Ductile Iron Pipe Market

Ductile Iron Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710148 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

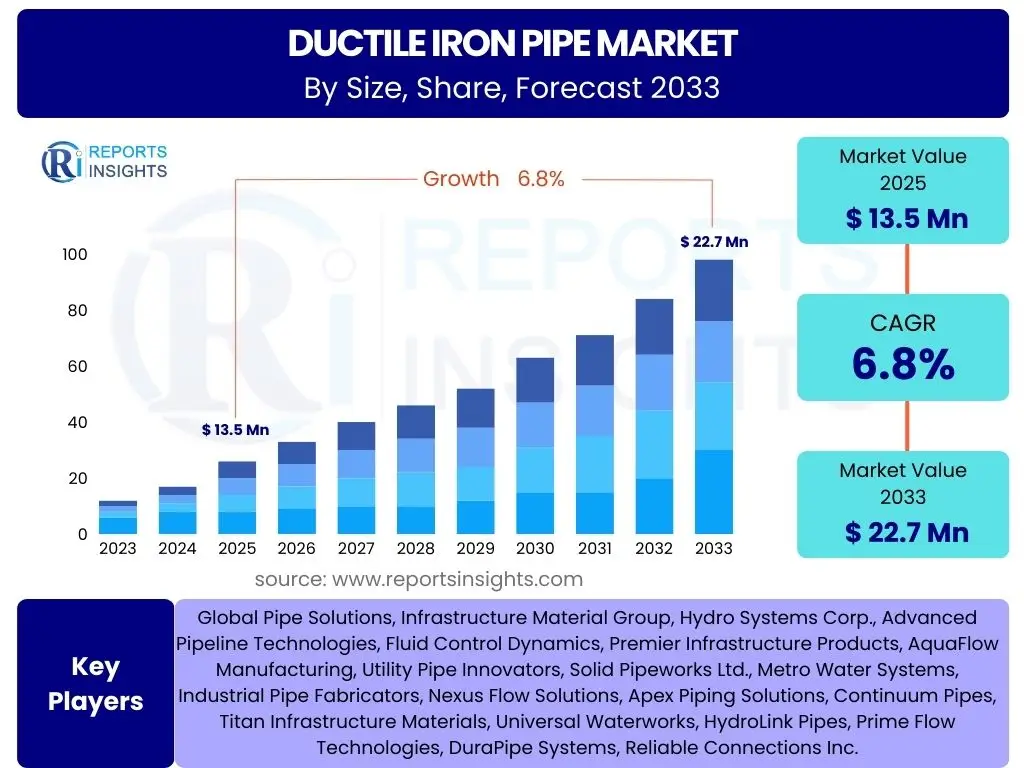

Ductile Iron Pipe Market Size

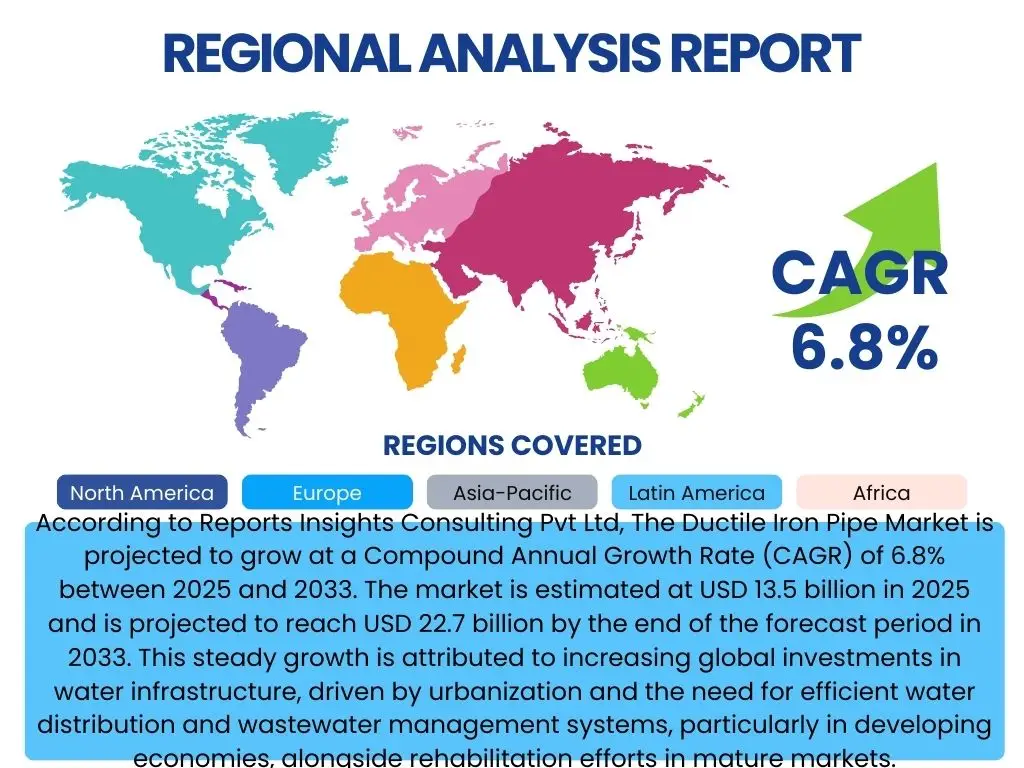

According to Reports Insights Consulting Pvt Ltd, The Ductile Iron Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 13.5 billion in 2025 and is projected to reach USD 22.7 billion by the end of the forecast period in 2033. This steady growth is attributed to increasing global investments in water infrastructure, driven by urbanization and the need for efficient water distribution and wastewater management systems, particularly in developing economies, alongside rehabilitation efforts in mature markets.

Key Ductile Iron Pipe Market Trends & Insights

The Ductile Iron Pipe market is currently shaped by several significant trends reflecting global shifts towards sustainable infrastructure, enhanced material performance, and improved project efficiency. Stakeholders are keenly focused on advancements in pipe coatings for increased longevity and corrosion resistance, the growing emphasis on smart water networks that integrate advanced sensor technologies, and the impact of environmental regulations pushing for more durable and recyclable materials. Additionally, the increasing complexity of urban infrastructure projects is driving demand for pipes that offer both strength and flexibility, alongside efficient installation methods.

Another prominent trend involves the strategic expansion into emerging economies where rapid urbanization and industrialization are creating substantial demand for new water and wastewater infrastructure. Manufacturers are also exploring opportunities in specialized applications, such as high-pressure systems and applications requiring enhanced seismic resilience. The market is also witnessing a gradual shift towards standardized, high-quality products that minimize leakage and reduce maintenance costs over their operational lifespan, contributing to a more resilient and sustainable global water supply.

- Global urbanization fueling demand for new water and wastewater infrastructure.

- Aging infrastructure replacement and rehabilitation initiatives in developed regions.

- Advancements in corrosion-resistant coatings and linings for extended pipe lifespan.

- Increased adoption of smart water management systems and digital integration.

- Growing emphasis on sustainable and recyclable materials in construction.

- Demand for larger diameter pipes for bulk water transmission projects.

- Technological innovations improving pipe manufacturing efficiency and quality.

- Focus on reducing non-revenue water through superior jointing and sealing technologies.

- Expansion into specialized applications such as seismic-resistant installations.

AI Impact Analysis on Ductile Iron Pipe

The integration of Artificial Intelligence (AI) into the Ductile Iron Pipe sector is increasingly viewed as a transformative force, with inquiries centering on its potential to optimize operations, enhance product quality, and revolutionize infrastructure management. Common discussions revolve around AI's capacity for predictive maintenance, allowing for early detection of potential failures in pipe networks, thus minimizing downtime and preventing catastrophic leaks. Furthermore, AI is expected to streamline manufacturing processes through advanced analytics, improving production efficiency, reducing waste, and ensuring higher product consistency. Its role in supply chain optimization, from raw material procurement to logistics and distribution, is also a significant area of interest, promising cost reductions and improved responsiveness.

Beyond operational efficiencies, AI’s impact is anticipated in the design and planning phases of water infrastructure projects. Generative design principles, supported by AI, could lead to more optimized pipe network layouts, considering factors like terrain, flow dynamics, and material stresses, thereby enhancing overall system performance and resilience. The deployment of AI-powered sensors in smart water grids will enable real-time monitoring of pipe conditions, leak detection, and pressure management, leading to more efficient water usage and reduced losses. Such innovations underscore AI's potential to drive a new era of intelligent, data-driven infrastructure management within the ductile iron pipe industry.

- Predictive maintenance for pipe networks, reducing failures and extending asset life.

- Optimized manufacturing processes through AI-driven analytics, enhancing efficiency and quality control.

- Supply chain optimization, improving logistics, inventory management, and material procurement.

- Enhanced design and planning of pipe networks using AI for optimal routing and system resilience.

- Real-time leak detection and pressure management in smart water grids through AI-powered sensors.

- Automated inspection and quality assurance, ensuring product consistency and adherence to standards.

- Improved resource allocation and project management for infrastructure development.

Key Takeaways Ductile Iron Pipe Market Size & Forecast

The Ductile Iron Pipe market's trajectory indicates robust growth, primarily driven by critical global infrastructure needs. Key insights reveal that the market's expansion is intrinsically linked to rising urbanization and industrialization, necessitating significant investments in reliable water and wastewater systems. The enduring attributes of ductile iron pipes, such as their strength, durability, and corrosion resistance, continue to position them as a preferred choice over alternative materials, particularly for long-term infrastructure projects. The market forecast highlights sustained demand from both developed regions focused on upgrading aging systems and emerging economies focused on building new infrastructure from the ground up.

Furthermore, technological advancements in pipe coatings, jointing methods, and manufacturing processes are contributing to increased market penetration and operational efficiency. The emphasis on water conservation and the reduction of non-revenue water losses are also critical factors propelling the adoption of high-performance ductile iron pipes. Stakeholders should note the increasing regional disparities in demand, with Asia Pacific and parts of Latin America showing accelerated growth due to rapid development, while North America and Europe focus on maintenance, replacement, and smart system integration. The market's resilience against economic fluctuations, given the essential nature of its applications, further solidifies its long-term growth outlook.

- Consistent growth trajectory, projected to reach USD 22.7 billion by 2033, driven by essential infrastructure needs.

- Urbanization and industrial development are primary demand generators, especially in emerging markets.

- Strong preference for ductile iron pipes due to superior strength, durability, and extended lifespan.

- Technological innovations in coatings and jointing enhancing product performance and reducing leakage.

- Significant investments in water and wastewater infrastructure globally.

- Asia Pacific leading in market growth due to rapid economic development and population increase.

- Emphasis on reducing non-revenue water and improving water utility efficiency.

- Replacement of aging infrastructure in developed regions remains a key demand driver.

Ductile Iron Pipe Market Drivers Analysis

The global Ductile Iron Pipe market is significantly propelled by substantial governmental and private sector investments in water infrastructure, particularly in regions experiencing rapid population growth and urbanization. As cities expand and existing infrastructure ages, there is an escalating need for efficient and resilient water supply and wastewater management systems. Ductile iron pipes, with their proven strength, durability, and longevity, are frequently chosen for these critical applications, ensuring reliable delivery of potable water and effective sewage disposal. The increasing awareness regarding water conservation and the imperative to reduce water losses from leakages further drives the adoption of high-quality, leak-proof piping solutions, where ductile iron excels.

Beyond municipal applications, the industrial sector's continuous demand for robust piping systems to transport water, chemicals, and industrial effluents also acts as a key market driver. Developing economies, in particular, are witnessing unprecedented infrastructure development, from new residential complexes to expansive industrial zones, all requiring extensive piping networks. This global trend towards upgrading and expanding essential utilities creates a sustained demand for ductile iron pipes, cementing their position as a fundamental component in modern infrastructure projects. Furthermore, the push for sustainable infrastructure and the circular economy principles favor ductile iron pipes due to their recyclability and long service life, aligning with contemporary environmental goals.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Urbanization and Population Growth | +1.8% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Increased Investment in Water & Wastewater Infrastructure | +1.5% | Global, particularly North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Replacement of Aging Infrastructure | +1.2% | North America, Europe, Japan | Long-term (2025-2033) |

| Industrial Expansion and Demand for Utility Pipes | +1.0% | China, India, Southeast Asia | Mid to Long-term (2025-2033) |

| Emphasis on Water Conservation and Leakage Reduction | +0.8% | Global | Mid to Long-term (2025-2033) |

Ductile Iron Pipe Market Restraints Analysis

Despite its numerous advantages, the Ductile Iron Pipe market faces notable restraints that could temper its growth trajectory. One significant factor is the volatility in raw material prices, particularly iron ore and scrap steel. Fluctuations in these commodity markets directly impact production costs, which can translate into higher prices for the end-users, making ductile iron pipes less competitive against alternative materials. The energy-intensive nature of iron production also makes manufacturers vulnerable to rising energy costs, further adding to operational expenses and potentially affecting profit margins. This economic unpredictability can complicate long-term planning for both producers and large-scale infrastructure project developers.

Another key restraint is the strong competition from alternative pipe materials such as PVC, HDPE, and concrete pipes. While ductile iron offers superior strength and durability, alternative materials often present advantages in terms of lower initial cost, lighter weight for easier transport and installation, and specific resistance properties (e.g., chemical resistance of certain plastics). Project developers, especially in cost-sensitive markets or for less demanding applications, may opt for these alternatives. Furthermore, the relatively high initial installation cost of ductile iron pipes, including labor and specialized equipment, can be a deterrent, especially for smaller projects or in regions with limited financial resources for infrastructure development. Regulatory hurdles and environmental concerns related to mining and manufacturing processes also present ongoing challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Iron Ore, Scrap Steel) | -0.9% | Global | Short to Mid-term (2025-2029) |

| Competition from Alternative Pipe Materials (PVC, HDPE, Concrete) | -0.8% | Global | Long-term (2025-2033) |

| High Initial Installation and Transportation Costs | -0.7% | Developing Economies, Remote Regions | Long-term (2025-2033) |

| Strict Environmental Regulations and Manufacturing Compliance | -0.6% | Europe, North America | Long-term (2025-2033) |

| Skilled Labor Shortage for Installation and Maintenance | -0.5% | North America, Europe | Mid to Long-term (2025-2033) |

Ductile Iron Pipe Market Opportunities Analysis

The Ductile Iron Pipe market is poised for significant opportunities, primarily stemming from the global push towards smart city development and the increasing adoption of digital infrastructure. As urban areas evolve, the integration of advanced sensor technology and IoT solutions into water networks presents a substantial avenue for ductile iron pipe manufacturers to offer value-added products that are compatible with intelligent monitoring systems. This trend allows for enhanced leak detection, pressure management, and predictive maintenance, thereby improving the overall efficiency and resilience of water distribution. Furthermore, the growing focus on sustainable water management practices and the circular economy positions ductile iron pipes favorably due to their high recyclability and long service life, aligning with environmental objectives of governments and utilities worldwide.

Another major opportunity lies in the expanding demand for robust infrastructure in rural and underserved areas, particularly in emerging economies. Governments are increasingly investing in extending water supply and sanitation networks to remote populations, where the durability and ease of installation of ductile iron pipes make them an ideal choice for challenging terrains and conditions. The development of trenchless technology for pipe installation and rehabilitation also opens new markets, allowing for efficient repair and replacement of existing pipelines with minimal disruption to urban environments. Innovation in advanced coatings and linings that offer superior corrosion resistance and extend product lifespan will further enhance the competitiveness of ductile iron pipes, catering to specialized applications and improving their economic viability over time.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Smart City Initiatives and Digital Water Infrastructure | +1.3% | Global, especially North America, Europe, Asia Pacific | Mid to Long-term (2025-2033) |

| Expansion of Water and Sanitation Networks in Rural Areas | +1.1% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Advancements in Trenchless Installation Technologies | +0.9% | North America, Europe | Mid to Long-term (2025-2033) |

| Demand for Advanced Coatings and Linings for Corrosion Resistance | +0.8% | Global | Mid to Long-term (2025-2033) |

| Sustainable Development Goals (SDGs) Driving Water Infrastructure Development | +0.7% | Global | Long-term (2025-2033) |

Ductile Iron Pipe Market Challenges Impact Analysis

The Ductile Iron Pipe market faces several persistent challenges that could impede its growth and operational efficiency. One significant challenge is the increasing stringency of environmental regulations, particularly concerning carbon emissions and waste management in the manufacturing process. Adhering to these evolving standards often requires substantial investments in new technologies and processes, which can increase production costs and complexity. Furthermore, the industry grapples with the global supply chain disruptions, which have become more frequent due to geopolitical tensions, natural disasters, and pandemics. These disruptions can lead to delays in raw material procurement, manufacturing, and delivery, impacting project timelines and increasing overall costs for end-users.

Another critical challenge is the shortage of skilled labor required for the specialized installation and maintenance of ductile iron pipe networks. As experienced workers retire, there is a growing gap in the workforce, particularly for complex projects that demand precise engineering and execution. This scarcity can lead to higher labor costs, delays, and potentially compromise the quality of installations. Moreover, the economic pressure to reduce infrastructure project costs often puts ductile iron pipes, which may have a higher initial material cost than some alternatives, at a disadvantage. Navigating these financial constraints while maintaining high-quality standards and meeting project deadlines remains a crucial balancing act for market participants, compelling innovation in cost-effective manufacturing and installation methods.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Carbon Footprint Reduction | -0.8% | Europe, North America, Japan | Long-term (2025-2033) |

| Global Supply Chain Disruptions and Logistics Volatility | -0.7% | Global | Short to Mid-term (2025-2029) |

| Shortage of Skilled Labor for Installation and Maintenance | -0.6% | North America, Europe | Mid to Long-term (2025-2033) |

| High Capital Expenditure for Manufacturing Upgrades | -0.5% | Global | Mid to Long-term (2025-2033) |

| Funding Limitations and Budgetary Constraints for Infrastructure Projects | -0.4% | Developing Economies | Long-term (2025-2033) |

Ductile Iron Pipe Market - Updated Report Scope

This report provides a comprehensive analysis of the global Ductile Iron Pipe market, offering detailed insights into market dynamics, segmentation, and regional trends. It covers the period from 2019 to 2033, with a specific focus on the forecast period from 2025 to 2033. The scope includes an examination of market size, growth drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. Special attention is given to the impact of emerging technologies and sustainability initiatives on market evolution, helping stakeholders make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 22.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Pipe Solutions, Infrastructure Material Group, Hydro Systems Corp., Advanced Pipeline Technologies, Fluid Control Dynamics, Premier Infrastructure Products, AquaFlow Manufacturing, Utility Pipe Innovators, Solid Pipeworks Ltd., Metro Water Systems, Industrial Pipe Fabricators, Nexus Flow Solutions, Apex Piping Solutions, Continuum Pipes, Titan Infrastructure Materials, Universal Waterworks, HydroLink Pipes, Prime Flow Technologies, DuraPipe Systems, Reliable Connections Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ductile Iron Pipe market is comprehensively segmented to provide granular insights into its diverse applications and product specifications. This segmentation allows for a detailed understanding of demand patterns across various diameters, catering to different flow requirements and project scales, from small-scale municipal connections to large-scale bulk water transmission lines. Furthermore, the classification by application highlights the pipe's utility in essential services like potable water distribution and wastewater management, alongside its crucial role in industrial processes and irrigation. The end-use industry segmentation differentiates demand from public utilities, private industrial entities, and commercial/residential developments, reflecting varying project priorities and procurement strategies. Lastly, segmentation by coating type underscores the importance of corrosion resistance and longevity, with different coatings offering tailored solutions for diverse environmental conditions.

Analyzing these segments provides strategic clarity for market participants, enabling them to identify niche opportunities and tailor their product offerings to specific market needs. For instance, the growing demand for large diameter pipes in major infrastructure projects in emerging economies contrasts with the continuous replacement of smaller diameter pipes in aging networks of developed regions. Similarly, advancements in internal linings are crucial for potable water applications, while external coatings are vital for pipes laid in corrosive soils. This multi-faceted segmentation elucidates the market's complexity and the factors driving preferences for specific ductile iron pipe products across the globe.

- By Diameter: DN 80-300mm, DN 300-600mm, DN 600-1000mm, Above DN 1000mm

- By Application: Potable Water Distribution, Wastewater & Sewage Systems, Irrigation, Industrial Applications, Others

- By End-Use Industry: Municipal, Industrial, Commercial, Residential

- By Coating Type: Cement Mortar Lining, Zinc Coating, Epoxy Coating, Polyurethane Coating, Bituminous Coating

Regional Highlights

- North America: Characterized by significant investments in replacing aging water infrastructure and upgrading existing networks. Demand is driven by municipalities aiming to reduce water losses and improve system resilience.

- Europe: Focuses on modernizing urban water supply systems, adhering to stringent environmental regulations, and implementing smart water technologies. Germany, France, and the UK are key markets for rehabilitation projects.

- Asia Pacific (APAC): Exhibits the highest growth potential due to rapid urbanization, industrialization, and extensive government spending on new infrastructure development in countries like China, India, and Southeast Asian nations.

- Latin America: Experiences steady growth propelled by efforts to expand access to clean water and sanitation, particularly in developing urban and rural areas, supported by international funding and national initiatives.

- Middle East and Africa (MEA): Driven by large-scale infrastructure projects, including new city developments, desalination plant connections, and agricultural irrigation systems, responding to population growth and water scarcity challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ductile Iron Pipe Market.- Global Pipe Solutions

- Infrastructure Material Group

- Hydro Systems Corp.

- Advanced Pipeline Technologies

- Fluid Control Dynamics

- Premier Infrastructure Products

- AquaFlow Manufacturing

- Utility Pipe Innovators

- Solid Pipeworks Ltd.

- Metro Water Systems

- Industrial Pipe Fabricators

- Nexus Flow Solutions

- Apex Piping Solutions

- Continuum Pipes

- Titan Infrastructure Materials

- Universal Waterworks

- HydroLink Pipes

- Prime Flow Technologies

- DuraPipe Systems

- Reliable Connections Inc.

Frequently Asked Questions

What is a Ductile Iron Pipe?

A ductile iron pipe is a robust, cast iron product treated to enhance its ductility, meaning it can deform under tensile stress without fracturing. It is widely used for water distribution, wastewater, and sewage systems due to its high strength, durability, corrosion resistance, and ability to withstand high internal pressures and external loads.

Why is Ductile Iron Pipe preferred over other materials?

Ductile iron pipes are preferred for their superior mechanical properties, including high tensile strength, impact resistance, and long service life of typically 100 years or more. They offer excellent leak-tightness with various jointing systems and are less susceptible to damage during handling and installation compared to brittle alternatives. Its recyclability and long-term cost-effectiveness further enhance its preference.

What are the primary applications of Ductile Iron Pipes?

The primary applications include municipal water supply and distribution networks, wastewater collection and sewage systems, industrial water lines and process piping, and large-scale irrigation projects. They are also utilized in fire protection systems and for transporting various liquids under pressure in critical infrastructure.

What factors are driving the growth of the Ductile Iron Pipe market?

Key growth drivers include rapid global urbanization and population growth, increasing investments in water and wastewater infrastructure, the need to replace aging utility networks in developed regions, and stringent regulations aimed at reducing water leakage and improving water quality. Industrial expansion and the push for sustainable infrastructure also contribute significantly.

Which region is expected to lead the Ductile Iron Pipe market growth?

The Asia Pacific (APAC) region is projected to lead the market growth due to its extensive infrastructure development projects, rapid urbanization, industrialization, and large-scale government initiatives to expand water and sanitation access across countries like China, India, and Southeast Asian nations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted