Dry Film Photoresist Market

Dry Film Photoresist Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702886 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

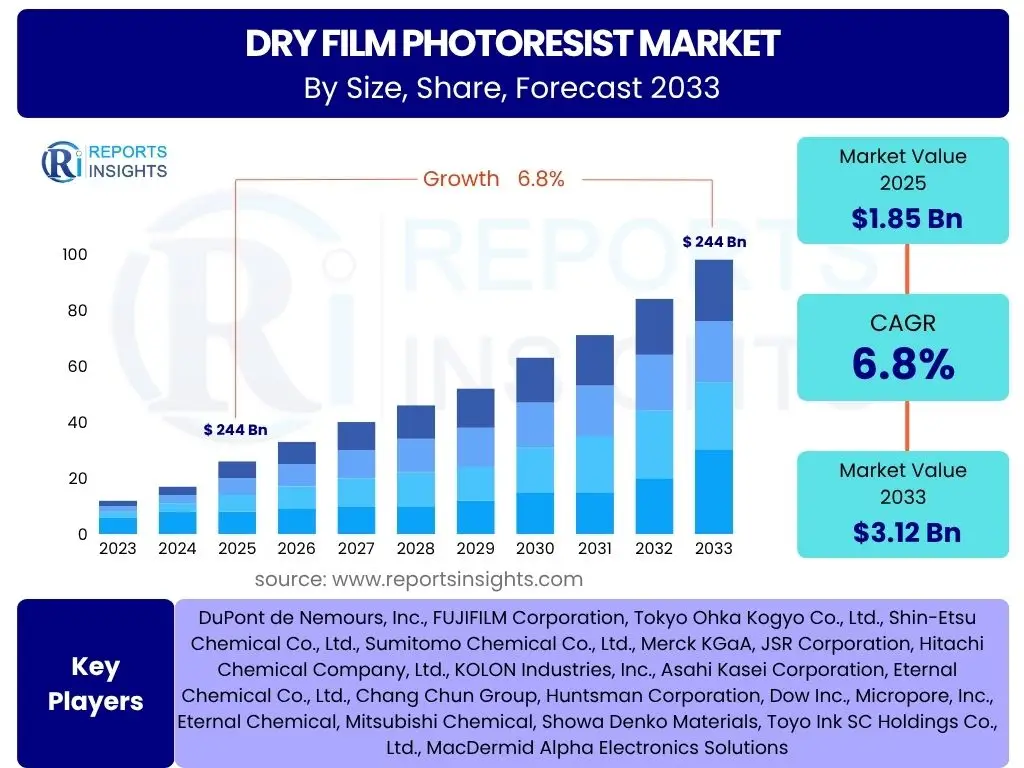

Dry Film Photoresist Market Size

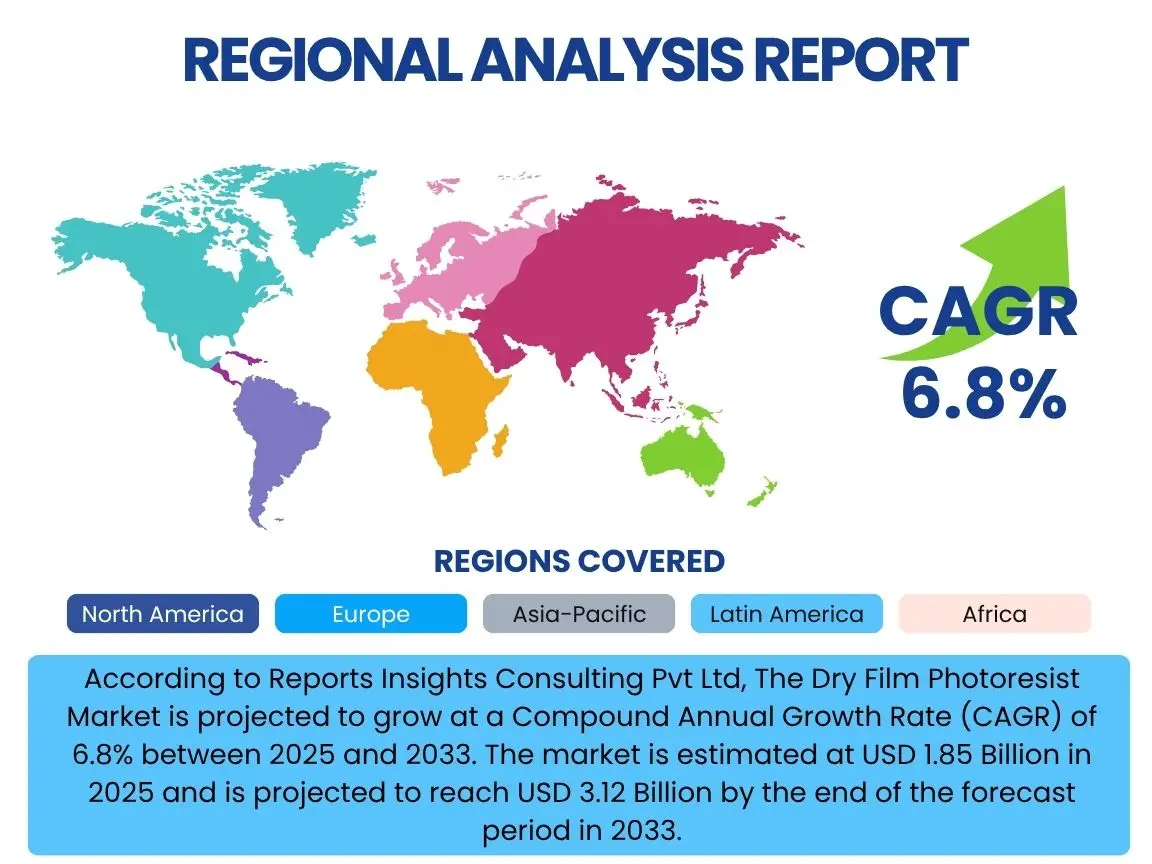

According to Reports Insights Consulting Pvt Ltd, The Dry Film Photoresist Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.12 Billion by the end of the forecast period in 2033.

Key Dry Film Photoresist Market Trends & Insights

The Dry Film Photoresist market is experiencing significant evolution driven by the relentless demand for miniaturization and enhanced performance in electronic components. Key trends indicate a strong push towards higher resolution capabilities, thinner film applications, and greater integration in advanced packaging technologies. Innovations in material science are also shaping the market, with a focus on developing photoresists that offer improved environmental profiles, better adhesion, and compatibility with diverse substrate materials, crucial for next-generation devices. Furthermore, the expansion of artificial intelligence, Internet of Things (IoT), and 5G technologies is creating new application frontiers, necessitating photoresists with superior precision and reliability.

This evolving landscape is leading to increased research and development investments aimed at addressing the complex requirements of advanced semiconductor manufacturing, including multi-layer patterning and finer line widths. The market is also seeing a shift towards more specialized photoresist formulations tailored for specific applications, such as microelectromechanical systems (MEMS), advanced displays, and flexible electronics. The emphasis on high-throughput processing and yield optimization further underlines the technical advancements and strategic directions within the dry film photoresist sector, ensuring its pivotal role in the future of electronics.

- Miniaturization in Semiconductor Devices and Printed Circuit Boards (PCBs)

- Rising Adoption of Advanced Packaging Technologies (e.g., Fan-out Wafer-Level Packaging, 3D ICs)

- Increasing Demand for High-Resolution and Fine-Line Patterning Capabilities

- Growing Integration in Flexible Electronics and Advanced Display Technologies (OLED, Micro-LED)

- Development of Environmentally Friendly and Low-VOC Photoresist Formulations

- Expansion of Internet of Things (IoT), Artificial Intelligence (AI), and 5G Infrastructure

- Increased Investment in Automotive Electronics and Autonomous Driving Systems

AI Impact Analysis on Dry Film Photoresist

The integration of Artificial Intelligence (AI) is set to significantly transform the Dry Film Photoresist market by enhancing various stages of the manufacturing process, from material design to quality control. AI algorithms can optimize photoresist formulations by simulating molecular interactions and predicting performance characteristics, drastically reducing the time and cost associated with traditional R&D cycles. Furthermore, AI-driven analytics enable precise process control in photolithography, allowing for real-time adjustments that improve yield rates and reduce defects, particularly critical for ultra-fine patterning in advanced semiconductor fabrication.

In manufacturing, AI and machine learning models are being deployed for predictive maintenance of lithography equipment, minimizing downtime and optimizing operational efficiency. These technologies can analyze vast datasets from production lines, identifying anomalies and potential failures before they occur, thereby ensuring consistent quality and throughput. The application of AI also extends to advanced defect inspection and classification, where AI-powered vision systems can identify microscopic flaws with greater accuracy and speed than human operators. This comprehensive impact of AI is expected to drive higher levels of automation, precision, and cost-effectiveness across the dry film photoresist ecosystem.

- Optimized Photoresist Formulation and Material Discovery through AI-driven Simulations

- Enhanced Process Control and Automation in Photolithography Manufacturing

- Predictive Maintenance for Lithography Equipment, Reducing Downtime and Improving Throughput

- AI-Powered Defect Inspection and Classification for Higher Yield Rates

- Data-Driven Yield Optimization and Quality Assurance in Production Lines

- Accelerated Research & Development Cycles for New Photoresist Chemistries

Key Takeaways Dry Film Photoresist Market Size & Forecast

The Dry Film Photoresist market is poised for substantial growth, driven primarily by the escalating demand for advanced electronic components across diverse industries. The forecast indicates a robust expansion, underscored by continuous technological advancements in semiconductor manufacturing and the proliferation of high-tech devices. This growth trajectory is also significantly influenced by the global shift towards smarter, more connected technologies, which require increasingly sophisticated and precise patterning solutions. The market’s resilience is further supported by ongoing innovation in materials and processes, enabling higher resolution and greater efficiency in production.

A significant takeaway is the pivotal role of Asia Pacific as the dominant region, propelled by its extensive electronics manufacturing base and rapid technological adoption. The market’s future is intrinsically linked to the evolution of integrated circuits, advanced packaging, and display technologies. Stakeholders must focus on strategic investments in R&D, sustainable manufacturing practices, and expanding their geographic footprint to capitalize on emerging opportunities. The competitive landscape will likely intensify, necessitating differentiation through specialized product offerings and strong customer partnerships to maintain market leadership and capture the forecasted growth.

- Consistent Growth Projected for the Dry Film Photoresist Market through 2033.

- Strong Demand Driven by Global Semiconductor and Advanced Electronics Manufacturing.

- Asia Pacific Region Expected to Remain the Largest and Fastest-Growing Market.

- Technological Advancements in Miniaturization and High-Resolution Patterning are Key Drivers.

- Emphasis on Environmentally Sustainable Photoresist Formulations is Increasing.

- Significant Opportunities Arising from IoT, AI, 5G, and Automotive Electronics.

Dry Film Photoresist Market Drivers Analysis

The Dry Film Photoresist market is propelled by several key drivers stemming from the rapid advancements and expanding applications within the electronics industry. The relentless pursuit of miniaturization in integrated circuits and printed circuit boards necessitates dry film photoresists that can achieve finer line widths and higher aspect ratios, directly boosting demand. Moreover, the surging global demand for consumer electronics such as smartphones, laptops, and wearables, along with the burgeoning market for advanced display technologies, provides a continuous impetus for market expansion. These applications rely heavily on high-precision patterning facilitated by advanced dry film photoresists, ensuring their critical role in the manufacturing ecosystem.

Another significant driver is the proliferation of advanced packaging technologies like wafer-level packaging (WLP), system-in-package (SiP), and 3D ICs. These technologies require sophisticated photoresist solutions to create complex, multi-layer interconnects with superior performance and reduced form factors. The growth of emerging technologies such as the Internet of Things (IoT), Artificial Intelligence (AI) devices, and 5G infrastructure further fuels the market, as these sectors demand robust and reliable electronic components. Furthermore, the automotive industry's increasing adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs) is generating substantial demand for high-reliability electronic components, indirectly driving the need for high-performance dry film photoresists in their manufacturing processes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of Electronic Components | +2.1% | Global, particularly Asia Pacific, North America | Short-term to Mid-term |

| Increasing Demand for Semiconductors | +1.9% | Global | Short-term to Mid-term |

| Growth in Advanced Packaging Technologies | +1.8% | Asia Pacific (Taiwan, South Korea), North America | Mid-term |

| Expansion of Consumer Electronics Market | +1.5% | Asia Pacific (China, India), Global | Short-term |

| Rising Adoption of IoT and AI Devices | +1.3% | Global, particularly Developed Economies | Mid-term to Long-term |

| Increasing Use in Automotive Electronics | +1.0% | Europe, North America, Asia Pacific | Mid-term to Long-term |

Dry Film Photoresist Market Restraints Analysis

Despite robust growth prospects, the Dry Film Photoresist market faces several restraints that could impede its expansion. One significant challenge is the high manufacturing cost associated with dry film photoresists, particularly for specialized formulations required for advanced applications. This cost factor can limit adoption, especially for smaller manufacturers or in price-sensitive emerging markets. Additionally, the complex and capital-intensive nature of photolithography equipment, which is essential for utilizing dry film photoresists, poses a barrier to entry and expansion for new market players, thereby concentrating market power among established entities.

Environmental concerns and stringent regulations pertaining to the disposal of chemical waste generated during photoresist processing represent another substantial restraint. As global environmental consciousness increases, companies face escalating pressure and costs to comply with environmental protection laws, influencing product development and manufacturing processes. Furthermore, volatility in raw material prices, particularly for key chemical components, can impact production costs and profit margins for photoresist manufacturers. The risk of technological obsolescence, driven by continuous innovation in alternative patterning techniques or the potential emergence of more cost-effective solutions, also presents a long-term challenge to the dry film photoresist market, necessitating constant research and development investment to remain competitive.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing and Processing Costs | -1.5% | Global | Short-term to Mid-term |

| Stringent Environmental Regulations | -1.2% | Europe, North America, Japan | Mid-term to Long-term |

| Volatility in Raw Material Prices | -1.0% | Global | Short-term |

| Technological Obsolescence Risk | -0.8% | Global | Long-term |

| Supply Chain Disruptions and Geopolitical Instability | -0.7% | Global | Short-term |

Dry Film Photoresist Market Opportunities Analysis

The Dry Film Photoresist market is ripe with opportunities driven by several emerging technological frontiers and evolving industrial demands. A significant opportunity lies in the development and adoption of eco-friendly photoresist formulations, including those with lower volatile organic compound (VOC) content or biodegradable properties. As industries increasingly prioritize sustainability and environmental compliance, companies offering greener solutions stand to gain a competitive advantage and capture a growing segment of environmentally conscious manufacturers. This push for sustainability aligns with global regulatory trends and consumer preferences, opening new market avenues.

Another compelling opportunity arises from the rapid expansion of flexible electronics and advanced display technologies, such as bendable smartphones, smart wearables, and large-area OLED displays. These applications demand specialized photoresists capable of precise patterning on flexible substrates, often requiring new material chemistries and processing techniques. Furthermore, the ongoing research into advanced chip architectures, including 3D ICs and heterogeneous integration, presents substantial opportunities for innovation in dry film photoresists that can facilitate complex multi-layer fabrication. Strategic collaborations between photoresist manufacturers and semiconductor foundries, as well as the exploration of new geographical markets with burgeoning electronics manufacturing bases, can further unlock significant growth potential for the dry film photoresist industry over the forecast period.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-friendly Photoresists | +1.6% | Global | Mid-term to Long-term |

| Expansion into Flexible Electronics and Advanced Displays | +1.5% | Asia Pacific, North America | Mid-term |

| Growing Demand for 3D ICs and Heterogeneous Integration | +1.4% | Global | Mid-term to Long-term |

| Emerging Markets in Southeast Asia and Latin America | +1.2% | Southeast Asia, Latin America | Mid-term |

| Strategic Partnerships and Collaborations | +1.0% | Global | Short-term to Mid-term |

Dry Film Photoresist Market Challenges Impact Analysis

The Dry Film Photoresist market faces several inherent challenges that can significantly influence its growth trajectory. Intense competition among established players, coupled with the entry of new specialized manufacturers, can lead to pricing pressures and reduced profit margins. This competitive landscape necessitates continuous innovation and differentiation, placing a heavy burden on research and development budgets. Furthermore, the highly capital-intensive nature of advanced photoresist manufacturing and the stringent quality control requirements for semiconductor applications pose significant hurdles, especially for smaller companies or new entrants, as high initial investments are required for state-of-the-art facilities and equipment.

Another critical challenge is the inherent complexity of achieving ultra-high resolution and precision patterning, especially as device dimensions continue to shrink. This requires not only advanced photoresist materials but also sophisticated lithography equipment and highly specialized process knowledge. Maintaining consistent product quality and performance across different batches and manufacturing sites also presents a formidable challenge, given the sensitivity of photoresist materials to environmental factors. Moreover, the global shortage of skilled labor, particularly in advanced materials science and semiconductor manufacturing, could impede the industry's ability to scale operations and innovate effectively, potentially leading to production bottlenecks and delayed market introduction of new solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pricing Pressures | -1.3% | Global | Short-term to Mid-term |

| Need for Continuous R&D Investment | -1.1% | Global | Mid-term to Long-term |

| Complexity of Ultra-High Resolution Patterning | -0.9% | Global | Mid-term to Long-term |

| Skilled Labor Shortage | -0.8% | North America, Europe, Japan | Mid-term |

| Intellectual Property Protection and Infringement Risks | -0.6% | Global | Long-term |

Dry Film Photoresist Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Dry Film Photoresist market, covering historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It also offers insights into the competitive landscape, profiling key market players and their strategic initiatives, to provide a holistic view of the industry. The report serves as a vital tool for stakeholders seeking to understand market trends, identify investment opportunities, and formulate effective business strategies within the global dry film photoresist sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.12 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DuPont de Nemours, Inc., FUJIFILM Corporation, Tokyo Ohka Kogyo Co., Ltd., Shin-Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., Merck KGaA, JSR Corporation, Hitachi Chemical Company, Ltd., KOLON Industries, Inc., Asahi Kasei Corporation, Eternal Chemical Co., Ltd., Chang Chun Group, Huntsman Corporation, Dow Inc., Micropore, Inc., Eternal Chemical, Mitsubishi Chemical, Showa Denko Materials, Toyo Ink SC Holdings Co., Ltd., MacDermid Alpha Electronics Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Dry Film Photoresist market is meticulously segmented to provide a granular understanding of its diverse components and their respective market dynamics. This segmentation facilitates detailed analysis of product types, their various applications, and the end-use industries driving demand. By categorizing the market based on these critical dimensions, stakeholders can gain insights into specific growth pockets, understand competitive nuances within sub-markets, and tailor their strategies to target particular consumer needs or industrial requirements. This structured approach allows for a comprehensive assessment of market opportunities and challenges across the entire value chain.

Each segment is influenced by unique technological requirements, regulatory frameworks, and market adoption rates, contributing differently to the overall market growth. For instance, the demand for specific photoresist types is often dictated by the precision and resolution needs of a particular application, while end-use industry growth is tied to broader economic and technological trends. The detailed analysis of these segments helps in identifying niche markets, assessing product penetration, and forecasting future demand patterns. This comprehensive segmentation ensures a thorough understanding of the Dry Film Photoresist market's complex structure and its future trajectory.

- By Type:

- Positive Tone Dry Film Photoresist

- Negative Tone Dry Film Photoresist

- Others

- By Application:

- Printed Circuit Boards (PCBs)

- Integrated Circuits (ICs)

- Microelectromechanical Systems (MEMS)

- Flat Panel Displays (FPDs)

- Advanced Packaging

- Others

- By End-Use Industry:

- Electronics

- Automotive

- Aerospace & Defense

- Medical

- Telecommunications

- Others

Regional Highlights

- Asia Pacific (APAC): Dominates the Dry Film Photoresist market due to the presence of major semiconductor manufacturing hubs, extensive consumer electronics production, and rapidly growing automotive and telecommunications industries in countries like China, South Korea, Taiwan, and Japan. This region is a global leader in both demand and supply of advanced electronic components.

- North America: Represents a significant market driven by robust research and development activities in advanced semiconductors, high adoption of cutting-edge technologies (AI, IoT), and a strong presence of aerospace and defense industries. The region focuses on high-value, specialized applications and continuous technological innovation.

- Europe: Characterized by a strong automotive sector, advanced industrial electronics, and a growing emphasis on smart manufacturing and sustainable practices. Countries like Germany, France, and the UK contribute significantly through their specialized electronics manufacturing and R&D initiatives.

- Latin America: An emerging market with growing electronics assembly and manufacturing capabilities, driven by increasing consumer demand for electronic devices and investments in automotive manufacturing. Brazil and Mexico are key contributors in this region.

- Middle East and Africa (MEA): A developing market with increasing investments in industrial infrastructure and telecommunications, leading to a gradual rise in demand for electronic components. While currently smaller, the region holds future growth potential as digitalization progresses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Dry Film Photoresist Market.- DuPont de Nemours, Inc.

- FUJIFILM Corporation

- Tokyo Ohka Kogyo Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Merck KGaA

- JSR Corporation

- Hitachi Chemical Company, Ltd.

- KOLON Industries, Inc.

- Asahi Kasei Corporation

- Eternal Chemical Co., Ltd.

- Chang Chun Group

- Huntsman Corporation

- Dow Inc.

- Micropore, Inc.

- Mitsubishi Chemical

- Showa Denko Materials

- Toyo Ink SC Holdings Co., Ltd.

- MacDermid Alpha Electronics Solutions

Frequently Asked Questions

What is Dry Film Photoresist?

Dry film photoresist is a light-sensitive polymer material supplied in solid film form, typically as a thin sheet, used in photolithography for etching patterns onto substrates. It offers high resolution, excellent adhesion, and uniform thickness, making it crucial for manufacturing printed circuit boards (PCBs), integrated circuits (ICs), and other microelectronic components.

Why is Dry Film Photoresist important in electronics manufacturing?

It is vital for enabling miniaturization and high-density circuitry in electronics. Its precise patterning capabilities allow for the creation of intricate designs on semiconductor wafers and PCBs, which are fundamental to the performance and functionality of modern electronic devices, including smartphones, computers, and advanced automotive systems.

What are the main applications of Dry Film Photoresist?

The primary applications include the fabrication of Printed Circuit Boards (PCBs), Integrated Circuits (ICs), Microelectromechanical Systems (MEMS), and Flat Panel Displays (FPDs). It is also extensively used in advanced packaging technologies and a growing range of specialized electronic components for industries like automotive and telecommunications.

What are the key market drivers for Dry Film Photoresist?

Key drivers include the global trend of miniaturization in electronic devices, the increasing demand for semiconductors, the rapid expansion of advanced packaging technologies, and the proliferation of consumer electronics, IoT devices, and 5G infrastructure. Growth in automotive electronics also significantly contributes to market expansion.

What is the market forecast for Dry Film Photoresist?

The Dry Film Photoresist market is projected to grow from USD 1.85 Billion in 2025 to USD 3.12 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period. This growth is driven by continuous technological advancements and rising demand in high-tech industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted