms

- Precision Digital Health

- Smart Medical Analytics

- Advanced Patient Engagement

- HealthNet Systems Corp.

- Biomedical Software Group

- Connected Health Devices Ltd.

- TeleMedica Innovations

- Synergy Health Technologies

- Optima Healthcare Solutions

- Prime Digital Medicine

- CureConnect Technologies

- Wellness Tech Global

- Unified Healthcare Platforms

Frequently Asked Questions

Analyze common user questions about the E Health market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is E Health?

E Health refers to the use of information and communication technologies (ICT) in healthcare, encompassing a wide range of services and systems such as electronic health records, telemedicine, mobile health applications, and health information exchanges. Its primary goal is to improve healthcare delivery, enhance patient care, and streamline administrative processes through digital means, making health services more accessible and efficient.

What are the primary benefits of E Health?

The main benefits of E Health include increased accessibility to care, especially for remote populations, improved efficiency in healthcare operations, reduced healthcare costs through optimized resource allocation, and enhanced patient engagement in their own health management. It also facilitates better data management and sharing, leading to more informed clinical decisions and personalized treatment plans.

How is AI transforming the E Health market?

AI is profoundly transforming the E Health market by enabling advanced analytics for predictive diagnostics, personalizing treatment protocols based on individual patient data, automating administrative tasks, and accelerating drug discovery. AI-powered tools enhance clinical decision support, improve image analysis for radiology, and offer intelligent virtual assistance, leading to more precise and efficient healthcare interventions.

What are the key challenges facing E Health adoption?

Key challenges in E Health adoption include concerns around data security and patient privacy, the lack of interoperability between disparate systems, high initial investment costs for implementing new technologies, and resistance to change from traditional healthcare providers. Additionally, addressing the digital divide and ensuring equitable access to technology for all demographics remain significant hurdles.

Which regions are leading in E Health market growth?

North America currently leads the E Health market in terms of market size due to its robust digital infrastructure and high technology adoption rates. However, the Asia Pacific region is projected to exhibit the highest growth rate, driven by expanding healthcare expenditure, increasing digital literacy, and government initiatives aimed at digitalizing healthcare systems in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted